L’article paru dans Harvard Law School sous la plume de Ted Sikora, chef de projet, des sondages et des analyses commerciales chez NACD, met en lumière les résultats du dernier sondage sur les tendances qui auront le plus grand effet sur les entreprises des répondants au cours de l’année 2023.

J’ai utilisé l’outil de traduction de Google afin de vous présenter les points saillants de l’article.

Bonne lecture !

Si 2020 a été l’année de la pandémie de COVID-19 et que 2021 a été l’année de la reprise, 2022 a offert peu de répit aux administrateurs supervisant les entreprises dans un environnement commercial chaotique. Pour mieux comprendre les principales tendances qui auront une incidence sur les conseils d’administration en 2023 et la façon dont les administrateurs prévoient de s’adapter, l’Association nationale des administrateurs de sociétés (NACD) a de nouveau mené son enquête annuelle sur les tendances et les priorités des conseils d’administration. Le rapport d’enquête de cette année comprend les commentaires de plus de 300 administrateurs, qui détaillent leurs attentes pour l’année à venir, ainsi que les principaux domaines d’amélioration qu’ils jugent importants. [1]

TOP TENDANCES

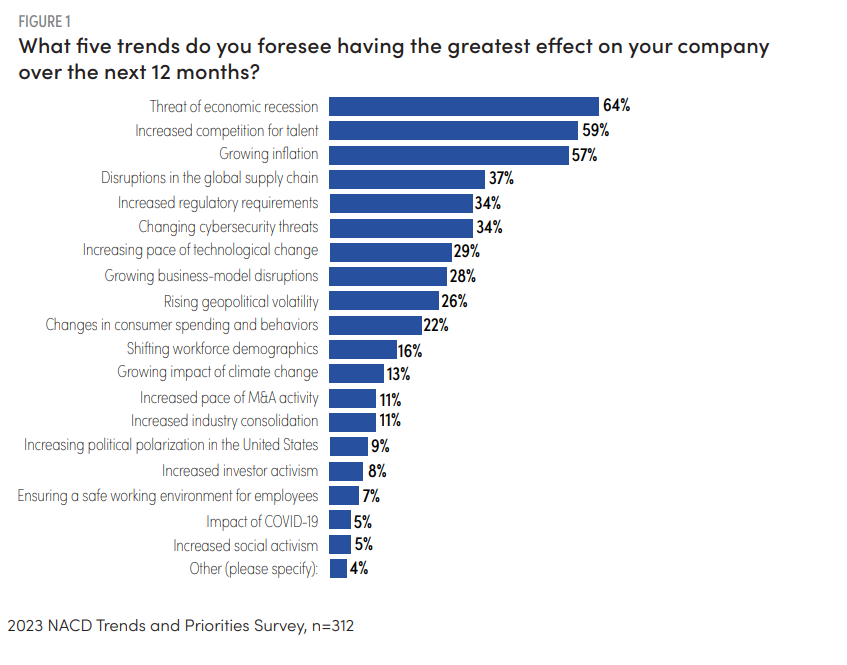

Les administrateurs ont été invités à sélectionner les cinq principales tendances qui, selon eux, auront le plus grand effet sur leur entreprise au cours de la prochaine année. Il n’est pas surprenant que l’inflation et la menace d’une récession économique soient au cœur des préoccupations. Après plusieurs mois d’inflation record, la menace d’une récession plane sur le paysage des affaires, 64 % des répondants la sélectionnant parmi leurs principales préoccupations. Alors que l’inflation persiste malgré une série de hausses de taux d’intérêt initiées par la Réserve fédérale, le pessimisme s’est accru à l’égard des perspectives de l’économie américaine. (Voir la figure 1.) En fait, seulement 29 % des répondants pensent que l’économie des États-Unis se dirige vers un « atterrissage en douceur », c’est-à-dire endiguer l’inflation tout en évitant une récession d’ici la mi-2023. Pendant ce temps, 65 % anticipent une récession, et 6 % anticipent une grave récession. (Voir Figure 2.)

Alors que les entreprises se réorganisent en vue d’un éventuel environnement de récession, la concurrence pour les personnes talentueuses qui peuvent les accompagner restera forte. Malgré les gros titres faisant état de licenciements importants et de gels des embauches dans le secteur de la technologie, le marché du travail reste historiquement tendu par rapport aux mesures traditionnelles, avec un ratio chômeurs/offres d’emploi de 0,5 en septembre 2022. [2] Plus de la moitié des répondants (59 %) ont indiqué que la concurrence accrue pour les talents est une préoccupation majeure. (Voir Figure 1 ci-dessous.)

Les perturbations des chaînes d’approvisionnement mondiales survenues pendant la pandémie ont alimenté l’inflation tout au long de 2022. L’invasion russe de l’Ukraine en février 2022 a encore amplifié les défis de la chaîne d’approvisionnement, et 37 % des personnes interrogées s’attendent à ce que les problèmes de chaîne d’approvisionnement aient un impact important sur leurs entreprises. l’année à venir. (Voir Figure 1 ci-dessous.)

Notamment, l’impact de la pandémie de COVID-19 et la garantie d’un environnement de travail sécuritaire pour les employés ne sont pas une priorité pour les administrateurs. Alors que les épidémiologistes doivent encore parvenir à un consensus quant à savoir si le virus est devenu endémique, une expérience plus large de la gestion du virus, l’acclimatation au travail à distance et la confiance dans l’efficacité des vaccins et des médicaments ont atténué les inquiétudes des directeurs par rapport à d’autres problèmes.

Collectivement, ces tendances auront une incidence sur la façon dont les conseils d’administration gouverneront à l’avenir, tant à long terme qu’à court terme.

L’AVENIR DE LA GOUVERNANCE DU CONSEIL

Comme indiqué dans le rapport Future of the American Board de la NACD , publié en octobre 2022, « étant donné que la gouvernance dépend fortement du contexte, l’évolution de l’environnement a des implications sur les pratiques de gouvernance ». [3] À la lumière de la myriade de tendances touchant les entreprises, les répondants sont d’accord avec les conclusions du rapport selon lesquelles la façon dont les conseils d’administration fonctionneront à l’avenir devra s’adapter.

Certains de ces changements se produiront alors que les conseils d’administration s’efforcent de fournir des conseils et une surveillance dans un monde complexe et en évolution rapide. Plus de la moitié (56 %) des répondants, par exemple, s’attendent à voir un engagement beaucoup plus profond et plus fréquent des conseils d’administration américains sur la stratégie au cours des trois prochaines années, et 45 % des répondants prévoient une augmentation considérable du temps consacré au service du conseil.

D’autres changements peuvent être provoqués et/ou accélérés par des pressions externes, que ce soit par les parties prenantes, les régulateurs ou la société en général. Par exemple, 85 % des répondants estiment que les conseils d’administration manquant de diversité deviendront moins acceptables avec le temps. L’indépendance de la direction du conseil d’administration est un autre exemple, 57 % des répondants indiquant que la pratique consistant à combiner les rôles de président du conseil d’administration et de PDG sera de moins en moins acceptable.

PRIORITÉS D’AMÉLIORATION

Alors que les tendances et les pressions externes motivent les changements dans la façon dont les conseils fonctionnent, les conseils devront examiner leur performance et leurs pratiques de gouvernance et prioriser les domaines à améliorer. Les sections suivantes passent en revue les principales opportunités identifiées par les administrateurs dans les relations conseil-direction, les questions de surveillance et les opérations du conseil.

Relations Conseil-Direction

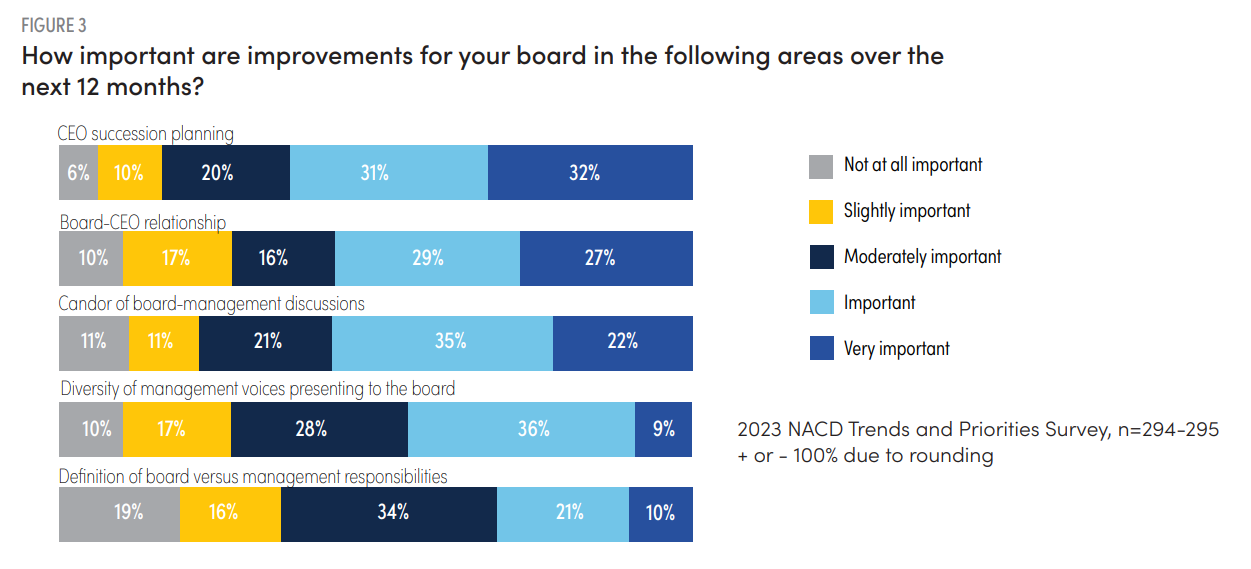

Avoir le bon leader à la barre est de plus en plus critique et difficile à une époque de changements vastes et rapides. Trente-sept pour cent des répondants ont indiqué que leur conseil n’avait pas alloué suffisamment de temps de réunion à la planification de la relève du chef de la direction au cours des 12 derniers mois, et 32 % jugeaient « très important » que leur conseil améliore ses pratiques en matière de planification de la relève du chef de la direction. (Voir la figure 3.) Alors que le roulement des PDG du Russell 3000 a ralenti au cours de la pandémie, il a augmenté en 2022. [4]

Le succès mutuel du PDG et du conseil dépend de leur capacité à gérer leur relation, visant une « tension constructive et saine », comme le recommande le rapport Future of the American Board. [5] Cette tension découle des devoirs du conseil en tant que surveillant et caisse de résonance. Il s’agit d’un équilibre délicat à trouver, et 56 % des répondants estiment que la relation entre leur conseil d’administration et leur PDG est un domaine d’amélioration important. (Voir Figure 3, ci-dessus.)

Surveillance du conseil

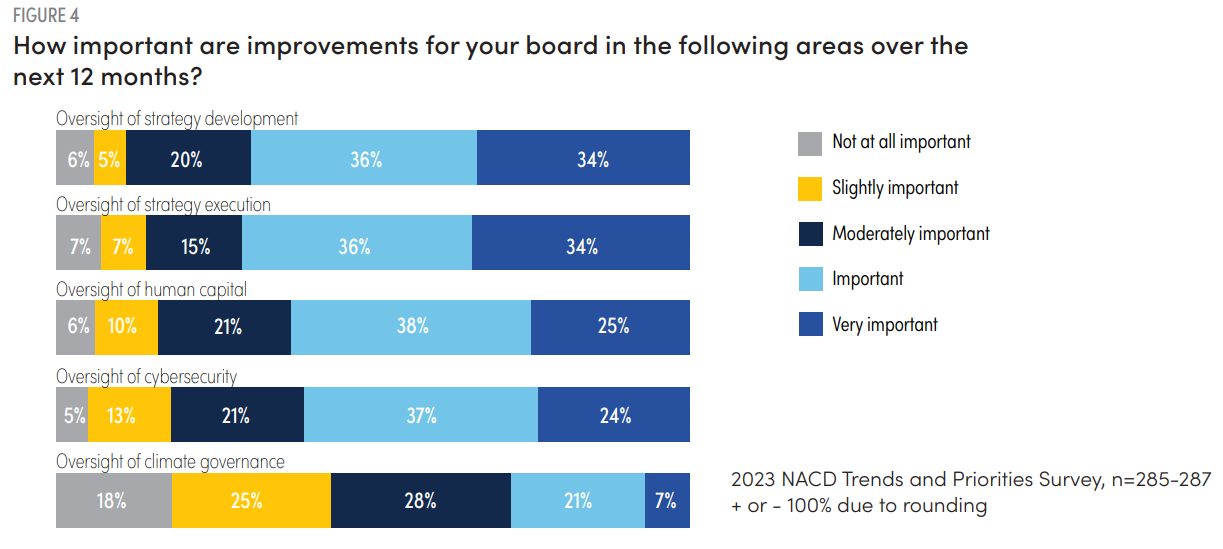

Compte tenu de l’augmentation attendue de l’engagement du conseil d’administration sur la stratégie au cours des trois prochaines années, il n’est pas surprenant que la surveillance de la stratégie de l’entreprise reste un domaine d’amélioration clé pour de nombreux conseils d’administration. Soixante-dix pour cent des répondants ont indiqué que l’amélioration de l’élaboration et de l’exécution de la stratégie était importante ou très importante. (Voir Figure 4.)

Pourtant, les responsabilités de surveillance des administrateurs s’étendent, et les administrateurs voient de plus en plus la valeur d’avoir une expérience diversifiée. Le rapport Future of the American Board recommande que « le conseil d’administration rassemble une variété de compétences, d’expériences et de points de vue pertinents pour les activités de l’entreprise dans un environnement propice à la prise de décisions consensuelles après une discussion approfondie et vigoureuse à partir de divers points de vue ». [6] La majorité (82 %) des répondants ont indiqué que la diversité élargit les perspectives et l’expertise du conseil. Un autre 64 pour cent ont indiqué que la diversité améliore la capacité d’un conseil à identifier ces lacunes en matière d’information/compétences en premier lieu.

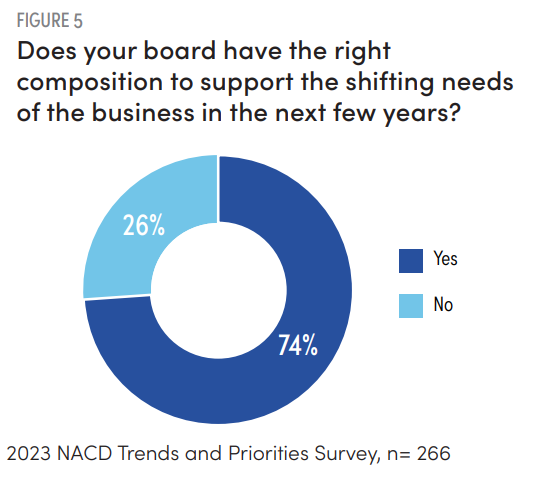

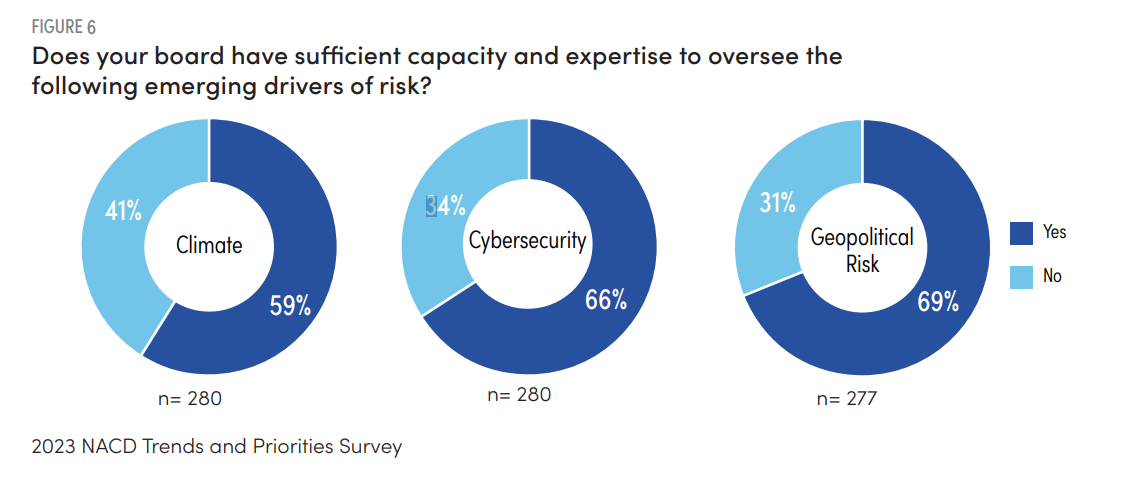

Alors que 74 % des répondants indiquent que la composition et l’expertise de leur conseil d’administration sont adaptées pour répondre aux besoins changeants de l’entreprise au cours des prochaines années, lorsque des facteurs spécifiques de risques émergents sont pris en compte, de nombreux conseils d’administration sont moins confiants. (Voir la figure 5.) Environ un tiers des répondants estiment que leur conseil n’a pas la capacité et l’expertise nécessaires pour superviser des domaines tels que la cybersécurité (34 %) ou les risques géopolitiques (31 %). (Voir Figure 6.)

C’est également le cas de la surveillance climatique : 41 % des répondants voient une opportunité d’accroître la capacité et l’expertise de leur conseil d’administration pour surveiller les questions climatiques. Cependant, fait intéressant, seuls 28 % des répondants ont estimé qu’il était « important » ou « très important » que leur conseil améliore ses pratiques en matière de gouvernance climatique. (Voir la figure 6.) Ce sentiment varie selon l’industrie. Par exemple, seuls 4 % des répondants du secteur financier ont indiqué qu’il était « très important » que leur conseil d’administration améliore la surveillance en matière de climat, et 20 % ont déclaré que ce n’était « pas du tout important ». Pendant ce temps, parmi les répondants du secteur de l’énergie, 24 % ont déclaré qu’il était « très important » que leur conseil d’administration s’améliore dans ce domaine, contre seulement 8 % qui estimaient que ce n’était « pas du tout important ».

Opérations du conseil

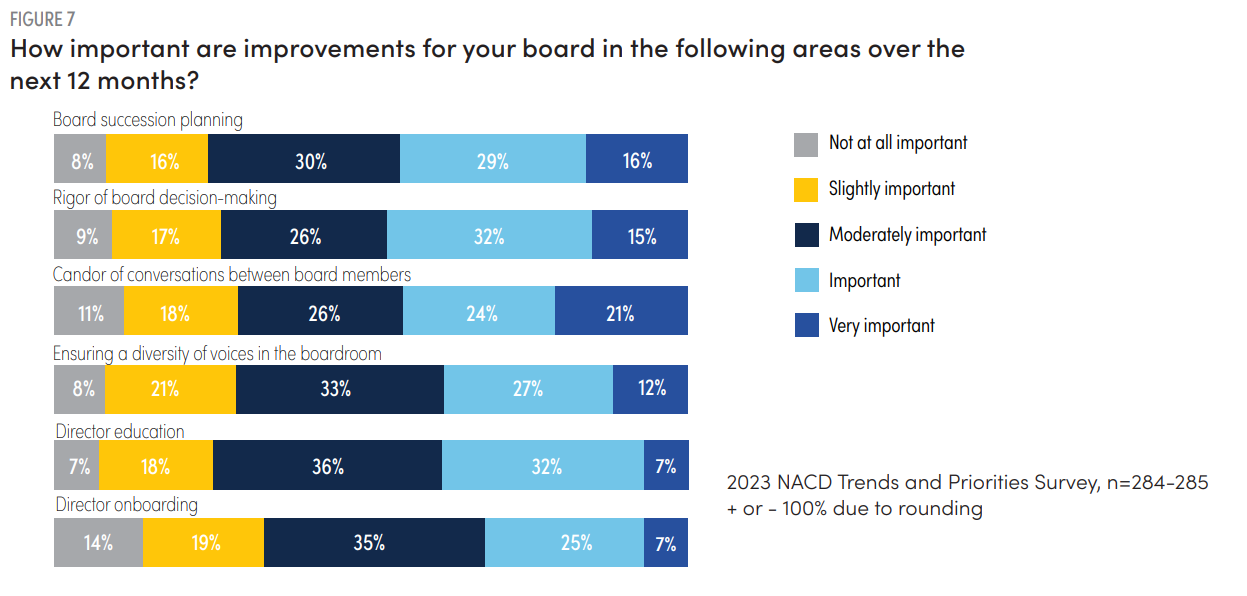

Les administrateurs cherchent également à améliorer la dynamique au sein de la salle de conférence. Environ la moitié des répondants ont indiqué qu’il est « important » ou « très important » qu’ils améliorent la rigueur de la prise de décision du conseil (47 %) ou la franchise des discussions du conseil (45 %) au cours des 12 prochains mois. (Voir Figure 7.)

Il a été noté ci-dessus que l’amélioration de la diversité au sein du conseil peut combler les lacunes en matière d’expertise. De même, des améliorations aux pratiques d’inclusion du conseil peuvent améliorer la dynamique du conseil. Dans l’ensemble, 76 % des répondants ont indiqué que les pratiques d’inclusion efficaces créent un dialogue plus riche dans la salle de conférence et 61 % ont indiqué que ces pratiques permettent une prise de décision de meilleure qualité sur les questions de gouvernance clés. Cependant, 42 % des répondants estimaient que leur conseil disposait de peu de temps pour discuter de l’inclusion au niveau du conseil compte tenu d’autres priorités.

Fait intéressant, l’intégration a été classée au dernier rang des problèmes opérationnels du conseil à améliorer. Le processus d’intégration peut donner aux nouveaux administrateurs une compréhension de la dynamique du conseil d’administration et des règles d’engagement non écrites entre les administrateurs et entre le conseil et la direction, les transformant en administrateurs très performants.

CONCLUSION

Chaque année, des tendances clés spécifiques inspirent des changements à long et à court terme dans les pratiques de gouvernance d’entreprise, qui, à leur tour, obligent les conseils à s’améliorer et à se réoutiller pour s’adapter. Une année 2022 très mouvementée laisse présager d’autres changements à venir en 2023, et les conseils doivent rester vigilants et continuer à s’améliorer pour suivre le rythme de l’évolution du monde de la gouvernance.

Notes de fin

1 L’enquête NACD 2023 sur les tendances et les priorités des conseils d’administration s’est déroulée sur le terrain du 25 octobre au 10 novembre 2022.(retourner)

2 Bureau of Labor Statistics des États-Unis, Graphics for Economic News Releases, « Nombre de chômeurs par offre d’emploi, corrigé des variations saisonnières. ”(retourner)

3 NACD, The Future of the American Board Report (Arlington, VA : NACD, 2022), p. dix.(retourner)

4 Jena McGregor, » Le chiffre d’affaires des PDG reprend à mesure que la pandémie diminue, mais pas pour de mauvaises performances « , publié sur Forbes CEO Next.(retourner)

5 NACD, The Future of the American Board Report (Arlington, VA : NACD, 2022), p. 32.(retourner)

6 NACD, The Future of the American Board Report (Arlington, VA : NACD, 2022), p. 49.(retourner)

Why Board Members Decide To Step Down

Why Board Members Decide To Step Down