Aujourd’hui, j’aborde un sujet assez peu étudié par les experts en gouvernance, mais néanmoins crucial pour assurer le succès de la croissance des entreprises : Il s’agit de l’attention qu’il faut apporter à la reconstitution du nouveau conseil d’administration résultant de la fusion ou de l’acquisition de deux entités privées ou publiques.

La période de transition post-acquisition se traduit souvent par des gestes et des attitudes des CA qui les rendent moins efficaces, à une période nécessitant une surveillance accrue.

L’article publié par Johanne Bouchard* et Ken Smith** dans la revue NACD Directorship décrit quatre principales situations de M&A, en illustrant les difficultés de fonctionnement susceptibles d’être vécues à la suite de la recomposition des conseils d’administration.

C’est un article phare qui montre clairement la nécessité pour les nouvelles entités de se faire accompagner dans les périodes critiques du choix des membres, de l’induction des nouveaux membres et de la dynamique de la nouvelle équipe d’administrateurs.

Je vous invite à lire le document ci-dessous. En voici, quelques extraits :

The board may be least effective post-deal, at the very time when its oversight may be most important.

The proposed board composition wouldideally be part of the merger proposal put to shareholders for approval.

Many boards surprise themselves with what they didn’t know about each other… until they put these things on the table in the context of a big challenge such as an acquisition.

The organization structure and culture should be aligned with the overall strategy and facilitate the deal logic.

*Johanne Bouchard is an advisor to boards, CEOs, and executives. She is an expert in board composition and dynamics, and provides support in strategic alignment, board effectiveness, and post-deal board integration. Bouchard has been a serial entrepreneur and held C-level management positions at leading high-tech companies in Silicon Valley.

**Ken Smith has been a strategy consultant for more than 25 years, having served leading Canadian and U.S. corporations. He is an expert in M&A strategy and implementation, and co-wrote The Art of M&A Strategy (McGraw-Hill, 2012) with NACD Chief Knowledge Officer, Alexandra R. Lajoux.

Dans ce billet, je vous propose une courte lecture suggérée par Chantal Rassart, associée | Chef de la gestion des connaissances en audit, de la firme Deloitte. Dans le numéro d’avril, un aperçu des nouveautés dans le domaine de la gouvernance d’entreprise, Chantal Rassart présente le point de vue de Heather Stockton, associée | Consultation, sur l’amélioration des pratiques des comités de ressources humaines du CA eu égard aux défis posés par la gestion des talents.

L’auteure insiste surtout sur l’importance cruciale de la mise en place d’un plan de formation à l’intention des hauts dirigeants. Les études montrent que les entreprises qui ont misées à fond sur le perfectionnement des dirigeants ont obtenu une performance financière significativement supérieure aux entreprises qui ont négligé cette acticité de développement des talents.

L’article présente également cinq questions que les comités de ressources humaines du CA devraient poser relativement à la gestion des talents.

Quel est votre point de vue à ce propos ? Voici un extrait de l’article en question.

Bonne lecture !

Nos prédictions se sont concrétisées

En 2011, nous avions prédit que nous assisterions à une baisse de l’importance accordée à la rémunération des cadres et à la relève du PDG et à une augmentation de l’importance accordée aux objectifs à long terme des entreprises en matière de gestion des talents et de diversité. Ces prédictions se sont bel et bien concrétisées. Il suffit de jeter un coup d’œil à ce qui est publié ou de discuter avec des administrateurs d’entreprises de toutes tailles et formes juridiques pour constater la place importante qu’occupent maintenant le leadership des futurs dirigeants et les talents dans les activités de gouvernance et de surveillance des conseils d’administration. Alors que nos regards se tournent vers l’avenir, nous constatons que les organisations devront faire face à de nouveaux défis et on s’attend à ce que les conseils d’administration adoptent une approche différente en matière de surveillance afin de les aider à répondre aux attentes de plus en plus élevées des clients, à la concurrence de plus en plus féroce, aux innovations rapides et à l’évolution accélérée des technologies.

Impératif d’affaires

L’attention accrue portée au perfectionnement des dirigeants a des incidences concrètes sur les indicateurs clés de performance de toutes les fonctions de l’organisation. Les organisations qui comptent au sein de leur équipe des dirigeants « de grande qualité » sont 13 fois plus susceptibles de dépasser leurs concurrents sur le plan notamment de la performance financière, de la qualité des produits et des services et de la fidélisation et de la mobilisation du personnel.

Une autre étude récente a examiné la performance d’entreprises durant une décennie en fonction du niveau d’effort consacré au perfectionnement des dirigeants. Les entreprises se situant dans la tranche des 15 % ayant consacré le plus d’efforts au perfectionnement des dirigeants ont accru leur capitalisation boursière de 122 pour cent, tandis que celles se situant dans la tranche des 15 % ayant consacré le moins d’efforts n’ont accru leur capitalisation boursière que de 37 pour cent.

Questions que les comités des ressources humaines devraient se poser

À la lumière de tous ces changements et compte tenu du rôle clair que joue le perfectionnement des talents dans la croissance de l’entreprise, les conseils d’administration devraient examiner continuellement comment leur entreprise se positionne par rapport à ses concurrents sur le plan des talents et comment elle parvient à répondre aux priorités d’affaires tandis que la concurrence s’intensifie. Le comité des ressources humaines peut contribuer au changement pour aider les chefs de la direction et des ressources humaines à diriger leur entreprise vers l’avenir. Outre les questions liées à la rémunération des dirigeants et à la relève du chef de la direction, les comités des ressources humaines devraient poser les cinq questions clés suivantes à la direction :

Quelles qualités et connaissances les futurs hauts dirigeants et dirigeants actuels possèdent-ils? Dans quelle mesure sont-ils prêts à assumer la relève?

Avez-vous en place un plan transition pour préparer les futurs candidats au poste de chef de la direction d’ici la fin du processus de relève?

Le comité de gouvernance du conseil d’administration a-t-il passé en revue la composition du conseil à la lumière de la stratégie d’entreprise, de sa clientèle et des marchés dans lesquels l’entreprise évolue pour s’assurer que l’entreprise dispose des personnes adéquates pour diriger l’entreprise?

Le comité des ressources humaines du conseil d’administration a-t-il discuté de la stratégie relative au travail de l’avenir lorsqu’il a approuvé la stratégie à moyen et à long terme et de la façon dont celle-ci pourrait changer les besoins immobiliers futurs, la nature du travail de votre entreprise et la façon dont vous appuierez vos dirigeants et employés dans le futur?

Le comité des ressources humaines comprend-il les plans du chef des ressources humaines pour moderniser la fonction des ressources humaines et s’aligner sur le travail de l’avenir et votre stratégie d’affaires?

Si le chef de la direction et son équipe de direction ont une vision claire du « comment », vous avez alors les bons ingrédients pour continuer de vous démarquer de vos concurrents et d’obtenir des résultats durables. Une réponse négative à l’une des questions ci-dessus peut avoir une incidence sur la capacité de l’entreprise à atteindre les objectifs de sa stratégie d’affaires. Vos leaders et vos gens sont la seule chose que vos concurrents ne peuvent copier – tout le reste peut être automatisé, créé ou imité.

Un article deDavid Doughty* nous rappelle que l’importance accordée à la gouvernance des sociétés dans le monde est de plus en plus décisive et qu’il y a une demande croissante pour des administrateurs qualifiés, dans tous les types d’organisations : privées, publiques, sociétés d’état, familiales, OBNL, etc.

Cependant, la compétition pour l’obtention d’un poste d’administrateur indépendant est significativement plus forte qu’auparavant. On fait de plus en plus appel à des firmes spécialisée en recrutement d’administrateurs. Comment se démarquer des autres candidats dans ces circonstances ?

L’auteur met l’accent sur l’étendue des connaissances en gouvernance de sociétés requises et sur la quasi-nécessité d’acquérir une formation dans ce domaine comme facteur-clé de différentiation.

Son billet présente les diverses formations en gouvernance offertes au Royaume-Uni et il montre qu’il y a une grande variabilité dans les frais d’inscription.

Le tableau des cours illustre parfaitement cette grande variabilité mais, dans l’ensemble, les formations sont d’environ 1 500 $ par jour.

Vous trouverez, ci-dessous, une comparaison des coûts de la formation en gouvernance pour les trois (3) principaux programmes de référence au Canada. Veuillez noter que le coût total de la formation au Directors College inclus les frais d’hébergement.

Comparaisondestrois principaux programmes en gouvernance au Canada : Collège des administrateurs de sociétés (CAS), Institute of Corporate Directors (ICD), The Directors College (DC)

Programmes de référence Désignation (titre)

CAS (ASC)

ICD (IAS.A)

DC (C.Dir.)

Nombre d’heures de formation

125

96

125

Coût total de la formation pour l’obtention d’une désignation (taxes incluses)

Cet article a été publié sur le site de IT Business.ca en avril 2015. Son auteur, Gerard Buckley*, est un expert en gouvernance; il nous fait part de son expérience avec le fonctionnement des conseils d’administration et il nous présente les six éléments-clés qui contribuent à l’efficacité des CA. et qui constituent sa recette secrète.

Ce bref article est intéressant et il va directement au cœur de la question du succès des bons conseils.

« There are few experiences that can have such an extremely different outcome on the spectrum from total nightmare to self-fulfilling achievement, but sitting on a board of directors is one of those experiences. When one has the privilege to serve on a good board it is both a pleasant, educational, and a rewarding experience. When the opposite is true, it can be exacerbating, draining of energy, and very frustrating. I have personally enjoyed the former and attempted to turn around the latter with varying degrees of success. In this blog post, I would like to provide some of the characteristics I find to be common in a good board. »

Great leadership

In most organizations I have been a part of – whether it is a public corporation or the youth organizations I serve on the board of – I always find if there is strong leadership, it leads to a well-run company and a well-functioning board. With a confident and mature CEO there most often will be a strong lead director or chair of the board. Both of these positions must be filled with well-meaning and strong individuals of integral character. If not, the leadership on the board must be instrumental in weeding out unqualified board members and those board members who are disruptive unprepared. Some may need coaching and others may need to be plainly relieved of their board duties.

Diversity

A well-functioning board requires diversity of thought, experience, gender, and culture. If all of the board members think and act alike, their decisions will reflect their lack of diversity. I don’t only mean culture and gender. Well run boards also reflect diversity of age, experience, and industry that include complementary skills such as risk management, channel distribution, sales, marketing, human resources, compensation, information technology, finance, fundraising, and industry vertical knowledge. A board needs to be clear about duties, roles and responsibilities of it’s directors in the recruiting process to ensure that applicants expectations and the company are aligned.

Directors who leave their egos at the door

When a board consists of directors who have the company or organization foremost in their minds and feel they don’t have to prove themselves most often make the best contribution to the company. These characteristics are most often present in confident, seasoned executives who have accumulated several years of board experience. All directors need to have their interests aligned with the company. When there is the existence of venture capital investor appointed directors, these directors need to be focused on the strategic direction of the company. That is often not the case and detracts from having a high functioning board.

Strategically minded

A organization with a strong strategic direction where the CEO, chair, directors, and management is most often the organization that will have a strong board and be successful. Whether it is a start-up, a charity or a Fortune 500 company. When the board is holding the CEO accountable for this strategic direction and the directors are not getting their fingers, or worse, noses into the weeds or micro-operations of the company, the best chance of success exists. I have often experienced boards where the director has a lack of governance experience and education. Often, they compensate for this by getting into the minutiae and minor details of the operations of the organization. When directors are mature, experienced, educated and confident in their board roles the resulting board is most often well functioning.

Strong committee structure

A high functioning board will have strong committees with good leadership that will do the heavy lifting on specific board work that will include committees such as audit, compensation, governance and risk. Then based on the need and complexity of the company there will be committees for IT, cyber security, investment, finance and merger and acquisitions when required. The directors will be confident in discharging their duties when they are presented with well-framed reports from the committees of the board.

Time commitment

The days are over when a board member can hold down 10 or 15 board roles. As an individual board member, you have to be committed to the agenda and work of the board you sit on. A board member should have the time and schedule flexibility to be able to attend between five and nine board meetings and another five committee meetings a year and be substantially prepared for those meetings by reading the pre-meeting materials. A director can not deliberate and participate in a discussion without being prepared. In the case of a large bank board the suggested time commitment is half of a full-time career position. Even if you are on the board of a growth stage private company that is raising financing or being acquired, the time commitment can be substantial for extended periods of time. Therefore to ensure your board is high functioning you require board members who have the proper amount of time a schedule flexibility to discharge their responsibilities properly.

When these characteristics exist whether it is in a tech Start-up or multi-billion dollar company the participation in this high functioning board of directors will be both a rewarding and educational experience.

_______________________________

*Gerard Buckley has been working in the financial industry for over 32 years, helping companies strategically plan for accelerated levels of growth at Scotia Capital, Maple Leaf Angels and Jaguar Capital where he is now Managing Director. He leads a management consulting practice with mandates focused on growth in entrepreneurial companies and is an expert in structuring companies to access financing by employing governance, financial management and funding strategies. Gerard has worked on Merger & Acquisition teams transacting over $10 billion of deal flow in his career.As an experienced investor and a member of Angel Investment Networks, he understands the process of investment in growth private companies and advises CEO’s on how to prepare. Gerard is Chairperson of The Board of Directors of Maple Leaf Angels Corporation and was the Entrepreneur in Resident at INcubes, an internet accelerator based in Toronto. He served as a member on the Small and Medium Enterprise Committee of The Ontario Securities Commission and has served on the board of an Exempt Market Dealer and a TSX.V Public Company. He has a passion for helping young entrepreneurs prepare their companies for scale. Read more about Gerard’s advisory firm at http://www.jaguarcapital.ca.

Vous trouverez, ci-dessous, un article publié dans Harvard Business Review (HBR) par Bill Huyettet Rodney Zemmel qui montre que l’engagement accru des administrateurs dans diverses facettes de leurs activités peut avoir des retombées très positives pour l’organisation.

« McKinsey research suggests that the most effective directors are meeting these challenges by spending twice as many days a year on board activities as other directors do« .

Ainsi, l’article explore cinq (5) façons pour accroître l’implication des administrateurs :

(1) l’implication entre les réunions;

(2) l’implication dans le processus d’élaboration de la stratégie;

(3) l’implication dans la recherche de nouveaux talents;

(4) l’implication dans certains projets;

(5) l’engagement par le questionnement critique.

Je vous invite à prendre connaissance des détails au sujet de chaque point. Bonne lecture !

“Ask me for anything,” Napoleon Bonaparte once remarked, “but time.” Board members today don’t have that luxury either. Directors remain under pressure from activist investors and other constituents, regulation is becoming more demanding, and businesses are growing more complex. McKinsey research suggests that the most effective directors are meeting these challenges by spending twice as many days a year on board activities as other directors do.

As directors and management teams adapt, they’re bumping into limits—both on the amount of time directors can be asked to spend before the role is no longer attractive and on the scope of the activities they can undertake before creating organizational noise or concerns among top executives about micromanagement. We recently discussed some of these tensions with board members and executives at Prium, a New York-based forum for CEOs (in which McKinsey participates). The ideas that emerged, while far from definitive, provide constructive lessons for boardrooms. If there’s one overriding theme, it’s that boosting effectiveness isn’t just about spending more time; it’s also about changing the nature of the engagement between directors and the executive teams they work with.

Engaging between meetings. Maggie Wilderotter, chairman and CEO of Frontier Communications (and a member of the boards of P&G and Xerox) stresses that “it’s not just about the meetings. It’s about being able to touch base in between meetings and staying current.” Such impromptu discussions strengthen a board’s hand on the company’s pulse. Keeping board members informed also minimizes the time spent on background that slows up regular board meetings. And the communication works both ways. “I also want board members to elevate issues that they’re seeing on the horizon that we should be thinking about,” explains Wilderotter. “To me, it’s really more of a two-way street.” Directors and executive teams will need to work out what rhythm and frequency are right for them. Denise Ramos, president and CEO of ITT, notes that “conversations with board members every week or every two weeks may be too much.” For boards seeking to boost their level of engagement between meetings, experimentation and course correction when things get out of balance are likely to be necessary.

Engaging with strategy as it’s forming. Strategy, especially on the corporate-wide (as opposed to BU) level, is an area where the diverse experiences and pattern-recognition skills of experienced directors enable them to add significant value. But that’s only possible if they’re participating early in the formation of strategy and stress-testing it along the way, as opposed to reviewing a strategy that’s been fully thought through by executives. In the description of Wilderotter, strategy needs to become “a collaborative process where different opinions can be put on the table” and “different options can be reviewed and discarded.” This shifts the board’s attitude from reactive to proactive and can infuse a degree of radicalism into the boardroom. Effective directors don’t shy away from bold strategic questions, such as “What businesses should this company own?” and “What businesses should this company not own?” We were impressed by one board that even dared ask, “Should this company continue to exist?” In fact, that board concluded that the company should not continue to exist, and effected a highly successful reorganization separating the firm into several freestanding enterprises.

Engaging on talent. Directors have long assumed responsibility for selecting and replacing CEOs, both in the normal course of business and in “hit by a bus” scenarios. Many also find it useful to track succession and promotion—for example, by holding annual reviews of a company’s top 30 to 50 key executives. But to raise the bar, some boards are moving from simply observing talent to actively cultivating it. Case in point: directors who tap their networks to source new hires. Donald Gogel, the chairman and CEO of Clayton, Dubilier & Rice, explains that “our board members can operate like a highly effective search firm. There’s nothing like recruiting an executive who worked for you for a long time, particularly in some functional areas where you know that he or she is both capable and a great fit.” Other boards actively mentor high-performing executives, which allows those executives to draw upon the directors’ experience and enables the board to evaluate in-house successors more fully.

Engaging the field. Another way to enhance board engagement is to assign directors specific operational areas to engage on. Board members can assume roles in specific company initiatives, such as cybersecurity, clean technologies, or risk— becoming not only “the board’s eyes and ears,” notes Eduardo Mestre, Senior Advisor for Evercore Partners and a board director of Comcast and Avis Budget, “but really being a very active participant in the process.” Jack Krol, chairman of Delphi Automotive and former chairman and CEO of DuPont, requires board members to visit at least one business site every 12 months. At the same time, directors should be mindful not to interfere with operational teams or to supplant managers. The goal is to target specific projects that are particularly appropriate for individual directors and to encourage participating board members to be, as one director says, “collaborative, not intrusive.”

Engaging on the tough questions. We noted above the value of probing difficult strategic issues, but the importance of asking uncomfortable questions extends beyond strategy sessions to a wide range of issues. “You should have some directors—perhaps 20% of the board—who know the industry and can challenge any operating executive in that company on industry content,” says Dennis Carey, a Korn Ferry vice chairman who has served on several boards. “But the problem is not too few people on boards who know their industries. The problem is too many people who know the industries, who are looking in the rearview mirror and assuming that what made money over the past 20 years will make money again.” Michael Campbell, a former chairman, CEO, and president of Arch Chemicals, builds on this theme by adding that “every board member does not necessarily need to have industry experience. But they must have the courage in the boardroom to ask difficult questions.”

Our McKinsey colleagues have noted in past articles that understanding how a company creates (and destroys) value makes it much easier to identify critical issues promptly. In fact, it is worth asking whether everyone in the boardroom does indeed understand how the company and each of its divisions make money. Gogel even suggested that “boards should have at least one person who has the responsibility to think like an activist investor. Many boards are caught unaware because no director is playing that role.”

As boards raise and grapple with uncomfortable questions, it’s important to connect the dots between issues—perhaps by tasking one director with serving in an “integrator” role. “We get into a boardroom,” Wilderotter remarked, “and everybody’s a peer. But having a specific capacity to bring disparate points together is critical to keeping a board functional versus having it be dysfunctional.”

Ultimately, there are no shortcuts to building and maintaining well-tuned board and executive mechanics. Each of the measures requires hard work from the board members, and sometimes a CEO with thick skin. But a good director will provide the extra effort, and an effective CEO will make the most of an engaged board’s limited time.

Bill Huyett is a director in McKinsey’s Boston office. Rodney Zemmel is a director in McKinsey’s New York office.

Ce billet présente les résultats d’une étude menée par Aaron J. Atkinson and Bradley A. Freelan, associés des pratiques de fusions et acquisitions chez Fasken Martineau Dumoulin, qui porte sur la situation des OPA hostiles au Canada et sur les propositions de changements visées par le processus de consultation des ACVM du règlement 62-105. Vous trouverez, ci-dessous, le sommaire exécutif de la version française de cette étude que vous pourrez télécharger sur le site de Fasken Martineau. Cette étude fait le point sur la situation canadienne et expose 5 conclusions très intéressantes. Bonne lecture !

Au Canada, les façons d’acquérir une société ouverte sont nombreuses. Toutefois, une offre publique d’achat (« OPA ») présentée directement aux actionnaires constitue le seul et unique moyen d’acquérir le contrôle légal de la société sans l’appui ni le consentement de son conseil d’administration. Une telle OPA non sollicitée (ou « hostile ») sert souvent à contourner le conseil de l’émetteur visé pour présenter une offre directement aux actionnaires après l’échec de discussions avec le conseil, une manœuvre qui place par le fait même la société visée « en jeu ».

C’est d’ailleurs cette caractéristique unique des OPA qui alimente un débat aussi nourri au sujet du rôle que doit jouer le conseil d’un émetteur visé et de la portée adéquate de ses pouvoirs pour réagir à une opération qui, fondamentalement, en est une entre l’initiateur et les actionnaires de cet émetteur visé. D’un côté, les lois sur les valeurs mobilières prévoient un rôle essentiellement « consultatif » pour le conseil, qui a alors pour tâche de formuler une recommandation aux actionnaires. D’un autre côté, les lois canadiennes sur les sociétés par actions confèrent au conseil une plus grande latitude dans la gestion des affaires de la société, ce qui, en théorie, et dans les limites de la règle du jugement commercial, permettrait au conseil de tout simplement « refuser » l’offre d’achat pour y mettre fin. Or, on sait qu’en pratique, cette théorie est difficilement applicable.

En réalité, le principal outil à la disposition du conseil pour se prémunir contre une OPA hostile, soit le régime de droits des actionnaires (couramment appelé la « pilule empoisonnée »), comporte un caractère inéluctablement temporaire. En effet, lorsqu’elles ont été appelées à le faire, les autorités de réglementation des valeurs mobilières ont presque toujours rendu inopérants les régimes de droits des actionnaires après un certain temps, ce qui a alors permis à l’initiateur de contourner le conseil et de donner aux actionnaires la possibilité de prendre leur propre décision.

Devant cette situation, certains intervenants du marché sont d’avis que « cette position est plus favorable aux initiateurs qu’aux émetteurs visés et à leurs actionnaires, qu’elle limite le pouvoir discrétionnaire du conseil et des actionnaires et qu’elle ne maximise pas nécessairement la valeur pour ces derniers.

En 2015, les autorités canadiennes en valeurs mobilières diffuseront une proposition afin d’aborder ces préoccupations et de traiter d’autres enjeux, en apportant d’importants changements au régime canadien de réglementation des OPA. Plutôt que d’imposer une limite à la durée des régimes de droits ou aux mesures que peut prendre le conseil d’un émetteur visé, les modifications proposées allongeront considérablement la période pendant laquelle une OPA hostile doit demeurer ouverte, qui passera de 35 à 120 jours, et prévoiront une condition de dépôt minimal correspondant à la majorité des actions de l’émetteur visé. Ainsi, les actionnaires, plutôt que le conseil de l’émetteur visé, continueront d’avoir le dernier mot dans toute OPA.

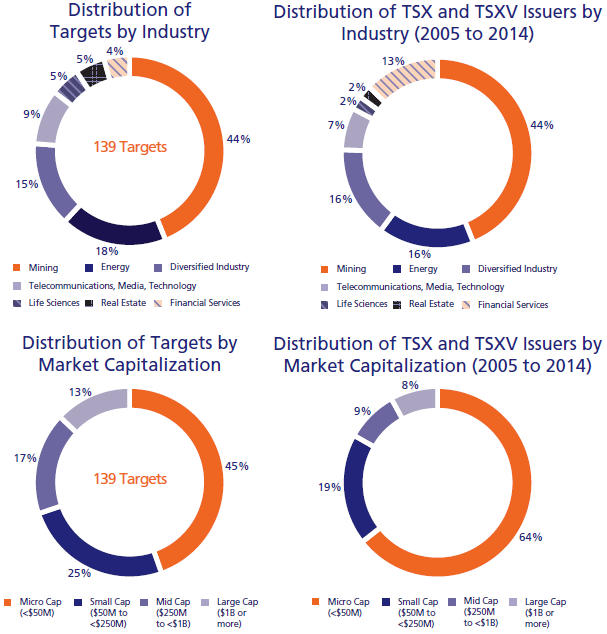

En vue de contribuer au débat, nous avons mené une analyse empirique de l’ensemble des 143 OPA non sollicitées visant l’acquisition du contrôle légal de sociétés ouvertes canadiennes cotées en bourse au cours de la période de dix ans terminée le 31 décembre 2014. Les parties qui ont lancé ces OPA étaient principalement des initiateurs dits « stratégiques » (90 %), plutôt que des initiateurs « financiers » (10 %), ce qui confirme la croyance populaire voulant que les acquéreurs financiers tendent à éviter la quête très publique du contrôle d’une société en l’absence du soutien de son conseil. Par ailleurs, deux tiers des initiateurs étaient situés au Canada, les autres étant américains (22 %) et étrangers (11 %).

Des 143 OPA analysées, 139 constituaient des courses aux procurations en vue d’acquérir le contrôle légal de la société ciblée. Parmi elles, des offres concurrentes visant une même société ont émergé dans quatre cas. La répartition des émetteurs ciblés reflétait essentiellement, pour la période visée par l’étude, la répartition des émetteurs canadiens cotés en bourse selon le secteur d’activité (à l’exception du secteur des services financiers, lequel était considérablement sous-représenté, possiblement en raison des contraintes réglementaires rigoureuses touchant la propriété de bon nombre des émetteurs de ce secteur) de même que selon la capitalisation boursière (à l’exception des émetteurs à microcapitalisation, qui étaient eux aussi considérablement sous-représentés, possiblement en raison des coûts élevés afférents au lancement d’une OPA en bonne et due forme par rapport à la taille de l’émetteur).

Nombre d’OPA non sollicitées visant le contrôle légal par année de déclenchement de l’OPA (143 OPA)

Parmi les sociétés ciblées, 127 d’entre elles (91 %) ont été ciblées par l’OPA d’un « premier joueur », c’est-à-dire que l’OPA a été lancée en l’absence de toute autre proposition publique d’acquisition. Pour déterminer si le régime canadien de réglementation des OPA favorise les initiateurs, un point de départ logique consiste à évaluer les résultats de telles OPA, puisqu’on peut présumer que, dans la plupart des cas, le conseil de l’émetteur visé ne cherchait pas activement un changement de contrôle lorsque l’initiateur a mis la société « en jeu ». Bien que ce fut le point de départ de notre étude, ce fut loin d’en être la fin.

Une minorité des sociétés ciblées (9 %) proposait publiquement une opération de changement de contrôle lorsque l’OPA hostile a été annoncée, c’est-à-dire que l’initiateur recherchait volontairement une enchère compétitive. Nous avons donc évalué séparément l’impact, s’il en est, de la dynamique de l’enchère sur les résultats. Enfin, bien que l’issue de toute OPA hostile soit le produit de nombreux facteurs, nous avons examiné, autant que possible, l’incidence potentielle de certains facteurs clés dont les parties avaient le contrôle. On pense par exemple à la prime et à la forme de la contrepartie offerte par l’initiateur, à l’adoption d’un régime de droits des actionnaires par la société ciblée, et à la recommandation formulée par le conseil d’administration.

Répartition des émetteurs viséspar secteur d’activité

Notre analyse vise à alimenter le débat actuel et ne prétend pas fournir des réponses définitives. Nous espérons que notre étude sera lue dans cet état d’esprit et, bien entendu, vos commentaires sont les bienvenus.

FAITS SAILLANTS

1. En lançant une opération de prise de contrôle publique, l’initiateur d’une OPA hostile réussissait dans plus de la moitié des cas. Toutefois, un changement de contrôle n’était en aucun cas inévitable.

L’OPA hostile d’un premier joueur a réussi dans 55 % des cas. En tenant compte des OPA contrecarrées par l’arrivée d’un chevalier blanc, c’est plus de 70 % des émetteurs canadiens cotés en bourse qui ont été acquis après avoir été mis « en jeu » par une OPA hostile. En même temps, près de 30 % des émetteurs visés par un initiateur premier joueur ont maintenu leur indépendance. C’est donc dire que la vente de la société n’est d’aucune façon inéluctable. Cependant, le bien-fondé d’une telle issue pour les actionnaires reste à prouver : au premier anniversaire de l’annonce de l’OPA, le titre de plus de 60 % de ces émetteurs visés se négociait à un escompte par rapport au prix définitif offert aux termes de l’OPA.

2. Bien que peu fréquents, les scénarios avec concurrence, lorsqu’ils se sont produits, ont été clairement à l’avantage des actionnaires alors que l’initiateur d’une OPA hostile se retrouvait souvent les mains vides.

Dans une bataille sans concurrent avec l’émetteur visé, l’initiateur a été victorieux dans les deux tiers des cas. En présence de concurrents, l’émetteur visé a été acquis dans 86 % des cas, mais l’acquéreur ultime fut l’initiateur dans seulement 33 % des cas. Mais peu importe la partie victorieuse, les actionnaires ont toujours bénéficié de l’émergence de concurrents, puisque dans de tels cas, la prime définitive offerte par l’initiateur était en moyenne de 76 % (une amélioration de 69 % par rapport à la prime définitive moyenne offerte aux termes des OPA sans concurrence). Bien que les initiateurs aient de bonnes raisons de craindre la concurrence, l’émergence de compétiteurs est demeurée somme toute rare : seules 37 % des OPA ont fait l’objet d’une concurrence.

3. Offrir une somme au comptant ou une prime solide augmentait les chances de réussite d’un initiateur d’OPA hostile. Toutefois, démarrer d’une position de force s’est révélé une formule avantageuse.

Plus des trois quarts de toutes les OPA comportaient une contrepartie au moins partiellement au comptant, et avec raison : en l’absence de compétition, l’initiateur offrant une contrepartie au moins partiellement au comptant avait gain de cause dans 72 % des cas et, en présence de concurrents, l’initiateur qui offrait une contrepartie entièrement au comptant améliorait substantiellement ses chances de succès (42 % contre 17 %). Bien qu’une prime initiale élevée n’ait pas dissuadé la concurrence, une prime de 30 % ou plus a permis à l’initiateur de remporter la mise dans près de 75 % des cas en l’absence de concurrence, et, en présence de concurrence, une prime relative positive était trois fois plus susceptible de faire gagner l’initiateur.

Parmi toutes les stratégies que peut envisager un initiateur pour remporter son OPA, l’acquisition d’une participation importante dans l’émetteur visé et la conclusion de conventions de dépôt avec ses actionnaires se sont révélées gagnantes. Ces stratégies se sont traduites par un taux de succès de 87 % lorsque l’initiateur détenait dès le début une participation de 20 % ou plus dans l’émetteur visé.

4. Les régimes de droits des actionnaires ont démontré leur valeur en permettant de du temps et en favorisant la concurrence.

Les régimes de droits des actionnaires ont permis aux conseils d’administration des émetteurs visés de gagner du temps, en doublant pratiquement, en moyenne, la période minimale de cinq semaines prévue par la loi avant que l’initiateur ne puisse prendre livraison d’actions aux termes de son offre. Ce délai additionnel s’est révélé critique : lorsqu’un initiateur premier joueur se trouvait confronté à une concurrence, cette concurrence a émergé après la fin de la période minimale prévue par la loi dans près de 70 % des cas. Il n’est donc pas surprenant que des concurrents se soient manifestés pour contrer l’initiateur premier joueur deux fois plus souvent lorsque l’émetteur visé avait adopté un régime de droits des actionnaires.

5. L’appui du conseil était un atout précieux : les initiateurs ont réalisé une OPA dans presque tous les cas où ceux-ci avaient obtenu l’appui du conseil d’administration, contrairement à ceux qui n’avaient pas un tel appui, notamment si la recommandation du conseil était plus susceptible d’influer sur le résultat.

Dans les cas où l’initiateur a ultimement obtenu le soutien du conseil d’administration de la société visée, son OPA a réussi dans tous les cas sauf un, soit 98 % du temps. Au contraire, sans l’appui du conseil, les OPA hostiles n’ont réussi que dans 22 % des cas. De plus, la décision du conseil de ne pas appuyer une OPA s’alignait plus fréquemment avec l’issue de l’OPA dans les cas où la recommandation du conseil aurait dû avoir plus d’influence : un alignement de 80 % dans les cas sans concurrence où le régime de droits des actionnaires était toujours en vigueur au moment de la recommandation finale du conseil; un alignement de 83 % lorsque l’actionnariat était moins concentré parmi les initiés, de sorte que le conseil était plus enclin à jouer un rôle de conseiller et de mandataire dans les négociations; et un alignement de 95 % dans le cas d’une OPA entièrement en actions, qui est davantage susceptible de faire les frais d’une critique négative du conseil de l’émetteur visé.

Ce que nous réserve l’avenir

Une OPA hostile demeure une manœuvre relativement peu fréquente au Canada : parmi les quelques 3 700 sociétés ouvertes cotées en bourse au Canada, en moyenne, seulement 14 ont fait l’objet d’une OPA hostile au cours d’une année donnée pendant la période de dix ans visée par l’étude. Cela ne veut pas dire pour autant que le spectre d’une OPA hostile est une menace en l’air. Dans une situation où des parties s’affrontent de façon évidente, si un régime favorisait réellement une partie plutôt qu’un autre et donnait un résultat nettement plus fréquent qu’un autre, le comportement (et le pouvoir de négociation de toutes les parties) sera naturellement influencé.

Les intervenants préoccupés par le fait que le régime actuel favorise les initiateurs plutôt que les émetteurs visés seront sans doute rassurés de savoir que le nouveau régime, s’il est adopté dans sa forme actuelle, devrait conférer un pouvoir accru aux conseils d’administration, en modifiant fondamentalement la dynamique des négociations futures en matière d’OPA, et pourrait faire augmenter l’incidence de la concurrence. D’un autre côté, à la lumière des risques accrus et des coûts potentiels du nouveau régime de réglementation pour les initiateurs, les prochaines années pourraient amener une baisse des OPA non sollicitées et, par le fait même, une baisse du risque même de faire l’objet d’une OPA. Dans la perspective où les réformes réglementaires visent à améliorer la dynamique des offres en conférant aux porteurs de titres un pouvoir de choix accru et en maximisant la valeur pour les actionnaires, cet objectif ne peut être atteint que si les initiateurs d’OPA estiment toujours avoir une chance de succès raisonnable malgré les risques inhérents au lancement d’une OPA.

Je vous invite à prendre connaissance du rapport publié par Ernst & YoungCenter for Board Matters dans lequel on présente les résultats d’une enquête portant, entre autre, sur la composition des CA et sur les mécanismes de renouvellement des membres du conseil.

Jamais la composition des conseils d’administration n’aura été autant scrutée par les investisseurs et les actionnaires. Et ce n’est que le début des interventions des actionnaires pour l’obtention d’un Board exemplaire…

Il y a vingt ans, il y avait peu d’interrogations sur la matrice des compétences, des habiletés et des expériences des membres des conseils d’administration. De nos jours les actionnaires veulent savoir si leurs élus sont aptes (1) à accompagner la direction dans l’exécution de la stratégie et (2) à superviser la gestion des risques (voir mon billet sur ce sujet Trois étapes pour aider le CA à s’acquitter de ses obligations à l’égard de la surveillance de la gestion des risques).

Le problème du renouvellement des membres du conseil, l’absence d’une politique claire concernant le nombre limite d’années de service au conseil, ainsi que le manque flagrant de diversité sur les conseils sont des facteurs-clés qui amènent les actionnaires à exiger une plus grande divulgation des profils des administrateurs et un processus de nomination plus ouvert, lors des assemblées annuelles.

L’article a été publié sur le blogue du Harvard Law School Forum on Corporate Governance. Voici une brève synthèse des résultats :

More than three-fourths of the investors we spoke with believe companies are not doing a good job of explaining why they have the right directors in the boardroom.

Companies can improve disclosures by making explicit which directors on the board are qualified to oversee key areas of risk for the company and how director qualifications align with strategy. Providing clarity around how board candidates are identified and vetted and the process for supporting board diversity goals may also strengthen investor confidence in the nomination process.

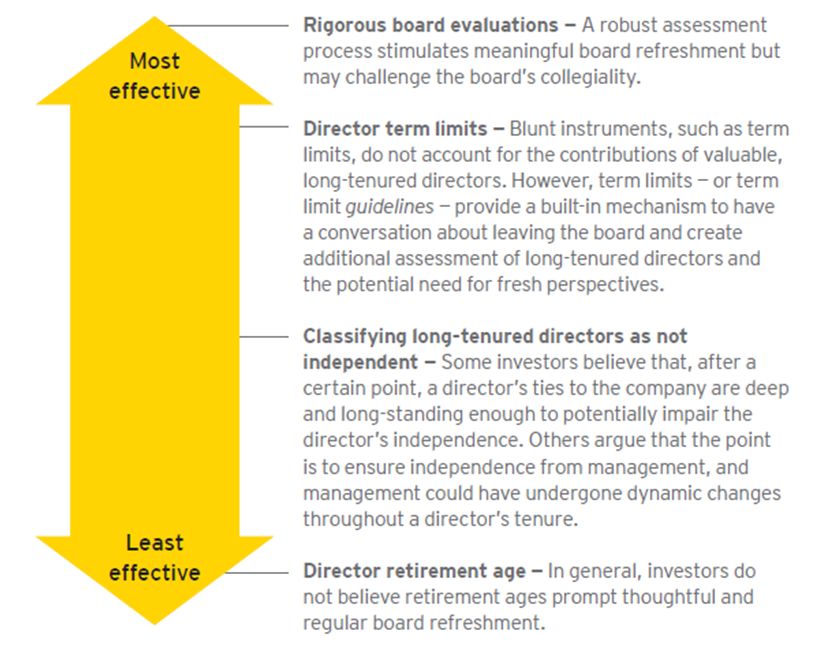

Rigorous board evaluations, including assessing the performance of individual board members, as well as the performance and composition of the board and its committees, are generally considered valuable mechanisms for stimulating thoughtful board turnover, but views about other approaches (e.g., term limits) differ widely.

L’article présente les avenues à explorer pour améliorer la composition des CA. Également, l’article propose trois bons moyens pour renforcer la divulgation liée à la composition du conseil. Enfin, l’article présente une manière originale de conceptualiser le renouvellement des conseils, en s’appuyant, notamment, sur de solides évaluations des administrateurs.

Room for improvement in making the case for board composition

Despite investor acknowledgement that some leading companies are doing an excellent job in this area, most of the investors we spoke with believe companies are generally not making a compelling enough case in the proxy statement for why their directors are the best candidates for the job.

Three ways companies can enhance board composition disclosures

Make disclosures company-specific and tie qualifications to strategy and risk: Be explicit about why the director brings value to the board based on the company’s specific circumstances. Companies should not assume that the connection between a director’s expertise and the company’s strategic and risk oversight needs is obvious. Also, explaining how the board, as a whole, is the right fit can be valuable, particularly given that most investors are evaluating boards holistically.

Provide more disclosure around the director recruitment process and how candidates are sourced and vetted: Disclosing more information around the nomination process—how directors were identified (e.g., through a search firm), what the vetting process entailed, etc.—can mitigate concerns about the recruitment process being insular and informal.

Discuss efforts to enhance gender and ethnic diversity: Many companies—nearly 60% of S&P 500 companies—say they specifically identify gender and ethnicity as a consideration when identifying director nominees, but that is not always reflected in the gender and ethnic makeup of the board. Disclosing a formal process to support board diversity, including providing clarity around what is considered an appropriate level of diversity, can highlight efforts to recruit diverse directors.

A skills matrix tied to company strategy can be a valuable disclosure tool but is not the only way to convey a thoughtful approach. A letter from the lead director or chairman that discusses the board’s succession planning and refreshment process and any recent composition changes can also be effective.

Beyond disclosure, engagement can provide investors a valuable dimension in assessing board quality. Involving key directors in conversations with shareholders can provide further insight into board dynamics, individual director strengths and composition decisions.

Views vary on mechanisms to trigger board renewal

When we asked investors what mechanisms boards can use to most effectively stimulate refreshment, the vast majority chose rigorous board evaluations as the optimal solution and director retirement ages as the least effective. However, views around the different mechanisms and how they should be used vary—as does how investors approach the topic of tenure altogether.

Some investors evaluate tenure and director succession planning as a forward-looking risk, while others focus on past company performance and decisions. The commentary below represents investor opinions on each mechanism.

One of the top takeaways from our dialogue dinners was the importance of robust board evaluations, including evaluations of individual board members, to meaningful board refreshment and board effectiveness. Some directors noted the value in bringing in an independent third party to facilitate in-depth board assessments and in changing evaluation methods as appropriate to reinvigorate the process. Some also noted that board evaluation effectiveness relies on the strength of the independent board leader leading the evaluation.

When it comes to how boards manage director tenure internally, setting expectations up front that directors’ board service will be for a limited amount of time—not necessarily until they reach retirement age—is important. We’ve heard from some directors that having periodic conversations with individual board members about their future on the board is valuable and can help provide “off ramps” and a healthy succession planning process.

Conclusion

Given investors’ increasing focus on board composition, companies may want to review and enhance proxy statement disclosures to ensure that director qualifications are explicitly tied to company-specific strategy and risks and that the board’s approach to diversity and succession planning is transparent.

Beyond disclosure, ongoing dialogue with institutional investors that involves independent board leaders may allow for a rich discussion around board composition. Also, through regular board refreshment and enhanced communications around director succession planning, companies may head off investor uncertainty and temptations to go down a rules-based path regarding director terms.

Virginie Seghers, fondatrice du cabinet Prophil, a co-publié avec Mazars, Delsol Avocats et la chaire « Philanthropie » de l’Essec une étude sur les « fondations actionnaires en Europe » où l’on découvre que les entreprises dont elles sont actionnaires sont en général plus stables que les autres, et sont souvent aussi plus rentables.

Notre pays méconnaît largement un mode de gouvernance répandu dans le reste de l’Europe. Au Danemark, en Suisse, en Allemagne, de grandes entreprises industrielles et commerciales sont couramment détenues par des fondations.

Et le modèle s’avère durable et vertueux. Pourquoi ?

Quelles sont les spécificités des fondations actionnaires ?

Les voici résumées autour de 10 mots clés.

Qu’en est-il au Québec ? Ce sera le sujet d’un autre billet.

Ikea, Lego, Rolex, Bosch, Carlsberg : ces marques sont mondialement connues. Mais parmi leurs millions de clients, combien connaissent leur autre particularité ? Les groupes industriels à l’origine de ces « success stories » sont, depuis longtemps, tous la propriété de… fondations ! Pourtant, faire rimer économie et philanthropie ne va pas de soi, et le terme même de « fondation actionnaire » peut paraître un oxymore. Car la philanthropie s’accorde a priori avec le « don », et l’actionnariat avec l’investissement.

Le terme n’est d’ailleurs pas stabilisé, et ne correspond à aucun statut juridique propre dans les pays étudiés : les Suisses parlent de « fondation entrepreneuriale » ou de « fondation économique», les Danois évoquent les « fondations commerciales », et les anglosaxons les « industrial fondations ». Chez nos voisins, industrie et philanthropie vont assurément de pair.

MAJORITAIRE

La fondation actionnaire, telle que nous la traitons dans cette étude, désigne une fondation à but non lucratif, propriétaire d’une entreprise industrielle ou commerciale. Elle possède tout ou partie des actions, et la majorité des droits de vote et/ou la minorité de blocage.

Ce qui n’empêche donc pas les entreprises concernées d’être en partie cotées en bourse (les fondations actionnaires représentent 54% de la capitalisation boursière de Copenhague).

Dès lors, plusieurs fondations, qui certes détiennent des actions d’entreprises, sortent du champ de cette étude, notamment celles qui ont décidé de filialiser des activités connexes à leur objet, en créant des sociétés (une fondation culturelle qui, par exemple, crée une maison d’édition).

FAMILLES

Les fondations actionnaires sont essentiellement des histoires de familles, d’engagement personnel, comme les nombreux cas de cette étude en témoignent.

Dans un esprit de résistance (La Montagne), avec la volonté de protéger et développer un patrimoine industriel (Bosch), ou avec le souhait d’articuler des engagements humanistes avec une transmission sereine de l’entreprise en absence d’ayant droits (Pierre Fabre), chaque histoire est celle d’un homme, d’une famille qui se projette dans le long terme, avec la volonté de perpétuer une culture d’entreprise singulière, dans une double approche économique et sociétale.

PHILANTHROPIE

Cette transmission est, en soi, un acte de philanthropie majeur. Car les propriétaires font don de leurs titres à une structure créée à cet effet, et renoncent donc aux gains, le cas échéant substantiels, d’une vente avec plus-value. Ils sont philanthropes.

Mais la philanthropie s’exprime aussi, et surtout, dans les dons des fondations, rendus possibles par les dividendes perçus et/ou les intérêts des dotations.

Par exemple, les fondations actionnaires donnent plus de 800 millions d’euros par an au Danemark (seul pays où des études aussi précises existent) et la fondation Novo Nordisk représente, à elle seule, 120 millions d’euros. Sa dotation est telle qu’elle pourrait continuer à vivre sans même percevoir de dividendes !

INTÉRÊT GÉNÉRAL

Au Danemark, la première mission des fondations actionnaires est majoritairement de protéger et de développer l’entreprise ; la seconde, de soutenir une cause culturelle et/ou sociale.

La double mission économique et philanthropique est parfaitement assumée et le rôle de gestion de l’entreprise, prioritaire. Maintenir le patrimoine industriel dans ce petit pays, conserver des fleurons industriels, protéger l’emploi sont considérés comme des sujets d’intérêt général.

Ce n’est pas le cas en France, où intérêt général et activité commerciale ne vont pas facilement de pair. Le principe de spécialité impose en effet aux fondations françaises d’avoir une mission exclusivement d’intérêt général, qui, dans une vision encore assez restrictive, ne peut être économique.

Quant à l’Allemagne, il n’est pas obligatoire d’avoir une mission d’intérêt général pour créer une fondation, a fortiori une fondation actionnaire. Comme le dit le célèbre banquier privé Thierry Lombard, les fondations actionnaires soulèvent des questions non seulement « de loi, mais d’idéologie ».

GOUVERNANCE

C’est le sujet clé. Dans les pays étudiés, et selon le droit national, deux modes de gouvernance prédominent :

1. soit une gestion directe de l’entreprise par la fondation, qui suppose une double finalité pleinement assumée et un conseil d’administration capable de prendre des décisions économiques et philanthropiques à la fois ;

2. soit une gestion indirecte, avec une distinction nette des instances de gouvernance de l’entreprise et de la fondation, via la création d’une société holding intermédiaire. Le droit et la fiscalité sont souvent complexes et variables d’un pays à l’autre : nous avons fait appel à d’éminents spécialistes nationaux pour nous décrire leur « état du droit ».

Notons que dans les fondations actionnaires, la succession des dirigeants n’est pas un sujet aussi sensible qu’ailleurs. La question se règle en général longtemps à l’avance, au niveau de la fondation.

RESPONSABILITÉ SOCIALE

Cette performance globale n’est pas une série de bonnes actions, mais un engagement stratégique d’une entreprise, qui se préoccupe de sa contribution économique, sociale et sociétale à son environnement.

Les entreprises les plus avancées ont compris que leur intérêt particulier rencontrait ici l’intérêt général, pour peu qu’elles ne restent pas les yeux rivés sur une gestion à court terme.

Alors que la pratique de la RSE est devenu de plus en plus un exercice imposé, et trop souvent l’instrument de directions de la communication, la fondation actionnaire place, par nature, la responsabilité sociale et l’approche de long terme au coeur de sa stratégie : dans une forme de fertilisation croisée, fondation et entreprise intrinsèquement liées, s’influencent.

LONG TERME

À un monde économique de plus en plus instable et à court terme, la fondation actionnaire oppose un modèle d’actionnariat stable et durable. La menace de prédateurs est évacuée, puisque toute tentative d’OPA hostile est impossible, et une vision de long terme, dont la redistribution de dividendes n’est pas l’unique préoccupation, oriente la stratégie.

TROISIÈME VOIE

Cette aventure, les tenants de l’économie positive et les philosophes de l’économie altruiste seraient prêts à la tenter. Car intrinsèquement les fondations actionnaires devraient faire consensus : elles allient la création de valeur économique à la force du don, au service d’une économie durable et d’une cohésion sociale renforcée.

C’est pourquoi il est si important de défricher cette troisième voie qui, en France, n’est encore qu’un sentier. La fondation actionnaire peut contribuer à faire émerger un nouveau capitalisme, plus altruiste et durable. Ce paysage pour les générations à venir, beaucoup l’appellent de leurs voeux.

EFFICACITÉ

Mais peut-on conjuguer gouvernance philanthropique et efficacité économique ? Les quelques études scientifiques (voir le panorama danois) existantes tendraient à le prouver : les performances des entreprises propriétés de fondations sont meilleures que celles où l’actionnariat est dispersé*. Le phénomène est comparable dans les sociétés familiales.

D’un point de vue social, ce type d’entreprises semble mieux traverser les crises conjoncturelles. Les dirigeants peuvent en effet s’appuyer sur une meilleure implication de leurs collaborateurs, rassurés par la stabilité de l’actionnariat.

Enfin, à l’heure où les cadres sont à la recherche de sens dans leur vie professionnelle, les valeurs promues par les fondations leur donnent une bonne raison de s’investir dans l’entreprise.

___________________________________

*Comparatif de l’efficacité des fondations actionnaires (colonne de droite), face aux entreprises à l’actionnariat dispersé (colonne de gauche), et aux entreprises à l’actionnariat familial (colonne du centre) (en anglais)

Source: Steen Thomsen, « Corporate ownership by industrial foundations »)

On constate que les fondations-actionnaires ne sous-performent jamais les autres types d’entreprises. Selon Steen Thomsen, auteur de l’étude dont est tirée le tableau (« Corporate Ownership by Industrial Foundations« ), « les fondations-actionnaires présentent un taux de rentabilité et de croissance comparable aux entreprises classiques, mais avec un niveau de sécurité financière bien plus élevé » (comme le montre le ratio « equity/assets » de 47 au lieu de 36 pour les entreprises à l’actionnariat dispersé, et 38 pour les entreprises familiales).

Quel doit être le rôle du conseil d’administration eu égard à la surveillance de la gestion des risques ? L’article publié par Scott Hodgkins, Steven B. Stokdyk, et Joel H. Trotter dans le forum du site du Harvard Law School présente, d’une manière très concise, les trois étapes qu’un conseil doit entreprendre en matière de gestion des risques d’une société.

Les auteurs rappellent l’utilisation d’un modèle développé par le COSO (Committee of Sponsoring Organizations de la Commission Treadway), bien connu en gouvernance, qui invite les CA à :

S’entendre avec la direction sur un niveau de risque acceptable (l’appétit pour le risque);

Comprendre les efforts de la direction dans l’exécution des pratiques de gestion des risques;

Revoir le portefeuille des risques en considérant l’appétit pour le risque;

Connaître les risques les plus importants de l’entreprise, ainsi que les stratégies de la direction pour les contrôler.

L’article discute des trois étapes que le CA doit accomplir afin de s’acquitter de son rôle en matière de gestion des risques :

Déterminer le modèle de supervision privilégié par le CA;

Convenir avec le management d’une approche appropriée à la gestion des risques et revoir l’approche retenue;

Évaluer les ressources du CA en matière de gestion de risques et éviter les biais et la pensée de groupe.

Voici donc un extrait de l’article qui précise chacune des trois étapes.

1. Determine the board’s preferred oversight model

Typically, boards either retain primary responsibility for risk oversight or delegate initial oversight duties to a committee, such as the audit committee or a risk committee. Where the board retains primary responsibility, individual committees may provide input on specific types of risk, such as compensation risk, audit and financial risk, and regulatory and compliance risk.

In selecting between the active board model and the committee model, the board should consider those directors with the necessary expertise to oversee unique market, liquidity, regulatory, innovation, cybersecurity and other risks that may require special attention. The board should also consider whether adding duties to an existing committee, such as the audit committee, may be too burdensome in light of existing workload.

These issues are unique to each company, and the key is to ensure that the model you choose is effective for your situation.

2. Develop a stated approach to risk management

Some companies may adopt a risk management statement or policy. As with other policy statements, a risk management statement can create a tone-at-the-top benchmark for assessing value-creation opportunities as they arise and provide guideposts for management’s operational decisions.

A risk management statement should separately identify:

Acceptable strategic risks

Undesirable risks

Risk tolerances or thresholds in stated categories, such as strategic, financial, operational and compliance

In developing the company’s approach, the board should consider:

Investor expectations of the company’s risk appetite

Competitors’ apparent risk appetite

Stress-tests for risk scenarios, using historical experience and sensitivity analysis

Long-term strategy versus existing core competencies

Effects of new business generation on desired risk profile

Strategic planning and operations compared to articulated risk appetite

Developing a stated approach to risk management requires good working relationships among the board members, the CEO and management, as well as active participation by all involved.

3. Assess board capabilities and effectiveness, reviewing for bias and groupthink

The board must evaluate its own capabilities and effectiveness, paying particular attention to the possible emergence of cognitive bias or groupthink.

In assessing board capabilities and effectiveness, the board should consider:

Directors’ skills and expertise compared to the company’s current and future operations

Possible director education initiatives or new directors with additional skills

Delegation of risk oversight in highly technical areas, such as cybersecurity

Retention of independent experts to evaluate specific risk management practices

Clear allocation of responsibility among the board committees and members

The balance between board-level risk oversight and management-level day-to-day ERM Boards must also guard against two types of bias:

Resistance to new ideas from outsiders, thus overlooking new opportunities or risks

Confirmation bias, incorrectly filtering information and confirming preconceptions

Maintaining contact with business realities also requires collegiality and open communication among management and directors.

Boards should consider their risk oversight in light of these three steps to assist in framing an effective approach to enterprise-level risk exposures.

Le Collège des administrateurs de sociétés présentera son nouveau cours Gouvernance et leadership à la présidence, les 19 et 20 mai prochains à Montréal, afin de répondre à la demande grandissante des administrateurs exerçant une fonction à la présidence d’un conseil d’administration, d’un comité du conseil ou d’un comité consultatif d’une PME.

Précédée d’un test en ligne sur le leadership, cette formation est axée sur la prise de conscience et le développement des habilités relationnelles et politiques qu’exigent les fonctions de présidence. Outre les résultats du test en ligne, des études de cas, une simulation et des témoignages seront aussi au rendez-vous.

Si vous assumez les fonctions de présidence, c’est un cours à ne pas manquer avec notre équipe de sept formateurs de haut calibre! Pour plus d’informations sur les critères d’admission, les objectifs et le contenu : consultez la page Web du cours ou le programme détaillé.

Au plaisir de vous compter parmi nous et nous vous invitons à relayer l’information aux présidents de vos conseils d’administration.

En gouvernance, on fait très souvent référence aux mécanismes de rémunération de la direction des entreprises mais on s’interroge assez peu sur la rémunération des administrateurs. Également, il y a peu d’études sur le sujet.

L’article qui suit a été publié par Ira Kay* dans le Harvard Law School Forum on Corporate Governance. L’auteure confirme que les administrateurs de sociétés sont de plus en plus sollicités; ils sont donc appelés à investir de plus en plus de temps dans leurs fonctions et ils doivent assumer plus de risques.

La rémunération des administrateurs augmente d’environ 5 % par année et les paiements se font généralement sur une base de 50 % en argent et 50 % en actions à paiement différé.

Les tendances qui se dessinent sont claires. En voici un extrait :

In recent years, total pay has increased by, on average, less than 5% per year

Most companies make pay changes less frequently (e.g., every two or three years)

Most large cap companies have eliminated regular meeting fees, in favor of higher annual cash/equity retainers

Equity awards, which are most often RSUs or some other type of full-value award, typically represents 55% to 60% of total pay

Near universal practice of having stock ownership and/or stock retention requirements, such as deferred stock units that are held until after board departure

Some pay practices vary widely by industry and company size; for example smaller cap companies continue to provide meeting fees and may also grant stock options

In the future, we expect annual director pay to increase, on average, by 3% to 5% and the weighting on equity awards to increase

Cash Compensation

The traditional directors’ compensation program included both an annual retainer and a separate fee provided for attending Board and Committee meetings. The presence of a meeting fee encouraged meeting attendance and automatically adjusts for workload as measured by the number of Board and Committee meetings. Meeting attendance is less of an issue today as companies disclose whether their directors attend at least 75% of meetings and proxy advisors scrutinize those directors who fail to meet the threshold. In recent years, most large companies and more mid-sized and small companies have simplified their approach to delivering cash compensation by eliminating the meeting fee element and instead providing a larger single cash retainer. The rationale for this change is to ease the administrative burden associated with paying a director a fee for each meeting attended and to communicate that meeting attendance is expected with less emphasis on actual time spent and more emphasis on the annual service provided to shareholders. We expect this shift to continue among smaller and mid-sized companies where the elimination of meeting fees is not yet a majority practice.

Equity and Cash Compensation Mix

Over time, as director compensation has increased, the trend has been to provide greater focus on equity compensation, which provides direct economic alignment to the shareholders who directors represent. Currently, it is common to have equity represent a slight majority of regular annual compensation – such as a pay mix of equity compensation 55% and cash compensation 45%. In analyzing broad market practices, we typically find directors’ total compensation allocated 40% to 50% to cash compensation and 50% to 60% to equity compensation. The emphasis on equity compensation is also directionally consistent with the typical pay mix for senior executives.

Equity Grant Design

In the early 2000s, stock options delivered most or all of director equity compensation, similar to the approach for compensating executives. The current trend has shifted to the use of full-value shares to deliver all (or at least most) of equity compensation. This shift in approach was driven by the change in accounting standards, negative views of stock options as a compensation vehicle for directors (and executives), and other factors. As a result, today, the most common market practice is to deliver equity compensation solely through full-value shares; a minority of companies (typically 25% or fewer, depending on the set of companies analyzed) continue to grant stock options.

Companies vary in the delivery of the full-value shares with the most common approaches including:

Restricted stock/units, which have a restriction period that may range from six months to three years

Deferred stock units, in which actual share are not delivered or sold until departing the Board

Outright grants, which are immediately vested at grant

The use of performance‐based awards for directors is nearly non‐existent due to the desire to avoid any misperceptions between compensation and their duties and fiduciary responsibilities.

Board Leadership Compensation

Today independent directors are either led by a Non-Executive Chairman (at companies who have separated the leadership role) or a Lead Director (for companies who maintain a combined Chairman and CEO role or an Executive Chairman). At companies who have separated the Board Chairman and CEO roles, an independent Non-Executive Chairman is appointed to lead the independent directors. The responsibilities of this position vary by company as does the amount of additional compensation, which is provided through cash, equity or a combination thereof. At the low end of the spectrum, the Non-Executive Chairman’s extra retainer is positioned modestly above the extra retainer provided to the Audit Committee Chairman (or the Lead Director, which is discussed below) or at the high end of the spectrum, the additional retainer can be significantly higher, such as an additional $200,000 or more.

For those companies who have decided to continue with a single combined role, an independent director serving in the role of Lead Director (or Presiding Director) has emerged as a best practice to lead executive sessions of independent directors. When this role emerged in the mid-2000s, the Lead Director often received no additional compensation and frequently rotated among independent Committee Chairmen or was represented by the Governance Committee Chairman. More recently, for companies to maintain the combined role of Chairman and CEO, Lead Directors have become more prominent and are now typically appointed by the independent directors and are compensated with an additional retainer.

Board Committee Chairmen are typically provided an extra retainer to compensate for the additional work with management and outside advisors in preparing to lead committee meetings. Following the introduction of Sarbanes-Oxley, the extra retainer provided to the Chairman of the Audit Committee increased at a higher rate than other committee chairmen in recognition of the additional workload in terms of number of meetings and required preparation, heightened risk, and the financial expertise required of the position. Following the introduction of the enhanced proxy disclosure rules in 2006 and the Say on Pay advisory vote in 2010, extra retainers provided to the Chairman of the Compensation Committee increased to be positioned closer to (or just below) that of the Audit Committee Chairman.

Stock Ownership Guidelines and Requirements

There is near universal use of stock ownership guidelines or holding requirements for directors, which is consistent with the prevalence of requirements for senior executives. In order to align directors’ economic interests with the shareholders they represent, companies typically provide full-value equity awards and require minimum stock ownership specified as a multiple of the annual retainer or equity award value. At larger companies, the minimum stock ownership guideline is typically three to five times the annual retainer or equity award value with the expectation that this will be achieved within five years of joining the Board. Some companies also have stock holding requirements, which may be used in addition to stock ownership guidelines. For example, companies may require directors to retain net (after tax) shares upon lapse of restrictions until the minimum stock ownership guideline is achieved. Other companies may solely use stock holding requirements (such as grant equity compensation as deferred stock units) to ensure directors accumulate and retain meaningful levels of stock ownership through their tenure as a director.

Contemporary Best Practices

Over time director compensation levels and program design have evolved to address the changing regulatory environment and the enhanced role of the typical director, as described above. Director compensation arrangements have settled to a general design adopted by most companies:

– Annual cash retainer representing approximately 40% to 45% of the total program value

– Annual equity award most often delivered through full-value shares that vest after a specified time and representing approximately 55% to 60% of the total program value

– Extra cash retainers for Non-Executive Chairman, Lead Directors and Committee Chairmen

– Stock ownership guidelines representing three to five times the annual retainer, with stock holding requirements of new grants until the ownership guideline is achieved.

________________________________

*Ira Kay is a Managing Partner at Pay Governance LLC. This post is based on a Pay Governance memorandum by Steve Pakela and John Sinkular.

Les personnes intéressées par les nouvelles recherches en gouvernance des entreprises sont invitées à assister au Colloque étudiant en gouvernance de société mardi 14 avril 2015

En partenariat avec la FSA et la Chaire en gouvernance des sociétés, le CÉDÉ organise un colloque étudiant. Les étudiants du cours de Gouvernance de l’entreprise DRT-6056 du professeur Ivan Tchotourian et du cours de Gouvernance des sociétés CTB-7000 du professeur Jean Bédard présenteront lors de cet événement le bilan de travaux de recherche réalisés durant la session d’hiver 2015.

Heure : 8 h 30 à 11 h 30

Lieu : Salon Hermès de la Faculté des sciences de l’administration

Plusieurs OBNL sont à la recherche d’un document présentant les principes les plus importants s’appliquant aux organismes à buts charitables.

Le site ci-dessous vous mènera à une description sommaire des principes de gouvernance qui vous servirons de guide dans la gestion et la surveillance des OBNL de ce type. J’espère que ces informations vous seront utiles.

Vous pouvez également vous procurer le livre The Complete Principles for Good Governance and Ethical Practice.

What are the principles ?

The Principles for Good Governance and Ethical Practice outlines 33 principles of sound practice for charitable organizations and foundations related to legal compliance and public disclosure, effective governance, financial oversight, and responsible fundraising. The Principles should be considered by every charitable organization as a guide for strengthening its effectiveness and accountability. The Principles were developed by the Panel on the Nonprofit Sector in 2007 and updated in 2015 to reflect new circumstances in which the charitable sector functions, and new relationships within and between the sectors.

The Principles Organizational Assessment Tool allows organizations to determine their strengths and weaknesses in the application of the Principles, based on its four key content areas (Legal Compliance and Public Disclosure, Effective Governance, Strong Financial Oversight, and Responsible Fundraising). This probing tool asks not just whether an organization has the requisite policies and practices in place, but also enables an organization to determine the efficacy of those practices. After completing the survey (by content area or in full), organizations will receive a score report for each content area and a link to suggested resources for areas of improvement.

Voici une liste des 33 principes énoncés. Bonne lecture !

Voici un communiqué du CAS sur le choix des entreprises qui se sont démarquées dans le domaine de gouvernance.

Première Grande soirée de la gouvernance Les Affaires

Afin de souligner les meilleures pratiques des conseils d’administration, Les Affaires, en collaboration avec le Collège des administrateurs de sociétés, l’Institut des administrateurs de sociétés et l’Institut sur la gouvernance d’organisations privées et publiques (IGOPP), tenait le 1er avril dernier la Grande soirée de la gouvernance.

Dans la catégorie Professionnalisation, c’est le conseil d’administration de Marquis Imprimeur qui a été retenu à titre de modèle en se dotant d’un conseil plus solide pour accompagner la croissance. Le Collège tient à souligner la participation du président du CA, M. Jacques Mallette, et du PDG de l’entreprise, M. Serge Loubier, parmi ses formateurs au cours Gouvernance des PME. De plus, M. Jacques Lefebvre, ASC, siège également sur ce conseil et en préside le comité de gouvernance depuis 2009.

Le conseil d’administration de Promutuel Assurance a été, quant à lui, désigné dans la catégorie Transformation en raison de son plan d’action pour changer sa culture grâce à la formation continue. Le Collège a collaboré étroitement à la réalisation de ce plan remarquable avec M. Martin Bergeron, ASC, dans l’un de ses volets visant la formation des 200 administrateurs de l’ensemble des mutuelles.

Le conseil d’administration de Pages Jaunes Limitée s’est aussi distingué dans la catégorie Situation de crise par les actions qu’il a posé au cours des dernières années pour sortir plus fort d’une crise financière.

Mary Ann Cloyd, responsable du Center for Board Governance de PricewaterhouseCoopers (PwC), vient de publier dans le forum du HLS un important document de référence sur le phénomène de l’activisme des actionnaires.

Son texte présente une excellente vulgarisation des activités conduites par les parties intéressées : Qui, Quoi, Quand et Comment ?

Je vous suggère de lire l’article au complet car il est très bien illustré par l’infographie. Vous trouverez ici un extrait de celui-ci.

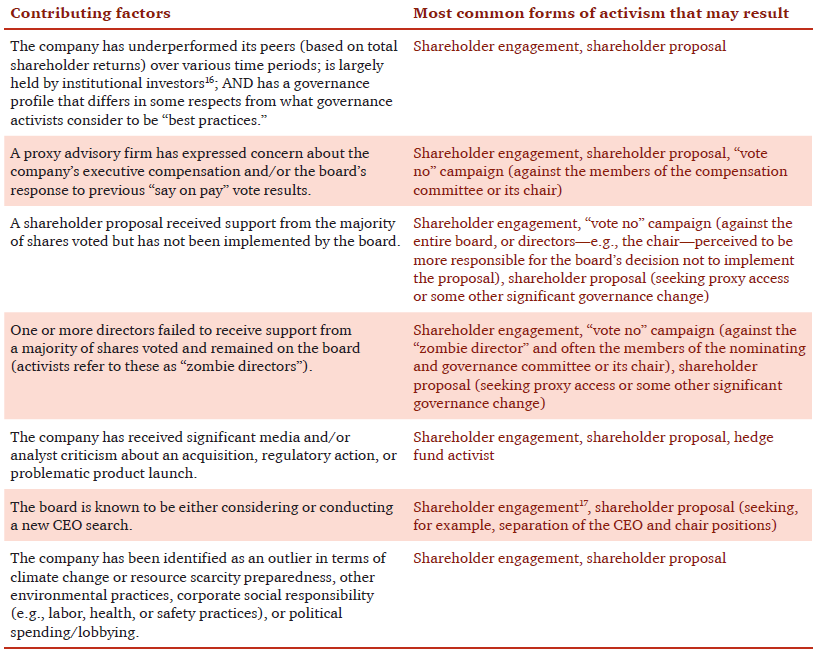

“Activism” represents a range of activities by one or more of a publicly traded corporation’s shareholders that are intended to result in some change in the corporation. The activities fall along a spectrum based on the significance of the desired change and the assertiveness of the investors’ activities. On the more aggressive end of the spectrum is hedge fund activism that seeks a significant change to the company’s strategy, financial structure, management, or board. On the other end of the spectrum are one-on-one engagements between shareholders and companies triggered by Dodd-Frank’s “say on pay” advisory vote.

The purpose of this post is to provide an overview of activism along this spectrum: who the activists are, what they want, when they are likely to approach a company, the tactics most likely to be used, how different types of activism along the spectrum cumulate, and ways that companies can both prepare for and respond to each type of activism.

Hedge fund activism

At the most assertive end of the spectrum is hedge fund activism, when an investor, usually a hedge fund or other investor aligned with a hedge fund, seeks to effect a significant change in the company’s strategy.

Background

Some of these activists have been engaged in this type of activity for decades (e.g., Carl Icahn, Nelson Peltz). In the 1980s, these activists frequently sought the breakup of the company—hence their frequent characterization as “corporate raiders.” These activists generally used their own money to obtain a large block of the company’s shares and engage in a proxy contest for control of the board.