On parle beaucoup des changements sociétaux que les avancées de l’IA sont susceptibles de produire à l’échelle planétaire. Je souhaitais avoir un exemple concret de l’utilité de l’IA dans un domaine plus spécifique.

Ainsi, j’ai interrogé une application d’intelligence artificielle générative (AI Chatbot) sur l’impact que l’IA pourrait avoir sur le management et la gouvernance des organisations.

L’intelligence artificielle (IA) a un impact significatif sur le management et la gouvernance des sociétés. Voici quelques-uns des principaux aspects de cet impact :

1. Prise de décision : L’IA peut aider les gestionnaires à prendre des décisions plus éclairées en analysant de grandes quantités de données et en identifiant des tendances et des modèles qui échapperaient à l’œil humain. Cela peut conduire à des décisions plus rapides et plus précises, ce qui peut améliorer la performance globale de l’entreprise.

2. Automatisation des tâches : L’IA peut automatiser de nombreuses tâches routinières et répétitives, libérant ainsi du temps pour les gestionnaires pour se concentrer sur des tâches plus stratégiques et à forte valeur ajoutée. Cela peut également réduire les coûts opérationnels et améliorer l’efficacité de l’entreprise.

3. Gestion des talents : L’IA peut aider les gestionnaires à identifier les talents les plus prometteurs au sein de l’entreprise, en analysant leurs performances passées et en prédisant leur potentiel futur. Cela peut permettre de mieux attribuer les ressources et de développer les compétences nécessaires pour faire progresser l’entreprise.

4. Personnalisation et adaptation : L’IA permet de personnaliser les interactions avec les employés et les clients en fonction de leurs préférences et de leurs comportements, ce qui peut améliorer l’engagement et la satisfaction.

5. Redéfinition des rôles et des compétences : L’introduction de l’IA peut nécessiter une adaptation des rôles et des compétences des managers, qui devront être capables de travailler en collaboration avec des systèmes intelligents et de comprendre leur fonctionnement.

6. Gouvernance d’entreprise : L’IA peut aider les conseils d’administration à prendre des décisions plus éclairées en fournissant des analyses et des insights basés sur des données. Cela peut améliorer la transparence et la responsabilité des entreprises, tout en aidant à identifier les risques et les opportunités potentielles.

En conclusion, l’IA a un impact profond sur le management et la gouvernance des sociétés en permettant une prise de décision plus éclairée, une automatisation des tâches, une meilleure gestion des talents et une gouvernance d’entreprise plus efficace. Il est crucial pour les entreprises de comprendre et d’exploiter pleinement le potentiel de l’IA pour rester compétitives dans un environnement en constante évolution.

À la lumière des réponses fournies par l’application, on peut se faire une assez bonne idée des facteurs de changements les plus importants. Il y a, bien sûr, d’autres facteurs à considérer pour évaluer l’impact de l’IA dans le monde des organisations, mais le système nous présente une bonne base de départ.

Aujourd’hui, je partage avec vous le compte rendu d’une recherche portant sur les relations entre les accès des entreprises aux décideurs politiques américains et l’augmentation de la valeur des firmes en termes d’avantages compétitifs.

L’article montre clairement toute l’importance de l’influence politique sur la valeur des organisations. Peu de recherches scientifiques à ce jour s’étaient penchées sur ce phénomène !

Cet article remarquable a été publié par Jeffrey R. Brown, professeur et doyen du College of Business, Jiekun Huang, professeur agrégé de finance et Vernon Zimmerman professeur à l’Université de l’Illinois

Je vous invite à lire la version française de la publication, en utilisant l’outil de traduction de Google, lequel est certainement perfectible.

L’accès aux décideurs politiques est une ressource rare, car les politiciens et leurs collaborateurs ont un temps limité et ne peuvent interagir qu’avec un nombre limité de personnes. Obtenir un accès politique peut être d’une grande valeur pour les entreprises, en particulier parce que les gouvernements jouent un rôle de plus en plus important pour influencer les entreprises.

Les gouvernements affectent les activités économiques non seulement par le biais de réglementations, mais aussi en jouant le rôle de clients, de financiers et de partenaires des entreprises du secteur privé. Il existe de nombreuses preuves anecdotiques suggérant que les entreprises bénéficient de l’accès à des politiciens puissants. Par exemple, un article du Wall Street Journal (2015) affirme que les visites fréquentes des dirigeants de Google à la Maison-Blanche ont joué un rôle déterminant dans la décision de la Federal Trade Commission d’abandonner son enquête antitrust sur l’entreprise.

Obtenir et conserver l’accès à des décideurs politiques influents peut être une source importante d’avantage concurrentiel pour les entreprises. Pourtant, malgré l’importance de l’accès politique pour les entreprises, la répartition de l’accès politique entre les entreprises et ses effets sur la valeur de l’entreprise restent sous-explorés.

Dans notre article All the President’s Friends: Political Access and Firm Value, publié dans le Journal of Financial Economics, nous étudions les caractéristiques des entreprises ayant un accès politique ainsi que les effets de valorisation de l’accès politique pour les entreprises. À l’aide d’un ensemble de données des journaux des visiteurs de la Maison-Blanche, nous identifions les principaux dirigeants d’entreprises du S&P 1500 qui ont des réunions en face à face avec des représentants de haut niveau du gouvernement fédéral.

Nous examinons deux questions fondamentales liées à l’accès politique. Premièrement, dans quelle mesure l’accès politique est-il répandu — sous la forme littérale de réunions avec des décideurs politiques influents — et quelles sont les caractéristiques des entreprises ayant accès aux politiciens ? Deuxièmement, l’accès politique augmente-t-il la valeur de l’entreprise et, dans l’affirmative, par quels canaux ?

Nous identifions 2 401 réunions entre les dirigeants d’entreprises du S&P1500 et des représentants du gouvernement fédéral à la Maison-Blanche entre 2009 et 2015. Nos résultats peuvent être résumés comme suit. Premièrement, en termes de prévalence et de caractéristiques des entreprises ayant un accès politique, nous constatons qu’environ 11 % des années-entreprises ont des cadres qui visitent la Maison-Blanche. Étant donné que les entreprises ayant un accès politique ont tendance à être plus grandes, ces années-entreprises représentent environ 40 % de la capitalisation boursière totale de toutes les années-entreprises de l’échantillon.

Conformément à la notion selon laquelle les contributions électorales « achètent » l’accès, nous constatons que les entreprises qui ont davantage contribué aux campagnes électorales présidentielles d’Obama sont plus susceptibles d’avoir accès à la Maison-Blanche. Nous constatons également que les entreprises qui dépensent plus en lobbying, les entreprises qui reçoivent plus de contrats gouvernementaux et les grandes entreprises cotées sont plus susceptibles d’avoir accès aux décideurs influents.

Deuxièmement, nous constatons que les réunions des dirigeants d’entreprise avec les responsables de la Maison-Blanche sont suivies de rendements anormaux cumulatifs (RAC) positifs significatifs. Par exemple, le RAC est d’environ 0,38 % pendant une fenêtre de 12 jours entourant les réunions. Nous constatons que ce résultat est principalement motivé par des entreprises étroitement liées, définies comme celles qui ont davantage contribué à la campagne présidentielle d’Obama que celle de son adversaire. Par exemple, les visites de dirigeants d’entreprises proches sont associées à un RAC sur 12 jours de 0,51 %, contre 0,27 % pour celles des dirigeants d’entreprises non fermées. De plus, nous trouvons des RAC positifs significatifs autour de la publication des journaux des visiteurs, en particulier pour les visites qui n’étaient pas couvertes par les médias avant la publication des journaux.

Troisièmement, pour examiner plus en détail les effets de valorisation associés à l’accès politique, nous observons que l’élection de Donald J. Trump a représenté un choc pour l’accès politique. Nous constatons que les entreprises ayant accès à l’administration Obama enregistrent des rendements boursiers significativement plus faibles après la publication du résultat des élections que les entreprises similaires.

L’ampleur économique est également non triviale : après avoir contrôlé divers facteurs qui sont probablement corrélés aux activités politiques des entreprises, tels les contributions électorales, les dépenses de lobbying et les contrats gouvernementaux, les actions des entreprises ayant accès à l’administration Obama sous-performent les actions d’entreprises similaires d’environ 0,70 % dans les trois jours suivants immédiatement l’élection. Ce résultat corrobore notre principale constatation selon laquelle l’accès politique est d’une grande valeur pour les entreprises. Nous constatons également que la RAC négative autour de l’élection présidentielle de 2016 pour les entreprises ayant accès à la Maison-Blanche d’Obama est principalement motivée par des entreprises proches, ce qui suggère que l’accès politique permet aux entreprises qui soutiennent le président de récolter des avantages significatifs.

Enfin, nous identifions deux canaux par lesquels l’accès politique augmente la valeur de l’entreprise. En utilisant un score de propension apparié à un échantillon d’entreprises ayant un accès politique (groupe de traitement) et celles sans accès politique (groupe de contrôle) et une approche de différence dans les écarts, nous constatons que les groupes de traitement, par rapport aux groupes de contrôle, reçoivent plus de contrats gouvernementaux après les réunions qu’avant les réunions. Nous trouvons également des preuves suggérant que les groupes de traitement, par rapport aux groupes de contrôle, obtiennent des mesures réglementaires plus favorables après les réunions qu’avant les réunions.

La principale contribution de notre article à la littérature est double. Premièrement, nous sommes les premiers à utiliser les données sur les visiteurs de la Maison-Blanche pour identifier les interactions physiques entre les dirigeants d’entreprise et les politiciens influents. Les informations détaillées contenues dans les données du journal des visiteurs nous permettent de fournir une mesure directe de l’accès politique et de fournir des preuves sur les effets d’attribution et d’évaluation de l’accès politique. Les données permettent également d’identifier le moment exact de l’accès des dirigeants d’entreprise à des politiciens puissants, nous permettant ainsi de mesurer les effets de valorisation à l’aide d’une approche d’étude des événements.

Deuxièmement, notre étude renforce la compréhension de la valeur des liens politiques avec les responsables de l’exécutif aux États-Unis. Parce que les entreprises sont souvent directement affectées par les décisions prises par les agences exécutives (par exemple, l’attribution des marchés publics et des décisions d’application de la réglementation), il est important de comprendre la valeur des liens avec les politiciens de l’exécutif et les canaux par lesquels un tel effet d’évaluation se produit. Les données de notre article suggèrent que l’accès aux hauts fonctionnaires de l’exécutif peut être une source importante d’avantage concurrentiel pour les entreprises. Nos résultats mettent également en lumière deux canaux, à savoir les marchés publics et les allègements réglementaires, par lesquels l’accès politique affecte la valeur de l’entreprise.

L’article complet est disponible en téléchargement ici.

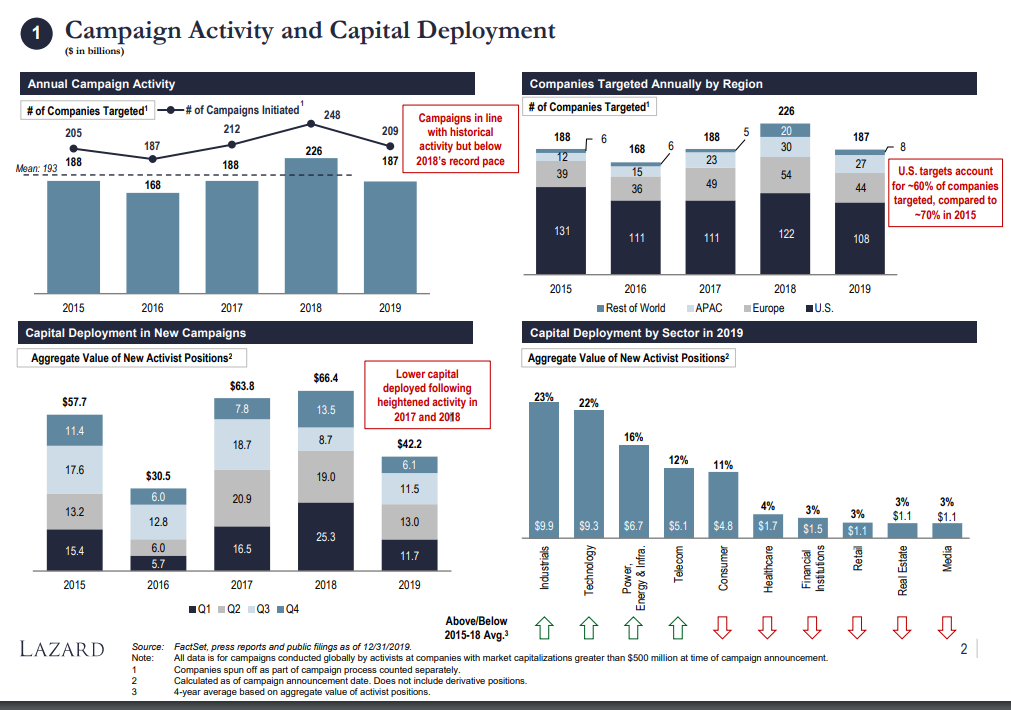

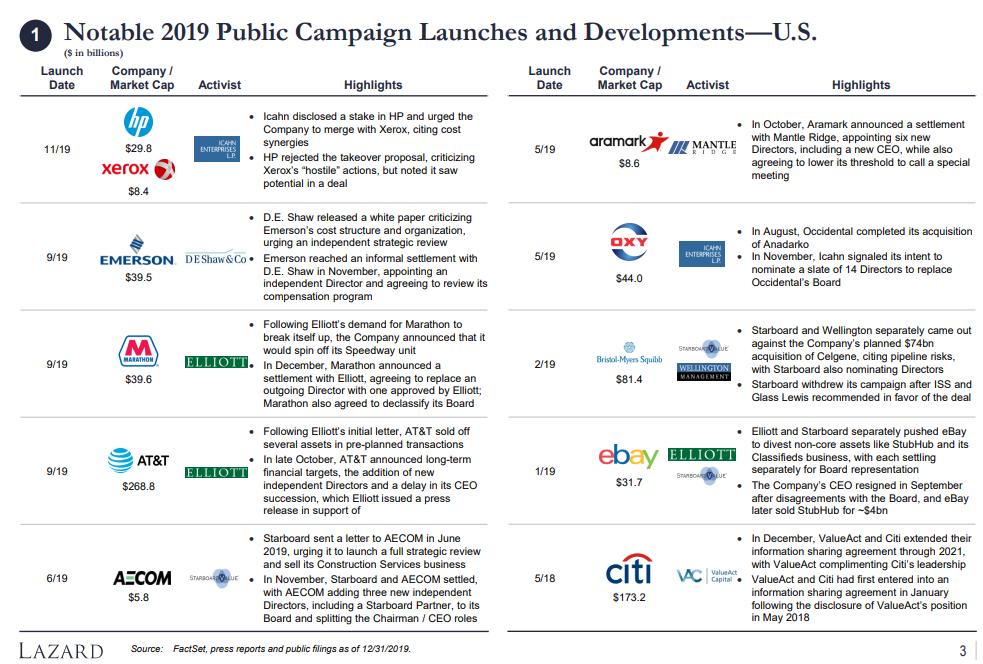

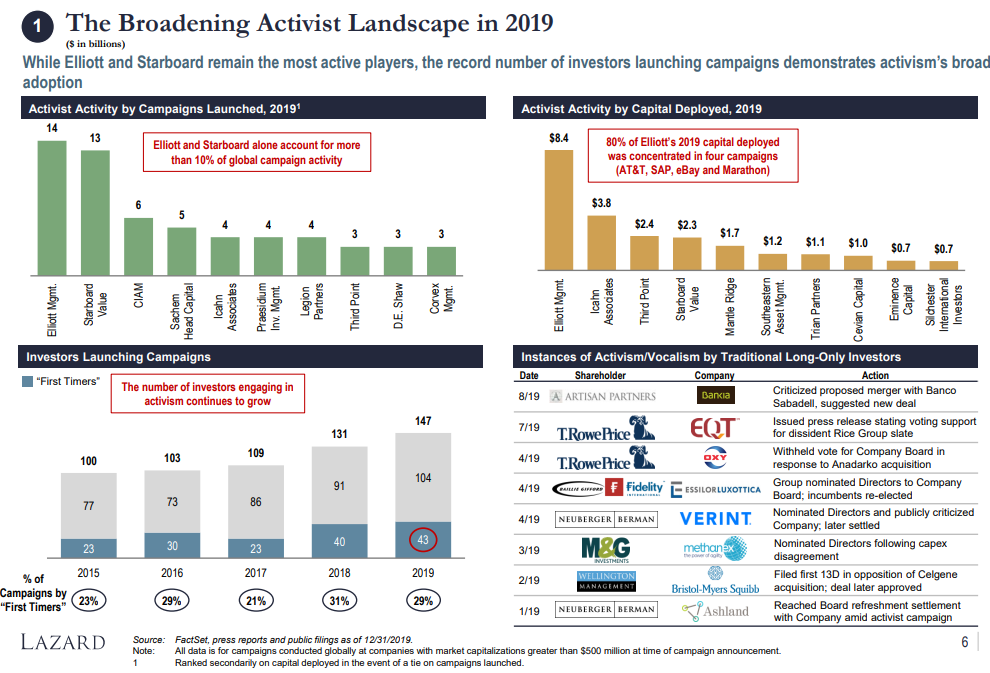

Aujourd’hui, je porte à votre attention une excellente publication de Jim Rossman*, directeur du conseil aux actionnaires, Kathryn Hembree Night, directrice, et Quinn Pitcher, analyste de la firme Lazard, qui présente une revue complète des actionnaires activistes.

Cette étude fait état de l’évolution des activistes en 2019, elle dégage les principales observations des auteurs :

L’activité militante reprend sa tendance pluriannuelle après un record en 2018 ;

La progression constante de l’activisme en dehors des États-Unis ;

Le nombre record de campagnes liées aux fusions et acquisitions ;

L’influence des activistes sur les conseils d’administration se poursuit,

Les pressions sur les gestionnaires actifs s’intensifient.

Autres observations importantes, dont les suivantes :

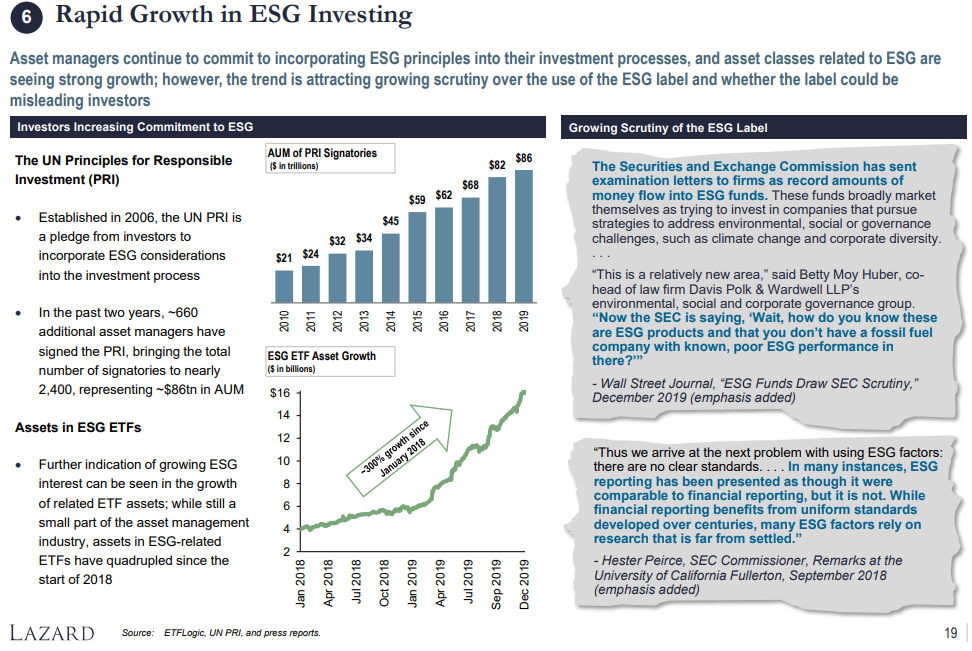

L’accent ESG continue de croître : au cours des deux dernières années, l’actif géré représenté par les signataires des Principes pour l’investissement responsable des Nations Unies a augmenté de 26 % à 86 milliards de dollars, et le nombre d’actifs dans les FNB liés à l’ESG a augmenté de 300 %.

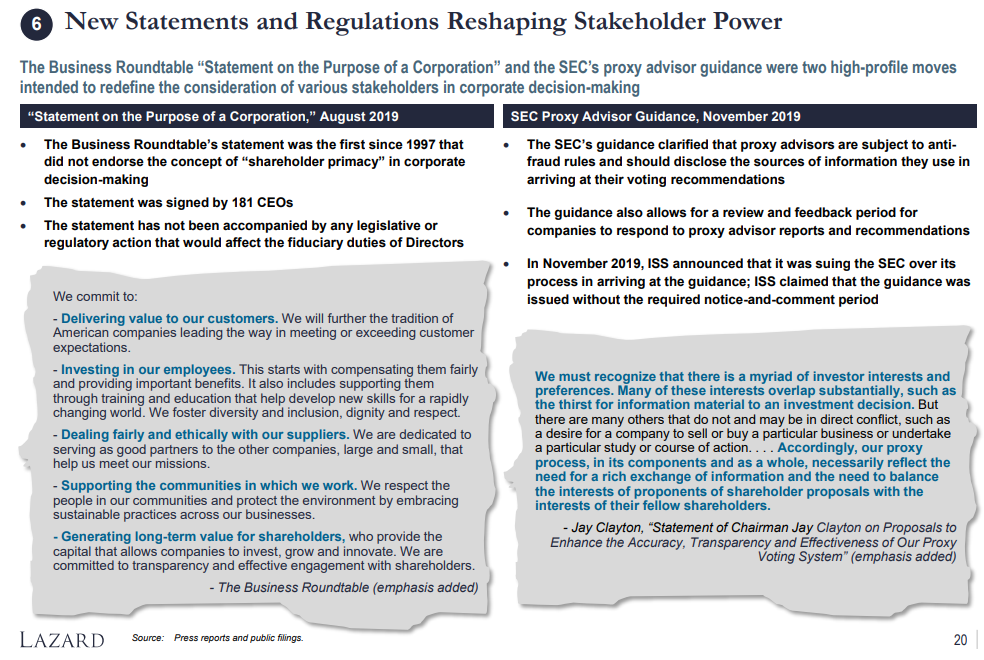

La « Déclaration sur l’objet de la société » de la table ronde des entreprises a souligné l’importance pour les entreprises d’intégrer les intérêts de toutes les parties prenantes, et pas seulement des actionnaires, dans leurs processus décisionnels.

Les directives de la SEC sur les conseillers en vote ont cherché à accroître les normes de responsabilité et de surveillance dans les évaluations de leur entreprise.

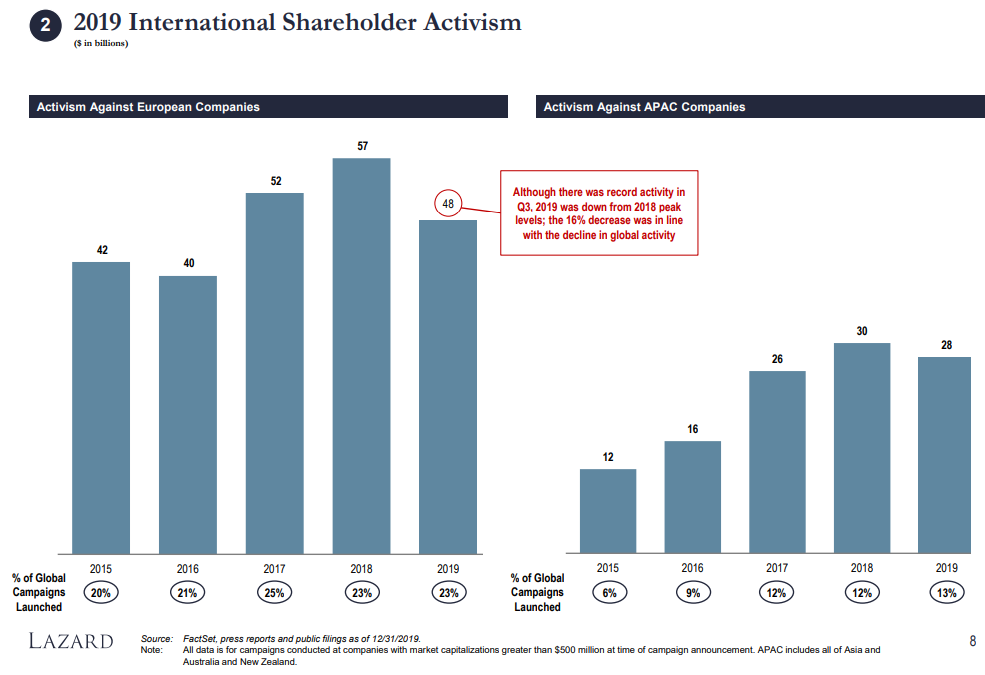

La publication utilise une infographie très efficace pour illustrer les effets de l’activisme aux États-Unis, mais aussi à l’échelle internationale.

Key Observations on the Activist Environment in 2019

1. Activist Activity Returns to Multi-Year Trend After Record 2018

187 companies targeted by activists, down 17% from 2018’s record but in line with multi-year average levels

Aggregate capital deployed by activists (~$42bn) reflected a similar dip relative to the ~$60bn+ level of 2017/2018

A record 147 investors launched new campaigns in 2019, including 43 “first timers” with no prior activism history

Elliott and Starboard remained the leading activists, accounting for more than 10% of global campaign activity

2. Activism’s Continued Influence Outside the U.S.

Activism against non-U.S. targets accounted for ~40% of 2019 activity, up from ~30% in 2015

Multi-year shift driven both by a decline in S. targets and an uptick in activity in Japan and Europe

For the first time, Japan was the most-targeted non-U.S. jurisdiction, with 19 campaigns and $4.5bn in capital deployed in 2019 (both local records)

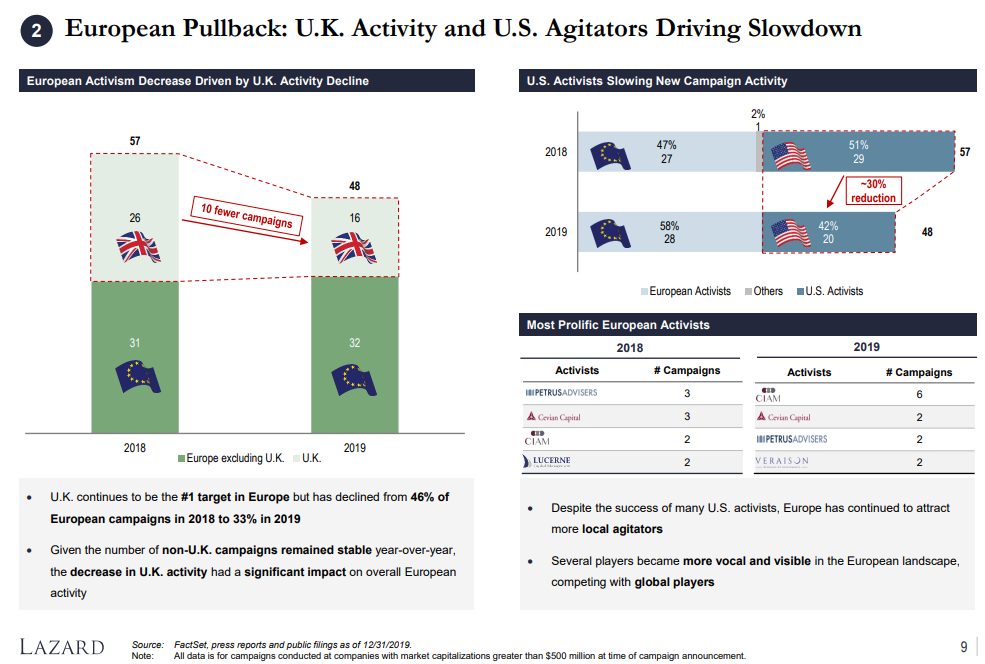

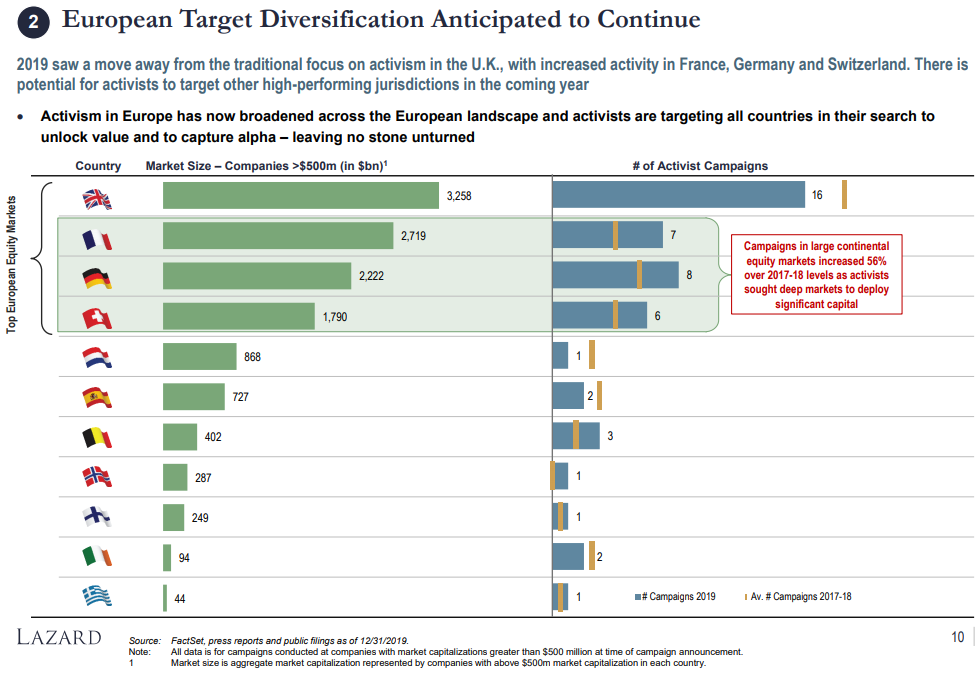

Overall European activity decreased in 2019 (48 campaigns, down from a record 57 in 2018), driven primarily by 10 fewer campaigns in the K.

Expanded activity in continental Europe—particularly France, Germany and Switzerland—partially offset this decline

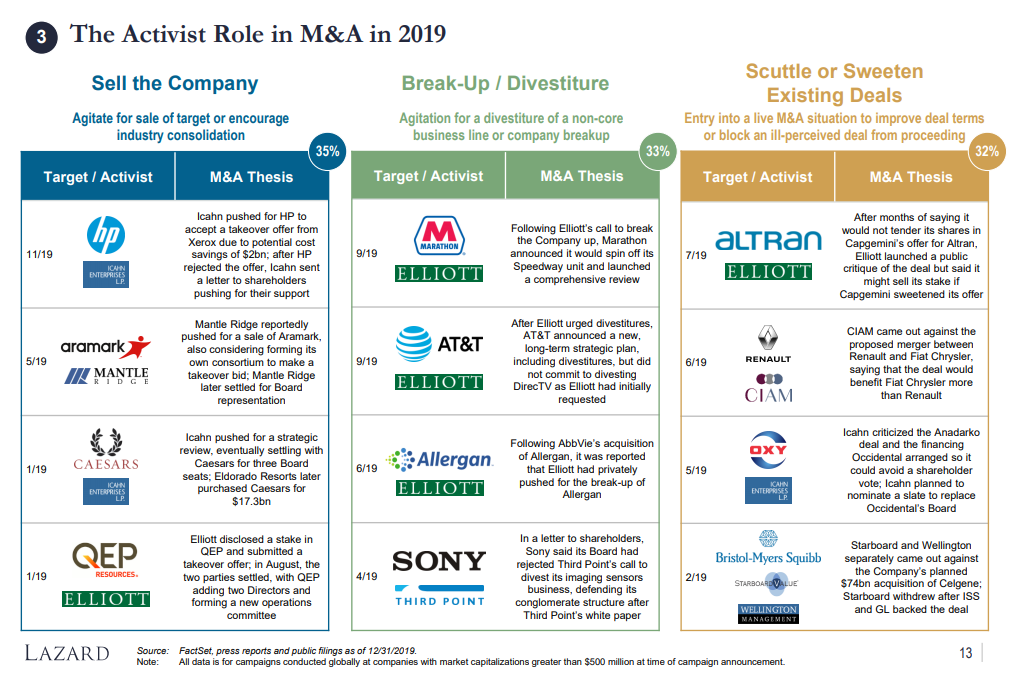

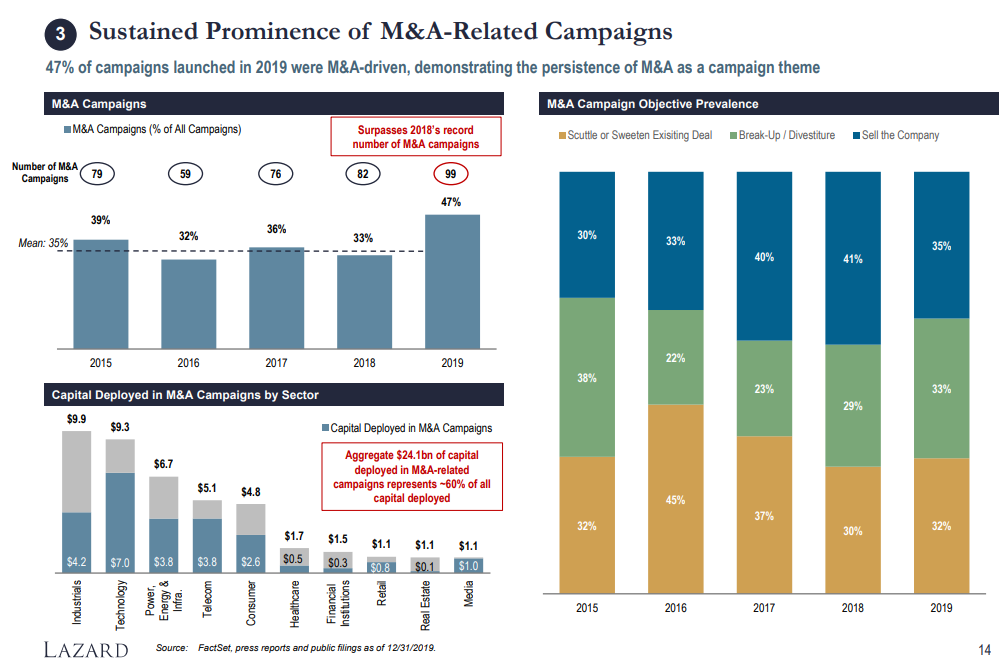

3. Record Number of M&A-Related Campaigns

A record 99 campaigns with an M&A-related thesis (accounting for ~47% of all 2019 activity, up from ~35% in prior years) were launched in 2019

As in prior years, there were numerous prominent examples of activists pushing a sale (HP, Caesars) or break-up (Marathon, Sony) or opposing an announced transaction (Occidental, Bristol-Myers Squibb)

The $24.1bn of capital deployed in M&A-related campaigns in 2019 represented ~60% of total capital deployed

The technology sector alone saw $7.0bn put to use in M&A related campaigns

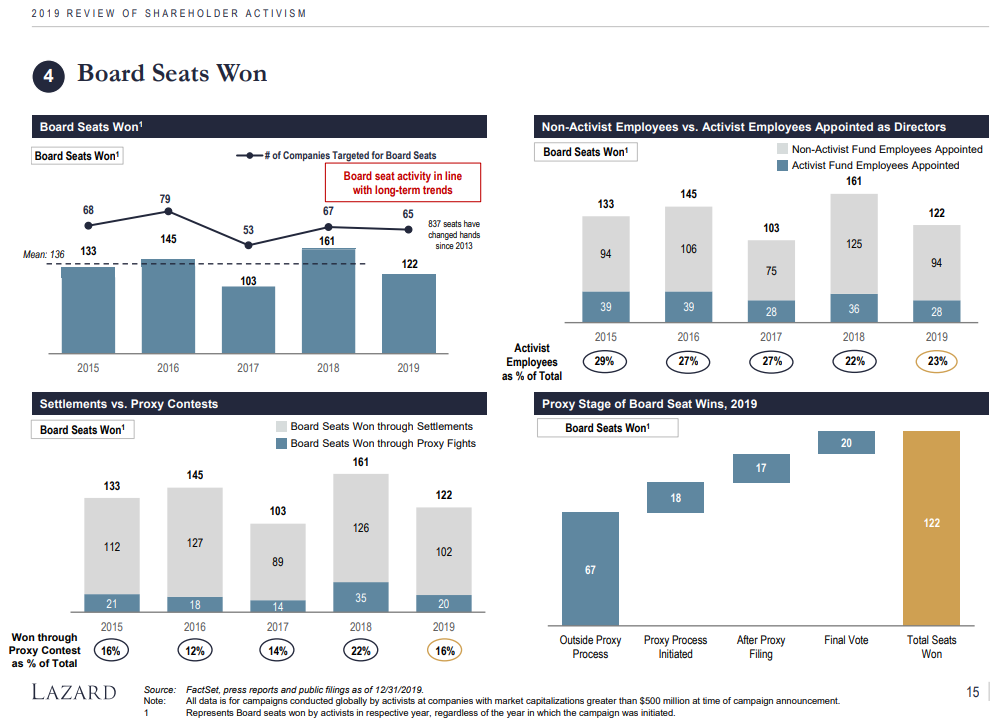

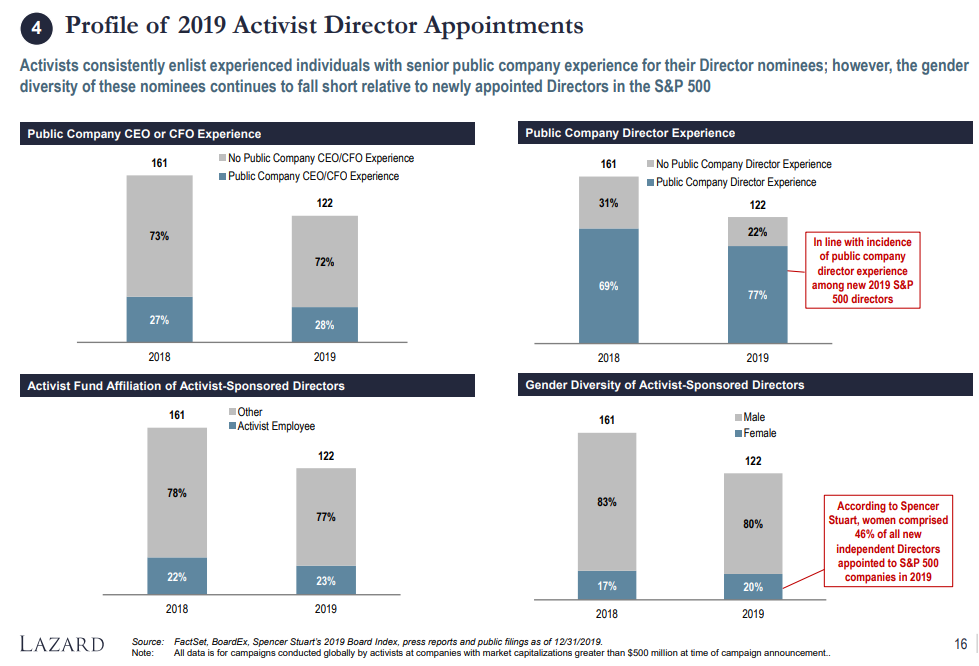

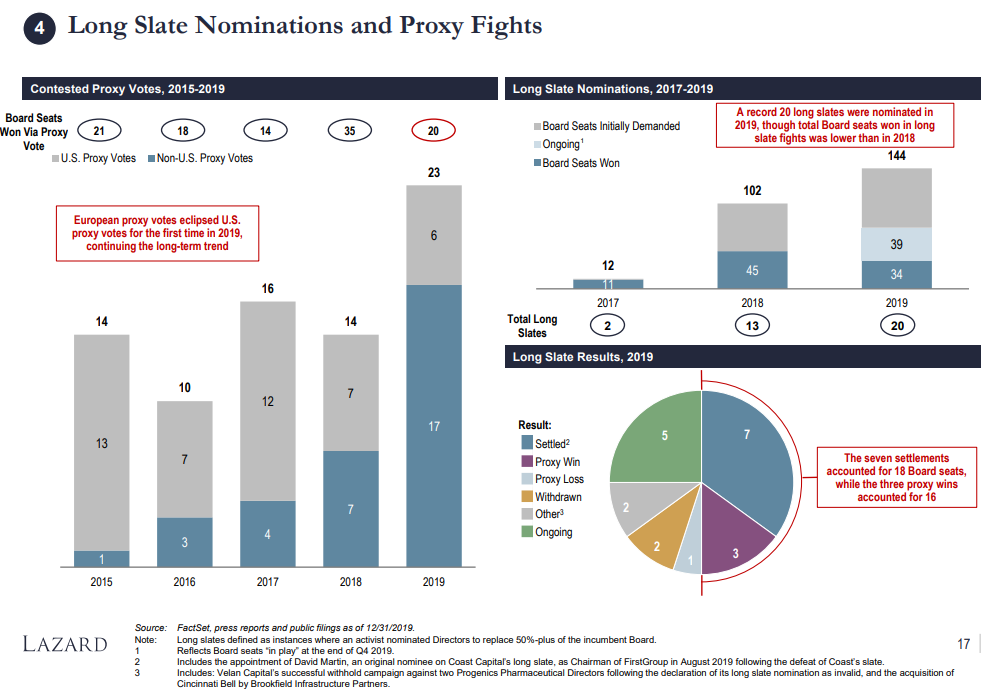

4. Activist Influence on Boards Continues

122 Board seats were won by activists in 2019, in line with the multi-year average [1]

Consistent with recent trends, the majority of Board seats were secured via negotiated settlements (~85% of Board seats)

20% of activist Board seats went to female directors, compared to a rate of 46% for all new S&P 500 director appointees [2]

Activists nominated a record 20 “long slates” seeking to replace a majority of directors in 2019, securing seats in two-thirds (67%) of the situations that have been resolved

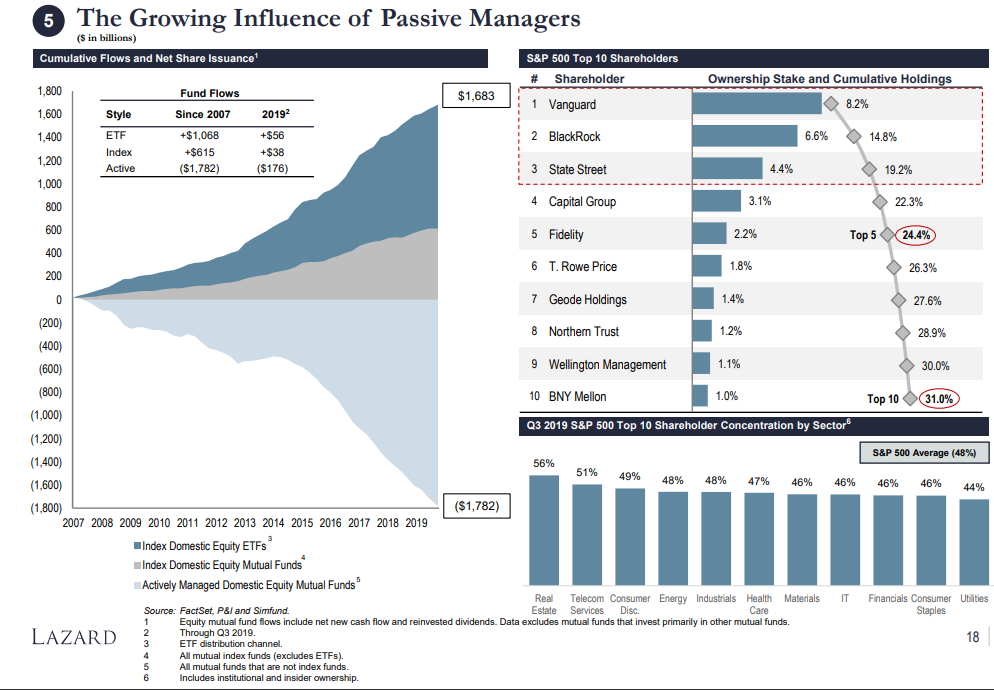

5. Outflow Pressure on Active Managers Intensifies

Actively managed funds saw ~$176bn in net outflows through Q3 2019, compared to ~$105bn in 2018 over the same period

The “Big 3” index funds (BlackRock, Vanguard and State Street) continue to be the primary beneficiaries of passive inflows, collectively owning ~19% of the S&P 500—up from ~16% in 2014

6. Other Noteworthy Observations

ESG focus continues to grow: over the past two years, the AUM represented by signatories to the UN’s Principles for Responsible Investment increased ~26% to ~$86tn, and the number of assets in ESG-related ETFs increased ~300%

The Business Roundtable’s “Statement on the Purpose of the Corporation” emphasized the importance of companies incorporating the interests of all stakeholders, not just shareholders, into their decision-making processes

The SEC’s guidance on proxy advisors sought to increase accountability and oversight standards in their company evaluations

Source: FactSet, ETFLogic, UN PRI, Simfund, press reports and public filings as of 12/31/2019. Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

The complete publication, including Appendix, is available here.

Endnotes

1Represents Board seats won by activists in the respective year, regardless of the year in which the campaign was initiated. (go back)

2According to Spencer Stuart’s 2019 Board Index.(go back)

Récemment, j’ai lu un article vraiment intéressant qui traite d’une problématique très pertinente et concrète pour toutes les organisations.

Les auteurs Arthur H. Kohn* et al ont exploré les avantages et les inconvénients de l’établissement d’une politique anti-fraternisation, c’est-à-dire une politique régissant les relations personnelles étroites entre les employés.

Les auteurs font référence à une récente étude sur le sujet qui montre que 35 à 40 % des employés ont eu une relation romantique consensuelle avec un collègue, et 72 % le feraient à nouveau ! Plus particulièrement, 22 % des employés ont déclaré être sortis avec une personne qui les supervisait.

Dans ce billet, je reproduis la traduction française de l’article paru sur le site de Harvard Law School on Corporate Governance. Je suis bien conscient que cette version n’est pas optimale, mais, selon moi, elle est tout à fait convenable.

À la lecture de ce billet, vous serez en mesure de vous poser les bonnes questions eu égard à l’instauration d’une telle politique de RH. Plus précisément, vous aurez de bons arguments pour répondre à cette question : mon entreprise doit-elle avoir une politique anti-fraternisation ?

Bonne lecture ! Vos commentaires sont les bienvenus.

Ces dernières années, de nombreux cadres supérieurs ont démissionné ou ont été licenciés pour avoir noué des relations consensuelles non divulguées avec des subordonnés. [1] Ces relations font l’objet d’une attention particulière à la suite de l’examen approfondi du comportement sur le lieu de travail, car elles suscitent des inquiétudes concernant, entre autres, les éventuels déséquilibres de pouvoir et les conflits d’intérêts sur le lieu de travail. Ainsi, il est de plus en plus important pour les entreprises de réfléchir à l’opportunité d’instituer des politiques régissant les relations personnelles étroites et à quoi pourraient ressembler ces politiques. Nous abordons quelques considérations clés pour guider ces décisions.

Mon entreprise doit-elle avoir une politique anti-fraternisation ?

Le pourcentage d’entreprises qui ont instauré des politiques concernant les relations personnelles étroites sur le lieu de travail est décidément à la hausse. [2] Certaines entreprises ont des politiques régissant les relations personnelles étroites entre tous les employés, tandis que d’autres politiques se limitent aux relations entre les superviseurs et les subordonnés. Ces derniers types de politiques sont au centre de cette publication (et nous les désignerons, en bref, comme des politiques « anti-fraternisation »). L’an dernier, plus de la moitié des cadres RH interrogés ont déclaré que leur entreprise avait des politiques formelles et écrites concernant les relations personnelles étroites entre les employés, et 78 % ont déclaré que leur entreprise décourageait de telles relations entre les subordonnés et les superviseurs. [3]

Cependant, toutes les entreprises n’ont pas de politiques anti-fraternisation, et ces politiques présentent des avantages et des inconvénients. La manière dont ces avantages et inconvénients se comparent dépendra en grande partie des circonstances spécifiques de l’employeur, telles que sa culture, son expérience en matière de comportement au travail potentiellement inapproprié, sa taille et sa structure organisationnelle.

Côté « pro », adopter une politique anti-fraternisation…

Envoie un message contre le harcèlement sexuel : la préoccupation la plus évidente soulevée par les relations de travail entre les subordonnés et les superviseurs est que, à la lumière du déséquilibre inhérent au pouvoir, ces relations peuvent ne pas être, ou rester, consensuelles et bienvenues, malgré les apparences. Comme le mouvement #MeToo l’a mis en évidence, un subordonné peut ne pas se sentir à l’aise de dire « non » à un superviseur, plutôt d’acquiescer à la relation par crainte d’une action défavorable en matière d’emploi. Ainsi, ce qui peut sembler à première vue une relation bienvenue peut en fait constituer du harcèlement sexuel du point de vue du subordonné. L’instauration d’une politique portant sur de telles relations envoie un message aux employés — de toute ancienneté — que l’entreprise est consciente de ces risques et les prend suffisamment au sérieux pour agir de manière préventive.

Atténue le risque juridique : quand une relation prend fin, l’employeur peut avoir une exposition juridique dérivée pour la conduite des employés impliqués dans la relation, y compris si le subordonné prétend que la relation est le résultat d’une avance indésirable ou si un contact post-relationnel entre les individus est acrimonieux. L’interdiction de la relation devrait atténuer ce risque.

Évite certaines situations d’environnement de travail toxiques : une relation entre un superviseur et un subordonné augmente également le risque de favoritisme réel et/ou perçu. En cas de favoritisme réel, une telle conduite expose l’employeur à des allégations de discrimination ou de harcèlement sexuel sous la forme d’un environnement de travail hostile (par exemple, d’autres employés peuvent prétendre qu’une contrepartie est le seul moyen d’aller de l’avant). De plus, que le favoritisme soit réel ou perçu, il peut réduire la productivité des autres employés, qui peuvent avoir l’impression que leurs contributions passent inaperçues et peuvent ainsi se désengager. La productivité des deux employés impliqués dans la relation peut également en souffrir, dans la mesure où ils poursuivent la relation pendant les heures de travail.

Fournit aux employés un avis concernant les conséquences potentielles d’une relation de travail : les relations de travail peuvent être difficiles, même en l’absence de problème de fraternisation. Des relations personnelles étroites, en particulier entre des employés d’ancienneté variable, aggravent encore ces difficultés. Si une relation de travail a une incidence sur le rendement au travail des employés, elle peut entraîner la réaffectation — ou, dans certaines circonstances, la résiliation — de l’une ou des deux parties. Informer les employés de ces conséquences potentielles grâce à une politique officielle leur permet de prendre des décisions plus éclairées sur l’opportunité de poursuivre une relation de travail. Cela peut également réduire le risque de litiges futurs, en particulier dans les situations où la protection du travail est importante, comme dans les juridictions étrangères ou dans les lieux de travail syndiqués.

Donne aux employeurs une règle claire : lorsque les relations de travail se rompent et qu’un dysfonctionnement survient, les causes peuvent être contestées et légitimement obscures. L’employeur se retrouve souvent à gérer les retombées, y compris à devoir décider lequel des employés dans la relation devrait être réaffecté à un rôle différent ou se séparer de l’entreprise. Une politique anti-fraternisation peut fournir une règle de ligne claire utile.

Côté « con », une politique anti-fraternisation…

Peut créer une perception de paternalisme : les données d’une enquête récente suggèrent qu’environ 35 à 40 % des employés ont eu une relation romantique consensuelle avec un collègue, et 72 % le feraient à nouveau. [4]Plus particulièrement, 22 % des employés ont déclaré être sortis avec quelqu’un qui les supervisait. [5] Ainsi, les relations amoureuses se forment et s’épanouissent souvent sur le lieu de travail, et les efforts d’un employeur pour les décourager peuvent être perçus par les employés comme paternalistes et comme un empiétement sur leur vie personnelle. Cela est particulièrement probable pour une entreprise qui a une structure organisationnelle plus hiérarchisée avec de nombreux niveaux de superviseurs, car une grande partie de ses employés seraient affectés par une politique anti-fraternisation, même limitée aux relations personnelles étroites entre les superviseurs les subordonnés. Cela pourrait également être une préoccupation pour les cultures de travail moins formelles, dans lesquelles l’aspect paternaliste de la politique pourrait être particulièrement difficile à l’encontre de la culture globale.

Requiert une appréciation difficile : définir ce qui constitue une relation personnelle étroite sur le lieu de travail n’est pas une tâche facile. Cela nécessite de porter des jugements sur des questions très subjectives et spécifiques aux faits. De plus, cela nécessite de s’attaquer à des sujets rarement abordés sur le lieu de travail. Il est essentiel d’avoir des professionnels des RH désireux et capables de répondre à ces questions pour une politique efficace.

Est difficile à « contrôler » : étant donné le caractère très privé du sujet, l’instauration d’une politique anti-fraternisation soulève également des questions complexes sur les types de mesures qu’un employeur peut ou devrait prendre — à la fois d’un point de vue juridique et pratique — dans le suivi de la politique. Par exemple, les superviseurs doivent-ils certifier la conformité à la politique ? Comment les entreprises démontrent-elles aux parties prenantes que la politique est appliquée ? L’entreprise effectue-t-elle une surveillance de la conformité, par exemple en examinant les courriels ou les réseaux sociaux des superviseurs ?

Que doit dire la politique anti-fraternisation de mon entreprise ?

Si un employeur choisit d’instituer une politique anti-fraternisation, il existe un large éventail d’approches, notamment en ce qui concerne la portée des comportements interdits et les conséquences de s’engager dans des relations personnelles étroites.

Quelle conduite est interdite ?

À un extrême, l’employeur peut choisir d’interdire les relations entre tous les employés. L’employeur peut également choisir de limiter sa politique anti-fraternisation aux relations entre les employés d’ancienneté variable ou, plus précisément, entre les superviseurs et leurs subordonnés directs ou indirects. D’après notre expérience, l’interdiction des relations entre les superviseurs et leurs subordonnés directs ou indirects présente le meilleur équilibre de considérations pour la plupart des grandes entreprises.

Une approche viable pourrait consister à ce que la politique anti-fraternisation :

décrive les préoccupations de l’employeur eu égard aux relations de travail (y compris les préoccupations discutées ci-dessus, ainsi que toutes les autres applicables au lieu de travail de l’employeur) ;

exige des employés qu’ils signalent des relations personnelles étroites par le biais de canaux désignés (selon la culture de l’employeur et les circonstances spécifiques, une telle exigence de déclaration pourrait s’appliquer à tous les employés ou se limiter aux relations entre des employés d’ancienneté variable) ; et

interdit les relations entre les superviseurs et leurs subordonnés directs (ou proches) (en gardant à l’esprit que chaque employé relève du PDG), et peut-être entre les employés dans certaines fonctions commerciales sensibles, telles que les finances, l’audit et le juridique, où une relation peut donner lieu à préoccupations particulièrement difficiles.

Instituer une obligation de déclaration peut, selon la culture d’entreprise, rassurer les employés plus jeunes quant au risque potentiel de harcèlement. Il peut également répondre à certaines des autres préoccupations évoquées ci-dessus, en permettant à l’employeur de surveiller les effets négatifs de la relation sur l’environnement de travail global et de fournir aux employés un avis plus détaillé des conséquences potentielles de la relation divulguée.

Qu’est-ce qui constitue une « relation personnelle étroite » ?

Comme indiqué ci-dessus, l’instauration d’une politique anti-fraternisation nécessite de naviguer dans certaines zones grises, notamment les types de relations qui devraient entrer dans le champ d’application de la politique. D’après notre expérience, la plupart des entreprises qui adoptent des politiques anti-fraternisation utilisent l’expression « relation personnelle étroite » pour décrire la conduite qui fait l’objet de la politique.

En raison de la nature hautement subjective et diversifiée des relations interpersonnelles, il est généralement difficile de trouver une approche « taille unique ». Ainsi, les employeurs peuvent choisir de laisser cela indéfini, ce qui incombe aux employés de déterminer si, dans les circonstances, leur relation entre dans le cadre de la politique de l’employeur. Une autre approche consiste à ce que la politique anti-fraternisation prévoie qu’une relation entre dans son champ d’application dans la mesure où elle a un impact subjectif ou objectif sur la performance au travail des employés dans la relation et/ou d’autres employés. Par exemple, la politique s’appliquerait si la relation crée des tensions entre les employés de la relation et les autres, ou si les employés de la relation ne s’acquittent pas de leurs responsabilités quotidiennes.

Plus important encore, la définition de la politique devrait être adaptée à la culture et à l’environnement de travail de l’employeur, et elle devrait également être flexible, compte tenu des circonstances variables dans lesquelles la politique peut être impliquée.

Quelles sont les obligations de déclaration et leurs implications ?

Si l’employeur établit des obligations de déclaration en ce qui concerne les relations personnelles étroites, ces obligations devraient être imposées au superviseur ou à un employé plus âgé dans la relation, afin d’atténuer les déséquilibres de pouvoir inhérents. Selon la situation particulière de l’employeur, le canal de communication peut être adressé à un chef d’entreprise ou à un représentant de l’équipe des ressources humaines.

La politique devrait également indiquer les mesures que l’employeur prendra, une fois la relation révélée, afin d’atténuer les préoccupations évoquées ci-dessus. Par exemple, l’employeur devrait envisager des mesures qui supprimeront la relation de supervision entre les employés, comme la réaffectation d’un ou des deux, et devrait également récuser le superviseur de toute décision liée à l’emploi ou à la performance concernant le subordonné. Il convient de veiller tout particulièrement à ce que les réaffectations ne soient pas mises en œuvre d’une manière qui puisse donner lieu à une plainte pour discrimination fondée sur le sexe contre l’employeur.

Conclusion

Il est essentiel que les employeurs acquièrent une compréhension nuancée des risques et des causes profondes des comportements potentiellement inappropriés sur leur lieu de travail, et développent des outils efficaces pour atténuer ces risques. Une politique anti-fraternisation peut servir d’outil de ce type, et les employeurs devraient évaluer les avantages et les inconvénients d’une telle politique dans le contexte des circonstances uniques de leur lieu de travail.

Voici un excellent article deJames E. Langston*, associé de la firme Cleary Gottlieb Steen & Hamilton, sur les nouvelles perspectives offertes par les activités activistes de tout ordre. Cet article a paru sur le site de Harvard Law School on Corporate Governance.

Les points saillants exposés par l’auteur dans cet article sont les suivants :

Les activités activistes sont moins orientées vers le profit à court terme ; les investisseurs sont toujours préoccupés par les résultats à court terme, mais ils adoptent également une vision de plus en plus à long terme ;

On observe la montée d’une nouvelle forme d’activisme : l’activisme des parties prenantes (stakeholders), ou activisme social, qui emprunte aux méthodes de l’activisme traditionnel pour avancer leurs causes. On parle ici des fonds de pension, des gestionnaires d’actifs et des organisations à but charitables ;

Également, on note l’accroissement des activités d’activisme uniquement à long terme. Ces parties prenantes exercent de plus en plus de pression activiste auprès des administrateurs des CA ;

Dans le cas des très grandes entreprises, les conseils d’administration et les directions générales sont plus ouverts à des arrangements de gré à gré pour effectuer les changements réclamés par les activistes. Cependant, cette pause dans les relations entre ces deux entités n’est pas une garantie qu’elle ne sera pas suivie de nouvelles demandes toujours plus contraignantes pour les sociétés ;

Enfin, le développement de l’activisme continue de prendre de l’ampleur dans les marchés internationaux, en adoptant le modèle et les manières de faire des activistes américains ;

Les auteurs incitent les conseils d’administration à être très vigilants dans l’évaluation des nouveaux risques de gouvernance ainsi que dans la prise en compte des nouvelles occasions qui se présentent.

En tant qu’administrateur, je vous invite à lire cet article pour vous sensibiliser à la nouvelle donne.

Bonne lecture !

Shareholder Activism in 2020: New Risks and Opportunities for Boards

The era of stakeholder governance and corporations with a purpose beyond profits is taking hold, with corporate directors expected to answer to more constituencies and shoulder a greater burden than ever before. At the same time, investors—both in the US and abroad—continue to expect corporations to deliver superior financial performance over both the short and long term.

This convergence of purpose and performance will not only shape discussions in the boardroom, but also the complexion of shareholder activism. As the nature of the activist threat has evolved it has created additional obstacles for directors to navigate. But at the same time, this environment has created additional opportunities for boards to level the activist playing field and lead investors and other stakeholders into this new era.

Environmental, Social and Corporate Activism

Today, shareholder activists and governance gadflies are not the only constituencies using the corporate machinery to advocate for change. Social activists and institutional investors are increasingly joining forces and borrowing tactics from the shareholder activist playbook, particularly as they push for ESG reforms. For example, in 2019, prominent pension funds, asset managers and other charitable organizations sent a joint letter to all Fortune 500 companies calling for greater disclosure of mid-level worker pay practices. In addition, the Interfaith Center for Corporate Responsibility—on behalf of over 100 investors—spearheaded the submission of more than 10 shareholder proposals focusing on environmental and labor issues for the annual meeting of a single corporation.

We expect this type of stakeholder activism—or the convergence of shareholder activism and social activism—to continue and eventually move beyond the ESG realm. Although this marks yet another trend that boards must be prepared to face, it also offers directors an opportunity to embrace stakeholder interests other than EPS accretion or margin expansion to support the company’s governance profile and long-term strategic plan. To be sure, financial performance of the corporation over the long term, which benefits all stakeholders, will remain paramount, but focusing on the merits of the strategic plan for all stakeholders should help the board ensure management has sufficient runway to implement that plan and garner the support of more, rather than fewer, corporate constituencies along the way.

Long-Only Activism

At the same time, activism by traditional long-only investors also has increased. For example, Neuberger Berman pushed for board refreshment at Ashland Global as part of a Cruiser Capital-led campaign and launched a short-slate proxy contest at Verint Systems that settled when the company agreed to refresh its board and enhance its investor disclosures. Wellington Management also joined the fray, publicly backing—and by some accounts initiating—Starboard’s efforts to scuttle the Bristol Myers/Celgene merger. And T. Rowe Price doubled down on its activism efforts by publicly backing the Rice Brothers’ successful campaign to take control of the EQT board.

The takeaway for directors from this sort of activism is clear – no longer will institutional investors be content to sit on the sidelines or express their views privately. Directors should expect that increased long-only activism will create a challenging environment for active managers (including continued pressure on management fees) and will likely lead more of them to embrace activism, and to do so more publicly, as a way to differentiate their investment strategy.

The question for boards in this new environment is not just whether institutional investors will be a source of ideas for an activist or side with the board or the activist in the event of a campaign, but also whether its institutional investors are likely to themselves “go activist.” Shareholder engagement efforts will continue to be crucial in building support for a strategic plan and counteracting activist tendencies among long-only investors. But in the course of such efforts, directors must be mindful of the fact that not all institutional investors will have the same objectives and be careful to structure their interactions with investors accordingly. Well-advised boards will look for ways to find common ground with long-only investors while articulating the company’s long-term strategy in a manner that emphasizes its corporate purpose and is more likely to resonate with all stakeholders.

Large-Cap Activism and Settlement Agreements

Another trend boards must be aware of in 2020 is the success of certain brand-name activists in “settling” large-cap campaigns without committing to a settlement agreement with a standstill undertaking. Typically, a standstill, preventing the activist from exerting pressure on the company for a certain period of time, is the price the activist pays for the company committing to take certain of the steps proposed by the activist. The standstill is intended to ensure that the company has the breathing room necessary to implement the agreed-upon changes and make its case to investors.

However, several recent large-cap activist situations followed a different script. The companies engaged with the activists and announced a series of changes designed to appease the activist, ranging from purported governance and operational enhancements to full-blown strategic reviews. The activist then issued a separate, choreographed press release, often taking much of the credit for the changes and promising to work with the company to bring about the proposed changes. But that was it—there was no settlement agreement or other commitment by the activist to cease its efforts to influence the board.

Not surprisingly, in at least one of these situations, the company “settled” with an activist without a standstill only to face additional demands from the same activist several months later (and which required additional concessions). As always, the terms of peace with an activist will be shaped by the situational dynamics, but as 2020 dawns, directors should continue to be mindful of the benefits of a standstill.

Activism Abroad

Shareholder activism also continues to expand globally. Boards in Europe and Asia are increasingly finding themselves under pressure from activists. In these situations, boards have faced not only home-grown activists, but also US activists looking to expand their influence and investor base abroad.

We expect this trend to accelerate in 2020 for several reasons:

The number of easy activist targets in the US has dwindled.

US-based index funds continue to consolidate their ownership of public companies across the globe.

Foreign investors are becoming more prone to expect US-style capital allocation policies and shareholder return metrics from non-US companies.

The message to non-US boards is clear: If you aren’t thinking about activism, you should be. This doesn’t mean foreign issuers should reflexively adopt US practices; they shouldn’t. But it does mean that non-US boards should ensure they are prepared to deal with an activist event and consider a strategy that not only takes into account local conditions but also is informed by the relevant lessons from the US experience with shareholder activism.

Je partage avec vous l’excellente prise de position de Martin Lipton *, Karessa L. Cain et Kathleen C. Iannone, associés de la firme Wachtell, Lipton, Rosen & Katz, spécialisée dans les fusions et acquisitions et dans les questions de gouvernance fiduciaire.

L’article présente un plaidoyer éloquent en faveur d’une gouvernance fiduciaire par un conseil d’administration qui doit non seulement considérer le point de vue des actionnaires, mais aussi des autres parties prenantes,

Depuis quelque temps, on assiste à des changements significatifs dans la compréhension du rôle des CA et dans l’interprétation que les administrateurs se font de la valeur de l’entreprise à long terme.

Récemment, le Business Roundtable a annoncé son engagement envers l’inclusion des parties prenantes dans le cadre de gouvernance fiduciaire des sociétés.

Among the developments followers of business ethics may have thought they’d never see, the end of the shareholder value myth has to rank very high.

Yet one of America’s leading business lobbying groups just buried the myth. “We share a fundamental commitment to all of our stakeholders,” reads a statement issued Monday by the Business Roundtable and signed by 181 CEOs. (Emphasis in the original.)

The statement mentions, in order, customers, employees, suppliers, communities and — dead last — shareholders. The corporate commitment to all these stakeholders may be largely rhetorical at the moment, but it’s hard to overstate what a reversal the statement represents from the business community’s preexisting viewpoint.

Stakeholders are pushing companies to wade into sensitive social and political issues — especially as they see governments failing to do so effectively.

Since the 1970s, the prevailing ethos of corporate management has been that a company’s prime responsibility — effectively, its only responsibility — is to serve its shareholders. Benefits for those other stakeholders follow, but they’re not the prime concern.

In the Business Roundtable’s view, the paramount duty of management and of boards of directors is to the corporation’s stockholders; the interests of other stakeholders are relevant as a derivative of the duty to stockholders,” the organization declared in 1997.

Bonne lecture. Vos commentaires sont les bienvenus !

JPMorgan Chase Chief Executive Jamie Dimon signed the business statement disavowing the shareholder value myth.(J. Scott Applewhite / Associated Press)

There has recently been much debate and some confusion about a bedrock principle of corporate law—namely, the essence of the board’s fiduciary duty, and particularly the extent to which the board can or should or must consider the interests of other stakeholders besides shareholders.

For several decades, there has been a prevailing assumption among many CEOs, directors, scholars, investors, asset managers and others that the sole purpose of corporations is to maximize value for shareholders and, accordingly, that corporate decision-makers should be very closely tethered to the views and preferences of shareholders. This has created an opportunity for corporate raiders, activist hedge funds and others with short-termist agendas, who do not hesitate to assert their preferences and are often the most vocal of shareholder constituents. And, even outside the context of shareholder activism, the relentless pressure to produce shareholder value has all too often tipped the scales in favor of near-term stock price gains at the expense of long-term sustainability.

In recent years, however, there has been a growing sense of urgency around issues such as economic inequality, climate change and socioeconomic upheaval as human capital has been displaced by technological disruption. As long-term investors and the asset managers who represent them have sought to embrace ESG principles and their role as stewards of corporations in pursuit of long-term value, notions of shareholder primacy are being challenged. Thus, earlier this week, the Business Roundtable announced its commitment to stakeholder corporate governance, and outside the U.S., legislative reforms in the U.K. and Europe have expressly incorporated consideration of other stakeholder interests in the fiduciary duty framework. The Council of Institutional Investors and others, however, have challenged the wisdom and legality of stakeholder corporate governance.

To be clear, Delaware law does not enshrine a principle of shareholder primacy or preclude a board of directors from considering the interests of other stakeholders. Nor does the law of any other state. Although much attention has been given to the Revlon doctrine, which suggests that the board must attempt to achieve the highest value reasonably available to shareholders, that doctrine is narrowly limited to situations where the board has determined to sell control of the company and either all or a preponderant percentage of the consideration being paid is cash or the transaction will result in a controlling shareholder. Indeed, theRevlon doctrine has played an outsized role in fiduciary duty jurisprudence not because it articulates the ultimate nature and objective of the board’s fiduciary duty, but rather because most fiduciary duty litigation arises in the context of mergers or other extraordinary transactions where heightened standards of judicial review are applicable. In addition, Revlon’s emphasis on maximizing short-term shareholder value has served as a convenient touchstone for advocates of shareholder primacy and has accordingly been used as a talking point to shape assumptions about fiduciary duties even outside the sale-of-control context, a result that was not intended. Around the same time that Revlon was decided, the Delaware Supreme Court also decided the Unocal and Household cases, which affirmed the board’s ability to consider all stakeholders in using a poison pill to defend against a takeover—clearly confining Revlonto sale-of-control situations.

The fiduciary duty of the board is to promote the value of the corporation. In fulfilling that duty, directors must exercise their business judgment in considering and reconciling the interests of various stakeholders—including shareholders, employees, customers, suppliers, the environment and communities—and the attendant risks and opportunities for the corporation.

Indeed, the board’s ability to consider other stakeholder interests is not only uncontroversial—it is a matter of basic common sense and a fundamental component of both risk management and strategic planning. Corporations today must navigate a host of challenges to compete and succeed in a rapidly changing environment—for example, as climate change increases weather-related risks to production facilities or real property investments, or as employee training becomes critical to navigate rapidly evolving technology platforms. A board and management team that is myopically focused on stock price and other discernible benchmarks of shareholder value, without also taking a broader, more holistic view of the corporation and its longer-term strategy, sustainability and risk profile, is doing a disservice not only to employees, customers and other impacted stakeholders but also to shareholders and the corporation as a whole.

The board’s role in performing this balancing function is a central premise of the corporate structure. The board is empowered to serve as the arbiter of competing considerations, whereas shareholders have relatively limited voting rights and, in many instances, it is up to the board to decide whether a matter should be submitted for shareholder approval (for example, charter amendments and merger agreements). Moreover, in performing this balancing function, the board is protected by the business judgment rule and will not be second-guessed for embracing ESG principles or other stakeholder interests in order to enhance the long-term value of the corporation. Nor is there any debate about whether the board has the legal authority to reject an activist’s demand for short-term financial engineering on the grounds that the board, in its business judgment, has determined to pursue a strategy to create sustainable long-term value.

And yet even if, as a doctrinal matter, shareholder primacy does not define the contours of the board’s fiduciary duties so as to preclude consideration of other stakeholders, the practical reality is that the board’s ability to embrace ESG principles and sustainable investment strategies depends on the support of long-term investors and asset managers. Shareholders are the only corporate stakeholders who have the right to elect directors, and in contrast to courts, they do not decline to second-guess the business judgment of boards. Furthermore, a number of changes over the last several decades—including the remarkable consolidation of economic and voting power among a relatively small number of asset managers, as well as legal and “best practice” reforms—have strengthened the ability of shareholders to influence corporate decision-making.

To this end, we have proposed The New Paradigm, which conceives of corporate governance as a partnership among corporations, shareholders and other stakeholders to resist short-termism and embrace ESG principles in order to create sustainable, long-term value. See our paper, It’s Time to Adopt The New Paradigm.

Martin Lipton* is a founding partner of Wachtell, Lipton, Rosen & Katz, specializing in mergers and acquisitions and matters affecting corporate policy and strategy; Karessa L. Cain is a partner; and Kathleen C. Iannone is an associate. This post is based on their Wachtell Lipton publication.

Aujourd’hui, je veux porter à l’attention de mes lecteurs un article de Assaf Hamdani* et Sharon Hannes* qui aborde deux développements majeurs qui ont pour effet de bouleverser les marchés des capitaux.

D’une part, les auteurs constatent le rôle de plus en plus fondamental que les investisseurs institutionnels jouent sur le marché des capitaux aux É. U., mais aussi au Canada.

En effet, ceux-ci contrôlent environ les trois quarts du marché, et cette situation continue de progresser. Les auteurs notent qu’un petit nombre de fonds détiennent une partie significative du capital de chaque entreprise.

Les investisseurs individuels sont de moins en moins présents sur l’échiquier de l’actionnariat et leur influence est donc à peu près nulle.

Dans quelle mesure les investisseurs institutionnels exercent-ils leur influence sur la gouvernance des entreprises ? Quels sont les changements qui s’opèrent à cet égard ?

Comment leurs actions sont-elles coordonnées avec les actionnaires activistes (hedge funds) ?

La seconde tendance, qui se dessine depuis plus de 10 ans, concerne l’augmentation considérable de l’influence des actionnaires activistes (hedge funds) qui utilisent des moyens de pression de plus en plus grands pour imposer des changements à la gouvernance des organisations, notamment par la nomination d’administrateurs désignés aux CA des entreprises ciblées.

Quelles sont les nouvelles perspectives pour les activistes et comment les autorités réglementaires doivent-elles réagir face à la croissance des pressions pour modifier les conseils d’administration ?

Je vous invite à lire ce court article pour avoir un aperçu des changements à venir eu égard à la gouvernance des sociétés.

Two major developments are shaping modern capital markets. The first development is the dramatic increase in the size and influence of institutional investors, mostly mutual funds. Institutional investors today collectively own 70-80% of the entire U.S. capital market, and a small number of fund managers hold significant stakes at each public company. The second development is the rising influence of activist hedge funds, which use proxy fights and other tools to pressure public companies into making business and governance changes.

Our new article, The Future of Shareholder Activism, prepared for Boston University Law Review’s Symposium on Institutional Investor Activism in the 21st Century, focuses on the interaction of these two developments and its implications for the future of shareholder activism. We show that the rise of activist hedge funds and their dramatic impact question the claim that institutional investors have conflicts of interest that are sufficiently pervasive to have a substantial market-wide effect. We further argue that the rise of money managers’ power has already changed and will continue to change the nature of shareholder activism. Specifically, large money managers’ clout means that they can influence companies’ management without resorting to the aggressive tactics used by activist hedge funds. Finally, we argue that some activist interventions—those that require the appointment of activist directors to implement complex business changes—cannot be pursued by money managers without dramatic changes to their respective business models and regulatory landscapes.

We first address the overlooked implications of the rise of activist hedge funds for the debate on institutional investors’ stewardship incentives. The success of activist hedge funds, this Article argues, cannot be reconciled with the claim that institutional investors have conflicts of interest that are sufficiently pervasive to have a substantial market-wide effect. Activist hedge funds do not hold a sufficiently large number of shares to win proxy battles, and their success to drive corporate change therefore relies on the willingness of large fund managers to support their cause. Thus, one cannot celebrate—or express concern over—the achievements of activist hedge funds and at the same time argue that institutional investors systemically desire to appease managers.

But if money managers are the real power brokers, why do institutional investors not play a more proactive role in policing management? One set of answers to this question focuses on the shortcomings of fund managers—their suboptimal incentives to oversee companies in their portfolio and conflicts of interest. Another answer focuses on the regulatory regime that governs institutional investors and the impediments that it creates for shareholder activism.

We offer a more nuanced account of the interaction of activists and institutional investors. We argue that the rising influence of fund managers is shaping and is likely to shape the relationships among corporate insiders, institutional investors, and activist hedge funds. Institutional investors’ increasing clout allows them to influence companies without resorting to the aggressive tactics that are typical of activist hedge funds. With institutional investors holding the key to their continued service at the company, corporate insiders today are likely to be more attentive to the wishes of their institutional investors, especially the largest ones.

In fact, in today’s marketplace, management is encouraged to “think like an activist” and initiate contact with large fund managers to learn about any concerns that could trigger an activist attack. Institutional investors—especially the large ones—can thus affect corporations simply by sharing their views with management. This sheds new light on what is labeled today as “engagement.” Moreover, the line between institutional investors’ engagement and hedge fund activism could increasingly become blurred. To be sure, we do not expect institutional investors to develop deeply researched and detailed plans for companies’ operational improvement. Yet, institutional investors’ engagement is increasingly likely to focus not only on governance, but also on business and strategy issues.

The rising influence of institutional investors, however, is unlikely to displace at least some forms of activism. Specifically, we argue that institutional investors are unlikely to be effective in leading complex business interventions that require director appointments. Activists often appoint directors to target boards. Such appointments may be necessary to implement an activist campaign when the corporate change underlying the intervention does not lend itself to quick fixes, such as selling a subsidiary or buying back shares. In complex cases, activist directors are required not only in order to continuously monitor management, but also to further refine the activist business plan for the company.

This insight, however, only serves to reframe our Article’s basic question. Given the rising power of institutional investors, why can they not appoint such directors to companies’ boards? The answer lies in the need of such directors to share nonpublic information with the fund that appointed them. Sharing such information with institutional investors would create significant insider trading concerns and would critically change the role of institutional investors as relatively passive investors with a limited say over company affairs.

Aujourd’hui, je présente un article publié par Azeus Convene qui montre l’importance accrue que les entreprises doivent apporter au développement durable.

L’article insiste sur le rôle du conseil d’administration pour faire des principes du développement durable à long terme les principales conditions de succès des organisations.

Les administrateurs doivent concevoir des politiques qui génèrent une valeur ajoutée à long terme pour les actionnaires, mais ils doivent aussi contribuer à améliorer le sort des parties prenantes, telles que les clients, les communautés et la société en général.

Il n’est cependant pas facile d’adopter des politiques qui mettent de l’avant les principes du développement durable et de la gestion des risques liés à l’environnement.

Dans ce document, publié sur le site de Board Agenda, on explique l’approche que les conseils d’administration doivent adopter en insistant plus particulièrement sur trois points :

Un leadership capable de faire valoir les nombreux avantages stratégiques à tirer de cette approche ;

Des conseils eu égard à l’implantation des changements

Le processus de communication à mettre en œuvre afin de faire valoir les succès des entreprises

L’article qui suit donne plus de détails sur les fondements et l’application de l’approche du développement durable.

Bonne lecture ! Vos commentaires sont appréciés.

Le développement durable, la création de valeur et le rôle du CA

Businesses everywhere are developing sustainability policies. Implementation is never easy, but the right guidance can show the way.

When the experts sat down to write the UK’s new Corporate Governance Code earlier this year, they drafted a critical first principle. The role of the board is to “promote the long-term sustainable success of the company”. Boardroom members should generate value for shareholders, but they should also be “contributing to wider society”.

It is the values inherent in this principle that enshrines sustainability at the heart of running a company today.

Often sustainability is viewed narrowly, relating to policies affecting climate change. But it has long since ceased to be just about the environment. Sustainability has become a multifaceted concern embracing the long-term interests of shareholders, but also responsibilities to society, customers and local communities.

Publications like Harvard Business Review now publish articles such as “Inclusive growth: profitable strategies for tackling poverty and inequality”, or “Competing on social purpose”. Forbes has “How procurement will save the world” and “How companies can increase market rewards for sustainability efforts”. Sustainability is a headline issue for company leaders and here to stay.

But it’s not always easy to see how sustainability is integrated into a company’s existing strategy. So, why should your company engage with sustainability and what steps can it take to ensure it is done well?

…one of the biggest issues at the heart of the drive for sustainability is leadership. Implementing the right policies is undoubtedly a “top-down” process, not least because legal rulings have emphatically cast sustainability as a fiduciary duty.

The reasons for adopting sustainability are as diverse as the people and groups upon which companies have an impact. First, there is the clear environmental argument. Governments alone cannot tackle growing environment risk and will need corporates to play their part through their strategies and business models.

The issues driving political leaders have also filtered down to investment managers who have developed deep concerns that companies should be building strategies that factor in environmental, social and governance (ESG) risk. Companies that ignore the issue risk failing to attract capital. A 2015 study by the global benchmarking organisation PRI (Principles for Responsible Investment), conducted with Deutsche Bank Asset Management, showed that among 2,200 studies undertaken since 1970, 63% found a positive link between a company’s ESG performance and financial performance.

There’s also the risk of being left behind, or self-inflicted damage. In an age of instant digital communication news travels fast and a company that fails on sustainability could quickly see stakeholder trust undermined.

Companies that embrace the topic can also create what might be termed “sustainability contagion”: businesses supplying “sustainable” clients must be sustainable themselves, generating a virtuous cascade of sustainability behaviour throughout the supply chain. That means positive results from implemented sustainability policies at one end of the chain, and pressure to comply at the other.

Leadership

But perhaps one of the biggest issues at the heart of the drive for sustainability is leadership. Implementing the right policies is undoubtedly a “top-down” process, not least because legal rulings have emphatically cast sustainability as a fiduciary duty. That makes executive involvement and leadership an imperative. However, involvement of management at the most senior level will also help instil the kind of culture change needed to make sustainability an ingrained part of an organization, and one that goes beyond mere compliance.

Leaders may feel the need to demonstrate the value of a sustainability step-change. This is needed because a full-blooded approach to sustainability could involve rethinking corporate structures, processes and performance measurement. Experts recognise three ways to demonstrate value: risk, reward and recognition.

“Risk” looks at issues such as potential dangers associated with ignoring sustainability such as loss of trust, reputational damage (as alluded to above), legal or regulatory action and fines.

A “rewards”-centred approach casts sustainability as an opportunity to be pursued, as long as policies boost revenues or cut costs, and stakeholders benefit.

Meanwhile, the “recognition” method argues that sharing credit for spreading sustainability policies promotes long-term engagement and responsibility.

Implementation

Getting sustainability policies off the ground can be tricky, particularly because of their multifaceted nature.

A recent study into European boards conducted by Board Agenda & Mazars in association with the INSEAD Corporate Governance Centre showed that while there is growing recognition by boards about the importance of sustainability, there is also evidence that they experience challenges about how to implement effective ESG strategies.

Proponents advise the use of “foundation exercises” for helping form the bedrock of sustainability policies. For example, assessing baseline environmental and social performance; analysing corporate management, accountability structures and IT systems; and an examination of material risk and opportunity.

That should provide the basis for policy development. Then comes implementation. This is not always easy, because being sustainable can never be attributed to a single policy. Future-proofing a company has to be an ongoing process underpinned by structures, measures and monitoring.

Policy delivery can be strengthened by the appointment of a chief sustainability officer (CSO) and establishing structures around the role, such as regular reporting to the chief executive and board, as well as the creation of a working committee to manage implementation of policies across the company.

Proponents advise the use of “foundation exercises” for helping form the bedrock of sustainability policies.

Sustainability values will need to be embedded at the heart of policies directing all business activities. And this can be supported through the use of an organisational chart mapping the key policies and processes to be adopted by each part of the business. The chart then becomes a critical ready reckoner for the boardroom and its assessment of progress.

But you can only manage what you measure, and sustainability policies demand the same treatment as any other business development initiative: key metrics accompanying the plan.

But what to measure? Examples include staff training, supply chain optimisation, energy efficiency, clean energy generation, reduced water waste, and community engagement, among many others.

Measuring then enables the creation of targets and these can be embedded in processes such as audits, supplier contracts and executive remuneration. If they are to have an impact, senior management must ensure the metrics have equal weight alongside more traditional measures.

All of this must be underpinned by effective reporting practices that provide a window on how sustainability practices function. And reporting is best supported by automated, straight-through processing, where possible.

Reliable reporting has the added benefit of allowing comparison and benchmarking with peers, if the data is available. The use of globally accepted standards—such as those provided by bodies like the Global Reporting Initiative—build confidence among stakeholders. And management must stay in touch, regularly consulting with the CSO and other stakeholders—customers, investors, suppliers and local communities—to ensure policies are felt in the right places.

Communication

Stakeholders should also hear about company successes, not just deliver feedback. Communicating a sustainability approach can form part of its longevity, as stakeholders hear the good news and develop an expectation of receiving more.

Companies are not expected to achieve all their sustainability goals tomorrow. Some necessarily take time. What is expected is long-term commitment and conviction, honest reporting and steady progress.

Care should be taken, however. Poor communication can be damaging, and a credible strategy will be required, one that considers how to deliver information frequently, honestly and credibly. It will need to take into account regulatory filings and disclosures, and potentially use social media as a means of reaching the right audience.

And that’s because successful sustainability policies are something to shout about. There is enormous pressure on companies to think differently, to reject a blinkered focus only on the bottom line and develop strategies that enable their companies to provide value, not only for shareholders but other stakeholders—society, customers, and suppliers—alike.

Companies are not expected to achieve all their sustainability goals tomorrow. Some necessarily take time. What is expected is long-term commitment and conviction, honest reporting and steady progress. The landscape on which businesses function is changing. They must change with it.

This article has been produced by Board Agenda in collaboration with Azeus Convene, a supporter of Board Agenda.

Je partage avec vous l’excellente prise de position de Martin Lipton *, Karessa L. Cain et Kathleen C. Iannone, associés de la firme Wachtell, Lipton, Rosen & Katz, spécialisée dans les fusions et acquisitions et dans les questions de gouvernance fiduciaire.

L’article présente un plaidoyer éloquent en faveur d’une gouvernance fiduciaire par un conseil d’administration qui doit non seulement considérer le point de vue des actionnaires, mais aussi des autres parties prenantes,

Depuis quelque temps, on assiste à des changements significatifs dans la compréhension du rôle des CA et dans l’interprétation que les administrateurs se font de la valeur de l’entreprise à long terme.

Récemment, le Business Roundtable a annoncé son engagement envers l’inclusion des parties prenantes dans le cadre de gouvernance fiduciaire des sociétés.

Among the developments followers of business ethics may have thought they’d never see, the end of the shareholder value myth has to rank very high.

Yet one of America’s leading business lobbying groups just buried the myth. “We share a fundamental commitment to all of our stakeholders,” reads a statement issued Monday by the Business Roundtable and signed by 181 CEOs. (Emphasis in the original.)

The statement mentions, in order, customers, employees, suppliers, communities and — dead last — shareholders. The corporate commitment to all these stakeholders may be largely rhetorical at the moment, but it’s hard to overstate what a reversal the statement represents from the business community’s preexisting viewpoint.

Stakeholders are pushing companies to wade into sensitive social and political issues — especially as they see governments failing to do so effectively.

Since the 1970s, the prevailing ethos of corporate management has been that a company’s prime responsibility — effectively, its only responsibility — is to serve its shareholders. Benefits for those other stakeholders follow, but they’re not the prime concern.

In the Business Roundtable’s view, the paramount duty of management and of boards of directors is to the corporation’s stockholders; the interests of other stakeholders are relevant as a derivative of the duty to stockholders,” the organization declared in 1997.

Bonne lecture. Vos commentaires sont les bienvenus !

JPMorgan Chase Chief Executive Jamie Dimon signed the business statement disavowing the shareholder value myth.(J. Scott Applewhite / Associated Press)

There has recently been much debate and some confusion about a bedrock principle of corporate law—namely, the essence of the board’s fiduciary duty, and particularly the extent to which the board can or should or must consider the interests of other stakeholders besides shareholders.

For several decades, there has been a prevailing assumption among many CEOs, directors, scholars, investors, asset managers and others that the sole purpose of corporations is to maximize value for shareholders and, accordingly, that corporate decision-makers should be very closely tethered to the views and preferences of shareholders. This has created an opportunity for corporate raiders, activist hedge funds and others with short-termist agendas, who do not hesitate to assert their preferences and are often the most vocal of shareholder constituents. And, even outside the context of shareholder activism, the relentless pressure to produce shareholder value has all too often tipped the scales in favor of near-term stock price gains at the expense of long-term sustainability.

In recent years, however, there has been a growing sense of urgency around issues such as economic inequality, climate change and socioeconomic upheaval as human capital has been displaced by technological disruption. As long-term investors and the asset managers who represent them have sought to embrace ESG principles and their role as stewards of corporations in pursuit of long-term value, notions of shareholder primacy are being challenged. Thus, earlier this week, the Business Roundtable announced its commitment to stakeholder corporate governance, and outside the U.S., legislative reforms in the U.K. and Europe have expressly incorporated consideration of other stakeholder interests in the fiduciary duty framework. The Council of Institutional Investors and others, however, have challenged the wisdom and legality of stakeholder corporate governance.

To be clear, Delaware law does not enshrine a principle of shareholder primacy or preclude a board of directors from considering the interests of other stakeholders. Nor does the law of any other state. Although much attention has been given to the Revlon doctrine, which suggests that the board must attempt to achieve the highest value reasonably available to shareholders, that doctrine is narrowly limited to situations where the board has determined to sell control of the company and either all or a preponderant percentage of the consideration being paid is cash or the transaction will result in a controlling shareholder. Indeed, theRevlon doctrine has played an outsized role in fiduciary duty jurisprudence not because it articulates the ultimate nature and objective of the board’s fiduciary duty, but rather because most fiduciary duty litigation arises in the context of mergers or other extraordinary transactions where heightened standards of judicial review are applicable. In addition, Revlon’s emphasis on maximizing short-term shareholder value has served as a convenient touchstone for advocates of shareholder primacy and has accordingly been used as a talking point to shape assumptions about fiduciary duties even outside the sale-of-control context, a result that was not intended. Around the same time that Revlon was decided, the Delaware Supreme Court also decided the Unocal and Household cases, which affirmed the board’s ability to consider all stakeholders in using a poison pill to defend against a takeover—clearly confining Revlonto sale-of-control situations.

The fiduciary duty of the board is to promote the value of the corporation. In fulfilling that duty, directors must exercise their business judgment in considering and reconciling the interests of various stakeholders—including shareholders, employees, customers, suppliers, the environment and communities—and the attendant risks and opportunities for the corporation.

Indeed, the board’s ability to consider other stakeholder interests is not only uncontroversial—it is a matter of basic common sense and a fundamental component of both risk management and strategic planning. Corporations today must navigate a host of challenges to compete and succeed in a rapidly changing environment—for example, as climate change increases weather-related risks to production facilities or real property investments, or as employee training becomes critical to navigate rapidly evolving technology platforms. A board and management team that is myopically focused on stock price and other discernible benchmarks of shareholder value, without also taking a broader, more holistic view of the corporation and its longer-term strategy, sustainability and risk profile, is doing a disservice not only to employees, customers and other impacted stakeholders but also to shareholders and the corporation as a whole.

The board’s role in performing this balancing function is a central premise of the corporate structure. The board is empowered to serve as the arbiter of competing considerations, whereas shareholders have relatively limited voting rights and, in many instances, it is up to the board to decide whether a matter should be submitted for shareholder approval (for example, charter amendments and merger agreements). Moreover, in performing this balancing function, the board is protected by the business judgment rule and will not be second-guessed for embracing ESG principles or other stakeholder interests in order to enhance the long-term value of the corporation. Nor is there any debate about whether the board has the legal authority to reject an activist’s demand for short-term financial engineering on the grounds that the board, in its business judgment, has determined to pursue a strategy to create sustainable long-term value.

And yet even if, as a doctrinal matter, shareholder primacy does not define the contours of the board’s fiduciary duties so as to preclude consideration of other stakeholders, the practical reality is that the board’s ability to embrace ESG principles and sustainable investment strategies depends on the support of long-term investors and asset managers. Shareholders are the only corporate stakeholders who have the right to elect directors, and in contrast to courts, they do not decline to second-guess the business judgment of boards. Furthermore, a number of changes over the last several decades—including the remarkable consolidation of economic and voting power among a relatively small number of asset managers, as well as legal and “best practice” reforms—have strengthened the ability of shareholders to influence corporate decision-making.

To this end, we have proposed The New Paradigm, which conceives of corporate governance as a partnership among corporations, shareholders and other stakeholders to resist short-termism and embrace ESG principles in order to create sustainable, long-term value. See our paper, It’s Time to Adopt The New Paradigm.