Voici un article qui devrait inciter les entreprises à adopter de meilleures pratiques eu égard à la contribution des membres du conseil d’administration.

L’article a été publié sur le Forum de Harvard Law School par deux experts des questions stratégiques.

Jeffrey Greene est conseiller principal chez Fortuna Advisors et Sharath Sharma est le leader d’EY Americas pour les transformations stratégiques.

Je vous soumets la version française de l’introduction de la publication, en utilisant l’outil de traduction de Google, lequel est certainement perfectible.

Les équipes de direction n’ont pas à affronter seules les défis redoutables de la pandémie. Alors qu’ils passent de la stabilisation des flux de trésorerie et de la réingénierie des lieux de travail à la création d’un peu de répit — à la fois financièrement et mentalement — les PDG et la haute direction devraient réfléchir à la manière de déployer leurs conseils d’administration le plus efficacement possible.

Quelle que soit la situation de la performance de l’entreprise sur le spectre — de la difficulté (détaillants physiques) à la prospérité (logiciel de vidéoconférence), les dirigeants peuvent améliorer les résultats en :

Impliquer systématiquement les administrateurs dans les décisions critiques sur la stratégie, la culture, le renforcement de la résilience, la communication avec les investisseurs et la rémunération ;

Mettre l’accent sur la formation des administrateurs, notamment en approfondissant les connaissances de l’entreprise et de ses marchés ;

Tirer pleinement parti de l’expérience collective du conseil d’administration, des perspectives diverses, des connaissances en temps réel et des réseaux étendus.

La direction et les actionnaires ne peuvent pas se permettre de sous-utiliser le conseil d’administration pour faire face à cette crise, pour laquelle il n’existe pas de livres de recettes, ou à ses conséquences, qui ne ressembleront probablement pas aux reprises antérieures.

Les entreprises sont confrontées à des défis dans de multiples dimensions — science médicale, soins de santé, marchés financiers, économie, chaînes d’approvisionnement et géopolitique — pour lesquels leur seule approche viable est un processus de résolution de problèmes adaptatif, rapide et décisif, mais itératif, à mesure que de nouvelles informations apparaissent.

Les incertitudes accrues et évolutives dans chaque domaine signifient que les dirigeants doivent résoudre les tensions persistantes entre (1) faire face aux événements à court terme et (2) se préparer à d’éventuelles phases de reprise. La contribution des administrateurs est cruciale pour faciliter l’obtention d’un équilibre raisonnable.

Le tableau ci-dessous montre l’étendue des contributions des administrateurs en cette période critique.

Figure 1: Améliorer le rendement grâce à l’engagement actif du conseil

Une étude de cas pour mieux saisir l’engagement accru des administrateurs dans l’exercice de leurs rôles de fiduciaires

Pour décider comment éduquer, informer et impliquer les administrateurs dans l’environnement actuel, les pratiques de gouvernance de Netflix nous fournissent une étude de cas instructive :

Les administrateurs assistent régulièrement aux réunions de la haute direction à titre d’observateurs ;

Avant chaque réunion du conseil, les administrateurs reçoivent une note narrative de 20 à 40 pages décrivant les performances, les tendances du secteur et les développements des concurrents, avec des liens vers les données sous-jacentes et l’analyse à l’appui ;

Les administrateurs ont accès à toutes les informations sur les systèmes internes de l’entreprise ;

Les membres du conseil sont habilités à assurer un suivi individuel avec le PDG et les autres dirigeants.

Ces pratiques ont vu le jour afin d’inciter les administrateurs à mieux comprendre les plans à long terme de la direction. Les administrateurs créditent la direction pour la transparence et pour la volonté de débattre des décisions de gestion, en toute confiance.

Il y a tellement d’étapes de transformation radicales majeures que Netflix a accomplies depuis que je suis membre du conseil d’administration : distribution de DVD en diffusion continue sur le Web, passage à l’international, engagement de millions de dollars en contenu…

L’équipe de direction est si réfléchie et ouverte aux différents points de vue dans le processus de prise de décision que cela rend les décisions très difficiles relativement plus aisées en raison de la rigueur du processus.

Chaque action pourrait s’appliquer directement aux défis de gestion de crise, de reprise et de croissance future auxquels chaque entreprise doit s’adapter aujourd’hui.

Des administrateurs bien informés avec des canaux de communication ouverts à la direction peuvent débattre des problèmes en temps réel et tester les hypothèses qui sous-tendent les recommandations des dirigeants.

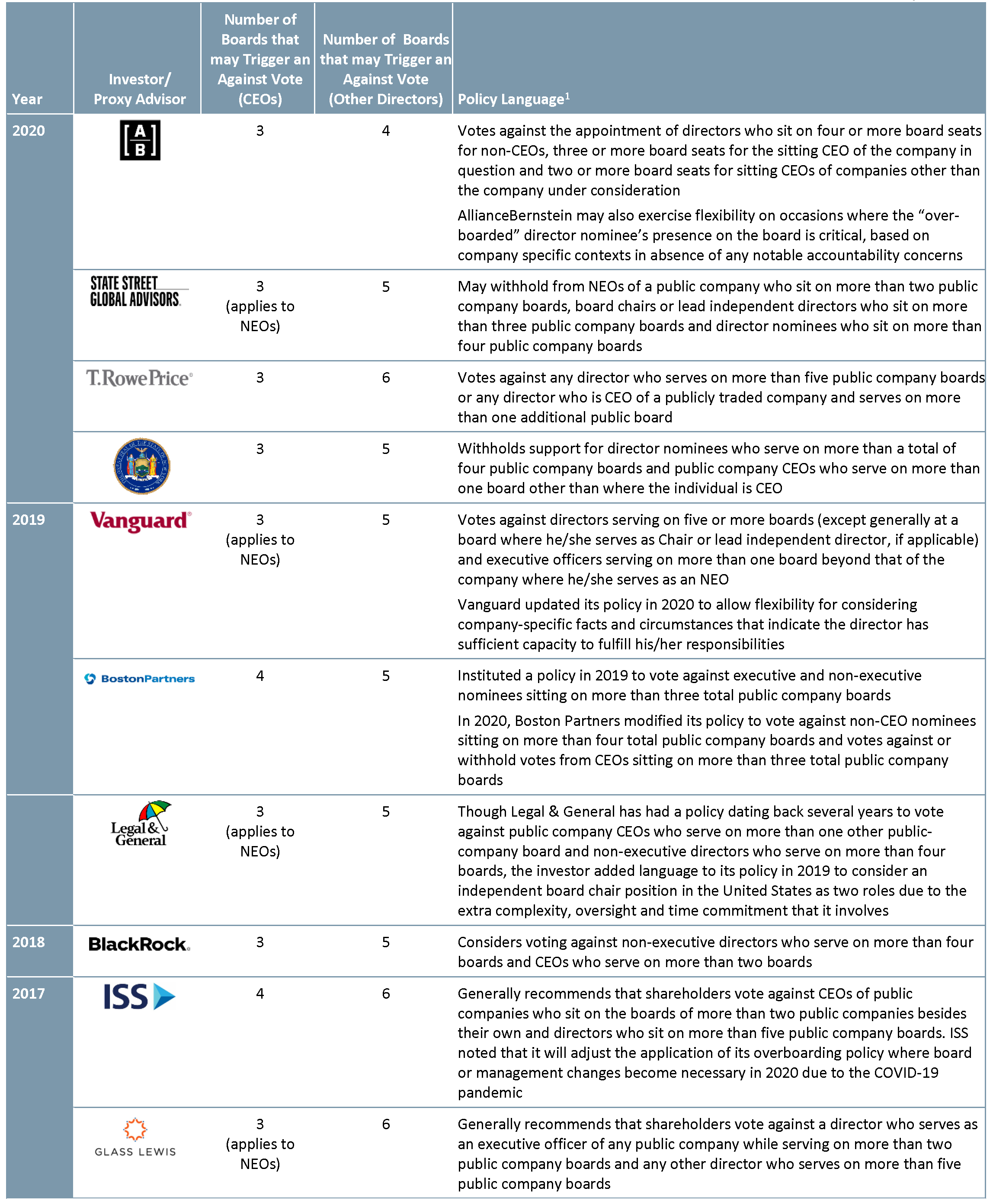

Quelles sont les lignes directrices énoncées par les firmes de conseil en vote américaines eu égard au nombre de conseils d’administration sur lesquels les administrateurs devraient siéger ?

L’article de Krystal Berrini * publié sur le site de Harvard Law School Forum on Corporate Governance, présente un très bon résumé des politiques mises de l’avant par les firmes de conseil en vote.

Voici une traduction Google révisée du court texte publié récemment.

Au cours des dernières années, de grands investisseurs institutionnels ont répondu à leurs préoccupations croissantes concernant les demandes de services au conseil en adoptant ou en renforçant des politiques concernant le nombre total d’engagements d’un administrateur.

Cette tendance a entraîné une baisse importante du soutien au vote pour certains administrateurs jugés « Overboard » selon ces lignes directrices nouvelles ou resserrées. Dans de nombreux cas, ces politiques sont plus strictes que celles des principaux conseillers en vote.

À l’approche de la saison des procurations 2020, trois investisseurs institutionnels, State Street Global Advisors (SSGA), T. Rowe Price et AllianceBernstein, ont resserré leurs politiques d’engagement des administrateurs.

Grâce à ces politiques d’investisseurs renforcées, les administrateurs non exécutifs qui siègent à plus de quatre conseils d’administration et les PDG qui siègent à plus d’un conseil d’administration externe peuvent s’attendre à voir une diminution du soutien des actionnaires par rapport aux années précédentes.

La pandémie de COVID-19 a concentré l’attention des investisseurs sur une gamme de sujets de gouvernance et de surveillance du conseil d’administration, y compris la gestion des risques, la continuité des activités et la gestion des ressources humaines. Au cours des dernières semaines, un certain nombre d’investisseurs, dont BlackRock et SSGA, ont réitéré leur engagement à tenir les entreprises responsables de leurs pratiques ESG à long terme pendant cette période difficile.

Il est peu probable que les investisseurs s’écartent des directives sur les pratiques existantes, y compris les engagements du conseil. La crise actuelle de COVID-19, qui impose des contraintes supplémentaires au temps consenti par les administrateurs, renforcera probablement encore davantage les points de vue des investisseurs sur l’importance d’avoir la capacité de s’engager pleinement dans tous leurs engagements au sein du conseil en temps de crise.

Vous trouverez ci-dessous un résumé des mises à jour récentes des politiques des investisseurs et des conseillers en matière de procuration sur la participation excessive des administrateurs.

Le tableau indique le nombre de conseils auxquels un administrateur recevra généralement une recommandation ou un vote négatifs. En règle générale, les investisseurs et les conseillers en vote ne s’opposent aux administrateurs exécutifs (PDG) qu’en ce qui concerne leurs engagements comme administrateurs externes.

Les informations concernant les politiques de conseil aux investisseurs et aux procurations sont obtenues à partir des politiques américaines publiées qui peuvent être consultées sur leurs sites Web respectifs.

Depuis le début de la crise de santé publique et économique causée par la COVID-191, la tentation peut être grande pour les administrateurs de s’immiscer dans la gestion quotidienne de la société ou se substituer à la direction, surtout s’ils portent également le chapeau d’actionnaire. Or, c’est le comité de gestion de crise, souvent composé de dirigeants exécutifs, qui a la responsabilité de gérer la crise au quotidien. Néanmoins, les administrateurs ont eux aussi un rôle à jouer : ils ont le devoir de s’assurer de la bonne gouvernance de la société à court, moyen et long terme2.

Cette responsabilité s’accroît face à la crise et commande une réflexion pour les administrateurs de sociétés qui devront, d’une part, examiner attentivement la manière de gérer les risques actuels au sein de l’organisation ainsi que les risques collatéraux qui pourraient en découler et, d’autre part, prendre note des éléments à améliorer pour le futur.

Dans le cadre de cet article sur la gouvernance de sociétés en période de crise, nous nous penchons plus spécifiquement sur les réflexes de gouvernance à adopter dans le contexte actuel, tout en ne perdant pas de vue l’après COVID-19.

Voici dix éléments qui doivent être pris en considération au moment où toutes les entreprises sont préoccupées par la crise du COVID-19.

Cet article très poussé a été publié sur le forum du Harvard Law School of Corporate Governance hier.

Les juristes Holly J. Gregory et Claire Holland, de la firme Sidley Austin font un tour d’horizon exhaustif des principales considérations de gouvernance auxquelles les conseils d’administration risquent d’être confrontés durant cette période d’incertitude.

Je vous souhaite bonne lecture. Vos commentaires sont appréciés.

The 2019 novel coronavirus (COVID-19) pandemic presents complex issues for corporations and their boards of directors to navigate. This briefing is intended to provide a high-level overview of the types of issues that boards of directors of both public and private companies may find relevant to focus on in the current environment.

Corporate management bears the day-to-day responsibility for managing the corporation’s response to the pandemic. The board’s role is one of oversight, which requires monitoring management activity, assessing whether management is taking appropriate action and providing additional guidance and direction to the extent that the board determines is prudent. Staying well-informed of developments within the corporation as well as the rapidly changing situation provides the foundation for board effectiveness.

We highlight below some key areas of focus for boards as this unprecedented public health crisis and its impact on the business and economic environment rapidly evolves.

1. Health and Safety

With management, set a tone at the top through communications and policies designed to protect employee wellbeing and act responsibly to slow the spread of COVID-19. Monitor management’s efforts to support containment of COVID-19 and thereby protect the personal health and safety of employees (and their families), customers, business partners and the public at large. Consider how to mitigate the economic impact of absences due to illness as well as closures of certain operations on employees.

2. Operational and Risk Oversight

Monitor management’s efforts to identify, prioritize and manage potentially significant risks to business operations, including through more regular updates from management between regularly scheduled board meetings. Depending on the nature of the risk impact, this may be a role for the audit or risk committee or may be more appropriately undertaken by the full board. Document the board’s consideration of, and decisions regarding, COVID-19-related matters in meeting minutes. Maintain a focus on oversight of compliance risks, especially at highly regulated companies. Watch for vulnerabilities caused by the outbreak that may increase the risk of a cybersecurity breach.

3. Business Continuity

Consider whether business continuity plans are in place appropriate to the potential risks of disruption identified, including through a discussion with management of relevant contingencies, and continually reassess the adequacy of the plans in light of developments. Key issues to consider include:

Employee/Talent Disruption. As more employees begin working remotely or are unable to work due to disruptions caused by COVID-19, continually assess what minimum staffing levels and remote work technology will be required to maintain operations. (Also, as noted above, consider how to mitigate the economic impact of absences due to illness as well as closures of certain operations on employees.)

Supply Chain and Production Disruption. Review with management the risks that a disruption in the supply chain will cause interruptions in operations and how to protect against such risks, including the availability of alternate sources of supply. Ask management to assess the risks that the company will have difficulty in fulfilling its contractual obligations and how management is preparing to address those risks, including through review of relevant provisions in customer contracts (e.g., force majeure, events of default and termination) to determine what recourse is available.

Financial Impact and Liquidity. Review with management the near-term and longer term financial impact (including the ability to meet obligations) of the COVID-19 pandemic and the related impact of the extreme volatility in the financial markets. Understand the assumptions underlying management’s assessment and discuss the likely outcome if those assumptions prove incorrect. Consider the need to seek additional financing or amend the terms of existing debt arrangements.

Internal Controls and Audit Function. Consider whether COVID-19 may have an impact on the functioning of internal controls and audit. For publicly-traded companies, remember that any material changes in internal control over financial reporting will require disclosure in the next periodic report.

Recent Securities Exchange Commission (SEC) guidance: In a March 4, 2020 press release, SEC Chair Jay Clayton urged companies to work with their audit committees and auditors to ensure that their financial reporting, auditing and review processes are sufficiently robust to enable them to meet their obligations under the federal securities laws in the current environment.

Key Person Risks and Emergency Succession Plans. Consider whether an up-to-date emergency succession plan is in place that identifies a person who can step in immediately as interim CEO in the event the CEO contracts COVID-19. Consider the need to implement similar plans for other key persons.

Incentives. Consider whether incentive plans need to be reworked in light of the circumstances, to ensure that appropriate behaviors are encouraged. Consider delaying setting incentive plan goals until the uncertainty has subsided or try to build in flexibility with respect to any goals set.

Board/Governance Continuity. Consider whether the board is appropriately positioned to provide guidance and oversight as the COVID-19 threat expands. Consider scheduling in advance special board meetings and/or information conference calls over the next three to four months, which can be cancelled if not needed. Decide whether to replace in-person meetings with conference calls to help limit the threat of contagion. Consider whether contingencies are in place if a board quorum is not available. Continue to meet regularly in executive session to discuss assessment of how management is managing the crisis.

4. Crisis Management

During this turbulent time, employees, shareholders and other stakeholders will look to boards to take swift and decisive action when necessary. Consider whether an up-to-date crisis management plan is in place and effective. A well-designed plan will assist the company to react appropriately, without either under- or over-reacting. Elements of an effective crisis management plan include:

Cross-Functional Team. Crisis response teams typically include key individuals from management, public relations, human resources, legal and finance. Identify these individuals now and begin meeting so that they are prepared to respond quickly as the crisis develops. The team should be in regular contact with the board (or a designated board member or committee) as the COVID-19 pandemic evolves.

Quick and Decisive Deployment. The plan should include crisis response procedures, communications templates, checklists and manuals that can be readily adapted to a variety of situations for effective, time-critical and agile deployment. The crisis response team should be familiar with the elements of the plan and ready to implement it at a moment’s notice.

Contingency Plans. A crisis is inherently unpredictable. However, the company should endeavor to anticipate all potential crises to which it is vulnerable and develop contingency plans to deal with those crises to minimize on-the-fly decision-making.

Examples of scenarios to prepare for: What will our response be if there is a confirmed case of COVID-19 within the company? How will we notify employees of a confirmed case and what privacy implications do we need to consider? What planning (e.g., IT training) is required if we need to mandate that our employees work remotely?

Thoughtful Communications. The board should oversee the company’s communication strategy. Clear communication and planning within the crisis response team will allow the company to communicate internally and externally in a calm and thoughtful manner, which will help build confidence during a volatile situation.

5. Oversight of Public Reporting and Disclosure for Publicly-Traded Companies

Companies must consider whether they are making sufficient public disclosures about the actual and expected impacts of COVID-19 on their business and financial condition. The level of disclosure required will depend on many factors, such as whether a company has significant operations in China or is in a highly affected industry (e.g., airlines and hospitality companies). In any event, boards should monitor to ensure that corporate disclosures are accurate and complete and reflect the changing circumstances.

Because the COVID-19 pandemic is unprecedented and changing by the day, the SEC acknowledges that it is challenging to provide accurate information about the impact it could have on future operations.

Recent SEC guidance: “We recognize that [the current and potential effects of COVID-19] may be difficult to assess or predict with meaningful precision both generally and as an industry- or issuer-specific basis.” Statement by SEC Chairman Jay Clayton on January 30, 2020.

Earnings Guidance. Consider whether previously issued earnings guidance should be downgraded to reflect the actual or likely impact of COVID-19 and, if so, how to describe the reason for the revision. Due to the current unpredictability of COVID-19’s impact, consider withdrawing previously-issued earnings guidance altogether or refraining from issuing guidance in the near term.

Risk Factor Disclosure. Consider how the COVID-19 pandemic may require additions or revisions to risk factor disclosures.

Recent SEC guidance: “We also remind all companies to provide investors with insight regarding their assessment of, and plans for addressing, material risks to their business and operations resulting from the coronavirus to the fullest extent practicable to keep investors and markets informed of material developments.” SEC March 4, 2020 press release.

Potential topics for risk factor disclosure include:

Disruptions to business operations whether from travel restrictions, mandated quarantines or voluntary “social distancing” that affects employees, customers and suppliers, production delays, closures of manufacturing facilities, warehouses and logistics supply and distribution chains and staffing shortages

Uncertainty regarding global macroeconomic conditions, particularly the uncertainty related to the duration and impact of the COVID-19 pandemic, and related decreases in customer demand and spending

Credit and liquidity risk, loan defaults and covenant breaches

Inventory writedowns and impairment losses

Ensure that risk factor disclosure is consistent with the board’s conversations with management about material risks.

Recent SEC guidance: “One analytical tool to evaluate disclosure in this context is to consider how management discusses … risks with its board of directors. Obviously not all discussions between management and the board are appropriate for disclosure in public filings, but there should not be material gaps between how the board is briefed and how shareholders are informed.” Statement by SEC Director, Division of Corporation Finance William Hinman on March 15, 2019.

As always, risk factor disclosure should be specific to a company’s individual circumstances and avoid generic language. Finally, be careful not to describe a risk related to COVID-19 as hypothetical if it has actually occurred.

Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A). Consider whether the actual or likely impact of COVID-19 on a company’s business (including its supply chain), financial condition, liquidity, results of operations and/or prospects would be deemed material to an investment decision in the company’s securities and require disclosure. Consider whether the impact or potential impact of COVID-19 on the company is a “known trend or uncertainty” requiring disclosure in the MD&A of the next periodic report. Tailor any MD&A disclosures to the impact of COVID-19 on the company’s business in particular. Consider whether disclosures appropriately address the potential impact of the COVID-19 pandemic on future results of operations.

Subsequent Events. A joint statement by SEC and Public Company Accounting Oversight Board (PCAOB) leadership on February 19, 2020 specific to COVID-19 reporting considerations encouraged companies to consider the need to potentially disclose subsequent events in the notes to the financial statements in accordance with guidance included in Accounting Standards Codification 855, Subsequent Events.

Forward-Looking Statements. Consider whether the company’s forward-looking statement disclaimer language adequately protects the company for statements it makes regarding the expected impacts of COVID-19. It should be specific and consistent with updates made to the risk factors and other public disclosures.

Recent SEC guidance: “Companies providing forward-looking information in an effort to keep investors informed about material developments, including known trends or uncertainties regarding the coronavirus, can take steps to avail themselves of the safe harbor in Section 21E of the Exchange Act for this information.” SEC March 4, 2020 press release.

Updates. Consider whether prior disclosures should be revised to ensure they are accurate and complete. While there is no express duty to update a forward-looking statement, courts are divided as to whether a duty to update exists for a forward-looking statement that becomes inaccurate or misleading after the passage of time (from the perspective of claim under Exchange Act Section 10(b) and Rule 10b-5).

Recent SEC guidance: “Depending on a company’s particular circumstances, it should consider whether it may need to revisit, refresh, or update previous disclosure to the extent that the information becomes materially inaccurate.” SEC March 4, 2020 press release.

Proxy Statements. Given the SEC’s emphasis on discussion of how boards oversee the management of material risks, consider expanding the proxy statement disclosure of board oversight of COVID-19-related risks where material to the business. 5Recent SEC guidance: “To the extent a matter presents a material risk to a company’s business, the company’s disclosure should discuss the nature of the board’s role in overseeing the management of that risk. The Commission last noted this in the context of cybersecurity, when it stated that disclosure about a company’s risk management program and how the board engages with the company on cybersecurity risk management allows investors to better assess how the board is discharging its risk oversight function. Parallels may be drawn to other areas where companies face emerging or uncertain risks, so companies may find this guidance useful when preparing disclosures about the ways in which the board manages risks, such as those related to sustainability or other matters.” Statement by SEC Director, Division of Corporation Finance William Hinman on March 15, 2019.

Also, consider cautioning stockholders that the annual meeting date and logistics are subject to change.

Current Reports. Consider the need to file a Form 8-K for material developments such as if the CEO or another key person or a significant portion of the workforce contracts COVID-19.

Conditional Filing Relief. Companies that anticipate filing delays due to COVID-19 should consider taking advantage of the SEC’s March 4, 2020 order granting an additional 45 days to meet Exchange Act reporting obligations for reports due between March 1 and April 30, 2020. See the Sidley Update available here for more details.

6. Compliance with Insider Trading Restrictions and Regulation FD for Publicly-Traded Companies

Insider Trading. Closely monitor and consider further restricting trading in company securities by insiders who may have access to material nonpublic information related to COVID-19 impacts (e.g., by requiring additional training, imposing blackout periods or enhancing preclearance procedures).

Recent SEC guidance: If a company “become[s] aware of a risk related to the coronavirus that would be material to its investors, it should refrain from engaging in securities transactions with the public and … take steps to prevent directors and officers (and other corporate insiders who are aware of these matters) from initiating such transactions until investors have been appropriately informed about the risk.” SEC March 4, 2020 press release.

Carefully consider whether the company should potentially buy back stock to take advantage of significantly depressed stock prices.

Regulation FD. Be mindful of Regulation FD requirements, particularly if sharing information related to the impact of COVID-19 with customers and other stakeholders.

Recent SEC guidance: “When companies do disclose material information related to the impacts of the coronavirus, they are reminded to take the necessary steps to avoid selective disclosures and to disseminate such information broadly.” SEC March 4, 2020 press release.

7.Annual Shareholder Meeting

With the Center for Disease Control recommending that gatherings of 50 or more persons be avoided to assist in containment of the virus, consider with management whether to hold a virtual-only shareholders meeting or a hybrid meeting that permits both in-person and online attendance. Public companies that are considering changing the date, time and/or location of an annual meeting, including a switch from an in-person meeting to a virtual or hybrid meeting, will need to review applicable requirements under state law, stock exchange rules and the company’s charter and bylaws. Companies that change the date, time and/or location of an annual meeting should comply with the March 13, 2020 guidance issued by the Staff of the SEC’s Division of Corporation Finance and the Division of Investment Management. See the Sidley Update available here for more details.

8. Shareholder Relations

Activism and Hostile Situations. Continue to ensure communication with, and stay attuned to the concerns of, significant shareholders, while monitoring for changes in stock ownership. Capital redemptions at small- and mid-sized funds may lead to fewer shareholder activism campaigns and proxy contests in the next several months. However, expect well-capitalized activists to exploit the enhanced vulnerability of target companies. The same applies to unsolicited takeovers bids by well-capitalized strategic buyers. If they have not already done so, boards should update or activate defense preparation plans, including by identifying special proxy fight counsel, reviewing structural defenses, putting a poison pill “on the shelf” and developing a “break the glass” communications plan.

9. Strategic Opportunities

Consider with management whether and if so where opportunities are likely to emerge that are aligned with the corporation’s strategy, for example, opportunities to fulfill an unmet need occasioned by the pandemic or opportunities for growth through distressed M&A.

10. Aftermath

Consider with management whether the changes in behavior occasioned by the pandemic will have any potential lasting effects, for example on employee and consumer behavior and expectations. Also, be prepared when the crisis abates to assess the corporation’s handling of the situation and identify “lessons learned” and actionable ideas for improvement.

Voici un cas publié sur le site de Julie McLelland qui aborde une situation où Trevor, un administrateur indépendant, croyait que le grand succès de l’entreprise était le reflet d’une solide gouvernance.

Trevor préside le comité d’audit et il se soucie de mettre en place de saines pratiques de gouvernance. Cependant, cette société cotée en bourse avait des failles en matière de gestion des risques numériques et de cybersécurité.

De plus, le seul administrateur indépendant n’a pas été informé qu’un vol de données très sensibles avait été fait et que des demandes de rançons avaient été effectuées.

L’organisation a d’abord nié que les informations subtilisées provenaient de leurs systèmes, avant d’admettre que les données avaient été fichées un an auparavant ! Les résultats furent dramatiques…

Trevor se demande comment il peut aider l’organisation à affronter la tempête !

Le cas a d’abord été traduit en français en utilisant Google Chrome, puis, je l’ai édité et adapté. On y présente la situation de manière sommaire puis trois experts se prononcent sur le cas.

Bonne lecture ! Vos commentaires sont toujours les bienvenus.

Trevor est administrateur d’une société cotée qui a été un «chouchou du marché». La société fournit des évaluations de crédit et une vérification des données. Les fondateurs ont tous deux une solide expérience dans le secteur et un solide réseau de contacts et à une liste de clients qui comprenait des gouvernements et des institutions financières.

Après l’entrée en bourse, il y a deux ans, la société a atteint ou dépassé les prévisions et Trevor est fier d’être le seul administrateur indépendant siégeant au conseil d’administration aux côtés des deux fondateurs et du PDG. Il préside le comité d’audit et, officieusement, il a été l’initiateur des processus de gouvernance et de sa documentation.

Les fondateurs sont restés très actifs dans l’entreprise et Trevor s’est parfois inquiété du fait que certaines décisions stratégiques n’avaient pas été portées à son attention avant la réunion du conseil d’administration. Comme l’expérience de Trevor est l’audit et l’assurance, il suppose qu’il n’aurait pas ajouté de valeur au-delà de la garantie d’un processus sain et de la tenue de registres.

Il y a trois semaines, tout a changé. Une grande partie des données de l’entreprise ont été subtilisées et transférées sur le « dark web ». Ce vol comprenait les données financières des personnes qui avaient été évaluées ainsi que des données d’identification tels que les numéros de dossier fiscal et les adresses résidentielles. Pire, la société a d’abord affirmé que les informations ne provenaient pas de leurs systèmes, puis a admis avoir reçu des demandes de rançon indiquant que les données avaient été fichées jusqu’à un an avant cette catastrophe.

Plusieurs clients ont fermé leur compte, les actionnaires sont consternés, le cours de l’action est en chute libre et la presse réclame plus d’informations.

Comment Trevor devrait-il aider l’entreprise à surmonter cette tempête ?

This is a critical time for Trevor legally and reputationally, it is also a time when being an independent director carries additional responsibility to the company, the shareholders, the staff and the customers.

All Directors and Executives can only have one response to a blackmail attempt. That is to immediately report it to the police and not respond to the ransomware demands. Secondly the company should have had a crisis management plan in place ready for such an eventuality. In this day and age, no company should operate without a cybercrime contingency plan.

In this case it is unclear, but it appears that the authorities were not informed and that Trevor’s company was unprepared for a data breach or ransomware demands.

There are 2 scenarios open to Trevor:

1) If Trevor was not informed straight away of the ransom demands and the CEO and founding Executive Directors knew but did not brief him on the ransom issue and the company’s response, then his independent status has been compromised and he should resign.

2) If Trevor was informed and the whole Board was involved in the response, then Trevor must remain and help the company ride out the storm. This will involve working with the police, the ASX and crisis management guidance from external suppliers – technical and PR.

The rule to follow is full transparency and speedy action.

Trevor should refer to the recent ransomware attack on Toll Logistics and their response which was exemplary.

Adam Salzer OAM is the Chair and Global Designer for Whitewater Transformations. His other board experience includes Australian Transformation and Turnaround Association (AusTTA), Asian Transformation and Turnaround Association (ATTA), Australian Deafness Council, Bell Shakespeare Company, and NSW Deaf Society. He is based in Sydney, Australia.

Julie’s Answer

This is a listed company; Trevor must ensure appropriate disclosure. A trading halt may give the company time to investigate, and respond to, the events and then give the market time to disseminate the information. His customer liaison at the stock exchange should assist with implementing a halt and issuing a brief statement saying what has happened and that the company will issue more information when it becomes available.

This will be a costly and distracting exercise that could derail the company from its current successful track.

Three of the four board members are executives. That doesn’t mean the fourth can rely on their efforts. Trevor must add value by asking intelligent questions that people involved in the operations will possibly not think to ask. This board must work as a team rather than a group of individuals who each contribute their own expertise and then come together to document decisions that were not made rigorously or jointly.

Trevor has now learnt that there is more to good governance than just having meetings and documenting processes. He needs to get involved and truly understand the business. If his fellow directors do not welcome this, he needs to consider whether they are taking him seriously or just using him as window-dressing. He should ensure that the whole board is never again left out of the information flow when something important happens (or even when it perhaps might happen).

He should also take the lead on procuring legal advice (they are going to need it), liaising with the regulators, and establishing crisis communications. Engaging a specialist communications firm may help.

Julie Garland McLellan is a non-executive director and board consultant based in Sydney, Australia.

Jinan’s Answer

I recommend three separate parallel streams of work for Trevor.

1. Immediate public facing actions Immediately apologize and state your commitment to your customers. Hire a PR firm and have the most public facing person issue an apology. The person selected to issue the apology has to be selected carefully (cannot be the person responsible for leak, and has potential to become the new trusted CEO)

2. Tactical internal actions Assess the damage and contain the incident. Engage an incident response firm to assess how the breach happened, when it happened, what was stolen. Confirm that leak doors are closed. Select your IR firm carefully – the better reputed they are, the better you will look in litigation. Conduct an immediate audit and investigation. You need to understand who knew, when and why this was buried for a year. Take disciplinary action against anyone who was part of the breach. Post audit, either allow them to keep their equity or buy them out.

3. Strategic actions Review and update your cybersecurity incident response process. This includes your ransomware processes (e.g. will you pay, how you pay, etc.), and how you communicate incidents. Build cybersecurity awareness, behavior and culture up, down and across your company. Ensure that everyone from the board down are educated, enabled and enthusiastic about their own and your company’s cyber-safety. This is a journey not a one-off miracle. Extend cybersecurity engagement to your customers. Be proactive not only on the status of this incident, but also on how you are keeping their data safe. Go a step further and offer them help in their own cyber-safety. Create a forward thinking, business and risk-aligned cybersecurity strategy. Understand your current people, process and technology gaps which led to this decision and how you’ll fix them. Elevate the role of cybersecurity leadership. You will need a chief information security officer who is empowered to execute the strategy, and has a regular and independent seat at the board table.

Jinan Budge is Principal Analyst Serving Security and Risk Professionals at Forrester and a former Director Cyber Security, Strategy and Governance at Transport for NSW. She is based in Sydney, New South Wales, Australia.

En gouvernance des sociétés, il existe un certain nombre de responsabilités qui relèvent impérativement d’un conseil d’administration.

À la suite d’une décision rendue par la Cour Suprême du Delaware dans l’interprétation de la doctrine Caremark (voir ici),il est indiqué que pour satisfaire leur devoir de loyauté, les administrateurs de sociétés doivent faire des efforts raisonnables (de bonne foi) pour mettre en œuvre un système de surveillance et en faire le suivi.

Without more, the existence of management-level compliance programs is not enough for the directors to avoid Caremark exposure.

L’article de Martin Lipton *, paru sur le Forum de Harvard Law School on Corporate Governance, fait le point sur ce qui constitue les meilleures pratiques de gouvernance à ce jour.

Recognize the heightened focus of investors on “purpose” and “culture” and an expanded notion of stakeholder interests that includes employees, customers, communities, the economy and society as a whole and work with management to develop metrics to enable the corporation to demonstrate their value;

Be aware that ESG and sustainability have become major, mainstream governance topics that encompass a wide range of issues, such as climate change and other environmental risks, systemic financial stability, worker wages, training, retraining, healthcare and retirement, supply chain labor standards and consumer and product safety;

Oversee corporate strategy (including purpose and culture) and the communication of that strategy to investors, keeping in mind that investors want to be assured not just about current risks and problems, but threats to long-term strategy from global, political, social, and technological developments;

Work with management to review the corporation’s strategy, and related disclosures, in light of the annual letters to CEOs and directors, or other communications, from BlackRock, State Street, Vanguard, and other investors, describing the investors’ expectations with respect to corporate strategy and how it is communicated;

Set the “tone at the top” to create a corporate culture that gives priority to ethical standards, professionalism, integrity and compliance in setting and implementing both operating and strategic goals;

Oversee and understand the corporation’s risk management, and compliance plans and efforts and how risk is taken into account in the corporation’s business decision-making; monitor risk management ; respond to red flags if and when they arise;

Choose the CEO, monitor the CEO’s and management’s performance and develop and keep current a succession plan;

Have a lead independent director or a non-executive chair of the board who can facilitate the functioning of the board and assist management in engaging with investors;

Together with the lead independent director or the non-executive chair, determine the agendas for board and committee meetings and work with management to ensure that appropriate information and sufficient time are available for full consideration of all matters;

Determine the appropriate level of executive compensation and incentive structures, with awareness of the potential impact of compensation structures on business priorities and risk-taking, as well as investor and proxy advisor views on compensation;

Develop a working partnership with the CEO and management and serve as a resource for management in charting the appropriate course for the corporation;

Monitor and participate, as appropriate, in shareholder engagement efforts, evaluate corporate governance proposals, and work with management to anticipate possible takeover attempts and activist attacks in order to be able to address them more effectively, if they should occur;

Meet at least annually with the team of company executives and outside advisors that will advise the corporation in the event of a takeover proposal or an activist attack;

Be open to management inviting an activist to meet with the board to present the activist’s opinion of the strategy and management of the corporation;

Evaluate the individual director’s, board’s and committees’ performance on a regular basis and consider the optimal board and committee composition and structure, including board refreshment, expertise and skill sets, independence and diversity, as well as the best way to communicate with investors regarding these issues;

Review corporate governance guidelines and committee workloads and charters and tailor them to promote effective board and committee functioning;

Be prepared to deal with crises; and

Be prepared to take an active role in matters where the CEO may have a real or perceived conflict, including takeovers and attacks by activist hedge funds focused on the CEO.

Afin de satisfaire ces attentes, les entreprises publiques doivent :

Have a sufficient number of directors to staff the requisite standing and special committees and to meet investor expectations for experience, expertise, diversity, and periodic refreshment;

Compensate directors commensurate with the time and effort that they are required to devote and the responsibility that they assume;

Have directors who have knowledge of, and experience with, the corporation’s businesses and with the geopolitical developments that affect it, even if this results in the board having more than one director who is not “independent”;

Have directors who are able to devote sufficient time to preparing for and attending board and committee meetings and engaging with investors;

Provide the directors with the data that is critical to making sound decisions on strategy, compensation and capital allocation;

Provide the directors with regular tutorials by internal and external experts as part of expanded director education and to assure that in complicated, multi-industry and new-technology corporations, the directors have the information and expertise they need to respond to disruption, evaluate current strategy and strategize beyond the horizon; and

Maintain a truly collegial relationship among and between the company’s senior executives and the members of the board that facilitates frank and vigorous discussion and enhances the board’s role as strategic partner, evaluator, and monitor.

Martin Lipton* is a founding partner of Wachtell, Lipton, Rosen & Katz, specializing in mergers and acquisitions and matters affecting corporate policy and strategy. This post is based on a Wachtell Lipton memorandum by Mr. Lipton and is part of the Delaware law series; links to other posts in the series are available here.

En gouvernance des sociétés, il existe un certain nombre de responsabilités qui relèvent impérativement d’un conseil d’administration.

À la suite d’une décision rendue par la Cour Suprême du Delaware dans l’interprétation de la doctrine Caremark (voir ici),il est indiqué que pour satisfaire leur devoir de loyauté, les administrateurs de sociétés doivent faire des efforts raisonnables (de bonne foi) pour mettre en œuvre un système de surveillance et en faire le suivi.

Without more, the existence of management-level compliance programs is not enough for the directors to avoid Caremark exposure.

L’article de Martin Lipton *, paru sur le Forum de Harvard Law School on Corporate Governance, fait le point sur ce qui constitue les meilleures pratiques de gouvernance à ce jour.

Recognize the heightened focus of investors on “purpose” and “culture” and an expanded notion of stakeholder interests that includes employees, customers, communities, the economy and society as a whole and work with management to develop metrics to enable the corporation to demonstrate their value;

Be aware that ESG and sustainability have become major, mainstream governance topics that encompass a wide range of issues, such as climate change and other environmental risks, systemic financial stability, worker wages, training, retraining, healthcare and retirement, supply chain labor standards and consumer and product safety;

Oversee corporate strategy (including purpose and culture) and the communication of that strategy to investors, keeping in mind that investors want to be assured not just about current risks and problems, but threats to long-term strategy from global, political, social, and technological developments;

Work with management to review the corporation’s strategy, and related disclosures, in light of the annual letters to CEOs and directors, or other communications, from BlackRock, State Street, Vanguard, and other investors, describing the investors’ expectations with respect to corporate strategy and how it is communicated;

Set the “tone at the top” to create a corporate culture that gives priority to ethical standards, professionalism, integrity and compliance in setting and implementing both operating and strategic goals;

Oversee and understand the corporation’s risk management, and compliance plans and efforts and how risk is taken into account in the corporation’s business decision-making; monitor risk management ; respond to red flags if and when they arise;

Choose the CEO, monitor the CEO’s and management’s performance and develop and keep current a succession plan;

Have a lead independent director or a non-executive chair of the board who can facilitate the functioning of the board and assist management in engaging with investors;

Together with the lead independent director or the non-executive chair, determine the agendas for board and committee meetings and work with management to ensure that appropriate information and sufficient time are available for full consideration of all matters;

Determine the appropriate level of executive compensation and incentive structures, with awareness of the potential impact of compensation structures on business priorities and risk-taking, as well as investor and proxy advisor views on compensation;

Develop a working partnership with the CEO and management and serve as a resource for management in charting the appropriate course for the corporation;

Monitor and participate, as appropriate, in shareholder engagement efforts, evaluate corporate governance proposals, and work with management to anticipate possible takeover attempts and activist attacks in order to be able to address them more effectively, if they should occur;

Meet at least annually with the team of company executives and outside advisors that will advise the corporation in the event of a takeover proposal or an activist attack;

Be open to management inviting an activist to meet with the board to present the activist’s opinion of the strategy and management of the corporation;

Evaluate the individual director’s, board’s and committees’ performance on a regular basis and consider the optimal board and committee composition and structure, including board refreshment, expertise and skill sets, independence and diversity, as well as the best way to communicate with investors regarding these issues;

Review corporate governance guidelines and committee workloads and charters and tailor them to promote effective board and committee functioning;

Be prepared to deal with crises; and

Be prepared to take an active role in matters where the CEO may have a real or perceived conflict, including takeovers and attacks by activist hedge funds focused on the CEO.

Afin de satisfaire ces attentes, les entreprises publiques doivent :

Have a sufficient number of directors to staff the requisite standing and special committees and to meet investor expectations for experience, expertise, diversity, and periodic refreshment;

Compensate directors commensurate with the time and effort that they are required to devote and the responsibility that they assume;

Have directors who have knowledge of, and experience with, the corporation’s businesses and with the geopolitical developments that affect it, even if this results in the board having more than one director who is not “independent”;

Have directors who are able to devote sufficient time to preparing for and attending board and committee meetings and engaging with investors;

Provide the directors with the data that is critical to making sound decisions on strategy, compensation and capital allocation;

Provide the directors with regular tutorials by internal and external experts as part of expanded director education and to assure that in complicated, multi-industry and new-technology corporations, the directors have the information and expertise they need to respond to disruption, evaluate current strategy and strategize beyond the horizon; and

Maintain a truly collegial relationship among and between the company’s senior executives and the members of the board that facilitates frank and vigorous discussion and enhances the board’s role as strategic partner, evaluator, and monitor.

Martin Lipton* is a founding partner of Wachtell, Lipton, Rosen & Katz, specializing in mergers and acquisitions and matters affecting corporate policy and strategy. This post is based on a Wachtell Lipton memorandum by Mr. Lipton and is part of the Delaware law series; links to other posts in the series are available here.

Les auteures ont une solide expérience de consultation dans plusieurs grandes sociétés et sont associées de la firme Arsenal Conseils, spécialisée en gouvernance et en stratégie.

Elles sont aussi régulièrement invitées comme conférencières et formatrices dans le domaine de la stratégie et de la gouvernance.

Dans ce billet, qui a d’abord été publié dans le Journal Les Affaires, elles abordent une situation vraiment difficile pour tout conseil d’administration : le congédiement de son directeur général.

Les auteures discutent des motifs liés au congédiement, de l’importance d’une absolue confidentialité et du courage requis de la part des administrateurs.

La publication de ce billet sur mon blogue a été approuvée par les auteurs.

Bonne lecture ! Vos commentaires sont les bienvenus.

De plus en plus de PDG congédiés pour des manquements à l’éthique

Peu importe le motif, le congédiement du PDG demeure une des décisions les plus difficiles à prendre pour un conseil d’administration. Selon notre expérience, aucun CA n’est jamais tout à fait prêt à faire face à cette situation. Toutefois, certains facteurs peuvent faciliter la gestion de cette crise.

Le motif de congédiement influence la rapidité de réaction du conseil d’administration

Selon une étude américaine, les administrateurs sont plus prompts et rapides à congédier un PDG qu’autrefois, et ils le font de plus en plus pour des raisons éthiques.

Bien entendu, la décision de congédier le PDG sera plus facile à prendre lorsque le comportement du PDG pose un risque réputationnel pour l’entreprise. C’est notamment le cas en présence de comportements inadéquats, de fraude ou de perte de confiance des clients.

À titre d’exemple, la triste histoire de Brandon Truaxe, qualifié de génie des cosmétiques et fondateur de la marque de cosmétique canadienne The Ordinary, véritable phénomène mondial. L’automne dernier, les actionnaires et administrateurs de Deciem, groupe duquel fait partie la marque ont demandé et obtenu sa destitution, à titre d’administrateur et de PDG de Deciem. Le Groupe Estée Lauder, actionnaire minoritaire et dont un représentant est administrateur, estimait alors que le comportement erratique du PDG, qui a annoncé sans fondement la fermeture de son entreprise et qualifié ses employés de criminels, nuisait à la réputation de son entreprise, de ses administrateurs et de ses actionnaires en plus de compromettre le futur de l’entreprise.

À l’opposé, les administrateurs tergiversant plus longuement lorsque la situation est plus ambiguë et moins cristalline. Stratégie défaillante, équipe de gestion inadéquate ou mise à niveau technologique mal gérée, ces situations ne font pas toujours l’unanimité au sein du conseil à savoir si elles constituent ou non des motifs suffisants de congédiement. Dans ces cas, les discussions seront souvent plus longues et plus partagées.

Une bonne dynamique au sein du conseil d’administration facilite la tâche des administrateurs lorsque survient une crise. Dans ces circonstances, il est essentiel que les administrateurs placent l’intérêt supérieur de l’organisation au sommet de leurs préoccupations. Les intérêts personnels doivent demeurer au vestiaire. Pas toujours facile lorsque le conseil a appuyé un PDG pendant plusieurs années, que celui-ci a contribué à notre recrutement comme administrateur ou que l’entreprise se porte généralement bien, mais que le conseil d’administration juge que le PDG n’est plus la bonne personne pour mener l’organisation vers ses nouveaux défis.

Un CA mobilisé fait une différence lors des prises de décisions difficiles. Cette mobilisation se prépare de longue date. Elle n’apparaît pas de façon spontanée en période de haute tension.

Par ailleurs, les conseils qui mènent, sur une base annuelle, des exercices de simulation de crise sont également plus efficaces dans la prise de décisions difficiles, et sous-pression, tel le congédiement du PDG.

Confidentialité absolue

Une fois saisi de la question du congédiement du PDG, le conseil d’administration, même sous pression, doit agir rapidement tout en prenant le temps requis pour délibérer. Délicat équilibre à trouver ! Choisir de se départir du PDG est une décision fondamentale qui ne doit pas être prise à la légère. Pour ce faire, certains CA choisissent de mandater le comité exécutif ou un comité ad hoc pour évaluer en profondeur les tenants et aboutissants de la situation. Le CA sera par la suite mis au fait de leurs travaux et en discutera en plénière. Trois choix possibles : supporter, coacher ou congédier.

Dans tous les cas, aucun compromis possible sur la confidentialité des échanges ! Rien de pire qu’une décision de cette nature qui s’ébruite ou qui traîne en longueur. Parlez-en à cette PME des Laurentides dont le sujet du congédiement du PDG a alimenté les discussions de corridor et miné le moral des employés pendant quelques semaines alors que les rencontres du CA sur le sujet se tenaient dans une salle à l’insonorisation sonore…

Congédier le PDG est une chose, choisir son successeur en est une autre. Peu importe qu’une solution par intérim ou permanente soit retenue, le conseil d’administration doit prévoir le futur et la continuité des opérations. Il doit impérativement développer un plan pour la succession du PDG ou activer celui déjà en place. Pendant cette période de transition, les administrateurs doivent être conscients que leur engagement envers l’entreprise pourrait être plus soutenu.

Faire face à la musique

Enfin, le CA doit s’assurer d’une stratégie de communication impeccable pour le congédiement du PDG. Employés, clients, autorités gouvernementales, les parties prenantes de l’entreprise devront tôt ou tard être mises au fait de ce changement à la tête de l’entreprise. Assurez-vous de développer des messages cohérents et de choisir les bons canaux de communication.

Sophie-Emmanuelle Chebin*, LL.L, MBA, IAS.A, accompagne depuis 20 ans les équipes de direction et les conseils d’administration dans l’élaboration et le déploiement de leurs stratégies d’affaires. Au fil des ans, elle a développé une solide expertise dans les domaines des stratégies de croissance, de la gouvernance et de la gestion des parties prenantes. Joanne Desjardins**, LL.B., MBA, ASC, CRHA, possède une solide expérience comme administratrice de sociétés ; elle rédige actuellement un livre sur la stratégie des entreprises. Elle blogue régulièrement sur la stratégie et la gouvernance.

Cette semaine, nous renouons avec notre habitude de collaboration avec des experts avisés en matière de gouvernance et d’éthique. Ainsi, à l’occasion du colloque du réseau d’éthique organisationnel du Québec (RÉOQ) intitulé « Vivre l’éthique au quotidien dans son organisation : entre le rêve et la réalité », j’ai demandé à René Villemure*, conférencier d’honneur du colloque, d’agir à titre d’auteur invité sur mon blogue, et de jeter un regard philosophique sur une réalité avec laquelle tout administrateur et tout gestionnaire est confronté : le courage.

En tant qu’administrateur de société, faire preuve de courage, c’est de poser les bonnes questions, en temps opportun, et en lien avec nos valeurs profondes.

Voici donc la réflexion que nous livre René Villemure à ce sujet. Vous pouvez visiter son site à www.ethique.net pour mieux connaître ses champs d’intérêt et consulter ses nombreux bulletins réflexifs.

Le courage c’est l’exception, c’est automatiquement la solitude ; quel vide autour du courage ! — Jean Giono

Tant dans la direction des entreprises que lors de conseils d’administration, on parle peu de courage, sinon que pour citer ce vague courage managérial qui, au fond, ne signifie, au mieux, que l’on fera les choix qui doivent être faits afin de faire son boulot comme attendu.

Si un mot est la construction d’un son et d’un sens, il semblerait que le courage ne soit devenu qu’un son sans le sens, c’est-à-dire que l’on reconnaît le mot lorsqu’on l’entend, lorsque certains l’évoquent, mais que, au fond, personne ne sait réellement ce en quoi il consiste.

On aura beau créer des formations universitaires en gouvernance, en administration des affaires ou en management, le courage n’est pas une valeur qui se codifie ou qui s’enseigne.

Le courage ne consiste pas à faire son travail tel qu’on l’attend de vous, ce qui n’est que compétence. Non, le courage est une qualité du cœur qui porte à réfléchir et à agir contre la facilité, avec sagesse, dans des circonstances difficiles. Le courage n’existe pas en théorie, il ne peut se démontrer que dans l’action.

Tout comme l’éthique, le courage exige un peu moins de soi et un peu plus des autres. La personne courageuse mettra de côté son intérêt personnel à court terme en vue de réaliser la raison d’être de l’entreprise.

Dans la conduite des affaires, combien de personnes, devant l’adversité, préféreront détourner le regard, se voiler les yeux, ou dire que cela ne me regarde pas ? Combien préféreront la facilité ? Combien diront que c’est imposé et que je n’ai pas le choix ?

Il importe de savoir que le courage ne signifie pas l’absence de peur ; la personne courageuse peut avoir peur dans des circonstances difficiles. Toutefois, la personne courageuse mesurera le danger, évaluera les actions qui peuvent être entreprises, surmontera sa peur et fera ce qui peut être fait dans les circonstances. Le courage se distingue de la témérité, qui n’est après tout que de foncer sans réfléchir. La témérité n’est qu’un excès de courage — sans-réflexion.

Comme dirigeants, comme administrateurs, vous avez toujours le choix. Vous avez d’ailleurs été nommés afin d’exercer ce choix. La question n’est donc pas de savoir si vous avez ou non le choix, mais, plutôt, si vous aurez le courage d’exercer ce choix. Pour le dire autrement : aurez-vous assez de cœur afin de faire ce qui doit être fait ?

Malheureusement, l’observation de la vie des organisations nous offre de [trop] nombreux exemples où plusieurs ont préféré le confort au courage. Confort, c’est un joli mot, mais en réalité, ce confort n’est que lâcheté qui n’ose dire son nom. Certes, lâcheté, c’est moins joli, mais c’est plus exact.

Lorsque l’on y pense un instant, sans courage, on devient sans-cœur.

Dans une société qui change rapidement, on a plus besoin de modèles et de héros que de mercenaires à la fidélité douteuse. C’est pourquoi, dans la conduite des affaires, il convient de réhabiliter le courage, de comprendre sa distinction d’avec la témérité et d’agir de manière juste.

Avec courage.

Avec cœur.

Si le courage mène à l’héroïsme, le manque de courage mène au cynisme.

*René Villemure est Éthicien et Chasseur de tendances. Il a fondé l’Institut québécois d’éthique appliquée en 1998 et Éthikos en 2003. Il a été le premier éthicien au Canada à s’intéresser à la gestion éthique des organisations à l’époque où personne ne connaissait les termes « gouvernance », « responsabilité sociétale des entreprises », « développement durable » et « gestion éthique ». Il croyait que ces sujets étaient cruciaux, fondamentaux, incontournables, et ne devaient pas demeurer dans l’ombre ou le privilège de quelques experts et éthiciens d’occasion.

Éthicien depuis 1998, son point de vue est recherché par les gouvernements et les dirigeants de grandes sociétés publiques et privées tant en Amérique qu’en Europe et en Afrique. Il a, à ce jour, prononcé plus de 675 conférences et formé plus de 65 000 personnes, autour du monde, dans plus de 700 organisations puis a participé à plus de 375 entrevues dans les médias francophones et anglophones. Ses interventions sur l’éthique touchent des domaines aussi variés que le monde de l’entreprise, la santé, l’éducation, l’industrie du luxe, l’agroalimentaire, les relations internationales que la culture ou encore l’intelligence artificielle.

Voici un article qui met en garde les structures de gouvernance telles que Facebook.

L’article publié sur le site de Directors&Boards par Eve Tahmincioglu soulève plusieurs questions fondamentales :

(1) L’actionnariat à vote multiple conduit-il à une structure de gouvernance convenable et acceptable ?

(2) Pourquoi le principe de gouvernance stipulant une action, un vote, est-il bafoué dans le cas de plusieurs entreprises de la Silicone Valley ?

(3) Quel est le véritable pouvoir d’un conseil d’administration où les fondateurs sont majoritaires par le jeu des actions à classe multiple ?

(4) Doit-on réglementer pour rétablir la position de suprématie du conseil d’administration dirigé par des administrateurs indépendants ?

(5) Dans une situation de gestion de crise comme celle qui confronte Facebook, quel est le rôle d’un administrateur indépendant, président de conseil ?

(6) Les médias cherchent à connaître la position du PDG sans se questionner sur les responsabilités des administrateurs. Est-ce normal en gestion de crise ?

Je vous invite à lire l’article ci-dessous et à exprimer vos idées sur les principes de bonne gouvernance appliqués aux entreprises publiques contrôlées par les fondateurs.

Facebook is arguably facing one of the toughest challenges the company has ever faced. But the slow and tepid response from leadership, including the boards of directors, concerns governance experts.

The scandal involving data-mining firm Cambridge Analytica allegedly led to 50 million Facebook users’ private information being compromised but a public accounting from Facebook’s CEO and chairman Mark Zuckerberg has been slow coming.

Could this be a governance breakdown?

“This high-powered board needs to engage more strongly,” says Steve Odland, CEO of the Committee for Economic Development and a board member for General Mills, Inc. and Analogic Corporation. Facebook’s board includes Netflix’s CEO Reed Hastings; Susan D. Desmond-Hellmann, CEO of The Gates Foundation; the former chairman of American Express Kenneth I. Chenault; and PayPal cofounder Peter A. Thiel, among others.

Odland points out that Facebook has two powerful and well-known executives, Zuckerberg and Facebook COO Sheryl Sandberg, who have been publicly out there on every subject, but largely absent on this one.

“They need to get out and publicly talk about this quickly,” Odland maintains. “They didn’t have to have all the answers. But this vacuum of communications gets filled by others, and that’s not good for the company.”

Indeed, politicians, the Federal Trade Commission and European politicians are stepping in, he says, “and that could threaten the whole platform.”

Typically, he adds, it comes back to management to engage and use the board, but “I don’t think Zuckerberg is all that experienced in that regard. This is where the board needs to help him.”

But how much power does the board have?

Charles Elson, director of the University of Delaware’s Weinberg Center for Corporate Governance, sees the dual-class ownership structure of Facebook that gives the majority of voting power to Zuckerberg and thus undermines shareholders and the board’s power.

“It’s his board because of the dual-class stock. There is nothing [directors] can do; neither can the shareholders and a lawsuit would yield really nothing,” he explains.

Increasingly, company founders have been opting to shore up control by creating stock ownership structures that undercut shareholder voting power, where only a decade ago almost all chose the standard and accepted one-share, one-vote model.

Now the Snap Inc. initial public offering (IPO) takes it even further with the first-ever solely non-voting stock model. It’s a stock ownership structure that further undercuts shareholder influence, undermines corporate governance and will likely shift the burden of investment grievances to the courts.

By offering stock in the company with no shareholder vote at all, Snap — the company behind the popular mobile-messaging app Snapchat that’s all about giving a voice to the many — has acknowledged that public voting power at companies with a hierarchy of stock ownership classes is only a fiction. And it begs the question: Why does Snap even need a board?

Alas, Facebook’s shares have tanked as a result of the Cambridge Analytica revelations, and it’s unclear what’s happening among the leaders at Facebook to deal with the crisis.

Facebook’s board, advises Odland, needs to get involved and help create privacy policies and if those are violated, they need to follow up.

“This is a relatively young company in a relatively young industry that has grown to be a powerhouse and incredibly important,” he explains. Given that, he says, there are “new forms of risk management this board needs to tackle.”

Nous avons demandé à Richard Thibault *, président de RTCOMM, d’agir à titre d’auteur invité. Son billet présente sept leçons tirées de son expérience comme consultant en gestion de crise.

En tant que membres de conseils d’administration, vous aurez certainement l’occasion de vivre des crises significatives et il est important de connaître les règles que la direction doit observer en pareilles circonstances.

Voici donc l’article en question, reproduit ici avec la permission de l’auteur. Vos commentaires sont appréciés. Bonne lecture.

Sept leçons apprises en matière de communications de crise

Par Richard Thibault*

La crise la mieux gérée est, dit-on, celle que l’on peut éviter. Mais il arrive que malgré tous nos efforts pour l’éviter, la crise frappe et souvent, très fort. Dans toute situation de crise, l’objectif premier est d’en sortir le plus rapidement possible, avec le moins de dommages possibles, sans compromettre le développement futur de l’organisation.

Voici sept leçons dont il faut s’inspirer en matière de communication de crise, sur laquelle on investit généralement 80% de nos efforts, et de notre budget, en de telles situations.

The Deepwater Horizon oil spill as seen from space by NASA’s Terra satellite on May 24, 2010 (Photo credit: Wikipedia)

(1) Le choix du porte-parole

Les médias voudront tout savoir. Mais il faudra aussi communiquer avec l’ensemble de nos clientèles internes et externes. Avoir un porte-parole crédible et bien formé est essentiel. On ne s’improvise pas porte-parole, on le devient. Surtout en situation de crise, alors que la tension est parfois extrême, l’organisation a besoin de quelqu’un de crédible et d’empathique à l’égard des victimes. Cette personne devra être en possession de tous ses moyens pour porter adéquatement son message et elle aura appris à éviter les pièges. Le choix de la plus haute autorité de l’organisation comme porte-parole en situation de crise n’est pas toujours une bonne idée. En crise, l’information dont vous disposez et sur laquelle vous baserez vos décisions sera changeante, contradictoire même, surtout au début. Risquer la crédibilité du chef de l’organisation dès le début de la crise peut être hasardeux. Comment le contredire ensuite sans nuire à son image et à la gestion de la crise elle-même ?

(2) S’excuser publiquement si l’on est en faute

S’excuser pour la crise que nous avons provoqué, tout au moins jusqu’à ce que notre responsabilité ait été officiellement dégagée, est une décision-clé de toute gestion de crise, surtout si notre responsabilité ne fait aucun doute. En de telles occasions, il ne faut pas tenter de défendre l’indéfendable. Ou pire, menacer nos adversaires de poursuites ou jouer les matamores avec les agences gouvernementales qui nous ont pris en défaut. On a pu constater les impacts négatifs de cette stratégie utilisée par la FTQ impliquée dans une histoire d’intimidation sur les chantiers de la Côte-Nord, à une certaine époque. Règle générale : mieux vaut s’excuser, être transparent et faire preuve de réserve et de retenue jusqu’à ce que la situation ait été clarifiée.

(3) Être proactif

Dans un conflit comme dans une gestion de crise, le premier à parler évite de se laisser définir par ses adversaires, établit l’agenda et définit l’angle du message. On vous conseillera peut-être de ne pas parler aux journalistes. Je prétends pour ma part que si, légalement, vous n’êtes pas obligés de parler aux médias, eux, en contrepartie, pourront légalement parler de vous et ne se priveront pas d’aller voir même vos opposants pour s’alimenter. En août 2008, la canadienne Maple Leaf, compagnie basée à Toronto, subissait la pire crise de son histoire suite au décès et à la maladie de plusieurs de ses clients. Lorsque le lien entre la listériose et Maple Leaf a été confirmé, cette dernière a été prompte à réagir autant dans ses communications et son attitude face aux médias que dans sa gestion de la crise. La compagnie a très rapidement retiré des tablettes des supermarchés les produits incriminés. Elle a lancé une opération majeure de nettoyage, qu’elle a d’ailleurs fait au grand jour, et elle a offert son support aux victimes. D’ailleurs, la gestion des victimes est généralement le point le plus sensible d’une gestion de crise réussie.

(4) Régler le problème et dire comment

Dès les débuts de la crise, Maple Leaf s’est mise immédiatement au service de l’Agence canadienne d’inspection des aliments, offrant sa collaboration active et entière pour déterminer la cause du problème. Dans le même secteur alimentaire, tout le contraire de ce qu’XL Foods a fait quelques années plus tard. Chez Maple Leaf, tout de suite, des experts reconnus ont été affectés à la recherche de solutions. On pouvait reprocher à la compagnie d’être à la source du problème, mais certainement pas de se trainer les pieds en voulant le régler. Encore une fois, en situation de crise, camoufler sa faute ou refuser de voir publiquement la réalité en face est décidément une stratégie à reléguer aux oubliettes. Plusieurs années auparavant, Tylenol avait montré la voie en retirant rapidement ses médicaments des tablettes et en faisant la promotion d’une nouvelle méthode d’emballage qui est devenue une méthode de référence aujourd’hui.

(5) Employer le bon message

Il est essentiel d’utiliser le bon message, au bon moment, avec le bon messager, diffusé par le bon moyen. Les premiers messages surtout sont importants. Ils serviront à exprimer notre empathie, à confirmer les faits et les actions entreprises, à expliquer le processus d’intervention, à affirmer notre désir d’agir et à dire où se procurer de plus amples informations. Si la gestion des médias est névralgique, la gestion de l’information l’est tout autant. En situation de crise, on a souvent tendance à s’asseoir sur l’information et à ne la partager qu’à des cercles restreints, ou, au contraire, à inonder nos publics d’informations inutiles. Un juste milieu doit être trouvé entre ces deux stratégies sachant pertinemment que le message devra évoluer en même temps que la crise.

(6) Être conséquent et consistant

Même s’il évolue en fonction du stade de la crise, le message de base doit pourtant demeurer le même. Dans l’exemple de Maple Leaf évoqué plus haut, bien que de nouveaux éléments aient surgi au fur et à mesure de l’évolution de la crise, le message de base, à savoir la mise en œuvre de mesures visant à assurer la santé et la sécurité du public, a été constamment repris sur tous les tons. Ainsi, Maple Leaf s’est montrée à la fois consistante en respectant sa ligne de réaction initiale et conséquente, en restant en phase avec le développement de la situation.

(7) Être ouvert d’esprit

Dans toute situation de crise, une attitude d’ouverture s’avérera gagnante. Que ce soit avec les médias, les victimes, nos employés, nos partenaires ou les agences publiques de contrôle, un esprit obtus ne fera qu’envenimer la situation. D’autant plus qu’en situation de crise, ce n’est pas vraiment ce qui est arrivé qui compte mais bien ce que les gens pensent qui est arrivé. Il faut donc suivre l’actualité afin de pouvoir anticiper l’angle que choisiront les médias et s’y préparer en conséquence.

En conclusion

Dans une perspective de gestion de crise, il est essentiel de disposer d’un plan d’action au préalable, même s’il faut l’appliquer avec souplesse pour répondre à l’évolution de la situation. Lorsque la crise a éclaté, c’est le pire moment pour commencer à s’organiser. Il est essentiel d’établir une culture de gestion des risques et de gestion de crise dans l’organisation avant que la crise ne frappe. Comme le dit le vieux sage, » pour être prêt, faut se préparer ! »

* Richard Thibault, ABCP

Président de RTCOMM, une entreprise spécialisée en positionnement stratégique et en gestion de crise

Menant de front des études de Droit à l’Université Laval de Québec, une carrière au théâtre, à la radio et à la télévision, Richard Thibault s’est très tôt orienté vers le secteur des communications, duquel il a développé une expertise solide et diversifiée. Après avoir été animateur, journaliste et recherchiste à la télévision et à la radio de la région de Québec pendant près de cinq ans, il a occupé le poste d’animateur des débats et de responsable des affaires publiques de l’Assemblée nationale de 1979 à 1987.

Richard Thibault a ensuite tour à tour assumé les fonctions de directeur de cabinet et d’attaché de presse de plusieurs ministres du cabinet de Robert Bourassa, de conseiller spécial et directeur des communications à la Commission de la santé et de la sécurité au travail et de directeur des communications chez Les Nordiques de Québec.

En 1994, il fonda Richard Thibault Communications inc. (RTCOMM). D’abord spécialisée en positionnement stratégique et en communication de crise, l’entreprise a peu à peu élargi son expertise pour y inclure tous les champs de pratique de la continuité des affaires. D’autre part, reconnaissant l’importance de porte-parole qualifiés en période trouble, RTCOMM dispose également d’une école de formation à la parole en public. Son programme de formation aux relations avec les médias est d’ailleurs le seul programme de cette nature reconnu par le ministère de la Sécurité publique du Québec, dans un contexte de communication d’urgence. Ce programme de formation est aussi accrédité par le Barreau du Québec.

Richard Thibault est l’auteur de Devenez champion dans vos communications et de Osez parler en public, publié aux Éditions MultiMondes et de Comment gérer la prochaine crise, édité chez Transcontinental, dans la Collection Entreprendre. Praticien reconnu de la gestion des risques et de crise, il est accrédité par la Disaster Recovery Institute International (DRII).

Spécialités : Expert en positionnement stratégique, gestion des risques, communications de crise, continuité des affaires, formation à la parole en public.

Aujourd’hui, je vous présente un formidable guide, publié par McCarthyTetrault, sur les risques associés aux questions de la cybersécurité dans les entreprises.

Vous y trouverez une information complète ainsi que divers outils de diagnostic essentiels aux conseils d’administration qui doivent se préparer à affronter des attaques de nature cybernétique, lesquelles sont de plus en plus fréquentes.

Cet excellent document a été porté à mon attention par Joanne Desjardins, LL.B., MBA, CRHA, ASC, associée de la firme Arsenal conseils, spécialisés en gouvernance et en stratégie.

L’ouvrage est divisé en quatre parties :