Part 1. Perceptions of board diversity

The findings in this section show that the survey found nearly universal agreement on the need for diverse skill sets and perspectives on the board, and on the potential benefits of diversity.

Boards agree on the need for diversity

Note, however, that this finding does not reveal where diversity of skill sets and perspectives are needed. Thus, the skills and perspectives could be those of, say, financial or operating or information

technology executives. Such backgrounds would represent diversity of skills and perspectives, but not the demographic diversity that the term “diversity” usually implies.

Demographic diversity remains an essential goal in that gender and racial differences are key determinates of a person’s experiences, attitudes, frame of reference, and point of view.

As the next finding reveals, however, respondents do not see demographic diversity as enough.

Board members see diversity as going beyond basic demographics

Nine in ten respondents agree that gender and racial diversity alone does not produce the diversity required for an organization to be innovative or disruptive. This may be surprising, given that gender and racial differences are generally seen as contributing to diverse perspectives. Yet those contributions may be tempered if recruiting and selection methods skew toward candidates with the backgrounds and experiences of white males with executive experience.

More to the point, it would be unfortunate if a focus on diversity of skills and perspectives were to undermine or cloud the focus on gender and racial diversity. In fact, typical definitions of board diversity include a demographic component. Deloitte’s 2016 Board Practices Report found that 53 percent of large-cap and 45 percent of mid-cap organizations disclose gender data on their board’s diversity; the respective numbers for racial diversity are, far lower, however: 18 percent and 9 percent.

So, the deeper questions may be these: How does the board go about defining diversity? Does its definition include gender and racial factors? Does it also include factors such as skills, experiences, and perspectives? Will the board’s practices enable it to achieve diversity along these various lines?

Before turning to practices, we consider the potential benefits of diversity.

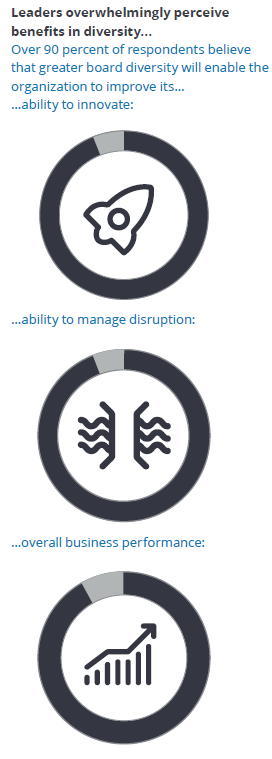

Leaders overwhelmingly perceive benefits in diversity

Taken at face value, these answers indicate that boards believe in diversity, however they go about defining it, for business reasons and not just for its own sake or reasons of social responsibility.

…Yet relatively few see a lack of diversity as a top problem

The foregoing findings show that leaders believe that boards need greater diversity of skills and perspectives, that demographic diversity alone may not produce that diversity, and that diversity is seen as beneficial in managing innovation, disruption, and business performance. Yet, somewhat surprisingly, few respondents cited a lack of diversity as a top problem.

So, while 95 percent of respondents agree that their board needs to seek out more candidates with diverse skills and perspectives, far smaller percentages cite lack of diversity as among the top problems they face in candidate recruitment or selection.

Does this reflect contentment with current board composition and acceptance of the status quo?

Perhaps, or perhaps not.

However, we can say that many board recruitment and selection practices remain very traditional.

Part 2. Recruitment and evaluation practices

Board recruitment practices have arguably not kept pace with the desire and need for greater board diversity.

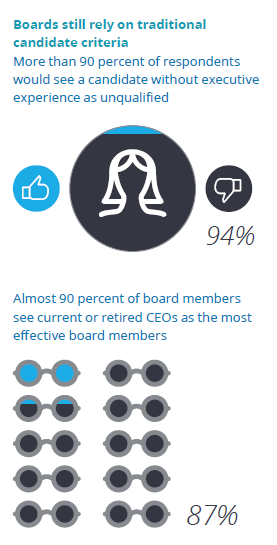

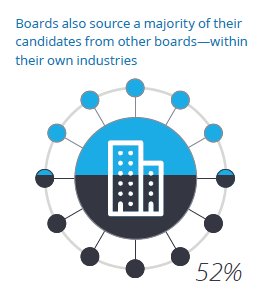

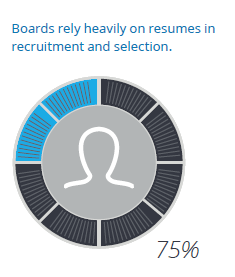

Boards still rely on traditional candidate criteria

In addition, 81 percent of respondents would expect multiple board members to see a candidate without executive experience as unqualified to serve on the board.

The low percentage of women candidates (16 percent) is striking, as is that of racial minorities (19 percent). However, that may be a logical outcome of a process favoring selecting candidates with board experience—who historically have tended to be white and male.

So, in the recruitment process, board members are often seeking people who tend to be like themselves—and like management. Such a process may help to reinforce a lack of diversity in perspectives and experiences, as well as (in most companies) in gender and race.

Relying on resumes, which reflect organizational and educational experience, helps to reinforce traditional patterns of board composition.

About half of organizations have processes focused on diverse skills and disruptive views

Given all their other responsibilities, many boards understandably rely on existing recruitment tools and processes. They use resumes, their networks, and executive recruiters—all of which tend to generate results very similar to past results.

However, our current disruptive environment likely calls for more creative approaches to reaching diverse candidates. Some organizations have taken steps to address these needs.

Our survey did not assess the nature or extent of the processes for recruiting candidates with diverse skills or perspectives, indicating an area for further investigation.

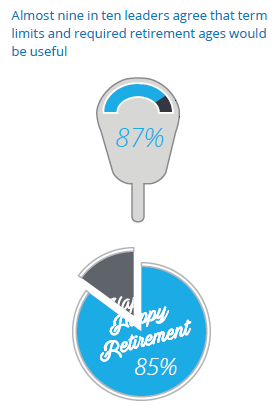

Policies affecting board refreshment

Policies, as well as processes, can affect board composition. Low turnover on boards can not only hinder movement toward greater diversity but also lead to myopic views of operations or impaired ability to oversee evolving strategies and risks.

While board members expressed agreement with term and age limits, the latter are far more common. Our separate 2016 Board Practices Report found that 81 percent of large-cap and 74 percent of mid-cap companies have age limits, but only 5 percent and 6 percent, respectively, have term limits. This evidences a large gap between agreement with term limits as an idea and term limits as a practice.

Current practices tend to limit diversity

Deloitte’s 2016 Board Practices Report also found that 84 percent of large-cap and 90 percent of mid-cap organizations most often rely on current directors’ recommendations of candidates. That same study found that 68 percent and 79 percent, respectively, use a recruiting firm when needed, and that 62 percent and 79 percent use a board skills matrix or similar tool.

Relying on current directors’ recommendations will generally produce candidates much like those directors. Recruiting firms can be valuable, but tend to adopt the client’s view of diversity. Tools such as board competency matrices generally do not account for an organization’s strategy, nor do they provide a very nuanced view of individual board members’ experiences and capabilities. In other words, bringing people with diverse skills, perspectives, and experiences to the board—as well as women and racial and ethnic minorities—requires more robust processes than those currently used by most boards.

Part 3. A path forward—The Mixtocracy Model

The term meritocracy describes organizational advancement based upon merit—talents and accomplishments—and aims to combat the nepotism and cronyism that traditionally permeated many businesses. However, too often meritocracy results in mirrortocracy in which all directors bring similar perspectives and approaches to governance, risk management, and other board responsibilities.

A board differs from a position, such as chief executive officer or chief financial officer, in that it is a collection of individuals. A board is a team and, like any other team, it requires people who can fulfill specific roles, contribute different skills and views, and work together to achieve certain goals.

Thus, a board can include nontraditional members who will be balanced out by more traditional ones. Many existing recruiting methods do too little to achieve true diversity. The prevalence of those criteria and methods can repeatedly send boards back to the same talent pool, even in the case of women and minority candidates. For example, Deloitte’s 2016 Board Diversity Census shows that female and black directors are far more likely than white male directors to hold multiple Fortune 500 board seats.

Therefore, organizations should consider institutionalizing a succession planning and recruitment process that more closely aligns to their ideal board composition and diversity goals. Here are three ways to potentially do that:

Look beyond “the tried and true.” Even when boards account for gender and race, current practices may tend to source candidates with similar views. Succession plans should create seats for those who are truly different, for example someone with no board experience but a strong cybersecurity background or someone who more closely mirrors the customer base.

Take a truly analytical approach. Developing the optimal mix on the board calls for considering risks, opportunities, and markets, as well as customers, employees, and other stakeholders. A data-driven analytics tool that assesses management’s strategies, the board’s needs, and desired director attributes can help define the optimal mix in light of those factors.

Use more sophisticated criteria. Look beyond resumes and check-the-box approaches to recruiting women, minorities, and those with the right title. Surface-level diversity will not necessarily generate varying perspectives and innovative responses to disruption. Deep inquiry into a candidate’s outlook, experience, and fit can take the board beyond standard criteria, while prompting the board to more fully consider women and minority candidates—that is, to not see them mainly as women and minority candidates.

To construct and maintain a board that can meet evolving governance, advisory, and risk oversight needs, leaders should also consider the following steps.

Rethink risk

Digitalization continues to disrupt the business landscape. The ability to not only respond to disruption, but to proactively disrupt, has commonly become a must. Yet boards have historically focused on loss prevention rather than value creation. Every board should ask itself who best can help in ascertaining that management is taking the right risks to innovate and win in the marketplace. The more diversity of thought, perspectives, experiences, and skills a board collectively possesses, the better it can oversee moves into riskier territory in an informed and useful way—and to assist management in making bold decisions that are likely to pay off.

Elevate diversity

Current definitions of board diversity tend to focus on at-birth traits, such as gender and race. While such diversity is essential, it may promote a check-the-box approach to gender and racial diversity. Boards that include those traits and also enrich them by considering differences gained through employment paths, industry experiences, educational, artistic, and cultural endeavors, international living, and government, military, and other service will more likely achieve a true mix of perspectives

and capabilities.

They may also develop a more holistic vision of gender and racial diversity. After all, woman and minority board members do not want to be “women and minority board members”—they want to be board members. In other words, this approach should aim to generate a fuller view of candidates and board members, as well as more diversity of skills and perspectives and gender and race.

Retool board composition

Current tools for achieving an optimal mix of directors can generally be classified as simplistic, generic, and outdated. They often help in organizing information, but provide little to no support in identifying strategic needs and aligning a board’s skills, perspectives, and experiences with those needs.

Successful board composition typically demands analysis of data on organizational strategies, customer demographics, industry disruption, and market trends to identify gaps and opportunities. A board should consider not only individual member’s profiles but also assess the board as one working body to ascertain that complementary characteristics and capabilities are in place or can be put in place.

A tool to support this analysis should be the initial input into the succession planning and recruitment process. It should also be used in ongoing assessments to help ensure that the board equals a whole that is greater than the sum of its parts.

Revitalize succession planning

The process of filling an open board position may be seen as similar to that for recruiting C-suite candidates. But that would ignore the fact that the board is a collection of individuals rather than a single role. An approach geared to creating a mixtocracy can strengthen the board by combining individual differences in a deliberate manner. Differing gender and ethnic backgrounds as well as skills, perspectives, and experiences can make for more rigorous, far-reaching, and thought-provoking discussions, inquiries, and challenges. This can enable the board to provide a more effective counterbalance to management as well as better support in areas such as innovation, disruption, and assessments of strategies, decisions, and underlying assumptions.

In plans for board succession, the uniqueness of thought an individual will bring to the table can be as important as his or her more ostensible characteristics and accomplishments.

Toward greater board diversity

Given its responsibility to provide guidance on strategy, oversight of risk, governance of practices, and protection of shareholders’ interests, the board arguably has a greater need for diversity than the C-suite, where diversity also enriches management. The path forward remains long, but it is becoming increasing clear as boards continue to work toward achieving greater diversity on multiple fronts.

____________________________________

Endnotes

1 2016 Boards Practices Report – A transparent look at the work of the board. Tenth edition, 2017, Society for Corporate Governance and Deloitte Development LLC.(go back)

2 ibid.(go back)

3 ibid.(go back)

4 Missing Pieces Report: The 2016 Board Diversity Census of Women and Minorities on Fortune 500 Boards, 2017, Deloitte Development LLC.(go back)