Aujourd’hui, je porte à votre attention une excellente publication de Jim Rossman*, directeur du conseil aux actionnaires, Kathryn Hembree Night, directrice, et Quinn Pitcher, analyste de la firme Lazard, qui présente une revue complète des actionnaires activistes.

Cette étude fait état de l’évolution des activistes en 2019, elle dégage les principales observations des auteurs :

-

- L’activité militante reprend sa tendance pluriannuelle après un record en 2018 ;

- La progression constante de l’activisme en dehors des États-Unis ;

- Le nombre record de campagnes liées aux fusions et acquisitions ;

- L’influence des activistes sur les conseils d’administration se poursuit,

- Les pressions sur les gestionnaires actifs s’intensifient.

- Autres observations importantes, dont les suivantes :

-

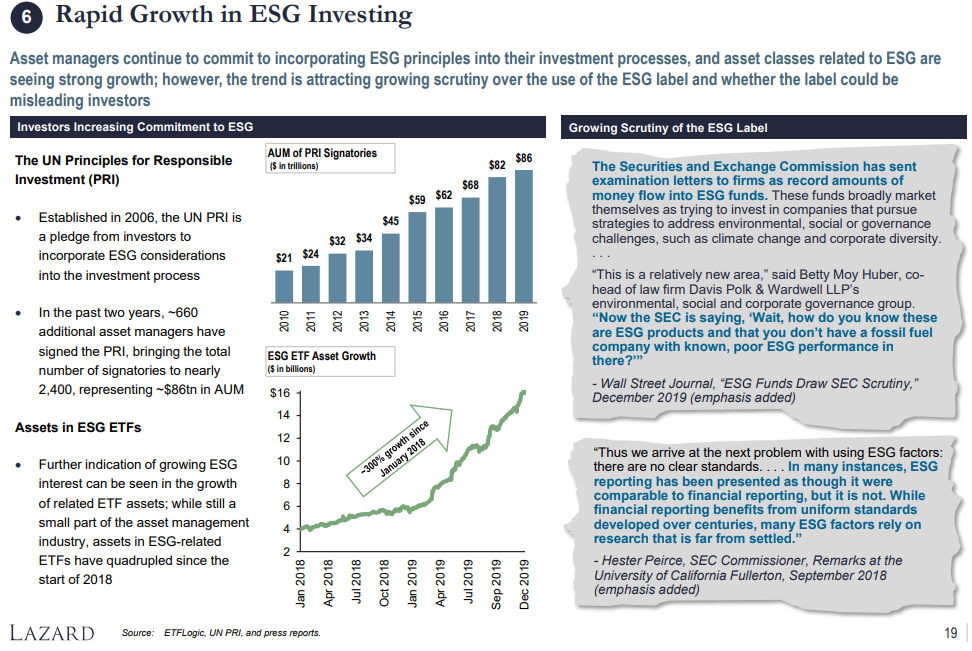

- L’accent ESG continue de croître : au cours des deux dernières années, l’actif géré représenté par les signataires des Principes pour l’investissement responsable des Nations Unies a augmenté de 26 % à 86 milliards de dollars, et le nombre d’actifs dans les FNB liés à l’ESG a augmenté de 300 %.

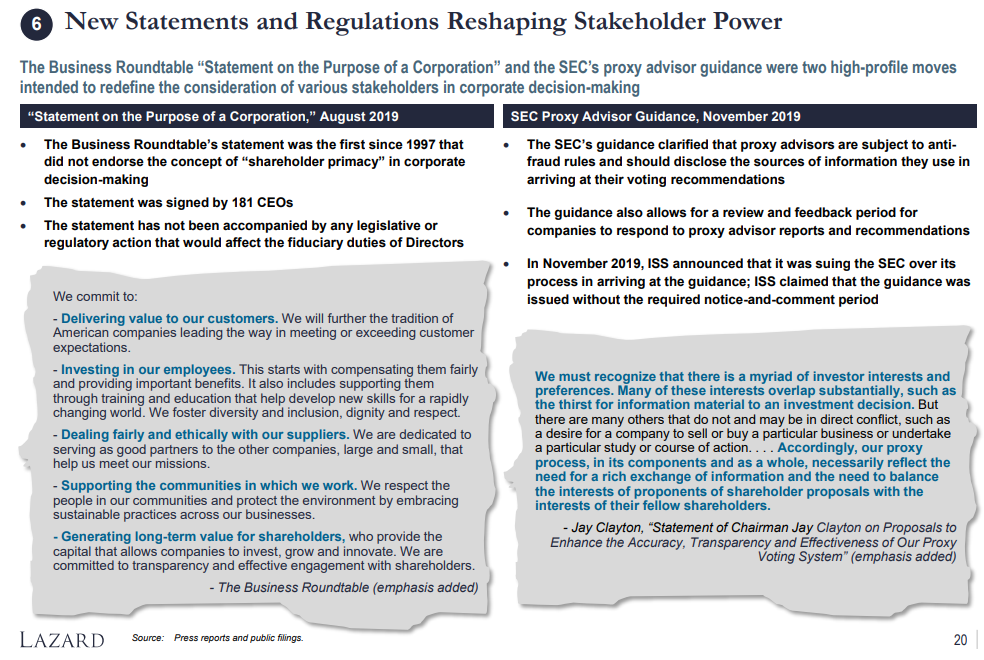

- La « Déclaration sur l’objet de la société » de la table ronde des entreprises a souligné l’importance pour les entreprises d’intégrer les intérêts de toutes les parties prenantes, et pas seulement des actionnaires, dans leurs processus décisionnels.

- Les directives de la SEC sur les conseillers en vote ont cherché à accroître les normes de responsabilité et de surveillance dans les évaluations de leur entreprise.

La publication utilise une infographie très efficace pour illustrer les effets de l’activisme aux États-Unis, mais aussi à l’échelle internationale.

Bonne lecture !

Key Observations on the Activist Environment in 2019

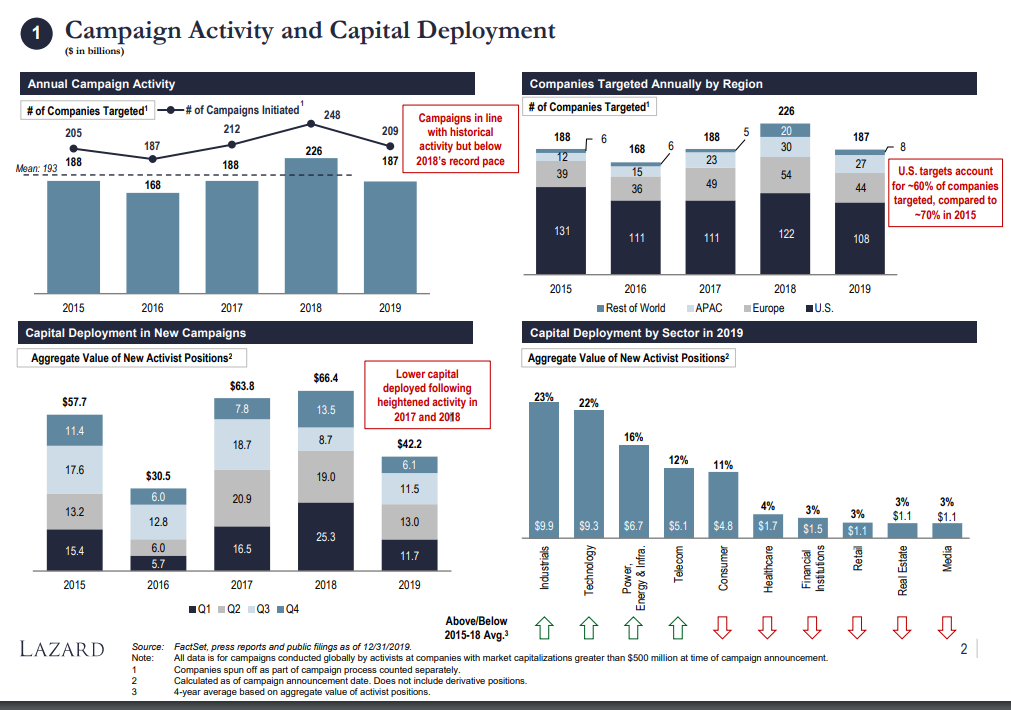

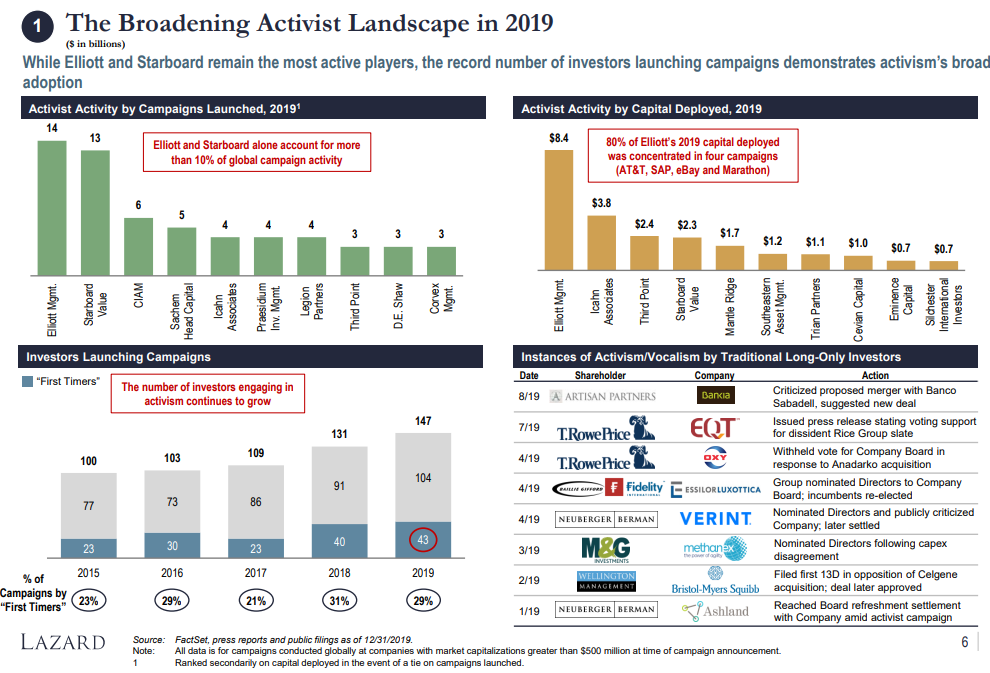

1. Activist Activity Returns to Multi-Year Trend After Record 2018

187 companies targeted by activists, down 17% from 2018’s record but in line with multi-year average levels

Aggregate capital deployed by activists (~$42bn) reflected a similar dip relative to the ~$60bn+ level of 2017/2018

A record 147 investors launched new campaigns in 2019, including 43 “first timers” with no prior activism history

Elliott and Starboard remained the leading activists, accounting for more than 10% of global campaign activity

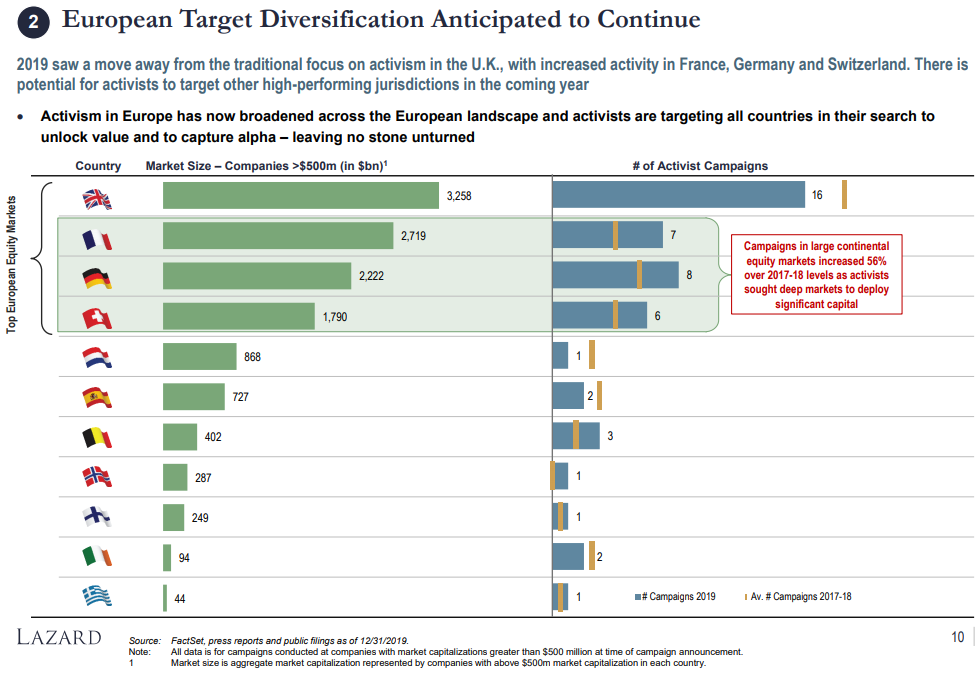

2. Activism’s Continued Influence Outside the U.S.

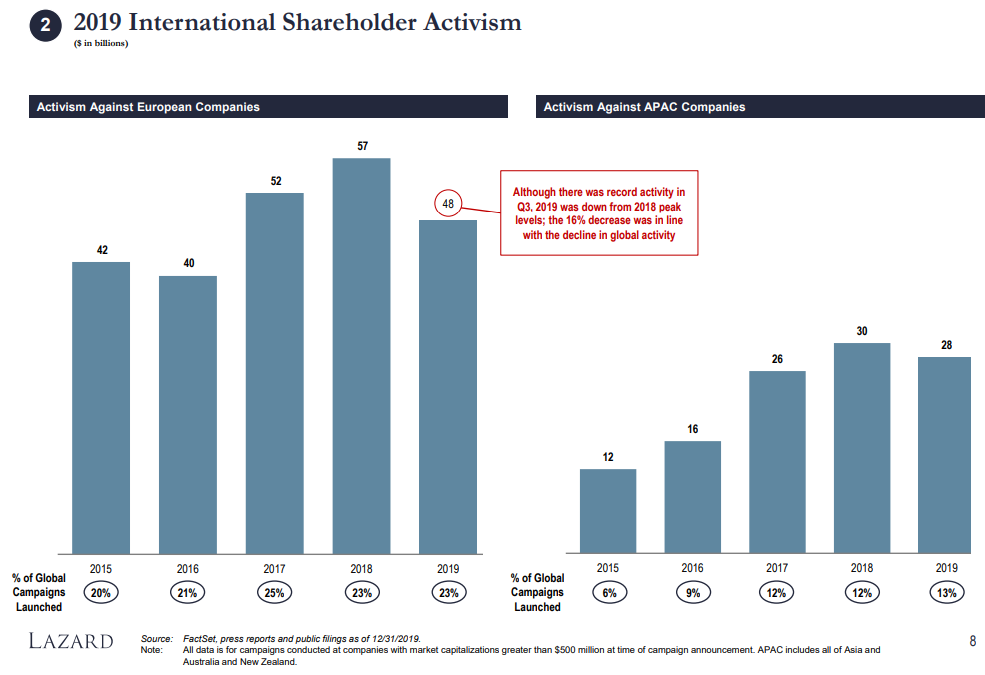

Activism against non-U.S. targets accounted for ~40% of 2019 activity, up from ~30% in 2015

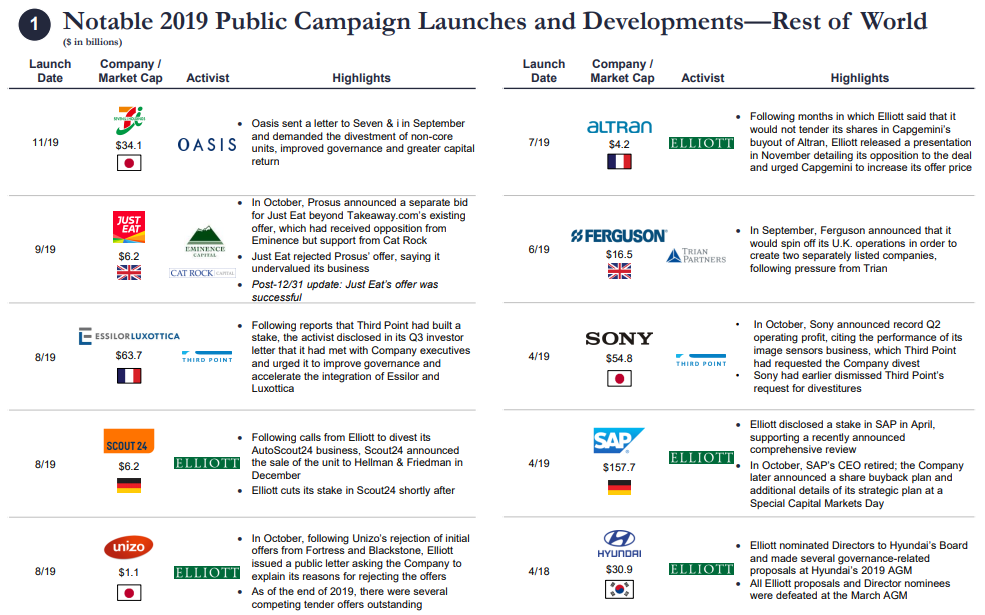

Multi-year shift driven both by a decline in S. targets and an uptick in activity in Japan and Europe

For the first time, Japan was the most-targeted non-U.S. jurisdiction, with 19 campaigns and $4.5bn in capital deployed in 2019 (both local records)

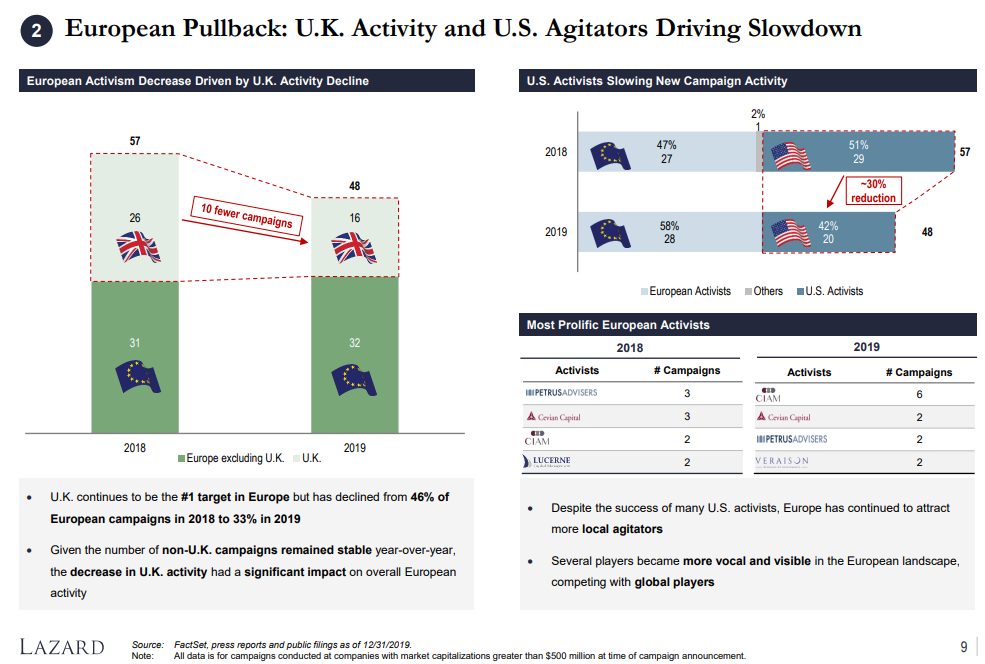

Overall European activity decreased in 2019 (48 campaigns, down from a record 57 in 2018), driven primarily by 10 fewer campaigns in the K.

Expanded activity in continental Europe—particularly France, Germany and Switzerland—partially offset this decline

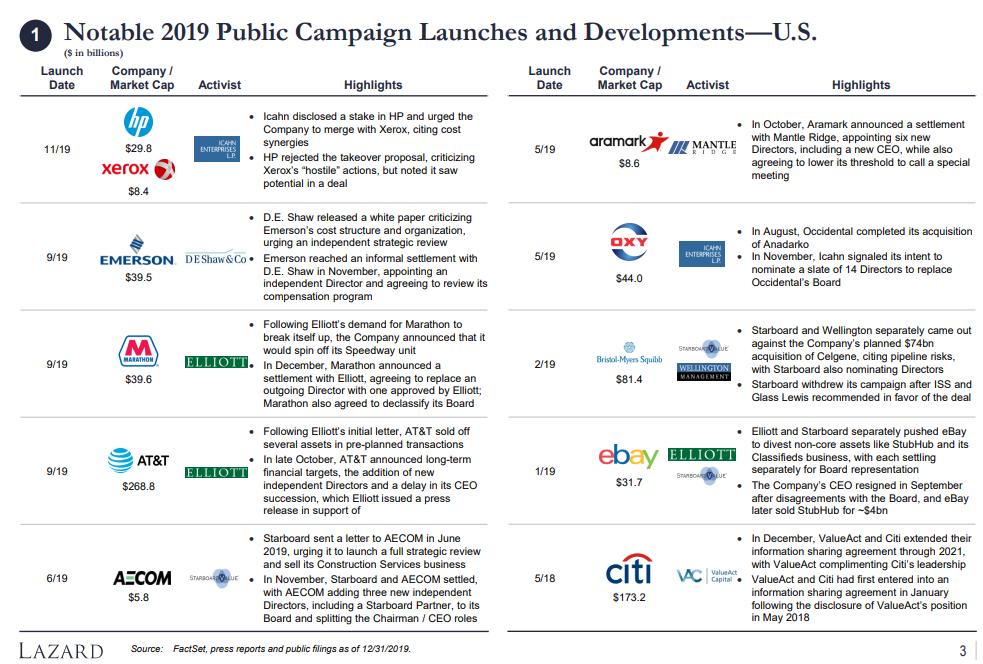

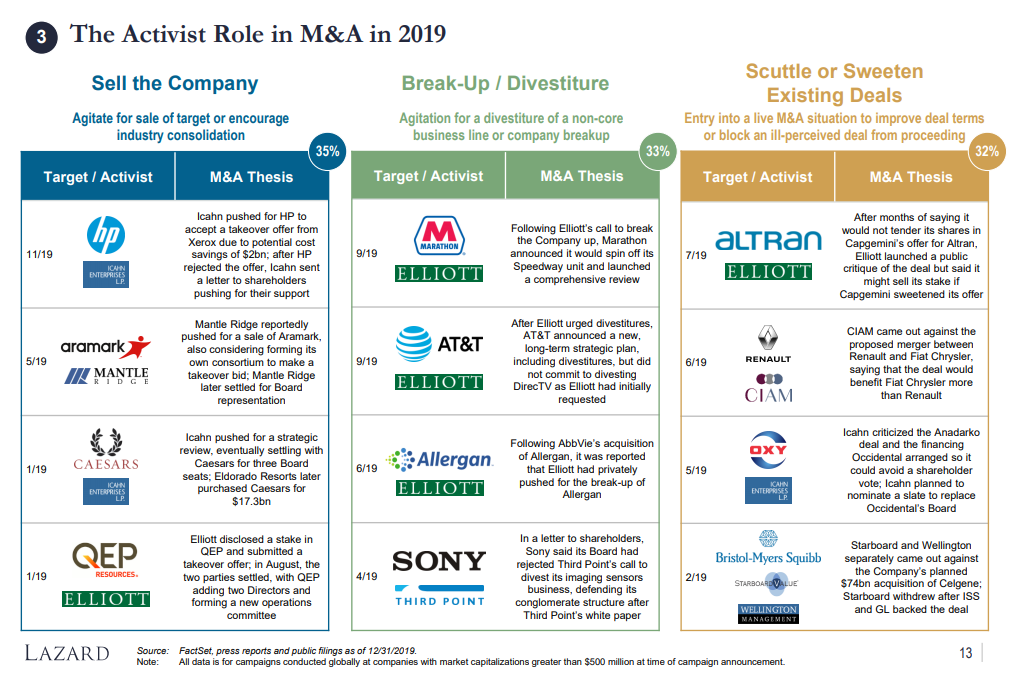

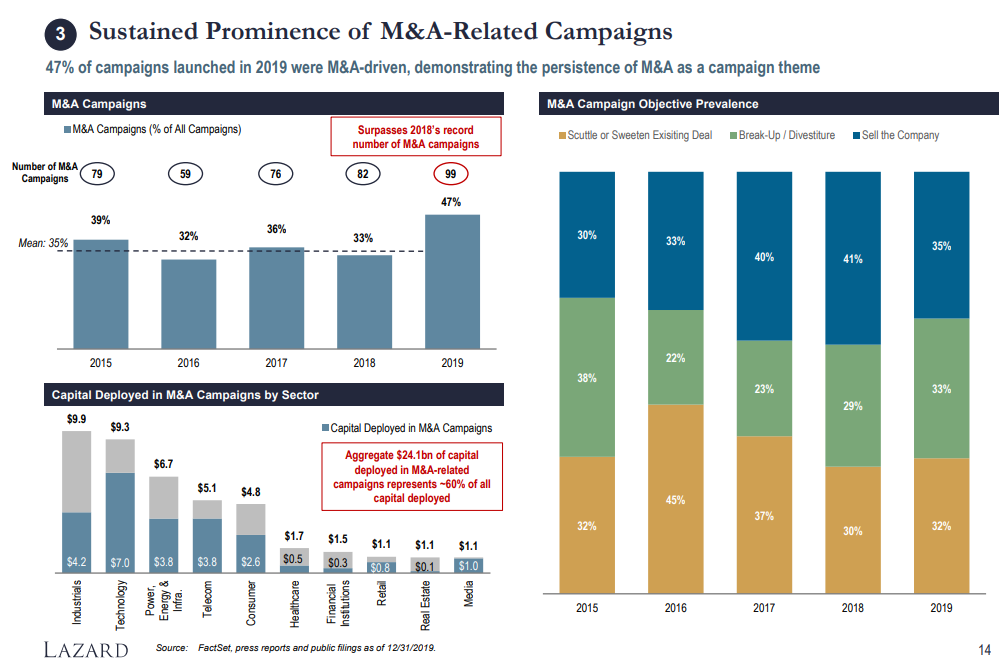

3. Record Number of M&A-Related Campaigns

A record 99 campaigns with an M&A-related thesis (accounting for ~47% of all 2019 activity, up from ~35% in prior years) were launched in 2019

As in prior years, there were numerous prominent examples of activists pushing a sale (HP, Caesars) or break-up (Marathon, Sony) or opposing an announced transaction (Occidental, Bristol-Myers Squibb)

The $24.1bn of capital deployed in M&A-related campaigns in 2019 represented ~60% of total capital deployed

The technology sector alone saw $7.0bn put to use in M&A related campaigns

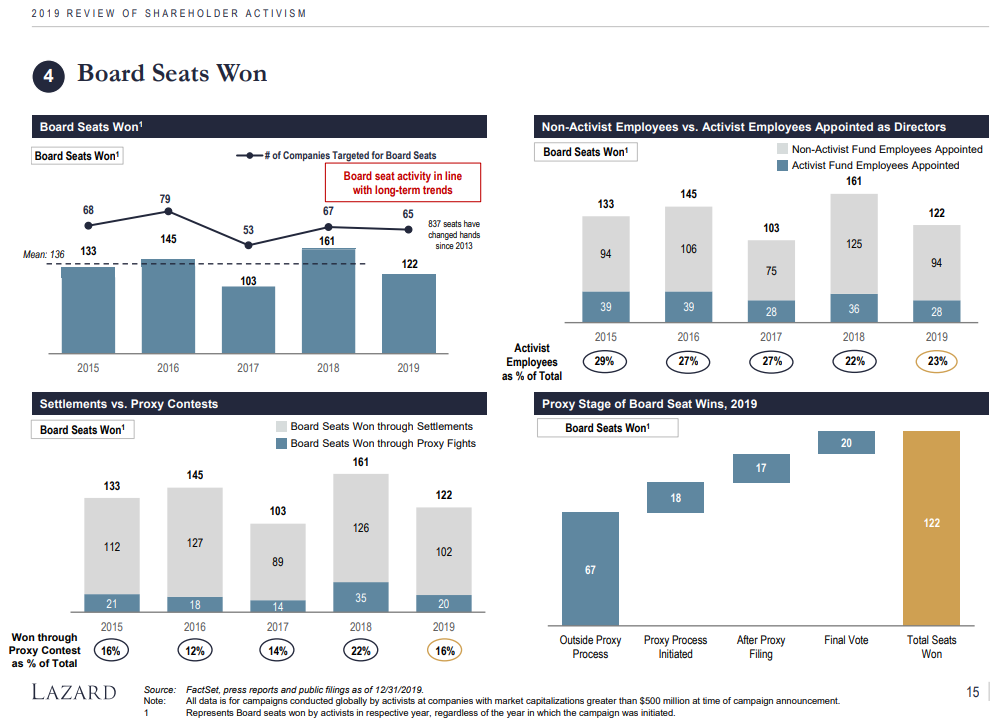

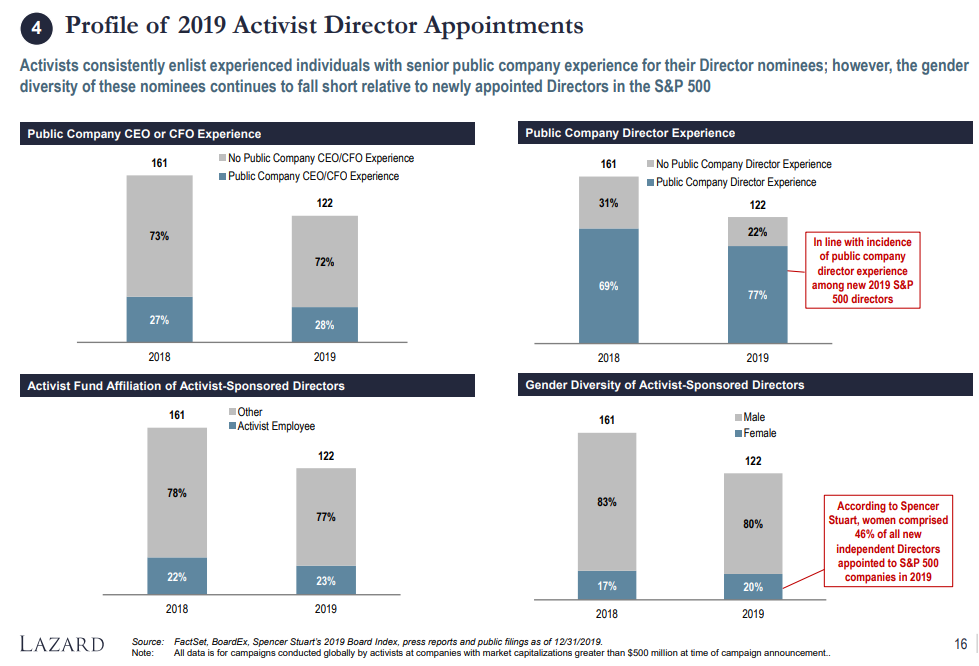

4. Activist Influence on Boards Continues

122 Board seats were won by activists in 2019, in line with the multi-year average

Consistent with recent trends, the majority of Board seats were secured via negotiated settlements (~85% of Board seats)

20% of activist Board seats went to female directors, compared to a rate of 46% for all new S&P 500 director appointees

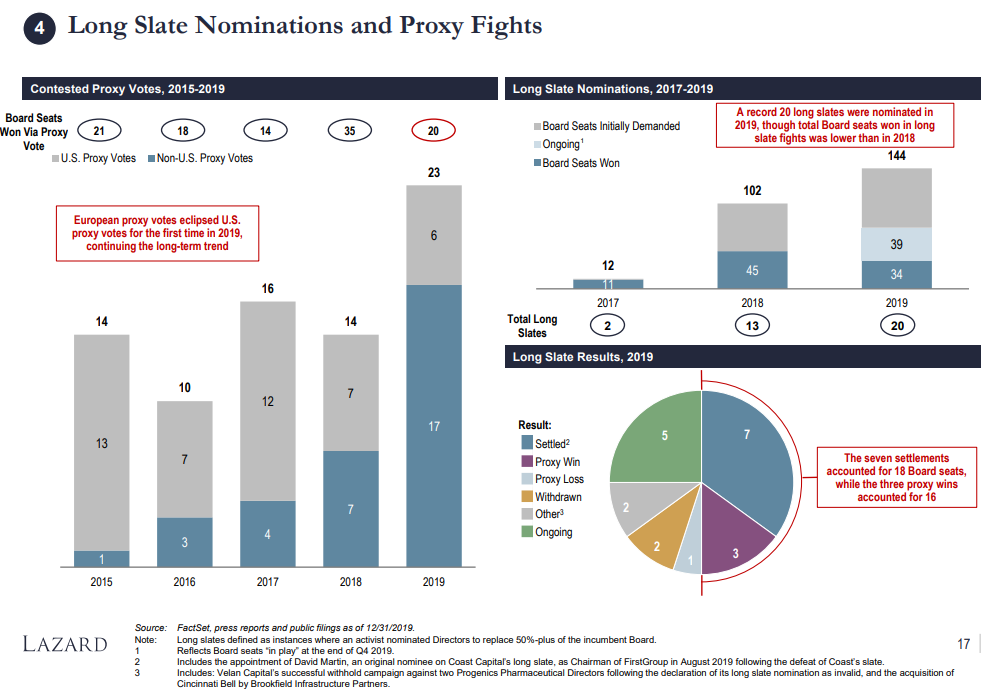

Activists nominated a record 20 “long slates” seeking to replace a majority of directors in 2019, securing seats in two-thirds (67%) of the situations that have been resolved

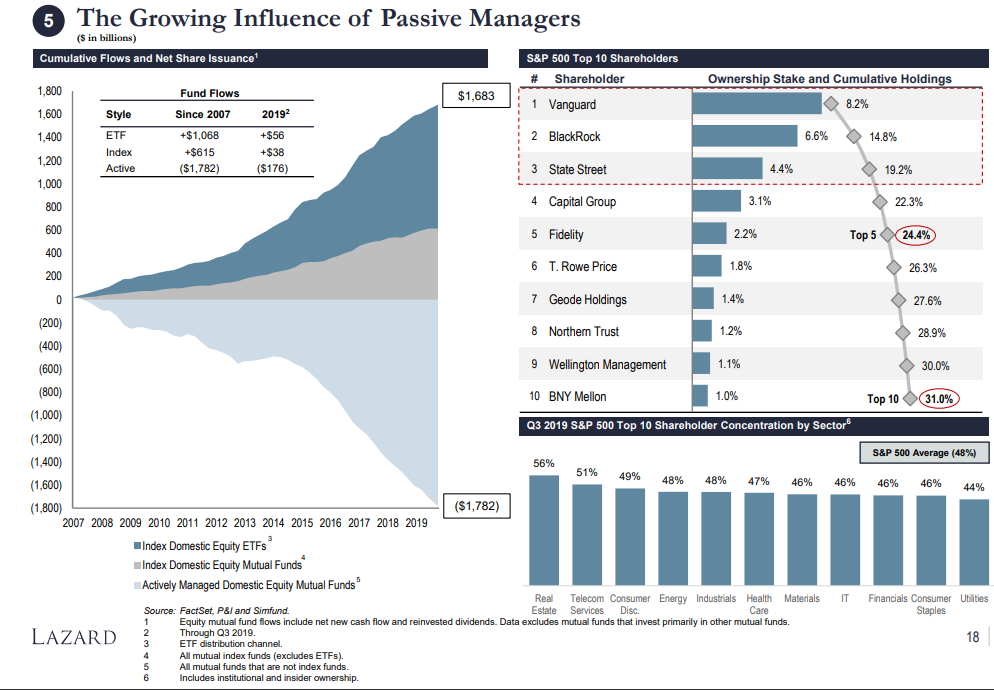

5. Outflow Pressure on Active Managers Intensifies

Actively managed funds saw ~$176bn in net outflows through Q3 2019, compared to ~$105bn in 2018 over the same period

The “Big 3” index funds (BlackRock, Vanguard and State Street) continue to be the primary beneficiaries of passive inflows, collectively owning ~19% of the S&P 500—up from ~16% in 2014

6. Other Noteworthy Observations

ESG focus continues to grow: over the past two years, the AUM represented by signatories to the UN’s Principles for Responsible Investment increased ~26% to ~$86tn, and the number of assets in ESG-related ETFs increased ~300%

The Business Roundtable’s “Statement on the Purpose of the Corporation” emphasized the importance of companies incorporating the interests of all stakeholders, not just shareholders, into their decision-making processes

The SEC’s guidance on proxy advisors sought to increase accountability and oversight standards in their company evaluations

Source: FactSet, ETFLogic, UN PRI, Simfund, press reports and public filings as of 12/31/2019.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

The complete publication, including Appendix, is available here.

Endnotes

1Represents Board seats won by activists in the respective year, regardless of the year in which the campaign was initiated. (go back)

2According to Spencer Stuart’s 2019 Board Index.(go back)

Jim Rossman* est directeur du conseil aux actionnaires, Kathryn Hembree Night est directrice et Quinn Pitcher est analyste chez Lazard. Cet article est basé sur une publication Lazard. La recherche connexe du programme sur la gouvernance d’entreprise comprend les effets à long terme de l’activisme des fonds spéculatifs par Lucian Bebchuk, Alon Brav et Wei Jiang (discuté sur le forum ici ); Danse avec des militants par Lucian Bebchuk, Alon Brav, Wei Jiang et Thomas Keusch (discuté sur le forum ici ); et qui saigne quand les loups mordent? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System par Leo E. Strine, Jr.