Introduction: Bridging the gap

The story of modern corporate governance in China is closely connected to the rapid evolution of its capital markets following the opening to the outside world in 1978. The 1980s brought the first issuance of shares by state-owned enterprises (SOEs) and a lively over-the-counter market. National stock markets were relaunched in Shanghai and Shenzhen in 1990 to 1991, while new guidance on the corporatisation and listing of SOEs was issued in 1992. The first overseas listing of a state enterprise came in October 1992 in New York, followed by the first SOE listing in Hong Kong in 1993. Corporate governance reform gained momentum in the late 1990s, but it was less a byproduct of the Asian Financial Crisis than a need to strengthen the governance of SOEs listing abroad. The early 2000s then brought a series of major reforms on independent directors, quarterly reporting and board governance aimed squarely at domestically listed firms.

A great deal has changed in China since then, with periods of intense policy focus on corporate governance followed by consolidation. In recent years, China’s equity market has undergone a renewed burst of internationalisation through Shanghai and Shenzhen Stock Connect, relaxed rules for Qualified Foreign Institutional Investors, and the landmark inclusion of 234 leading A shares in the MSCI Emerging Markets Index in June 2018. While capital controls and other restrictions on foreign investment remain, there seems little reason to doubt that foreign portfolio investment will play an increasing role in China’s public and private securities markets in the foreseeable future.

Running parallel to market internationalisation, and facilitated by it, is a broadening of the scope of corporate governance to include a focus on environmental and social factors (“ESG”), and a deepening concern about climate change and environmental sustainability. Pension funds and investment managers in China are now encouraged by the government to look closely at ESG risks and opportunities in their investment process. And green finance has become big business in China, with green bond issuance growing steadily. Indeed, these themes are also part of the newly revised Code of Corporate Governance for Listed Companies (2018) from the China Securities Regulatory Commission (CSRC); this is the first revision of the Code since 2002.

Turning point

China thus appears at a new turning point in its market development and application of corporate governance principles. While it is difficult to predict how this process will unfurl, we believe three broad developments would be beneficial:

-That unlisted and listed companies in China see corporate governance and ESG not merely as a compliance requirement, but as tools for enhancing organisational effectiveness and corporate performance over the longer term. This applies as much to entrepreneurial privately owned enterprises (POEs) as established SOEs. The view that good governance is not relevant or possible in young, innovative firms is misguided.

-That domestic institutional investors in China see corporate governance and ESG not only as tools for mitigating investment risk, but as a platform for enhancing the value of existing investments through active dialogue with investee companies. The process of engagement can also help investors differentiate between companies that take governance seriously and those which do not.

-That foreign institutional investors view corporate governance in China as something more nuanced than a division between “shareholder unfriendly” SOEs and “exciting but risky” POEs. We recommend foreign asset owners and managers spend more time on the ground in China and invest in studying China’s corporate governance system, if they are not already doing so.

Of course, there are many exceptions to these broad characterisations. It is possible to find companies which view governance as a learning journey—and they are not necessarily listed. Certain mainland asset managers have begun investigating how to integrate governance and ESG factors into their investment process. And there are a growing number of foreign investors, both boutique and mainstream, that have developed a deep understanding of the diversity among SOEs and POEs and which have achieved excellent investment returns from SOEs as well.

Not surprisingly, however, our research has found that significant gaps in communication and understanding do exist between foreign institutional investors and China listed companies. According to an original survey undertaken by ACGA for this report, a majority of foreign investor respondents (59%) admitted that they did not understand corporate governance in China. Only 10% answered in the affirmative, while another 31% felt they “somewhat” understood the system. Conversely, it appears that most China listed companies do not appreciate the challenges that foreign institutional investors face in navigating “corporate governance with Chinese characteristics”.

This report is written for both a domestic and international audience. Our aim is to describe in as fair and factual a manner as possible the system of corporate governance in China, highlighting what is unique, what looks the same but is different, and areas of genuine similarity with other major securities markets. The main part of the report focuses on “Chinese characteristics” and looks at the role of Party organisations/committees, the board of directors, supervisory boards, independent directors, SOEs vs POEs, and audit committees/auditing. Each chapter explains the current legal and regulatory basis for the governance institution described, the particular challenges that companies and investors face, and concludes with suggestions for next steps. Our intention has been to craft recommendations that are practical and anchored firmly in the current CG system in China—in other words, that are implementable by companies and institutional investors. We hope the suggestions, and indeed this report, will be viewed as a constructive contribution to the development of China’s capital market.

The remainder of this Introduction provides an overview of key macro results from our two surveys. We start with the good news—that a large proportion of foreign institutional investors and local companies are optimistic about China—then highlight the challenges both sides face in addressing governance issues. The following chapters draw upon additional material from the two surveys.

ACGA survey—The big picture

Are you optimistic?

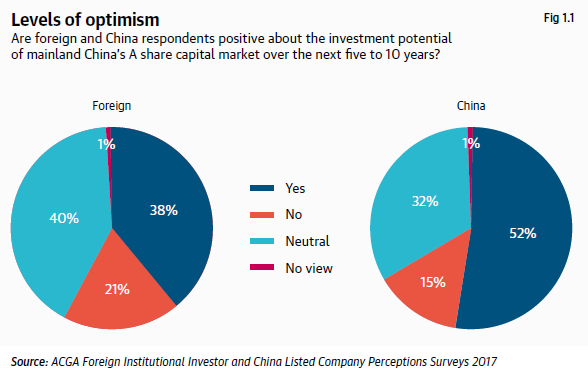

The good news from our survey is that a sizeable proportion of both foreign investors (38% of respondents) and China listed companies (52%) are optimistic about the investment potential of the A share market over the next five to 10 years, as Figure 1.1 below shows. Only 21% of foreign investors are negative, while the remainder are neutral. Not surprisingly, only 15% of China respondents were negative, while almost one-third were neutral.

Do you agree with MSCI?

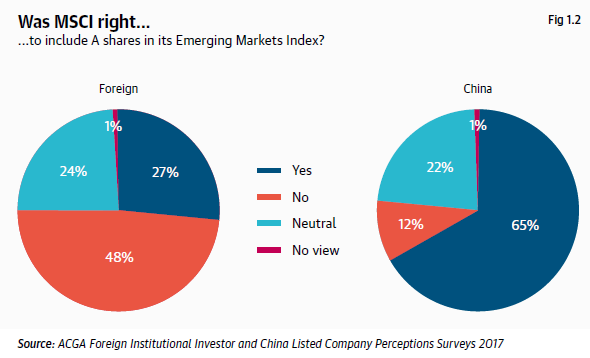

The picture diverges on the issue of whether MSCI was right to include A shares in its Emerging Markets Index in 2018: only 27% of foreign respondents agreed compared to 65% of Chinese respondents, as Figure 1.2, below, shows. Almost half the foreign respondents did not agree compared to a mere 12% for Chinese respondents. A similar proportion was neutral in both surveys.

Challenges—Foreign institutional investors

The investment process

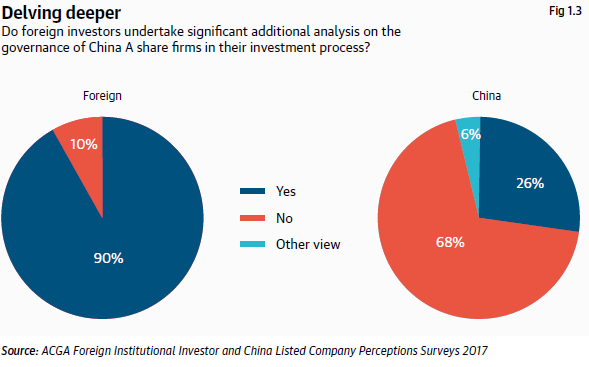

Foreign investors face a range of challenges investing in China, the first of which is understanding the companies in which they invest. As Figure 1.3 below indicates, foreign investors do not rely solely on information provided by companies when making investment decisions, but utilise a range of additional sources. It appears that listed companies are not aware of this issue.

Company engagement

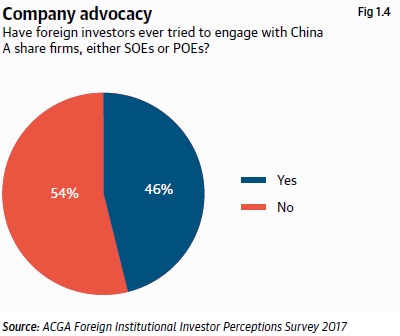

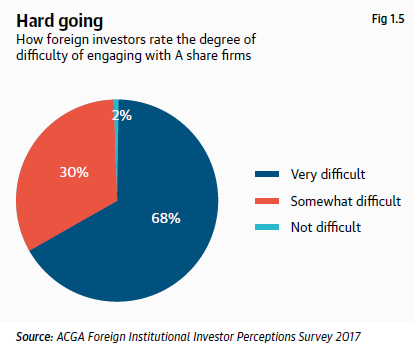

Globally, institutional investors seek to enter into dialogue with their investee companies. It is no different in China, as shown in Figure 1.4.

But the process is not easy.

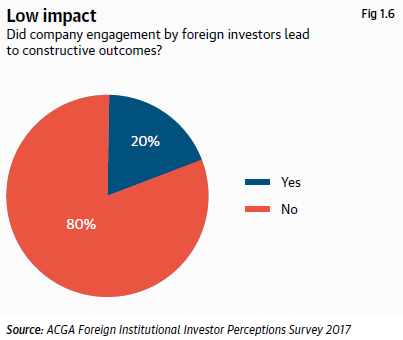

And successful outcomes are fairly thin on the ground to date.

Common threads

Respondents gave a range of answers as to why the process of engagement was difficult and successful outcomes limited, but some common threads were discernible:

Language and communication: In addition to straightforward linguistic difficulties (ie, companies not speaking English, investors not speaking Chinese), the communication problem is sometimes cultural. As one person said, “Even though I am from China, it is hard to interpret hidden messages.”

Access: Getting access to companies can be difficult. Getting to meet the right senior-level person, such as a director or executive, can be even more challenging.

Investor relations (IR): While some IR teams are professional, many are not. As one respondent commented: “IR (managers) are not very well trained and some of them lack basic understanding or knowledge of corporate governance or even financial information.”

CG as compliance: A common complaint is that companies view CG as merely a compliance exercise. Some refuse to give “detailed answers beyond the party line”.

Non-alignment: There is a recurring feeling that the interests of controlling shareholders in SOEs are not aligned with minority shareholders. One investor commented on the “lack of responsiveness” to outside shareholder suggestions, adding that SOEs “wait for government to give the direction, not investors”.

Lack of understanding: There can be a significant gap in the awareness of CG and ESG principles.

Empathy for companies

Conversely, a few respondents expressed empathy for the position of companies. As one wrote: “There also appears to be an under appreciation by international investors of the differences in culture, political context, and the path and stage of economic development between China and the rest of the world. Any attempt at influencing changes without a reasonable understanding of these differences is likely to be ineffective and (may) at times lead to unintended consequences.”

Another explained some of the regulatory challenges facing listed companies: “With a few exceptions, both SOEs and POEs have to deal with stringent and ever-changing industry regulations and government policies.”

A third said that some engagement had been positive: “Generally, where I have had access to the right people, engagement has been constructive. I suspect this is a result of the companies already appreciating the value of good governance in attracting non-domestic investors.”

And perhaps the most positive comment of all: “A number of the Chinese companies we speak to, especially the industry leaders, already address ESG risks in their businesses. Most of them publish ESG reports annually, which help to set the benchmark for their industry and also to garner positive feedback from society and hence, end-customers. Some of such companies end up enjoying a pricing premium on their products once this positive brand equity has been established. This creates a virtuous cycle, where ESG becomes part of their corporate culture. They understand that for the long-term sustainability of their business, and for the benefits of all their stakeholders, such investment can only enhance their competitiveness.”

Brave new world of stewardship

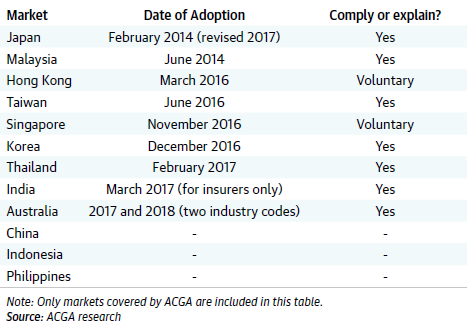

Yet most investors still find engaging with companies a challenge. A further reason may be that China is one of only three major markets in Asia-Pacific that has not yet issued an “investor stewardship code”. Such codes push institutional investors to take CG and ESG more seriously, incorporate these concepts into their investment process, and help to encourage greater dialogue between listed companies and their shareholders (see Table 1.1, below). In recent years, the bar has been quickly raised on this issue in Asia and expectations have risen commensurately.

Without an explicit policy driving investor stewardship, it is unlikely that the average listed company will give proper weight to a dialogue with shareholders. As one foreign investor said: “Generally speaking, it is relatively easier to engage with bigger listed companies. SOEs and larger companies tend to be more responsive. SOEs have more incentive to do so following government guidelines and trends.”

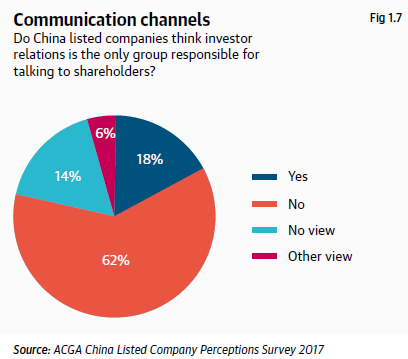

A key question to ask is who within a company should be responsible for engaging with shareholders? The short answer is the board, as a group representing and accountable to shareholders. Indeed, on a positive note, our survey found that most Chinese listed companies do admit that the responsibility for talking to shareholders should not be placed solely on the investor relations (IR) team (see Figure 1.7 below). But given that delegating this task to IR remains a common practice, it would appear that there is an inconsistency between words and actions here.