L’intelligence artificielle (IA) est en train de transformer de nombreux aspects de notre vie quotidienne, des voitures autonomes aux assistants vocaux en passant par les diagnostics médicaux. L’une des dernières frontières de cette révolution technologique est le domaine de la gouvernance d’entreprise. Les conseils d’administration, souvent perçus comme des bastions de traditions et de pratiques de conformité, voient désormais l’IA comme un outil prometteur pour améliorer la prise de décision, l’efficacité et la transparence.

En quoi l’intelligence artificielle est-elle utile pour les conseils d’administration ?

Les conseils d’administration sont responsables de la supervision stratégique et de la prise de décisions cruciales pour le futur des entreprises. Ces responsabilités nécessitent une analyse rigoureuse des données, une compréhension approfondie des tendances du marché et une capacité à anticiper les défis futurs. L’IA offre une multitude d’applications qui peuvent assister les conseils d’administration dans ces tâches essentielles.

Voici les principales utilisations.

Analyse prédictive

Les algorithmes d’IA peuvent analyser d’énormes quantités de données historiques pour identifier des tendances et des modèles. Par exemple, ils peuvent prédire les performances financières futures en se basant sur des données passées, des conditions de marché actuelles et des variables économiques. Cette capacité prédictive peut aider les conseils d’administration à prendre des décisions plus éclairées sur des questions telles que les investissements, les fusions et acquisitions, et les stratégies de croissance.

Gestion des risques

L’IA peut également jouer un rôle crucial dans la gestion des risques. En analysant des données en temps réel, les systèmes d’IA peuvent identifier des risques plus rapidement et avec une plus grande précision que les méthodes traditionnelles. Par exemple, ils peuvent détecter des anomalies dans les transactions financières qui pourraient indiquer une fraude ou des problèmes de conformité.

Optimisation des processus internes

Les tâches administratives et répétitives, telles que la préparation des rapports et la gestion des documents, peuvent être automatisées grâce à l’IA. Cela permet aux membres du conseil d’administration de se concentrer sur des tâches plus stratégiques et à valeur ajoutée.

Surveillance et conformité

Les systèmes d’IA peuvent surveiller en permanence les activités de l’entreprise pour s’assurer qu’elles respectent les réglementations en vigueur. Ils peuvent également générer des rapports de conformité automatiquement, réduisant ainsi la charge de travail des membres du conseil et minimisant les risques de non-conformité. Cela est particulièrement utile dans des environnements réglementaires complexes et en constante évolution.

Applications concrètes de l’IA dans les conseils d’administration

Analyse de la performance financière

Les outils d’IA peuvent fournir des analyses financières en temps réel, aider à la détection des tendances et des anomalies, et offrir des prévisions précises. Par exemple, des modèles d’apprentissage automatique peuvent prédire les flux de trésorerie futurs, identifier les secteurs sous-performant et recommander des actions correctives.

Évaluation des talents et de la succession

L’IA peut aider à évaluer les compétences et les performances des cadres supérieurs, identifier les lacunes en matière de compétences et planifier la succession. Des plateformes d’IA peuvent analyser des données sur les performances passées, les évaluations des employés et les rétroactions pour fournir des recommandations sur les promotions et les formations nécessaires. Les applications d’IA peuvent également être très utiles dans le processus de dotation des ressources humaines.

Optimisation des réunions du conseil

L’IA peut automatiser la préparation des réunions du conseil d’administration, en rassemblant et en analysant les documents pertinents, en générant des résumés et en proposant des ordres du jour optimisés. Cela permet de gagner du temps et d’assurer que les discussions se concentrent sur les sujets les plus critiques.

Surveillance des médias et de la réputation

L’IA peut analyser des millions de sources de médias, y compris les réseaux sociaux, pour surveiller la réputation de l’entreprise en temps réel. Cela permet aux conseils d’administration de réagir rapidement aux crises potentielles, de comprendre les perceptions publiques et de prendre des mesures proactives pour protéger la notoriété de l’entreprise.

Aide à la décision stratégique

Des outils d’IA avancés peuvent simuler différents scénarios stratégiques et évaluer leurs impacts potentiels. Par exemple, avant de décider d’une fusion ou d’une acquisition, le conseil d’administration peut utiliser des modèles d’IA pour simuler les impacts financiers, organisationnels et culturels de la transaction.

Les défis et les considérations éthiques

Bien que l’IA offre de nombreux avantages, son adoption dans les conseils d’administration n’est pas sans défis. Les questions de confidentialité des données, de biais algorithmique et de transparence des décisions prises par l’IA sont des préoccupations majeures.

Confidentialité et sécurité des données

Les conseils d’administration traitent souvent des informations confidentielles et sensibles. Il est crucial de garantir que les données utilisées par les outils d’IA sont protégées contre les cyberattaques et les fuites de données. Les entreprises doivent mettre en place des protocoles de sécurité robustes et s’assurer que les fournisseurs de solutions d’IA respectent les normes de confidentialité les plus strictes.

Biais algorithmique

Les algorithmes d’IA sont aussi bons que les données sur lesquelles ils sont formés. Si ces données sont biaisées, les décisions prises par l’IA peuvent également être biaisées. Par exemple, un algorithme de recrutement basé sur l’IA pourrait discriminer involontairement certains groupes de candidats s’il est formé sur des données historiques biaisées. Il est essentiel de surveiller et d’auditer régulièrement les algorithmes pour détecter et corriger les biais potentiels.

Transparence et explicabilité

Les décisions prises par les outils d’IA doivent être transparentes et explicables. Les conseils d’administration doivent comprendre comment les algorithmes arrivent à leurs conclusions pour pouvoir les défendre auprès des parties prenantes et des régulateurs. L’utilisation de modèles d’IA explicatifs, qui permettent de comprendre les facteurs influençant les décisions, est cruciale. Les administrateurs doivent questionner les dirigeants sur le sens des résultats générés par cette nouvelle technologie.

Responsabilité et gouvernance

L’adoption de l’IA dans les conseils d’administration nécessite une nouvelle approche de la gouvernance. Il est important de définir clairement les responsabilités en matière de prise de décision assistée par l’IA. Les conseils d’administration doivent également établir des cadres de gouvernance de l’IA pour garantir une utilisation éthique et responsable de la technologie.

Conclusion

L’intégration de l’intelligence artificielle dans les conseils d’administration offre un potentiel immense pour améliorer la prise de décision, l’efficacité et la réactivité. Cependant, il est essentiel de naviguer avec prudence en tenant compte des défis éthiques, de confidentialité et de biais potentiels. En adoptant une approche équilibrée, les conseils d’administration peuvent tirer parti des avantages de l’IA tout en minimisant les risques associés.

L’IA n’est pas une solution miracle, mais un outil puissant qui, lorsqu’il est utilisé de manière judicieuse, peut transformer la façon dont les conseils d’administration fonctionnent et prennent des décisions stratégiques.

La question de la diversité au sein des conseils d’administration (CA) est importante en soi, mais au-delà de l’aspect normatif, ce que les conseillers en gouvernance veulent connaître, c’est si ce facteur a une réelle incidence sur la performance des organisations.

Voici une présentation plus détaillée de l’impact de la diversité des conseils d’administration (CA) sur la performance de l’organisation et sur la prise en considération des parties prenantes.

Quelles sont les raisons qui incitent les CA à adopter une plus grande diversité ?

Il existe, à notre avis, plusieurs raisons pour lesquelles les conseils d’administration (CA) sont de plus en plus incités à adopter une plus grande diversité au sein de leur composition :

Importance de compter sur des perspectives variées : La diversité au sein du CA apporte une variété de perspectives, d’expériences et de compétences, ce qui peut enrichir les débats et les prises de décision. Des membres issus de différents horizons peuvent apporter des idées innovantes et des solutions créatives aux problèmes rencontrés par l’entreprise.

Familiarisation avec la clientèle et adaptation aux marchés : Dans un monde de plus en plus globalisé et diversifié, il est essentiel pour les entreprises de refléter la diversité de leur clientèle et de leurs marchés. Avoir un CA diversifié peut aider l’entreprise à mieux comprendre et répondre aux besoins et aux attentes de sa clientèle.

Raffermissement dela notoriété : Les entreprises qui prônent la diversité et l’inclusion au sein de leur CA peuvent bénéficier d’une meilleure réputation et être perçues comme des employeurs attractifs et socialement responsables. Cela peut également renforcer la confiance des investisseurs, des clients et des autres parties prenantes.

Lutte contre la discrimination : En favorisant la diversité au sein de leur CA, les entreprises envoient un signal fort contre la discrimination et l’exclusion. Cela peut contribuer à promouvoir l’égalité des chances et à lutter contre les préjugés et les stéréotypes.

Performance accrue : De nombreuses études ont montré que les entreprises avec des CA diversifiés ont tendance à être plus performantes sur le plan financier. La diversité peut favoriser l’innovation, la résilience et la prise de décision collective, ce qui peut avoir un impact positif sur la rentabilité et la croissance de l’entreprise.

Quel est l’impact de la diversité des conseils d’administration (CA) sur la performance de l’organisation ?

Il y a de nombreuses recherches empiriques qui montrent que la diversité au sein des conseils d’administration (CA) a une influence positive sur la performance de l’organisation. Voici quelques exemples de ces recherches :

Une étude menée par Catalyst (1) en 2011 a révélé que les entreprises ayant des conseils d’administration plus diversifiés sur le plan ethnique et de genre ont tendance à obtenir de meilleurs résultats financiers que celles dont les conseils sont moins diversifiés.

Une méta-analyse réalisée par Richard et Johnson (2) en 2001 a montré que la diversité des conseils d’administration est positivement associée à la performance financière des entreprises.

Une étude menée par Adams et Ferreira (3) en 2009 a montré que la diversité des conseils d’administration est positivement liée à l’innovation et à la prise de décision plus efficace dans les entreprises.

Une recherche menée par Carter et ses collègues (4) en 2003 a révélé que la diversité des conseils d’administration est associée à une meilleure surveillance des dirigeants et à une réduction du risque de faillite.

En résumé, de nombreuses recherches empiriques suggèrent que la diversité des conseils d’administration est bénéfique pour la performance des organisations, en favorisant l’innovation, la prise de décision efficace, la surveillance des dirigeants et les résultats financiers.

En quoi la diversité au sein d’un CA est-elle compatible avec la composition d’un CA qui reflète la préoccupation pour les parties prenantes ?

La diversité au sein d’un conseil d’administration (CA) est essentielle pour assurer une représentation équilibrée des parties prenantes et pour favoriser une prise de décision plus éclairée et inclusive. Lorsque le CA est composé de membres provenant de différentes origines, expériences, compétences et perspectives, cela permet de mieux refléter la diversité des parties prenantes de l’entreprise et d’apporter une plus grande variété d’idées et de points de vue dans les discussions et les prises de décision.

En intégrant des membres issus de différentes cultures, sexes, générations, domaines d’expertise, etc., au sein du CA, cela permet de mieux prendre en compte les intérêts et les besoins de l’ensemble des parties prenantes de l’entreprise, y compris les employés, les actionnaires, les clients, les fournisseurs, la communauté locale, etc. Une diversité au sein du CA peut également contribuer à renforcer la responsabilité sociale de l’entreprise en favorisant une meilleure prise en compte des enjeux sociaux, environnementaux et de gouvernance dans la stratégie et les décisions de l’entreprise.

Par conséquent, la diversité au sein du CA est parfaitement compatible avec une composition du CA qui reflète la préoccupation pour les parties prenantes. En favorisant une représentation équilibrée des parties prenantes et en intégrant des perspectives variées au sein du CA, l’entreprise peut mieux répondre aux attentes et aux besoins de l’ensemble de ses parties prenantes, ce qui contribue à renforcer sa légitimité, sa durabilité et sa performance à long terme.

Qu’entend-on par les parties prenantes de l’organisation ?

Les parties prenantes sont toutes les personnes ou entités qui sont directement ou indirectement affectées par les activités, les décisions et les performances d’une entreprise. Elles peuvent être internes à l’entreprise (employés, actionnaires, dirigeants) ou externes à l’entreprise (clients, fournisseurs, communauté locale, autorités réglementaires, OBLN, etc.).

La prise en compte des parties prenantes est un élément clé de la responsabilité sociale des entreprises et de la gouvernance d’entreprise, car elle vise à assurer une gestion plus éthique, transparente et durable de l’entreprise. Voici quelques exemples de parties prenantes et de leur importance dans la gouvernance d’entreprise :

Les employés : Les employés sont des parties prenantes essentielles pour toute entreprise, car ce sont eux qui contribuent directement à la réalisation des objectifs de l’entreprise. Il est important de prendre en compte leurs besoins, leurs attentes et leurs préoccupations pour favoriser un climat de travail positif, une motivation accrue et une meilleure performance globale de l’entreprise.

Les actionnaires : Les actionnaires sont des parties prenantes clés en tant que propriétaires de l’entreprise. Il est important de les informer régulièrement, de consulter leurs avis et de prendre en compte leurs intérêts à long terme dans les décisions stratégiques de l’entreprise.

Les clients : Les clients sont des parties prenantes importantes, car ce sont eux qui consomment les produits ou services de l’entreprise. Il est essentiel de les satisfaire, de répondre à leurs besoins et attentes, et de garantir la qualité et la sécurité des produits ou services fournis.

Les fournisseurs : Les fournisseurs sont des parties prenantes essentielles, car ils contribuent à la chaîne de valeur de l’entreprise en fournissant des matières premières, des services ou des produits. Il est important de maintenir des relations équitables et durables avec les fournisseurs, et de veiller à des pratiques d’approvisionnement responsables.

Les investisseurs : Les investisseurs sont également des parties prenantes importantes dans le processus de gouvernance d’entreprise. En tant que détenteurs de capitaux investis dans l’entreprise, les investisseurs ont un intérêt direct dans la performance financière et la valeur de l’entreprise. Il est essentiel pour l’entreprise de maintenir une relation transparente et constructive avec ses investisseurs pour assurer sa pérennité et sa croissance à long terme.

La communauté locale : La communauté locale est une partie prenante importante, car elle est directement impactée par les activités de l’entreprise

Quel est le rôle des différents intervenants dans le processus de gouvernance d’entreprise ?

Voici, à titre d’exemple, une classification des différents acteurs dans le processus de gouvernance des entreprises :

Les administrateurs : Les administrateurs sont les membres du conseil d’administration (CA) de l’entreprise. Leur rôle est de représenter les intérêts des actionnaires et de superviser la direction de l’entreprise. Ils sont responsables de prendre des décisions stratégiques, de contrôler la gestion de l’entreprise et de veiller à la création de valeur à long terme pour les actionnaires. Ils doivent prendre en considération l’impact de leurs décisions sur les parties prenantes de l’organisation.

Les dirigeants: Les dirigeants sont les membres de la direction de l’entreprise, tels que le PDG, le directeur financier, le directeur des opérations, etc. Leur rôle est de gérer au quotidien les activités de l’entreprise, de mettre en œuvre la stratégie définie par le CA, de prendre des décisions opérationnelles et de veiller à la performance et à la rentabilité de l’entreprise.

Les actionnaires : Les actionnaires sont les propriétaires de l’entreprise, détenant des parts sociales qui leur confèrent des droits, tels que le droit de vote en assemblée générale, le droit aux dividendes, etc. Leur rôle est de participer à la gouvernance de l’entreprise en élisant les membres du CA, en votant sur les résolutions importantes et en contrôlant la gestion de l’entreprise.

Les parties prenantes externes: Les parties prenantes externes sont toutes les personnes ou entités qui sont directement ou indirectement affectées par les activités de l’entreprise, telles que les clients, les fournisseurs, les investisseurs, la communauté locale, les autorités publiques, etc. Leur rôle est d’exprimer leurs attentes, leurs besoins et leurs préoccupations vis-à-vis de l’entreprise, et d’interagir avec celle-ci pour influencer ses décisions et ses pratiques.

Les parties prenantes internes : Les parties prenantes internes sont les personnes qui travaillent au sein de l’entreprise, telles que les employés, les syndicats, les comités d’entreprise, etc. Leur rôle est de contribuer à la performance et au succès de l’entreprise en apportant leur expertise, leur engagement et leur implication dans les activités de l’entreprise.

Enfin, j’aimerais attirer votre attention sur un modèle de gouvernance prôné par André Coupet (5), et qui est connu sous le nom d’entreprise progressiste. L’entreprise progressiste contribue à deux objectifs : « la prospérité économique de l’organisation d’une part et le bien-être de l’humanité d’autre part. Elle s’inscrit dans une économie de marché avec clairement une finalité au service de l’homme, et non l’inverse ».

Vous pouvez consulter les études citées dans cet article pour obtenir plus d’informations sur les résultats et les méthodologies utilisées dans ces recherches.

Richard, O. C., & Johnson, N. B. (2001), Understanding the impact of human resource diversity practices on firm performance. Journal of Managerial Issues, 13(2), 177-195.

Adams, R. B., & Ferreira, D. (2009), Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291-309.

Carter, D. A., Simkins, B. J., &. Simpson, W. G. (2003), Corporate governance, board diversity, and firm value. Financial Review, 38(1), 33-53

Aujourd’hui, je vous propose la présentation de l’excellent article de mon collègue André Coupet, rédigé en collaboration avec Pierre Victoria, et paru sur le site de la Fondation Jean Jaurès.

Cet article est un formidable plaidoyer en faveur de l’adoption d’une nouvelle gouvernance des sociétés. Vous trouverez, ci-dessous, un résumé de l’article de 19 pages.

La théorie des parties prenantes est une approche à la gouvernance des entreprises qui consiste à prendre en compte les intérêts et les attentes de tous les acteurs qui ont une influence ou sont influencés par les activités de l’entreprise.

Selon cette théorie, l’entreprise n’a pas seulement une responsabilité envers ses actionnaires, mais aussi envers ses salariés, ses clients, ses fournisseurs, ses partenaires, ses concurrents, la société civile et l’environnement. L’objectif est de créer de la valeur pour l’ensemble des parties prenantes et de favoriser la coopération plutôt que la rivalité.

La théorie des parties prenantes repose sur une vision élargie de la gouvernance, qui implique une négociation et une participation des parties prenantes aux décisions stratégiques.

Les avantages de cette théorie sont les suivants :

Elle permet de prendre en considération les intérêts et les attentes de tous les acteurs liés à l’entreprise, ce qui peut favoriser la création de valeur partagée, la coopération, la confiance, la légitimité et la réputation de l’entreprise.

Elle encourage l’entreprise à adopter une vision à long terme, à intégrer les enjeux sociaux et environnementaux dans sa stratégie, à être plus transparente et responsable vis-à-vis de ses parties prenantes.

Elle offre à l’entreprise une meilleure compréhension de son environnement, de ses opportunités et de ses risques, ainsi qu’une plus grande capacité d’adaptation et d’innovation face aux changements.

Bref résumé de l’article :

Les auteurs analysent les évolutions du capitalisme et les limites du modèle actionnarial, qui privilégie les intérêts des actionnaires au détriment des autres acteurs liés à l’entreprise, tels que les salariés, les clients, les fournisseurs, la société civile ou l’environnement.

Ils proposent de passer à un modèle alternatif, fondé sur la prise en compte des parties prenantes dans la gouvernance de l’entreprise, ce qui implique une transformation en profondeur de sa vision, de son partage du pouvoir et de la valeur créée, et de sa mesure de la performance.

Ils suggèrent trois mesures concrètes pour mettre en œuvre cette approche :

Énoncer une raison d’être de l’entreprise, qui exprime sa contribution positive à la société et qui guide ses décisions stratégiques.

Créer un comité des parties prenantes, qui représente les différents acteurs concernés par l’activité de l’entreprise et qui dialogue avec le conseil d’administration et la direction sur les enjeux sociaux, environnementaux et sociétaux.

Ouvrir le conseil d’administration à une gouvernance tripartite, qui associe les actionnaires, les salariés et les parties prenantes externes, afin de favoriser la diversité des points de vue et la prise en compte de l’intérêt général.

Cette publication montre clairement ce qui fera l’objet des sujets à l’ordre du jour des conseils d’administration pour les années à venir. J’ai utilisé l’outil de traduction Google pour présenter le texte en français lequel a subi de multiples ajustements.

Les CA sont toujours intéressés par les nouvelles préoccupations en matière de gouvernance.

L’ordre du jour du conseil d’administration s’est d’abord concentré sur les « sujets brûlants » de l’année à venir en janvier 2018. [1] Regarder cette publication cinq ans plus tard est instructif ; il nous rappelle que même si de nombreux nouveaux sujets sont susceptibles d’être à l’ordre du jour du conseil en 2023, certains sujets continuent d’être au premier plan des considérations du conseil, même si les détails ont changé à certains égards.

Bien sûr, de nombreuses questions ont été ajoutées à l’ordre du jour du conseil depuis 2018 et resteront des priorités en 2023. Les nouvelles questions les plus importantes concernent peut-être le rôle de la société dans la société en général. Ce sujet a fait l’objet d’une attention particulière en 2019, lorsque la Business Roundtable a publié sa « Déclaration sur l’objet de la société » [2] menant à des discussions sur la question de savoir si les sociétés ont des obligations envers des groupes autres que les actionnaires, tels que les employés, les clients, les fournisseurs et les communautés dans lesquelles elles opèrent. Parmi les autres préoccupations sociétales qui ont eu un impact sur les salles de conseil, citons une myriade d’événements qui peuvent avoir contribué à l’orientation plus large de DE&I, ce qui a conduit les entreprises et leurs conseils d’administration à se demander s’ils offrent des environnements de travail équitables et inclusifs, et la pandémie de COVID-19, qui continue d’avoir un impact sur les entreprises en ce qui concerne des questions telles que la santé et le bien-être des employés et la nature fondamentale du travail et du lieu de travail.

Nous discutons ci-dessous de certains des sujets critiques qui sont restés relativement constants au cours des cinq dernières années, ainsi que des sujets nouveaux et émergents qui seront probablement à l’ordre du jour du conseil en 2023.

Composition et compétences du conseil

En 2023 comme en 2018, la composition du conseil est un domaine d’intérêt principal pour les conseils. De plus, certaines des questions que les conseils d’administration aborderont probablement en 2023 ont également des implications importantes pour la composition du conseil d’administration.

La cybersécurité est l’une de ces questions. Cela reste une préoccupation majeure pour les entreprises et leurs conseils d’administration, et de nombreux conseils d’administration ont envisagé l’opportunité d’ajouter des administrateurs possédant une gamme de compétences allant de l’expertise en cyberrisque à la maîtrise générale de la technologie. Ce sujet a été abordé en 2022 dans les propositions de la Securities and Exchange Commission (SEC) qui imposeraient de nouvelles exigences de divulgation concernant la cybersécurité, y compris « si un membre du… conseil d’administration possède une expertise en cybersécurité et, le cas échéant, la nature de cette expertise ». [3] Un certain nombre de commentaires soumis à la SEC sur cette proposition remettent en question la nécessité et l’opportunité de cette exigence, notant qu’il n’est pas possible d’ajouter un « expert » sur chaque sujet que les conseils doivent aborder et que d’autres administrateurs peuvent se fier indûment sur un « expert » sur un sujet donné.

Cependant, que cette exigence soit adoptée telle qu’elle a été proposée, retirée de la règle finale ou quelque chose entre les deux, les conseils d’administration resteront presque certainement concentrés sur la présence d’un ou plusieurs membres ayant un certain degré d’expérience ou de connaissances en technologie.

D’autres domaines d’intérêt du conseil en développement ont également des répercussions sur la composition du conseil. Les données suggèrent que les entreprises ne cherchent plus à limiter les recherches de nouveaux membres du conseil d’administration aux personnes qui occupent ou ont déjà occupé le poste de directeur général. [4] De plus en plus, les conseils d’administration recherchent des administrateurs ayant de l’expérience dans les domaines où leurs entreprises ont les plus grands besoins ; les entreprises en contact direct avec les consommateurs peuvent chercher à ajouter des administrateurs ayant une expérience en marketing ; les entreprises ayant des opportunités de stratégie en matière de capital humain peuvent envisager d’ajouter des administrateurs qui ont servi comme CHRO ou dans des fonctions similaires ; et les entreprises ayant des activités internationales peuvent envisager d’ajouter des administrateurs ayant une formation en géopolitique.

Technologie et cyberrisque

Il y a cinq ans, la discussion sur les risques technologiques se concentrait presque entièrement sur les risques associés aux nouvelles technologies, tels que les risques perturbateurs et les problèmes éthiques associés à l’utilisation de l’intelligence artificielle (IA) ; Le « piratage » a été mentionné, mais il ne semble pas avoir été un sujet de préoccupation majeure.

Alors que les risques, les défis et les opportunités associés aux perturbations et à l’utilisation de l’IA restent à l’ordre du jour du conseil d’administration, la discussion s’est clairement déplacée vers la cybersécurité, reflétant peut-être l’augmentation du nombre et de la gravité des cyberattaques ainsi que le plus grand degré de confiance désormais placé sur les infrastructures numériques. Comme indiqué ci-dessus, la cybersécurité est devenue suffisamment importante pour générer des propositions de la SEC qui élargiraient considérablement les divulgations sur le sujet, y compris la mesure dans laquelle le conseil s’appuie sur des employés et/ou des conseillers externes pour l’aider à s’acquitter de ses fonctions de surveillance en matière de cybersécurité, comment souvent, le conseil discute de la cybersécurité et si le conseil comprend des personnes ayant une expertise en cybersécurité. Le conseil d’administration devra peut-être participer aux discussions sur l’infrastructure et l’architecture technologique plus large compte tenu des implications sur les risques, l’innovation, les implications éthiques potentielles et les contrôles. Même en l’absence d’exigences de la SEC, les investisseurs continueront probablement à s’attendre à ce que les conseils d’administration traitent les risques de cybersécurité et divulguent comment les conseils d’administration le font.

Stratégie et risque

Bien que certains sujets à l’ordre du jour des conseils d’administration de 2018 se soient estompés et que de nouveaux points soient apparus, la stratégie et le risque sont des éléments pérennes en tête de l’ordre du jour du conseil, au sens figuré sinon au sens littéral. En fait, l’expérience montre que les conseils d’administration se concentrent encore plus sur la supervision des stratégies de leurs entreprises. Il est révolu le temps où les conseils d’administration et les membres supérieurs de la direction organisaient une retraite stratégique annuelle, mais se concentraient rarement, voire jamais, sur la stratégie jusqu’à la prochaine retraite. Aujourd’hui, les conseils d’administration discutent régulièrement d’un aspect de la stratégie au plus, sinon à toutes les réunions, en posant des questions telles que celles-ci : « Quelles mesures avons-nous prises pour mettre en œuvre notre stratégie ? » « Où en sommes-nous dans le processus de mise en œuvre ? » « Notre stratégie s’avère-t-elle viable ? “A-t-elle besoin d’être peaufinée, de subir des ajustements importants, ou d’être abandonné ? « Avons-nous besoin de pivoter compte tenu des risques associés à certains objectifs stratégiques ? » Et ainsi de suite.

La surveillance des risques demeure également un point prioritaire à l’ordre du jour des conseils d’administration, d’autant plus que le nombre et la gravité des risques semblent augmenter de jour en jour. Par exemple, en 2018, peu d’entreprises, voire aucune, n’avaient prévu les risques d’une pandémie mondiale, les perturbations qu’elle entraînerait dans les chaînes d’approvisionnement mondiales, les défis économiques actuels et les domaines prioritaires du capital humain tels que la santé au travail, le bien-être et les risques culturels globaux.

En raison de la prolifération de nouveaux risques, les conseils d’administration — et les comités d’audit — peuvent vouloir réexaminer les programmes de risque d’entreprise de leurs entreprises pour déterminer si ces programmes traitent de nouveaux risques et ne deviennent pas un simple processus de « cocher la case ». Pour surveiller efficacement ces risques, les comités d’audit devraient recevoir un tableau de bord des risques les plus importants pour s’assurer que de nouveaux risques sont ajoutés et pour faciliter la compréhension de la façon dont les vulnérabilités aux risques spécifiques et les niveaux d’impact changent d’un trimestre à l’autre.

Questions relatives au lieu de travail et à la main-d’œuvre

Dès septembre 2020, il a été reconnu que les stratégies de main-d’œuvre devenaient aussi importantes que les stratégies commerciales pour les conseils d’administration :

‘Les événements liés à la pandémie… ont propulsé la gestion des effectifs au premier plan des programmes des conseils d’administration. Dans de nombreux cas, une réflexion tardive de la stratégie commerciale et technologique, la gestion de la main-d’œuvre est désormais une priorité majeure, sur un pied d’égalité avec d’autres domaines clés sur lesquels le conseil d’administration se concentre. [5]

Bien que la pandémie de COVID-19 ait pu précipiter l’attention du conseil sur les questions de main-d’œuvre, d’autres préoccupations ont renforcé la nécessité d’une plus grande attention du conseil sur le sujet :

‘… [Les commissions commencent à reconnaître que l’agence est passée des employeurs aux travailleurs ; la main-d’œuvre recherche un travail plus significatif, une plus grande concentration sur le bien-être avec des considérations telles qu’une plus grande flexibilité de temps et de lieu, et des modèles d’emploi et des parcours de carrière plus personnalisés et agiles. Selon le Bureau of Labor Statistics des États-Unis, 47,8 millions de personnes aux États-Unis ont quitté leur emploi en 2021, le plus grand nombre enregistré… depuis au moins 2001. Dans ce qui a été surnommé ‘la grande démission’, les démissions ont représenté 69,3 % du total des séparations en 2021. » [6]

Les exigences réglementaires ont également amené les conseils à se concentrer sur les questions liées au lieu de travail. Fin 2020, la SEC a adopté de nouvelles exigences de divulgation relatives aux ressources en capital humain. [7] Et la SEC a indiqué que davantage d’exigences de divulgation à ce sujet sont susceptibles d’être imposées à court terme.

Quelles qu’en soient les causes, les conseils d’administration se sont beaucoup plus concentrés sur les lieux de travail et les effectifs de leurs entreprises que par le passé, lorsque les questions relatives aux employés étaient autrefois considérées comme relevant principalement, sinon exclusivement, de la timonerie de la direction.

Changement climatique

Alors que les impacts du changement climatique sont devenus plus apparents ces dernières années, les investisseurs — principalement de nombreux grands investisseurs institutionnels — ont de plus en plus pressé les entreprises de prêter attention au changement climatique, souvent en cherchant à s’engager à réduire les émissions ou à prendre d’autres mesures concrètes. Associée à cette pression, on s’attend à ce que les conseils d’administration élargissent leur surveillance pour examiner le rôle de leurs entreprises dans le changement climatique, et voir comment ce rôle devrait changer. Dans certains cas, les investisseurs ont poussé à redoubler d’efforts pour atteindre la ‘durabilité’, c’est-à-dire s’assurer que les activités de l’entreprise peuvent rester viables et se développer ; dans d’autres, l’objectif est plus large : s’attaquer au changement climatique sur une base plus large.

Bien sûr, il existe de nombreuses réglementations entourant le changement climatique à tous les niveaux de gouvernement – local, étatique et fédéral. Cependant, jusqu’à relativement récemment, cela ne semblait pas être une priorité de l’ordre du jour de la SEC. Cela a commencé à changer à la fin de 2020, alors que des commissaires individuels ont prononcé des discours ou d’autres déclarations publiques sur l’importance de la divulgation du changement climatique, et le personnel de la SEC a intensifié son examen des divulgations, ou, dans certains cas, de l’absence de divulgation, concernant le changement climatique et son impact sur le présent et l’avenir de l’entreprise. Plus récemment, en 2022, la SEC a proposé des exigences de divulgation étendues dans ce domaine, y compris des divulgations concernant les émissions, la surveillance du conseil d’administration et d’autres questions. Les propositions ont reçu plus de 14 000 commentaires, ce qui pourrait être un record, et l’adoption de règles définitives sur le sujet peut entraîner des litiges contestant la règle. Dans l’intervalle, cependant, de nombreux conseils s’intéressent à la question et y prêteront certainement plus d’attention en 2023.

Le rôle de l’entreprise dans la société

Peut-être qu’aucun sujet commercial n’a suscité autant de controverse ces dernières années que le rôle de l’entreprise dans la société. La déclaration de la table ronde des entreprises de 2019 évoquée ci-dessus a peut-être suscité des conversations entre les parties prenantes, ce qui a accru les attentes des entreprises d’aujourd’hui. Par exemple, parmi les 10 principales conclusions du baromètre de la confiance Edelman 2022 figurait que ‘les entreprises doivent intensifier leurs efforts sur les questions de société’, ‘le leadership sociétal est désormais une fonction essentielle des entreprises’ et ‘les entreprises doivent montrer la voie pour briser le cycle de la méfiance. .’ [8]Certaines entreprises ont répondu à ces attentes en s’exprimant ouvertement sur les questions sociales, tandis que d’autres ont fait l’objet de critiques de la part des clients et des salariés. Il est important que les conseils d’administration travaillent avec la direction pour s’assurer qu’ils discutent et, dans certains cas, ont une politique sur la façon dont, le cas échéant, l’entreprise s’exprimera publiquement sur ces sujets sensibles, en d’autres termes, quelle que soit la position de l’entreprise sur la responsabilité sociale, son conseil d’administration doit être attentif au sujet et guider la direction en conséquence.

Il est également essentiel de noter que le rôle de la société dans la société est sans doute un défi unique pour les conseils, car, contrairement aux autres questions abordées ci-dessus, il n’a pas été considéré comme une partie essentielle du rôle du conseil jusqu’à très récemment. Les entreprises traitent depuis longtemps les problèmes des employés et de la main-d’œuvre, même si leurs conseils d’administration ont largement laissé ces problèmes à la direction. De même, les entreprises ont longuement réfléchi aux aspects de la durabilité ; par exemple, les entreprises de ressources naturelles ont dû tenir compte de l’épuisement des ressources, et les entreprises opérant dans des zones sujettes à des conditions météorologiques violentes ou sismiques ont pesé ces problèmes pendant de nombreuses années. En revanche, la responsabilité sociale, qui est étroitement liée à l’activisme social, est un phénomène relativement récent qui peut présenter des défis uniques pour les conseils d’administration.

Enfin, le conseil lui-même

Les sujets abordés ci-dessus ne représentent qu’un échantillon de ce qui apparaîtra probablement à l’ordre du jour des conseils d’administration en 2023. Il y a beaucoup, beaucoup plus de sujets qui pourraient être discutés, y compris de nombreux sujets pérennes ainsi que de nombreux nouveaux.

En d’autres termes, les conseils ont beaucoup à faire. Et bien que les statistiques indiquent que le temps que les administrateurs consacrent aux affaires du conseil augmente, il y a une limite au temps qu’ils peuvent y consacrer. En conséquence, il semble qu’un autre point à l’ordre du jour du conseil d’administration de 2023 sera l’efficacité du conseil lui-même. Les conseils d’administration cherchent à développer et à améliorer des moyens de faire les choses plus efficacement, allant d’une plus grande utilisation des soi-disant ‘programmes de consentement’ à l’optimisation des rôles des comités, ou éventuellement à la formation de comités supplémentaires, pour s’acquitter de la myriade de responsabilités du conseil.

Attentes pour l’avenir

Il semble certain que les responsabilités des conseils d’administration continueront d’augmenter, peut-être à un rythme rapide, et que peu de sujets auxquels les conseils d’administration seront confrontés disparaîtront ou deviendront plus faciles à gérer. Cependant, il y a lieu d’être optimiste. Au fil des décennies, et certainement au cours des cinq dernières années, les conseils d’administration ont démontré qu’ils sont remarquablement résilients et capables de relever des défis que personne n’avait anticipés. En fait, nous pouvons regarder en arrière dans cinq ans et nous demander pourquoi nous étions inquiets.

Voici un cas d’actualité présenté par Lucian A. Bebchuk, Kobi Kastiel et Anna Toniolo* (Harvard Law School) sur le Forum du HLS on Corporate Governance.

L’analyse fait clairement ressortir que, dans le cas de la transaction d’achat de Twitter par Elon Musk, les dirigeants de l’entreprise n’ont accordé aucune importance aux parties prenantes, notamment aux employés (qui ont été poussés sous le bus).

Les auteurs constatent « que l’on ne peut pas s’attendre à ce que les dirigeants d’entreprise qui vendent une entreprise veillent aux intérêts de leurs parties prenantes ».

La direction de Twitter a choisi d’allouer le produit de la vente de l’entreprise entièrement aux actionnaires, et à elle-même !

De plus, l’analyse du cas Twitter montre que l’on remet facilement en question l’importance des beaux énoncés concernant la mission, le but et les valeurs fondamentales de l’entreprise, lorsque le gain est très important .

J’ai corrigé la version traduite par Google, et le résultat final me semble très acceptable.

Vos commentaires sont bienvenus. Bebchuk ne fait pas toujours l’unanimité…

Notre essai à paraître, « Comment Twitter a poussé ses parties prenantes sous le bus », propose une étude de cas sur l’acquisition de Twitter par Elon Musk. Compte tenu du fort intérêt actuel pour cette acquisition, nous discutons, dans cet article et les suivants, de certaines de nos conclusions et de leurs implications pour les débats actuels sur le capitalisme des parties prenantes.

Une bataille épique a été menée cette année entre Twitter et Elon Musk après que Musk ait tenté de se retirer de l’accord d’acquisition entre eux. Twitter a gagné, et ses actionnaires et dirigeants ont ainsi obtenu d’importants gains financiers.

Alors que la bataille entre ces deux parties a attiré une couverture médiatique massive, nous pensons qu’une attention insuffisante a été accordée à un autre groupe qui devait être affecté par l’accord — les « parties prenantes » de Twitter (c’est-à-dire les composantes non-actionnaires). En particulier, notre analyse conclut que, malgré leur rhétorique des parties prenantes au fil des ans, lors de la négociation de l’accord, les dirigeants de Twitter ont choisi de pousser leurs parties prenantes sous le bus de Musk.

Ce n’est pas parce que la direction de Twitter a été bousculés par Musk. Au contraire, les dirigeants de Twitter ont obtenu de Musk, (et ils se sont battus pour le conserver), d’importants gains monétaires pour les actionnaires (une prime d’environ 10 milliards de dollars), ainsi que pour les dirigeants eux-mêmes (qui, ensemble, ont réalisé un gain de plus d’un milliard de dollars grâce à l’accord). En se concentrant exclusivement sur ces gains monétaires cependant, la direction de Twitter a choisi de ne pas tenir compte des intérêts des parties prenantes.

C’est ainsi que les employés de Twitter, que l’entreprise appelait affectueusement « tweeps » ont été poussés sous le bus, alors que Twitter avait, depuis longtemps, promis de prendre soin d’eux. Les dirigeants de Twitter n’ont pas tenté d’évoquer avec Musk, comment les tweeps seraient affectés par l’accord négocié.

Au lieu de cela, les dirigeants de Twitter ont choisi d’allouer le très important excédent monétaire produit par l’accord entièrement aux actionnaires et aux dirigeants eux-mêmes. Ils ont choisi de n’utiliser aucune partie de cet excédent pour fournir un coussin monétaire aux tweeps qui perdraient leurs positions après la transaction. Notons, qu’allouer, ne serait-ce que 2 % des gains monétaires (qui sont finalement allés aux actionnaires et aux dirigeants d’entreprise), à la protection des employés, auraient permis de fournir un coussin monétaire substantiel aux quelque 50 % des tweeps qui ont été licenciés peu de temps après la conclusion de l’accord.

Notamment, les dirigeants de Twitter n’ont même pas mené de négociations ou de discussions avec Musk pour s’assurer que les tweeps apprendraient leurs licenciements de manière humaine, plutôt que de le déduire après avoir été déconnectés au milieu de la nuit, ou que le travail à distance, l’environnement auquel Twitter avait exprimé un engagement, serait graduel plutôt que soudain.

Les déclarations de mission et les valeurs fondamentales auxquelles les dirigeants de Twitter avaient, depuis longtemps, prêté allégeance, ont également été poussées sous le bus. Lors de la négociation des conditions de la transaction, les dirigeants de Twitter n’ont négocié avec Musk aucune contrainte ni même aucun engagement souple concernant le maintien de ces engagements après la transaction. Les dirigeants de Twitter ne semblent même pas avoir eu de discussions avec Musk concernant ses plans à cet égard, car ils ont déclaré aux employés qu’ils n’avaient aucune information sur ces plans. Les dirigeants de Twitter ont choisi de procéder de cette manière malgré les avertissements et les indications selon lesquels Musk pourrait bien abandonner tout ou partie les solides engagements de Twitter avant l’accord.

Twitter avait depuis longtemps communiqué son engagement à avoir une mission et pas seulement un objectif de profit, et à faire progresser des valeurs telles que l’intégrité civique, l’exclusion des discours de haine, le respect des droits de l’homme, et même le soutien à l’Ukraine dans sa défense contre l’agression. Mais ces engagements semblent avoir reçu peu d’attention ou de poids de la part des dirigeants de Twitter lorsqu’ils ont négocié l’accord Musk.

Au-delà de l’affaire Twitter, nos conclusions ont des implications pour le débat houleux en cours sur la gouvernance des parties prenantes. À cet égard, nos conclusions soutiennent l’idée que la rhétorique des parties prenantes des chefs d’entreprise est principalement pour le spectacle et n’est généralement pas accompagnée de choix réels (par exemple, Bebchuk et Tallarita (2020).

Nos résultats suggèrent en outre que l’on ne peut pas s’attendre à ce que les dirigeants d’entreprise qui vendent leur entreprise veillent aux intérêts des parties prenantes. Ceci est contraire aux prédictions des promesses implicites et des théories de production en équipe de Shleifer-Summers (1988), Coffee (1988) et Blair-Stout (1999), qui ont longtemps été utilisées comme argument pour donner aux dirigeants d’entreprise un droit de veto sur les acquisitions d’entreprises afin qu’ils puissent utiliser ce pouvoir pour défendre les intérêts des parties prenantes.

Enfin, notre étude de cas remet en question le point de vue qui attache de l’importance à l’adoption par les entreprises d’énoncés concernant la mission, le but et les valeurs fondamentales (par exemple, Eccles & Youmans (2016) et Mayer (2019) ). Twitter a été « long » sur de telles déclarations pendant un certain temps, mais décidément « court » sur l’une d’entre elles.

Notre analyse de l’étude de cas sur Twitter est cohérente avec les conclusions de travaux empiriques antérieurs co-écrits par deux d’entre nous. Ce travail empirique a montré que les chefs d’entreprise se sont concentrés sur les intérêts des actionnaires et des hauts dirigeants eux-mêmes, et qu’ils n’ont pas réussi à négocier la protection des parties prenantes dans deux grands échantillons de transactions :

(i) les acquisitions d’entreprises publiques pendant la période COVID au cours de laquelle la rhétorique concernant les parties prenantes était largement employée par les chefs d’entreprise ( Bebchuk, Kastiel et Tallarita (2022) ) ;

(ii) les acquisitions régies par les statuts de la constitution des États autorisant et obligeant les dirigeants vendant leur entreprise à prendre en compte les intérêts des parties prenantes ( Bebchuk, Kastiel et Tallarita (2021)). En complément de ces études, notre étude de cas Twitter actuelle fournit un exemple particulièrement frappant et puissant de la façon dont les dirigeants d’entreprise ignorent en fait les parties prenantes (et toutes rhétoriques antérieures favorable aux parties prenantes) lors de la négociation d’une vente de leur entreprise.

*Lucian Bebchuk est titulaire de la chaire James Barr Ames de droit, d’économie et de finance et directeur du programme sur la gouvernance d’entreprise à la faculté de droit de Harvard ; Kobi Kastiel est professeur agrégé de droit à l’Université de Tel-Aviv et chercheur principal du programme de la faculté de droit de Harvard sur la gouvernance d’entreprise ; et Anna Toniolo est boursière postdoctorale au Programme sur la gouvernance d’entreprise de la Harvard Law School.

Voici un texte publié par Mary Ann Deignan, Rich Thomas, et Christopher Couvelier de la firme Lazard sur le site du HBLS on Corporate Governance.

Cet article montre les principaux changements observés eu égard à l’activisme international au troisième trimestre de 2022.

Je vous invite à lire la version française de l’article, publiée sur le Forum de Harvard Law School on Corporate Governance, effectuée par Google, que j’ai corrigé.

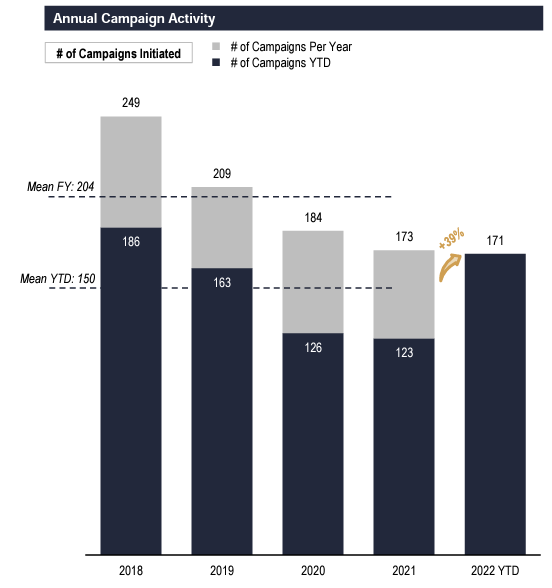

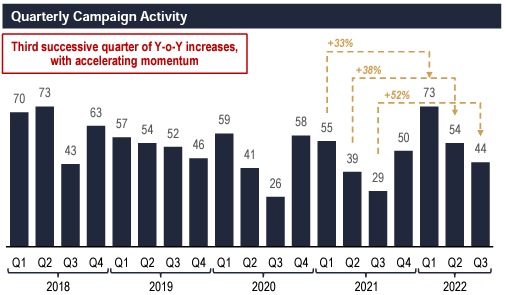

1. Poursuite d’une activité robuste alimentée par un troisième trimestre solide

44 nouvelles campagnes lancées au T3, une augmentation de 52 % par rapport au T3 de l’année précédente, marquant le troisième trimestre consécutif d’augmentation significative de l’activité d’une année sur l’autre

Nombre total de campagnes depuis le début de l’année (171) en hausse de 39 % par rapport à la même période l’an dernier, approchant déjà le total pour l’année 2021 (173)

Poursuivant une tendance au premier semestre, les entreprises technologiques ont été les plus fréquemment ciblées au troisième trimestre, représentant 22 % des nouvelles cibles activistes

Avec 5 nouvelles campagnes au troisième trimestre, Elliott a continué d’accélérer son rythme de 2022 et a maintenant lancé 11 campagnes depuis le début de l’année (plus du double des prochains noms les plus prolifiques)

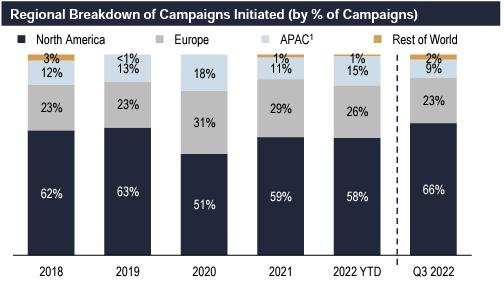

2. Cibles américaines en ligne de mire

Les cibles nord-américaines représentaient les deux tiers de toutes les nouvelles campagnes au troisième trimestre, au-dessus des niveaux du premier semestre (55 %) et de la moyenne 2018-2021 (59 %)

L’activité du troisième trimestre aux États-Unis (28 nouvelles campagnes) a représenté une augmentation de 133 % par rapport au troisième trimestre de l’année précédente (12 nouvelles campagnes)

L’activité aux États-Unis depuis le début de l’année (96 nouvelles campagnes) a augmenté de 43 % d’une année sur l’autre et correspond désormais au total de l’année 2021

Les récentes campagnes américaines ont ciblé les leaders de l’industrie des méga-capitalisations (dont Cardinal Health, Chevron, Disney, Pinterest et PayPal)

3. L’activité européenne approche déjà du niveau record de l’exercice 2021

Malgré un troisième trimestre relativement lent (10 nouvelles campagnes), l’activité depuis le début de l’année en Europe (45 campagnes) est en hausse de 32 % d’une année sur l’autre et approche déjà le total de l’année 2021 (50 campagnes)

Alors que les entreprises britanniques sont restées les cibles les plus fréquentes de l’Europe (40 % des campagnes européennes depuis le début de l’année, en ligne avec les niveaux moyens pluriannuels), la France a enregistré une part d’activité supérieure à celle des périodes précédentes (18 % des campagnes européennes, contre 12 % de 2019 à 2021)

4. Les revendications de la campagne reflètent l’approche « faites-le ou vendez-le »

Les objectifs liés aux fusions et acquisitions figuraient dans 48 % des campagnes du T3, un rebond significatif par rapport à 39 % au T2 et 32 % au T1

Les demandes « Vendre l’entreprise » depuis le début de l’année (26 campagnes) dépassent déjà les totaux annuels pour 2021 (20) et 2020 (14)

Les demandes autour de la stratégie/des opérations ont continué d’augmenter en fréquence au cours des derniers trimestres (21 % des campagnes du T3, contre 20 % au T2 et 14 % au T1) et restent supérieures à la moyenne 2018 – 2021 (15 %)

5. Thèmes émergents à surveiller

Avec la règle de procuration universelle maintenant en vigueur et une partie importante des fenêtres de nomination des sociétés ouvertes pour la saison AGA 2023 se déroulant au quatrième et au premier trimestre, les campagnes axées sur la représentation au conseil d’administration sont sur le point de se multiplier

Le rôle de l’ESG et l’attention que les entreprises et les investisseurs devraient lui accorder commencent à être remis en question

Le nouvel activiste Strive Asset Management s’en prend à plusieurs sociétés de premier ordre pour avoir donné la priorité aux problèmes E&S au détriment de la création de valeur pour les actionnaires

Le Texas a interdit à certaines entreprises et fonds (dont BlackRock) de faire des affaires dans l’État en raison de pratiques ESG en contradiction avec le secteur énergétique de l’État

Activité de campagne mondiale

L’activité YTD 2022 approche déjà les niveaux de l’année 2020 et 2021 ; alors que les tendances régionales depuis le début de l’année sont conformes aux dernières années, le troisième trimestre a vu une activité nord-américaine accrue

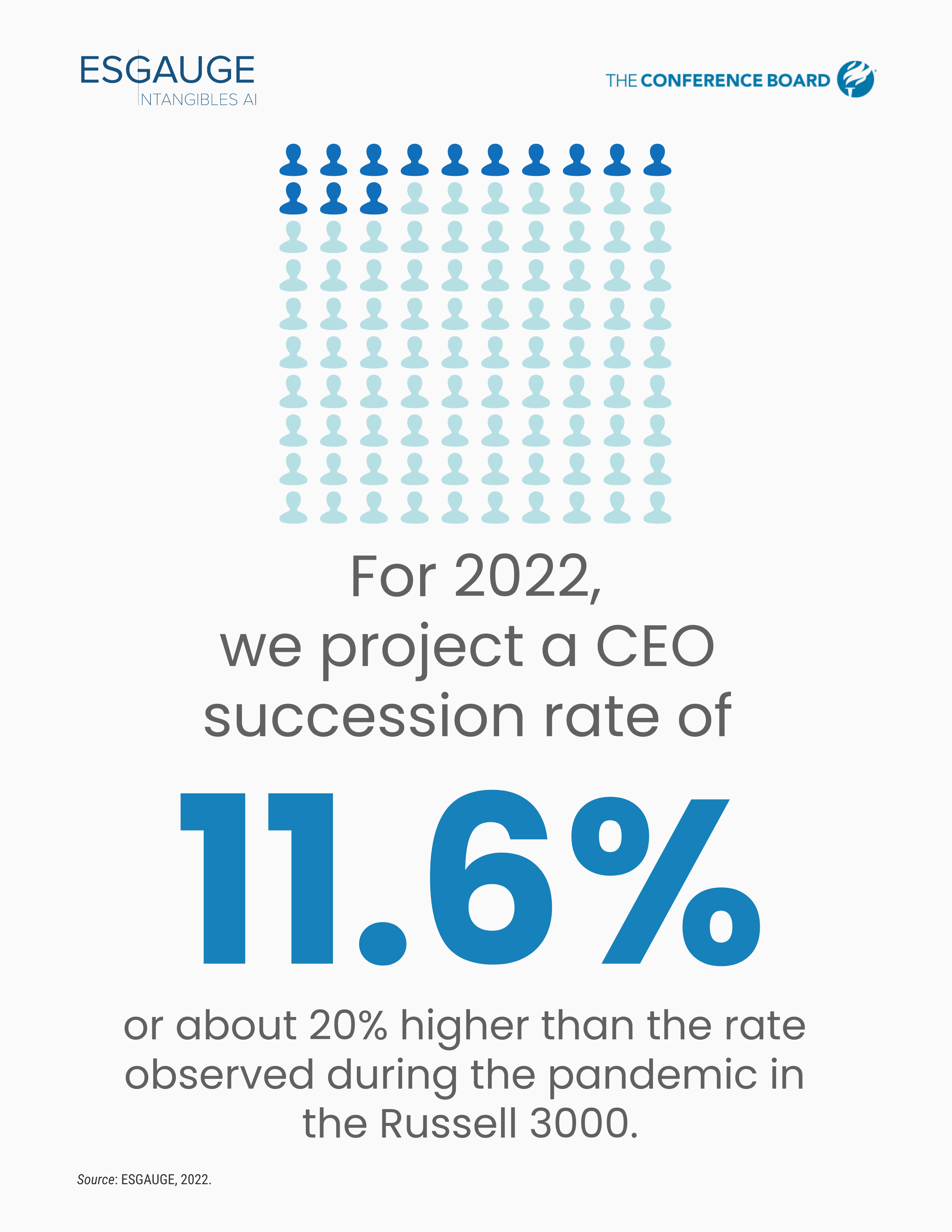

Voici le résumé d’un article, publié par Matteo Tonello* (The Conference Board, Inc.) et Jason D. Schloetzer* (Georgetown University), portant sur une étude des pratiques de successions des PDG dans le Russell 3000 et le S&P 500.

L’article est abondamment illustré et les principales conclusions sont présentées en caractère gras.

Le projet est mené par le Conference Board et la société d’analyse de données ESG ESGAUGE, en collaboration avec la société de recrutement de cadres Heidrick & Struggles.

Je vous invite à lire la version française de l’article, publiée sur le Forum de Harvard Law School on Corporate Governance, effectuée par Google, que j’ai corrigé.

Bonne lecture !

Après avoir diminué pendant la pandémie, le taux de rotation des PDG dans les entreprises publiques américaines augmente rapidement, alors que les conseils d’administration reprennent confiance dans leurs plans de succession et que les inquiétudes liées aux récessions incitent certains dirigeants de longue date à quitter leurs fonctions

Au plus fort de la pandémie, de nombreuses entreprises ont choisi d’éviter d’aggraver les risques commerciaux résultant de la crise avec les incertitudes d’un changement de direction. Une nette baisse du taux de succession des PDG en 2021 indique que, même dans les situations où un changement aurait pu être prévu, de nombreux PDG ont été invités à prolonger leur mandat et à aider à diriger le navire. Cependant, les données annualisées préliminaires sur le taux de 2022 montrent que ces chiffres antérieurs pourraient maintenant s’inverser et que cette année est sur le point d’être une année record pour les départs de PDG. Deux facteurs peuvent contribuer à expliquer ce constat.

Premièrement, de nombreux PDG sont prêts à passer à autre chose. La pression de la gestion pendant une crise sans précédent — qui, en raison de la situation géopolitique actuelle et de la perspective imminente d’une récession, n’a fait que s’accélérer au lieu de s’atténuer — a fait des ravages sur les dirigeants, en particulier ceux qui planifiaient leur retraite depuis des années. Deuxièmement, les conseils d’administration peuvent également être mieux préparés au changement. Au cours des deux dernières années, ils ont eu le temps de tester et de renforcer le plan de relève de leur entreprise, gagnant ainsi plus de confiance dans leur capacité à l’exécuter.

En 2021, le taux de succession des PDG a diminué par rapport à l’année précédente, tant dans le Russell 3000 (de 11,6 à 9,6 %) que dans le S&P 500 (de 11,1 à 10 %). Cependant, les données annualisées préliminaires pour 2022 montrent une inversion : en juillet 2022, le taux de succession annualisé était de 11,6 % dans le Russell 3000 et de 11,4 % dans le S&P 500. Une autre inversion intéressante peut être observée dans le taux de succession des PDG par Groupe d’âge : En 2021, le taux de succession des PDG parmi les PDG n’ayant pas atteint l’âge de la retraite (c’est-à-dire de moins de 64 ans) a diminué par rapport à l’année précédente, tant dans le Russell 3000 (de 9,4 à 7,4 %) que dans le S&P 500 (de 8,2 à 7,5). %), tandis que le taux de successions de PDG à l’âge de la retraite est resté stable par rapport à l’année précédente dans le Russell 3000 (de 20,5 à 20,8 %) et dans le S&P 500 (de 24,4 à 24,3 %).

Le mouvement à la hausse du taux de succession des PDG est plus prononcé dans les secteurs des services publics, de la santé et de la consommation discrétionnaire (avec des taux de succession annualisés pour 2022 de 19,6 %, 13,9 % et 13,3 %), alors qu’il est plus faible parmi les entreprises de l’immobilier. et les services de communication (7,4 et 8,7 %, respectivement). Il est intéressant de noter que le taux de succession des PDG dans le secteur discrétionnaire n’a jamais vraiment connu la baisse liée à la pandémie observée dans l’ensemble de l’indice. Le secteur comprend de nombreuses entreprises de distribution qui, depuis plusieurs années et bien avant la crise du Covid, recherchaient de nouveaux talents de leadership capables de contrer des menaces telles que le passage des consommateurs aux achats en ligne et la demande de produits nouveaux et durables. [1] La rotation des PDG dans les entreprises de consommation discrétionnaire est constamment élevée depuis plusieurs années ; au cours des derniers mois seulement, de grands détaillants tels que Gap Inc., Dollar General Corp., Bed Bath & Beyond Inc. et Under Armour Inc. ont annoncé un changement dans leur direction.

Il n’y a pas de corrélation directe entre le taux de succession et la taille des entreprises. En fait, pour les petites entreprises de l’indice Russell 3000 (c’est-à-dire dont le chiffre d’affaires annuel est inférieur à 100 millions de dollars), nous enregistrons un taux de succession annualisé du PDG pour 2022 de 14,7 %, soit à peine plus élevé que les 13,1 % de leurs homologues les plus importants (chiffre d’affaires annuel de 50 milliards de dollars ou plus). Les entreprises de taille moyenne signalent des taux inférieurs (par exemple, celles dont le chiffre d’affaires annuel se situe entre 5 et 9,9 milliards de dollars ont un taux de succession annualisé du PDG en 2022 de 7,8 %).

Les conseils d’administration ont été réticents à licencier les PDG des entreprises qui ont mal performé sur le marché boursier pendant la pandémie, compte tenu de l’évolution des objectifs de performance dans le cadre des fermetures imposées par le gouvernement et d’un contexte commercial bouleversé. Cette tendance semble se poursuivre en 2022, dans un contexte de nouvelles incertitudes géopolitiques et économiques

En 2021, nous avons enregistré une baisse significative du taux de succession de PDG parmi les entreprises peu performantes du Russell 3000 ainsi qu’aucun cas de licenciement parmi les entreprises du S&P 500. Les données annualisées préliminaires sur les taux de 2022 indiquent que la tendance pourrait se poursuivre pendant le reste de l’année ou peut-être au-delà. Comme. le montrent nos recherches sur les mesures de performance utilisées dans les plans d’incitation, [2] certains conseils d’administration peuvent adopter une approche attentiste avec les PDG qui offrent des performances boursières à la traîne, ce qui donne le temps à leurs dirigeants d’adapter les stratégies d’entreprise à l’évolution de l’activité. Il reste à voir si cette tendance s’inversera plus tard en 2022 ou en 2023.

En 2021, la part des successions de PDG que nous avons classées comme forcées (c’est-à-dire que le PDG n’a pas atteint l’âge de la retraite de 64 ans et que l’entreprise s’est classée dans le quartile inférieur du rendement total pour les actionnaires de son secteur) a considérablement diminué par rapport à l’année précédente, tant dans le Russell 3000 (de 5,2 à 1,4 %) et dans le S&P 500 (de 10,9 à 0 %). Les données annualisées préliminaires pour 2022 montrent que la part des successions forcées reste inférieure à la moyenne historique dans le Russell 3000 et le S&P 500 : en mai 2022, la part des successions forcées n’était que de 2,3 % dans le Russell 3000 (par rapport à la moyenne historique de 5,8 %) et reste à 0 % dans le S&P 500 (par rapport à la moyenne historique de 9,8 %).

Cette baisse de la part des successions forcées de PDG est généralisée, les secteurs des services de communication, des biens de consommation de base, de l’énergie, de l’industrie, des technologies de l’information, des matériaux, de l’immobilier et des services publics ne signalant aucun départ forcé de PDG en 2021. Selon les données annualisées pour 2022, il reste nul dans tous ces secteurs à l’exception de la consommation de base et de l’immobilier ; les soins de santé ne prévoient également aucune succession forcée de PDG pour l’année en cours.

Cette baisse de la part des successions forcées de PDG est présente dans les entreprises de toutes tailles, plusieurs groupes de taille ne signalant aucune succession forcée de PDG en 2021 et ne prévoyant aucune succession forcée de PDG pour l’année en cours.

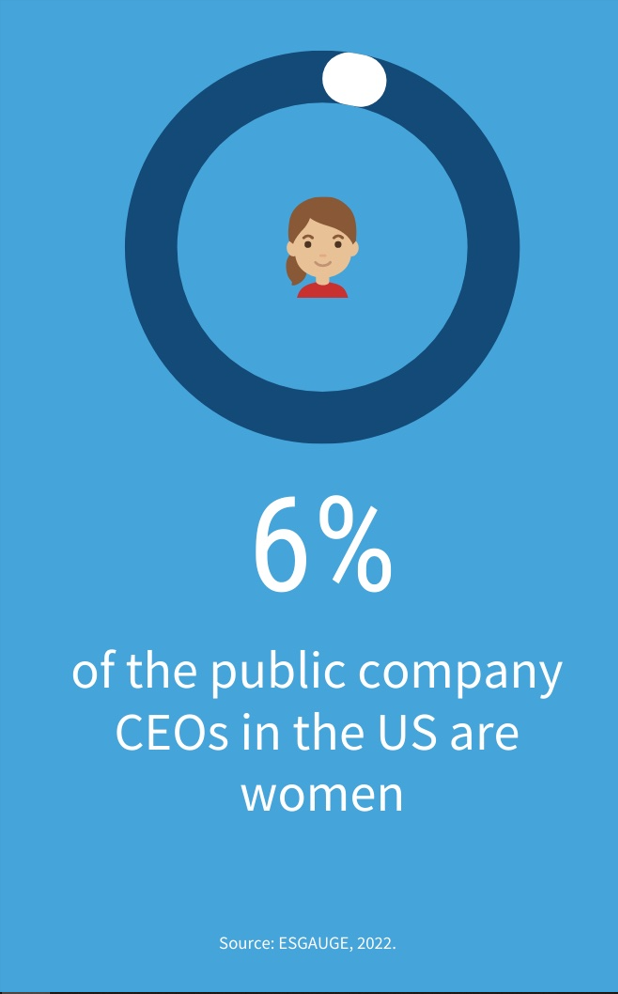

La population des PDG reste majoritairement masculine et blanche, et les progrès limités en matière de mixité enregistrés ces dernières années semblent stagner

Contrairement aux conseils d’administration, la pression en faveur de la diversité au sein de l’équipe de direction des sociétés ouvertes américaines n’a pas encore eu d’effet transformateur. Les PDG restent majoritairement masculins et blancs. Le pourcentage de femmes PDG en poste dans le Russell 3000 et le S&P 500 reste stable, et certains secteurs d’activité sont loin derrière la moyenne globale de l’indice, bien qu’ils soient largement examinés pour leur manque de représentation des sexes. La plupart des entreprises omettent encore dans leurs déclarations de procuration toute information sur l’origine raciale ou ethnique de leurs principaux dirigeants, ce qui complique la tentative de suivre les progrès en matière de diversité à ce niveau de l’entreprise.

En 2021, les femmes ne représentaient que 5,9 % de la population totale de PDG du Russell 3000 (contre 5,7 % l’année précédente) et 6,1 % du S&P 500 (contre 6,4 % en 2020). Les données annualisées préliminaires ne prévoient aucune augmentation pour 2022. Alors que pour 2021, nous avons enregistré une augmentation nette d’une année sur l’autre de 15 femmes PDG dans le Russell 3000, le nombre n’a pas eu d’impact sur le pourcentage total en raison des changements d’indice.

Dans le S&P 500, seules trois femmes PDG ont été nommées en 2021, contre sept en 2019 et 2020 et bien en deçà du record de 10 nominations de 2011 ; en 2021, deux femmes PDG du S&P 500 ont quitté leur poste, pour un gain net d’un seul.

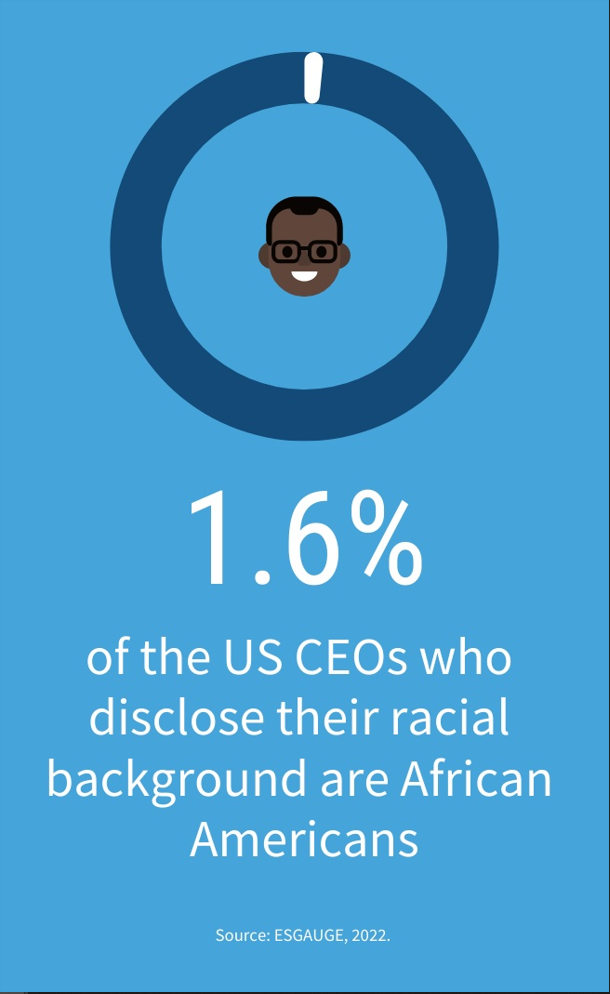

On s’attend généralement à ce que les entreprises deviennent plus ouvertes en divulguant la diversité raciale de leurs équipes de direction ; cependant, jusqu’à 95,9 % des sociétés du Russell 3000 et 88,4 % des sociétés du S&P 500 n’ont inclus dans leurs documents d’information de 2022 aucune information sur l’origine ethnique de leur PDG (les pourcentages en 2021 étaient de 95,7 et 87,8, respectivement). Dans le Russell 3000, dans les entreprises qui ont fourni ces informations, 85,6 % des PDG se sont identifiés comme blancs/caucasiens, 1,6 % comme Afro-Américains, 4,8 % comme latinos ou Hispaniques, 4,8 % comme Asiatiques, Hawaïens ou insulaires du Pacifique, et 3,2 % d’autres origines ethniques.

Les technologies de l’information, l’énergie et les services financiers continuent d’être à la traîne des autres secteurs d’activité en matière de diversité des sexes chez les PDG, avec leur part de femmes PDG en 2022 (3, 3,2 et 4,1 %, respectivement) se situant à environ la moitié du taux moyen de l’ensemble de l’indice Russell 3000. Deux des 11 secteurs d’activité GICS analysés ont signalé une diminution nette du nombre de femmes PDG en 2021 (énergie et services publics, chacun avec une diminution nette d’un), tandis que sept (services de communication, consommation de base, énergie, finance, technologie de l’information, matériaux et immobilier). Estate) ne prévoyait aucun changement dans le nombre de femmes PDG pour 2022. Le secteur des technologies de l’information comptait une seule femme PDG de plus en 2022 (ou 12) qu’en 2017 (alors que les femmes PDG étaient 11). Le secteur de l’énergie et des services publics comptait moins de femmes PDG en 2022 qu’en 2017.

L’analyse Russell 3000 par taille d’entreprise montre que la plupart des gains ont eu lieu parmi les petites et moyennes entreprises. Au total, les entreprises manufacturières et de services non financiers dont le chiffre d’affaires annuel est inférieur à 5 milliards de dollars ont ajouté 11 femmes PDG en 2021 et six femmes PDG au cours de la période du 1er janvier au 6 juillet 2022, contre aucune dans les entreprises manufacturières et de services non financiers avec un chiffre d’affaires annuel de 25 milliards de dollars et plus.

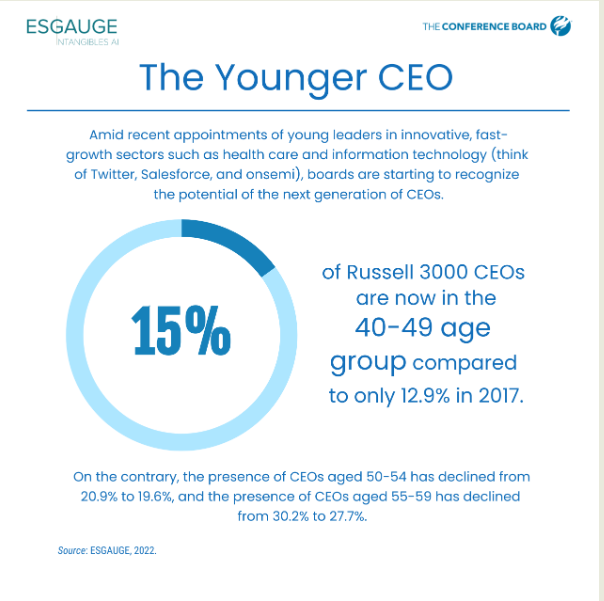

Au milieu des nominations récentes de jeunes leaders dans des secteurs innovants à croissance rapide tels que les soins de santé et les technologies de l’information, les conseils d’administration commencent à reconnaître le potentiel de la prochaine génération de PDG

Des sociétés telles que Twitter (NYSE : TWTR), Salesforce (NYSE : CRM), Onsemi (Nasdaq : ON) et Apollo Medical Holdings (NASDAQ : AMEH) ont récemment fait la une des journaux pour avoir nommé des PDG à la fin de la trentaine ou au début de la quarantaine (Parag Agrawal de Twitter a 38 ans ; Brett Taylor, co-PDG de Salesforce, et Hassane El-Khoury d’Onsemi ont tous deux 41 ans ; et Brandom Sim d’Apollo Medical n’a que 28 ans). Ces cas indiquent une tendance plus large, en particulier parmi les petites entreprises, comme le montre le pourcentage croissant de PDG dans les groupes d’âge inférieurs à 50 ans au cours des cinq dernières années.

Le pourcentage de PDG de Russell dans les groupes d’âge plus jeunes a augmenté au cours des cinq dernières années. Plus précisément, les PDG de la tranche d’âge 40-49 ans représentaient 12,9 % du total en 2017 et représentent désormais 15 %. Dans la tranche d’âge 30-39 ans, leur pourcentage est passé de 0,9 à 1,9. Au contraire, la présence de PDG âgés de 50 à 54 ans a diminué de 20,9 à 19,6 % et la présence de PDG âgés de 55 à 59 ans est passée de 30,2 à 27,7 %.

Contrairement au S&P 500, où il est resté stable à 58 ans, l’âge moyen des PDG en exercice dans l’indice Russell 3000 a baissé ces dernières années, passant de 57,2 en 2017 à 56,8 en 2022. Le PDG entrant typique a 54 dans le Russell 3000 et 55 dans le S&P 500.

L’âge du PDG peut varier considérablement d’un secteur d’activité à l’autre. L’âge médian le plus bas des PDG du Russell 3000 (56 ans) est observé dans les secteurs des technologies de l’information, de la consommation discrétionnaire et des soins de santé. Les sociétés financières et énergétiques rapportent la médiane la plus élevée (59 ans). Il est également à noter que les plus jeunes leaders de l’indice se retrouvent dans les secteurs les plus innovants de l’économie et sont souvent les fondateurs d’entreprises. Parmi les 25 plus jeunes PDG du Russell 3000, six travaillent dans des entreprises de soins de santé, cinq dans les technologies de l’information et cinq dans la consommation discrétionnaire. Au lieu de cela, les secteurs immobilier et industriel plus traditionnels de la vieille économie comptent quatre et cinq des 25 PDG les plus âgés de l’indice. Aucun PDG immobilier ne figure dans la liste des 25 plus jeunes de l’indice.

Il existe une corrélation directe entre l’âge médian du PDG et la taille de l’entreprise. Par exemple, parmi les entreprises des secteurs manufacturier et non financier, celles dont le chiffre d’affaires annuel est inférieur à 100 millions de dollars ont déclaré un âge médian de PDG de 55,5 ans, contre 58 ans dans le groupe avec un chiffre d’affaires de 50 milliards de dollars ou plus. Parmi les sociétés financières et immobilières, celles dont la valeur des actifs est inférieure à 500 millions de dollars ont un âge médian de PDG de 54 ans, contre 61,5 ans dans le groupe dont la valeur des actifs est de 100 milliards de dollars ou plus. Le pourcentage le plus élevé de PDG de moins de 50 ans se trouve dans le plus petit groupe d’entreprises (25,5 % dans le groupe des entreprises de fabrication et de services non financiers avec un chiffre d’affaires annuel inférieur à 100 millions de dollars, contre seulement 3,2 % dans le groupe des entreprises avec un chiffre d’affaires annuel compris entre 25 et 4,9 milliards de dollars et 8.

Les départs imprévus de PDG en raison d’un décès ou d’une maladie ont augmenté au cours des deux dernières années, ce qui suggère l’importance pour les conseils d’avoir des plans de relève et de communication d’urgence. Les deux indices ont également signalé un pourcentage plus élevé de changements de leadership en raison de regroupements d’entreprises

En 2021 et 2022, nous avons enregistré dans les indices Russell 3000 et S&P 500 un taux plus élevé de successions à la direction qui ont été expliquées pour le décès du PDG ou pour son incapacité à continuer à exercer les fonctions de la fonction. En plus de susciter un débat sur la quantité d’informations que les entreprises devraient divulguer sur la détérioration de la santé de leurs principaux dirigeants tout en protégeant leur vie privée, ces exemples suggèrent l’importance pour les conseils d’administration de maintenir un plan de relève d’urgence, y compris un protocole sur les communications aux employés et les intervenants extérieurs.

Parmi les entreprises du S&P 500, 10 % des successions de PDG en 2021 et 6,9 % de celles annoncées jusqu’en juillet 2022 étaient dues à un décès ou à une incapacité physique ou mentale, contre 3,6 % en 2020 et 4,5 % en 2019. Dans le Russell 3000, les cas de décès ou la maladie du PDG déclenchant un événement de roulement est passé de 2,3 % du total en 2020 à 3,5 % en 2021 et 2,9 % en 2022.

Alors que les licenciements de PDG ont diminué en 2021 et 2022, les deux indices ont signalé une augmentation du pourcentage de cas de roulement de PDG en 2021 en raison de transactions de regroupement d’entreprises, y compris des fusions ou des acquisitions avec d’autres organisations. Dans le Russell 3000, ces cas sont passés de 2,6 % du total en 2020 à 4,2 % en 2021 ; dans le S&P 500, ils sont passés de 3,6 % à 4,1 %.

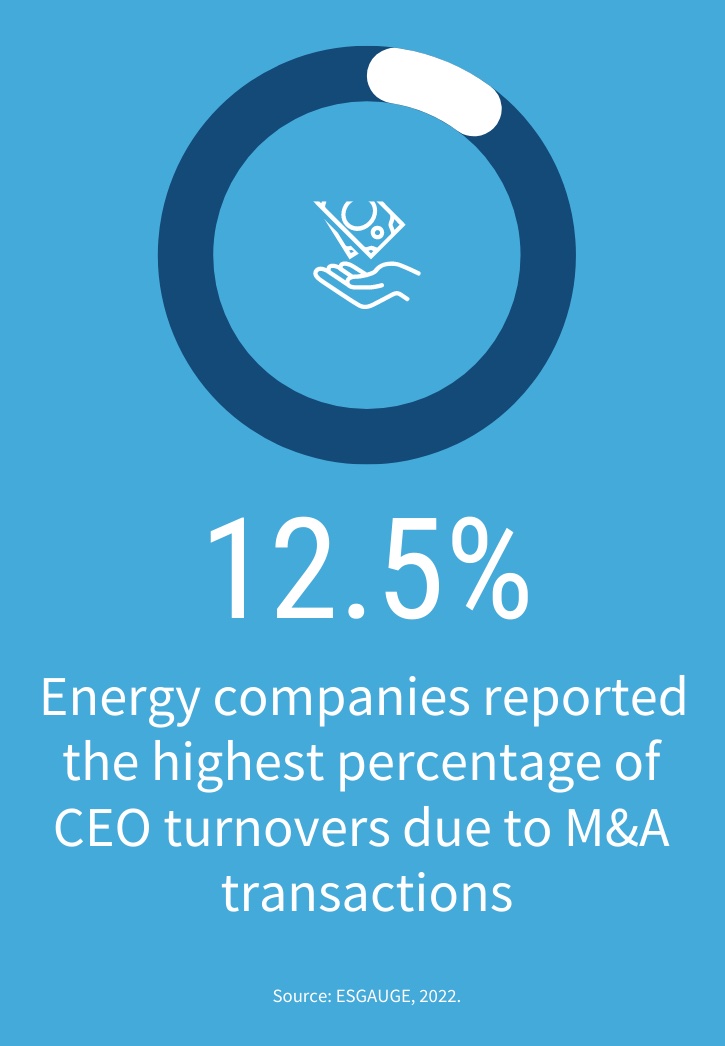

Les sociétés énergétiques [12,5 %], les sociétés industrielles [8,3 %] et les sociétés de matériaux [également 8,3 %] ont déclaré les pourcentages les plus élevés de chiffre d’affaires des PDG en 2021 en raison de transactions de fusions et acquisitions. Huit des 11 secteurs d’activité GICS n’ont eu aucun cas de succession forcée de PDG [licenciement] en 2021. Les secteurs qui ont signalé des licenciements étaient la consommation discrétionnaire [1,9 %], la finance [2,6 %] et les soins de santé [3,2 %].

L’analyse par chiffre d’affaires annuel et valeur d’actif ne montre aucune corrélation entre la taille de l’entreprise et les successions de PDG induites par des regroupements d’entreprises.

Les conseils d’administration promeuvent des initiés au poste de PDG à un rythme record. En plus de résulter des améliorations que les conseils d’administration ont apportées au cours des deux dernières décennies à la planification de la relève, ce constat pourrait être un signe de l’importance accordée à la connaissance de l’organisation et à la familiarité avec la culture d’entreprise

Les promotions internes au poste de PDG continuent d’augmenter, les nominations d’initiés parmi le S&P 500 atteignant le taux le plus élevé [soit près de neuf sur 10] depuis que le Conference Board et l’ESGAUGE ont commencé à suivre cette statistique en 2011. De plus, en 2021, les nominations internes avaient une ancienneté moyenne dans l’entreprise de 18 ans, éclipsée seulement par les 19 ans que nous avions enregistrés en 2002. La proportion de « cadres chevronnés » — ou ceux ayant au moins 20 ans de service dans l’entreprise — a également atteint des sommets historiques parmi les entreprises publiques américaines. La prévalence des nominations d’initiés semble se poursuivre selon les données annualisées préliminaires sur les événements de succession de 2022.

Tout comme d’autres découvertes récentes discutées dans cet article, le nombre de promotions d’initiés au poste de PDG peut s’expliquer par les défis de la crise de Covid et les incertitudes prolongées qui sont maintenant prévues par la plupart des analystes du marché : plus précisément, les administrateurs peuvent croire que les chefs d’entreprise plus expérimentés et chevronnés ayant une connaissance directe de l’organisation sont mieux placés pour gérer les risques posés par ces temps difficiles. La pandémie a également accentué l’importance de valoriser le capital humain pour atteindre un succès commercial durable, et de nombreux administrateurs peuvent conclure qu’une personne qui comprend la culture d’entreprise est plus susceptible d’assurer une transition de leadership en douceur et d’éviter les attritions.

En 2021, le taux de nomination des promotions internes au poste de PDG a augmenté par rapport aux années précédentes à la fois dans le Russell 3000 [de 66,7 à 71,1 %] et dans le S&P 500 [de 74,5 à 86 %]. Ces deux taux sont les plus élevés depuis que le Conference Board et l’ESGAUGE ont commencé à suivre ces statistiques. Les données annualisées préliminaires pour 2022 montrent que cette tendance se poursuit : en juin 2022, le taux de promotions internes au poste de PDG était de 72,7 % dans le Russell 3000 et de 86,2 % dans le S&P 500.

Le taux de hausse est encore plus prononcé dans les secteurs des services publics, de la finance et de l’industrie [avec des taux de succession d’initiés pour 2021 de 100 %, 84,2 % et 80,6 %], alors qu’il est plus faible parmi les entreprises des secteurs des matériaux et de l’immobilier [une baisse en 2021, par rapport à 2020, de 33,3 % et 11,9 %, respectivement].

Il n’y a pas de corrélation entre le taux de nomination d’initiés et la taille des entreprises.

Notes de fin

1 Voir, plus récemment, Suzanne Kapner et Sarah Nassauer, From Gap To Dollar General : Retail Chief Exit As Challenges Grow , The Wall Street Journal, 14 juillet 2022 ; et Melissa Repko et Lauren Thomas, From Gap to GameStop, There’s A Retail Executive Exodus Underway—And More Departures Are Coming, CNBC, 20 juillet 2022.(retourner]

Voici un article publié par Richard Holt, directeur général chez Alvarez & Marsal, et Amerino Gatti, directeur exécutif chez Helix Energy. Cet article est basé sur une publication NACD BoardTalk, et il a été publié sur le Forum du Harvard Law School on Corporate Governance.

L’article traite d’un sujet de la plus haute importance pour la saine gouvernance des entreprises : le rôle du conseil d’administration dans la préparation d’un solide plan de relève du PDG afin d’assurer la croissance de l’organisation.

Je vous invite à lire la version française de l’article, publiée sur le Forum de Harvard Law School on Corporate Governance, effectuée par Google, que j’ai corrigé. Ce travail de traduction est certainement encore perfectible, mais le résultat est très satisfaisant.

Naturellement, de nombreuses entreprises sont préoccupées par la perturbation économique majeure du marché et n’ont peut-être pas investi le temps, ou mis à profit l’expertise des membres de leur conseil d’administration pour se concentrer sur une planification efficace de la relève du PDG.

Si vous ne pensez pas à ce sujet maintenant, vous pourriez avoir besoin d’un coup de semonce, en particulier sur le marché du travail concurrentiel d’aujourd’hui. Tous les signes pointent vers une pénurie d’embauche pour les entreprises qui ne sont pas préparées. Plusieurs entreprises sont en retard dans la planification de la relève, mais il n’est jamais trop tard. Les conseils d’administration peuvent agir dès maintenant afin de s’assurer qu’ils sont prêts à relever les défis de l’avenir.

Apprenez à connaître votre PDG et votre plan stratégique

Le meilleur remède pour une planification de la relève plus saine consiste à acquérir une compréhension approfondie de ce dont votre entreprise a besoin chez un PDG, ce qui signifie vraiment apprendre à connaître votre PDG actuel et s’engager dans une solide planification de scénarios commerciaux avec le PDG et l’équipe de direction.

Les données suggèrent que de nombreux conseils d’administration ne sont pas préparés à s’engager dans le processus de développement et de succession du PDG. Une étude menée par le Rock Center for Corporate Governance de l’Université de Stanford et Heidrick & Struggles a révélé que seuls 51 % des conseils d’administration peuvent identifier leur successeur à l’interne. Trente-neuf pour cent disent n’avoir aucun candidat interne. Ce n’est pas surprenant étant donné que lorsque les conseils d’administration se réunissent pour discuter de la planification de la relève, ils ne consacrent en moyenne que 1,14 heure sur le sujet, selon une étude distincte du Rock Center et de l’Institute of Executive Development.

Une solide planification de scénarios d’entreprise et une planification de la relève du PDG vont de pair : vous ne pouvez pas avoir l’un sans l’autre. Connaître la trajectoire prévue de l’entreprise est un élément essentiel pour planifier correctement la succession du PDG.

Être activement impliqué et engagé dans la planification de scénarios d’entreprise et bien comprendre le rôle du PDG éclaire de manière critique la planification de la relève et, en fin de compte, les qualifications d’embauche d’un nouveau PDG. Il ne suffit pas non plus qu’un ou deux membres du conseil d’administration soient impliqués. Chaque membre du conseil d’administration doit être profondément engagé, appliquant une expertise et des perspectives uniques pour collaborer avec le PDG. Connaître votre prochain PDG, c’est connaître votre entreprise.

Considérez l’impact des forces et des faiblesses d’un PDG sur l’ensemble de l’équipe de direction

Un autre avantage d’être activement engagé dans la planification de scénarios de succession, en tant que conseil d’administration, est qu’il donne un aperçu des forces et des faiblesses d’un PDG actuel, et montre comment ces caractéristiques peuvent avoir un impact sur l’ensemble de l’écosystème de leadership. Bien sûr, l’une des principales responsabilités du conseil est de tenir le PDG responsable, mais au-delà de cela, la gestion efficace de la performance d’un PDG ouvre une fenêtre sur la dynamique de toute l’équipe de direction.