La firme-conseil ISS, (Institutional Shareholder Services) publie chaque année une étude de l’évolution des pratiques de gouvernance aux É.U. (Board Practices Study).

Rob Yates, vice-président d’ISS, est l’auteur de cet article paru sur le site de Harvard Law School Forum on Corporate Governance. Il y aborde cinq tendances majeures.

Les investisseurs continuent d’exercer des pressions sur les administrateurs du conseil, entre autres en continuant de demander d’inclure de nouvelles candidatures dans la circulaire de procuration.

On constate que les pratiques généralement reconnues de bonne gouvernance sont adoptées dans presque toutes les grandes sociétés ; elles sont de plus en plus acceptées dans les plus petites entreprises. On fait ici référence aux élections annuelles, au vote majoritaire et à l’élimination des pilules empoisonnées.

La question du choix d’un président du conseil totalement indépendant et différent du CEO semble être moins problématique si la société fait appel à président désigné (lead director) indépendant et fort.

La rémunération des administrateurs de sociétés a continué de croître significativement. Les CA évaluent différentes approches à la compensation des administrateurs. Ainsi, on élimine de plus en plus les jetons de présence pour les réunions et les conférences téléphoniques. La rémunération des administrateurs s’est accrue de 17 % de 2012 à 2016 tandis que celle des PDG a augmenté de 10 % pendant la même période.

ISS a produit plusieurs études sur les tendances en matière de limite des mandats (tenure), du renouvellement des administrateurs du CA et de l’importance de la diversité. Si le sujet vous intéresse, l’auteur vous réfère à plusieurs études américaines et mondiales.

This year’s Board Practices Study focuses not only on longstanding issues traditionally covered, but on those which have driven increased shareholder interest in the boardroom over the past several years. Governance continues to evolve, but investor focus in recent years has been particularly pointed as new concerns have emerged, and the ways in which companies address those concerns adapts to meet market demands. Particular focus has been placed on the role of the board as a representative of shareholders at a company, and how the board’s structure and practices promulgate this responsibility. As always, this study provides a snapshot of these facets of public company boards in the S&P 1500 for investors and issuers to compare and contrast.

Investors are continuing to push for board accountability

The pyroclastic spread of proxy access over the past two years has arguably been the most prominent governance story in the United States. In two short years, the S&P went from having only a handful of companies with proxy access, to having over half its constituents offering shareholders the right. Proxy access is also starting to show up in shareholder proposals at smaller firms; as of March 14, ISS is tracking a dozen such proposals at S&P 400 companies.

Advisory Board Best Practices: Roles and Advice

Proxy access is the most recent chapter in the much longer story of shareholders seeking board accountability. The next chapters are underway, with investors focusing on board self-regulation practices and measures, such as director tenure and board refreshment, board diversity, board evaluations, mandatory retirement ages, and more. Some of these are showing promise—such as board refreshment and continuing progress on gender diversity—while others are lagging, such as non-gender measures of board diversity.

Central to these concerns is shareholders’ desire that boards develop the skills, expertise, awareness, and experience to accurately assess and effectively manage emerging risks, such as cyber and environmental risks, and ensure that boards are constantly searching for weaknesses (and, when and where appropriate, soliciting external help to identify blind spots).

Traditional concerns still exist, but companies are making progress

More traditional approaches to increasing accountability, such as majority vote standards and annual elections in the director election process—features that are near-ubiquitous in the largest companies—have been adopted in greater frequency by smaller companies. Many problematic governance practices, such as poison pills, are also increasingly rare.

Investors are more accepting of alternative independent board leadership structures

Demonstrating that governance is both a give and take endeavor, investors are more accepting of alternative forms of independent board leadership. Whereas investors have historically favored independent chairs, many are increasingly comfortable with an alternative structure whereby a strong and empowered lead independent director counterbalances a combined chair/CEO.

Director compensation increased sharply

A new feature in this year’s study is an evaluation of director pay covering the preceding five years. While compensation disclosure for non-employee directors is not new itself, the rules and guidelines governing director pay disclosure have only recently standardized. Beginning in December 2006, SEC rules required the disclosure of director pay in a standardized table format. This disclosure increased transparency and comparability between companies. Additionally, both the NYSE and NASDAQ require that boards consider director pay when determining director independence for purposes of meeting listing requirements.

Director compensation has received increased scrutiny in recent years, particularly given rising pay levels and high-profile shareholder lawsuits alleging excessive pay. Amid this atmosphere, many companies have taken a proactive approach to director compensation programs, mainly through altering equity plans or, in a few rare instances, introducing ballot items.

As companies weigh the potential benefits of changing director pay structures, median pay continues to rise. In fact, non-employee director compensation grew 17 percent between 2012 and 2016, while median CEO pay in the S&P 500 (reported in ISS’ 2016 US Compensation Postseason Report) rose by less than 10 percent. One positive development is the streamlining observed among director compensation programs. For example, the elimination of meeting and telephonic meeting fees in many compensation structures.

Increased scrutiny of certain board practices has necessitated a more detailed review

Previous versions of the board study included an in-depth snapshot of new-director demographics and trends, such as tenure, refreshment, and diversity. As these components of board composition have become a significant part of the governance conversation, ISS has produced in-depth studies on each of these issues.

*Rob Yates is Vice President at Institutional Shareholder Services, Inc. This post is based on an ISS publication by Mr. Yates, Rachel Hedrick, and Andrew Borek.

Aujourd’hui, je ne peux passer sous silence la petite histoire de l’évolution de la pensée en gouvernance publiée par Lawrence Cunningham, professeur à la George Washington University Law School.

Ce court article a été publié sur le site du HLS Forum. Il décrit les grands courants de pensée et met l’accent sur les publications des bonzes universitaires américains.

Je suis assuré que cette brève chronologie des événements, à compter de 1976, vous donnera une vue d’ensemble utile de l’évolution de la discipline.

Bonne lecture !

The Ivory Tower on Corporate Governance

In 1976, [Directors & Boards]’s founding year, two influential academic works in corporate governance appeared: Berkeley law professor Melvin Eisenberg urged transforming the board from an advisory role to a monitoring model and mandating significant internal control systems, while University of Rochester economists Michael Jensen and William Meckling portrayed the firm as a nexus of contracts whose optimal design is for participants to choose.

These contrasting visions—obligatory uniformity versus free tailoring—have defined the field since, setting the boundaries of debate and helping participants think through positions. Into the early 1980s, the Eisenberg view dominated, with Columbia University law professor William Cary urging preemptive federal oversight of the field, traditionally handled by state law, and a generally pro-regulatory atmosphere imposing fiduciary mandates on independent directors and board committees.

But the nexus of contracts school soon ascended to greater influence, through the 1990s, after law professors such as Frank Easterbrook (now a judge) and Daniel Fischel, both of the University of Chicago, explored how the separation of ownership from control is a problem of agency costs, best addressed by contractual devices geared to maximizing shareholder value. Rather than federal mandates, states should experiment to offer a menu of tools for different corporations to tailor. Yale University law professor (also now judge) Ralph Winter theorized that competition among states for corporate charters constrained managers to promote shareholder interests.

While normative corporate governance scholarship has divided between the pro- and anti-regulatory camps of the 1970s and 1980s, the best academics learned from their intellectual opponents to refine stances and often forge consensus. For example, though assessments of the deal decade’s disruptive takeovers and comparative studies of non-U.S. practice found a place for non-shareholder constituents in corporate governance, a shareholder primacy norm nevertheless took root.

Even as both schools of thought contributed to the discourse, each had their heyday when current events cut in their favor. So the 1990s boom was a time of great enthusiasm for the economic approach, adding a productive trend of increasingly sophisticated empirical research, including on the value of state competition in corporate law. After the burst, however, and as widespread accounting fraud was revealed, scholars cited Eisenberg to diagnose failures to monitor and control—and prescribed cures found in the Sarbanes-Oxley Act (SOX). An industry-specific version of the dynamic transpired after the financial crisis, culminating in the Dodd-Frank Act.

In each case, scholarship was diverse, as pragmatic centrist resolution of pending challenges, exemplified by Columbia’s John Coffee, contended with cries on both normative sides of either too little or too much regulation (Yale’s Roberta Romano called SOX “quack governance”). Such episodes updated the Cary-Winter debate: full-scale federal preemption is probably dead but, as Harvard University law professor Mark Roe explained, less due to state competition than the threat to states of incremental federal incursion, a la SOX and Dodd-Frank.

Since 1976, scholars have helped shift power from managers to owners, especially institutional investors. Today, scholars such as Harvard Law professor Lucian Bebchuk urge continued expansion of shareholder power, while others, like UCLA law professor Stephen Bainbridge, observe and support a propensity toward director primacy instead. In the balance is the fate of shareholder activism, which though novel in some ways, at bottom raises issues debated for 40 years, particularly agency cost mitigation. Plus ça change, plus c’est la même chose.

C’est avec plaisir que je partage l’information et l’invitation à un important colloque intitulé « Gouvernance et performance : une perspective internationale » qui aura lieu à l’Université McGill les 11 et 12 mai 2017.

C’est mon collègue, le professeur Félix ZOGNING NGUIMEYA, Ph.D., Adm.A., qui est le responsable de l’organisation de ce colloque en gouvernance à l’échelle internationale.

À la lecture du programme, vous constaterez que les organisateurs n’ont ménagé aucun effort pour apporter un éclairage très large de ce phénomène.

Ce colloque traite des récents développements et des sujets émergents en matière de gouvernance. La gouvernance, comme thématique transversale, est abordée dans tous ses aspects : gouvernance d’entreprise, gouvernance économique, gouvernance publique, en lien avec la création de valeur ou la performance des organisations, des politiques ou des programmes concernés. Dans chacun des contextes, les travaux souligneront l’effet des mécanismes de gouvernance sur la performance des organisations, institutions ou collectivités.

La perspective internationale du colloque a pour but d’examiner les modèles et structures de gouvernance présents dans différents pays et dans les différentes organisations, selon que ces modèles dépendent fortement du système juridique, du modèle économique et social, ainsi que le poids relatif des différentes parties prenantes. Les contributions sont donc attendues des chercheurs et professionnels de plusieurs champs disciplinaires, notamment les sciences économiques, les sciences juridiques, les sciences politiques, la comptabilité, la finance, l’administration et la stratégie.

Jacques Bertrand

Marie Marchand

Sabrina Khemiri

Catherine Peyroux

Isabelle Bories-Azeau

Fatiha Fort

Florence Noguera

Alex Gildas Kengni Fomo

Samuel Mbiagzi Ndjeudji

Adja Hamida

Sabine Patricia Moungou Mbenda

Ahmadou Aly Mbaye

Fatou Gueye

Ndiack Fall

Ibrahim Barry

Mathias Marie Adrien Ndinga

Ahmed Belfahmi

Adam Elage

Arnaud Boris Bologo Bologo

12:00 – 13:00

Lunch

13:00 – 14:00

Table ronde :

La gouvernance, entre surveillance et création de valeur

Animée par Lisane Dostie, ISA Légal & Gouvernance

Pascal Bayl Balata, Conseil du Trésor du Canada

Danny Purcell, Hôpital Monfort

Mario Malouin, Université du Québec en Outaouais

Emmanuelle Létourneau, Gouvernance Entreprenante

14:00 – 17:00

Gouvernance, conseil d’administration et création de valeur

Session présidée par :

Jacques Bertrand – Université du Québec à Trois-Rivières

Mario Malouin

Steeve Massicotte

Jean-François Henri

Marie Elisabeth Dicko Dembélé

Patrick Perras

Rachid Boutti

Florence Rodhain

Isabelle Bourdon

Adil El Amri

André Dumas Tsambou

Benjamin Alain Fomba Kamga

14:00 – 17:00

Transparence, systèmes d’information et technologie de l’information

Session parallèle présidée par :

Florence Noguera – Université Paul Valery Montpellier 3

Selon un communiqué de l’Agence France Presse, publié le 7 avril 2017 dans le Journal de Montréal, « le fonds souverain de la Norvège, le plus gros au monde, a peaufiné vendredi son image d’investisseur responsable en réclamant un plafonnement de la rémunération des patrons et la transparence fiscale des entreprises ».

Bonne lecture !

Le fonds souverain de la Norvège, le plus gros au monde, a peaufiné vendredi son image d’investisseur responsable en réclamant un plafonnement de la rémunération des patrons et la transparence fiscale des entreprises

Dans chaque entreprise, le « conseil d’administration devrait (…) dévoiler un plafond pour la rémunération totale » du directeur général « pour l’année à venir », estime la banque centrale norvégienne, chargée de gérer le fonds, dans un nouveau « document de position ».

À une époque où les très gros salaires décollent, cette prise de position est d’autant plus importante que le fonds est présent au capital de quelque 9 000 entreprises à travers le monde, représentant 1,3 % de la capitalisation globale.

Par son poids et par sa gestion généralement jugée exemplaire en matière de transparence et d’éthique, le mastodonte scandinave donne souvent le « pas » pour d’autres investisseurs.

« C’est une très bonne nouvelle », s’est réjouie Manon Aubry, porte-parole d’Oxfam France. « Il s’agit d’un levier qui peut avoir un impact important sur le comportement des entreprises », a-t-elle expliqué à l’AFP, soulignant que le fonds norvégien n’était pas le seul à avoir pris ce genre de décision.

La contestation a un effet, parfois. Le directeur général du géant pétrolier britannique BP, Bob Dudley, a ainsi vu sa rémunération diminuer de 40 % en 2016, un an après un vote des actionnaires contre une hausse de son salaire, uniquement consultatif, mais offrant un désaveu cinglant.

Sous la pression de la classe politique et des syndicats, six hauts dirigeants de Bombardier ont accepté dimanche au Canada de réduire de moitié l’augmentation de 50 % initialement promise. Volkswagen a aussi décidé le mois dernier de plafonner les salaires pour les membres de son conseil d’administration, une question souvent débattue en Allemagne.

«Say on pay»

Le principe du « say on pay » vient par ailleurs d’entrer pour la première fois dans le droit français. Le vote des actionnaires en assemblée générale sur la rémunération des dirigeants est désormais contraignant grâce à la loi « Sapin 2 », dont le décret d’application a été publié en mars.

En 2016, la rémunération des dirigeants de trois entreprises, dont Carlos Ghosn chez Renault et Patrick Kron chez Alstom, avait été rejetée par les actionnaires. Mais ces avis, alors purement consultatifs, n’avaient pas été pris en compte par les conseils d’administration.

Longtemps peu regardant en la matière, le fonds norvégien s’implique de plus en plus dans la gouvernance des entreprises dont il est actionnaire. Il a par exemple voté l’an dernier contre la politique de rémunération des dirigeants d’Alphabet (Google), Goldman Sachs, JPMorgan ou encore Sanofi, selon le Financial Times.

« Nous ne sommes plus en position, en tant qu’investisseur, de dire que c’est une question sur laquelle on n’a pas d’avis », a déclaré au FT le patron du fonds, Yngve Slyngstad, en notant que le « say on pay » se répandait dans toujours plus de pays.

Jugeant que cela contribuerait à aligner les intérêts du patron sur ceux des actionnaires, le nouveau document prône aussi pour qu’« une part significative de la rémunération totale annuelle (soit) fournie en actions bloquées pour au moins cinq ans, et de préférence dix ans, indépendamment d’une démission ou d’un départ en retraite » et sans condition de performances.

Non à l’optimisation fiscale

Dans un autre document publié vendredi, la Banque de Norvège a aussi exigé la transparence fiscale de la part des entreprises.

« Les impôts devraient être payés là où la valeur économique est générée », souligne-t-elle notamment, visiblement hostile à l’optimisation fiscale, technique légale qui consiste à déplacer les bénéfices là où l’imposition est moindre.

Sur le Vieux Continent, des géants comme Apple, Starbucks ou Fiat ont eu ces dernières années maille à partir avec la Commission européenne pour avoir tiré parti d’avantages fiscaux indus.

Le fonds norvégien conforte ainsi son image d’investisseur responsable.

Conformément à un vote du Parlement en 2015, le fonds — alimenté, paradoxalement, par les revenus pétroliers de l’État — se refuse à investir dans les entreprises, compagnies minières ou énergéticiens, où le charbon, néfaste pour le climat, représente plus de 30 % de l’activité.

Il n’est pas non plus autorisé à investir dans les entreprises coupables de violations graves des droits de l’Homme, dans celles qui fabriquent des armes nucléaires ou « particulièrement inhumaines » ou encore dans les producteurs de tabac.

L’un des plus grands changements au cours des dix dernières années dans la gouvernance des entreprises est l’engagement accru des actionnaires et des investisseurs institutionnels dans les affaires de l’organisation. Cela se manifeste concrètement par des interventions activistes mal anticipées.

L’article ci-dessous est un bijou de réalisme et de pragmatisme eu égard au diagnostic de la situation de l’engagement des actionnaires ainsi qu’aux moyens à la disposition des entreprises pour favoriser le dialogue avec les grands actionnaires-investisseurs.

L’auteur propose six moyens à prendre en compte par l’entreprise afin d’assurer une meilleure communication avec les intéressés…

Les dirigeants d’entreprises ainsi que les présidents des conseils d’administration devraient prendre bonne note des suggestions présentées dans cet article.

Ils ont tout avantage à être proactif afin d’éviter les mauvaises surprises et les contestations susceptibles d’émerger de la part de groupes d’actionnaires mécontents ou opportunistes.

Bonne lecture ! Vos commentaires sont les bienvenus.

In today’s environment, companies cannot wait for a pressing issue to engage with their shareholders. By the time the issue becomes public because an activist has shown up or some other concern has emerged that affects the stock, it is often too late to have a productive conversation

The significant rise of activism over the last decade has sharpened the focus on shareholder engagement in boardrooms and executive suites across the US.

Once considered a perfunctory exercise, designed to simply answer routine questions on performance or, occasionally, drum up support for a corporate initiative, shareholder engagement has become a strategic imperative for astute executives and board members who are no longer willing to wait until the annual meeting to learn that their shareholders may not support change of some sort, or their strategic direction overall.

When active shareholder engagement works, it leads to a productive dialogue with the voters—the governance departments established by the big institutional firms, which typically oversee proxy voting. It is important to remember the reality of public company ownership. The vast majority of public companies have shareholder bases dominated by a diverse set of large, institutional funds. Engagement with these voters not only helps head off potential problems and activists down the road, but it also gives management valuable insight into how patient and supportive their shareholder base is willing to be as they implement strategies designed to generate long-term growth. Indeed, the rising level of engagement is a positive trend that could, over time, help mitigate the threat of activism if properly managed.

This all sounds encouraging in theory and, in some cases, it works in practice as well. But the simple fact remains that this kind of dialogue is unobtainable for the vast majority of public companies, despite the best of intentions on both sides.

Struggles with Engagement

Even the largest institutional investors, many of whom are voting well in excess of 10,000 proxies a year, have at most 25-30 people in their governance departments able to engage directly with companies. Those teams do yeoman’s work to meet demands, taking several hundred and in some cases well more than 1,000 meetings with company executives or board members a year. But with more issues on corporate ballots than ever before that need to be researched and analysed, companies are finding it increasingly hard to get an audience with proxy voters even when a determination is made to more proactively engage. This can be true for even large companies with market capitalisations in the billions.

Indeed, for small-cap companies, the idea is almost always a non-starter, though there are workarounds. Some institutional funds are willing

to use roundtable discussions with several issuers at once to cover macro topics. Most mid-cap companies are out of luck as well, unless they are able to make a compelling case around a particular issue that catches a governance committee’s eye (more on that in a minute). Large-cap companies certainly meet the size threshold, but even they need to be smart in making the request. The net result is a conundrum at companies that are willing to engage but find their institutional investors less willing to do so, or are stretched too thin to make it happen.

The problem is a difficult one to solve. In today’s environment, companies cannot wait for a pressing issue to engage with their shareholders. By the time the issue becomes public because an activist has shown up or some other concern has emerged that affects the stock, it is often too late to have a productive conversation. Investors in those situations must decide what they know or can learn in a condensed period; they have little ability to become invested in the long-term thinking behind, for instance, a company’s change to executive pay or corporate governance. At the same time, institutional investors, while very open to and, in many cases, strong advocates for meeting with executives, cannot always handle the number of requests they receive, particularly when the requests come in during a condensed period. This has led some investors to establish requirements around which companies ‘qualify’ for a meeting, leaving some executives that don’t meet the thresholds frustrated that they can’t get an audience. Both sides are striving to improve the process in this rapidly evolving dynamic. The fact is that both sides have a lot of room for improvement. Here are a few guidelines we advise companies to use when deciding how or even if they should more proactively engage with their largest investors.

In today’s environment, companies cannot wait for a pressing issue to engage with their shareholders. By the time the issue becomes public because an activist has shown up or some other concern has emerged that affects the stock, it is often too late to have a productive conversation

1. If a meeting is unlikely, make your case in other ways

Just because you can’t get a meeting does not mean you can’t effectively influence how your investors vote on an issue. Most companies today fall well short in communicating effectively with the megaphones they do control—namely, the financial reports that are distributed to all shareholders. When a governance committee sits down to review an issue, the first thing it does is pull out the proxy. Yet most companies bury the most compelling arguments under mountains of legalese or financial jargon that is off-message or confusing. In today’s modern era, proxies need to tell an easily digestible story from start to finish. They need to be short, compelling and to the point.

Figure out the three to four things you need your investors to understand and put it right up front in the proxy in clear, compelling language. Be concise and to the point. Remove unnecessary background and encourage questions. Add clear graphic elements to illustrate the most important points. And be sure not to contradict yourself with a myriad of financial charts and footnotes, or provide inconsistent information with what you’ve said before. The proxy statement is the most powerful disclosure tool companies have, yet most are produced by disparate committees, piecing the behemoth filing together with little recognition of the overall document coming to life.

2. Know when to make contact

Most large, institutional shareholders and even some mid-sized ones, are open to meeting with management and/or board members under certain circumstances, but timing is key. Go see your investors on a “clear day”when a meaningful discussion on results and strategy can be had without the overhang of activist demands. For most companies, this means making contact during the summer and fall months after their annual meeting and when the filing window opens for the next year’s proxy.

Institutional investors do lots of meetings during proxy season as well, but those tend to focus on whatever issues have emerged in the proxy, or even worse, whatever demands an activist is making. If you believe you are vulnerable to an activist position, address that concern before it becomes an issue with the right combination of people who will ultimately vote the shares.

3. Know who to talk to

The hardest part of this equation for most companies is figuring out who the right person is at the funds for these conversations. Is it the portfolio manager (PM) who follows the company daily and typically has the most robust relationship with the company’s investor relations department? Is it the governance department that may have more sway over voting the shares? The answer is likely some combination of both. Each institution has its own process for making proxy voting decisions.

In many cases, it involves input from the portfolio manager, internal analyst and the governance department, as well as perhaps some influence from proxy advisory firms, such as ISS or Glass Lewis. But the ultimate decision-maker is always somewhere in that mix. The trick is to find out where. Start with the contacts you know best, but don’t settle for one relationship. If you don’t know your portfolio manager and governance analyst, then you are not going to get a complete picture on where you stand. In many cases, the PM can be a helpful advocate in having a governance analyst understand why certain results or decisions make sense. Once you find the right mix of people, selling the story will be much easier.

4. Don’t assume passive investors are passive

Today, many so-called passive investors are anything but. One passive investor told me his firm held more than 200 meetings with corporations last year.

A governance head at another institution said there is little difference today in how the firm evaluated proxy questions between its active and passive holdings. You may not always get an audience, but on important matters, treat your passive investors like anyone else. You may be surprised at how active they are. These firms also tend to be the busiest, so be assertive and creative in building a relationship. The front door may not be the only option.

5. Choose the best Messenger

There is an interesting debate going on in the governance community right now about how involved CEOs and board members should be in shareholder discussions. As a rule, we view it this way: routine conversations around results and performance can be handled by investor relations (IR). More sophisticated financial questions get elevated to CFOs. Once the conversations delve into strategy and growth plans, CEOs should be involved, but usually only with the largest current or potential shareholders. And, finally, when it comes to matters of governance policy, consider having a board member involved.

Board engagement with shareholders is a relatively new trend, but an important one. Investors are often reassured when they see and hear from an engaged board and many will confess that those meetings can change their thinking. But having the right board member who can handle those conversations and be credible is key. A former CEO, who is used to shareholder interactions, or a savvy lead independent director can fit the bill.

But with investors increasingly asking for—and indeed many boards starting to offer—meetings with directors, every board should be evaluating who that representative will be if the opportunity comes along.

6. Be prepared and walk in with a clear set of goals

Too often, companies spend too much time just trying to determine what not to say in meetings with investors and not nearly enough time working on what they want to communicate. This mistake leads to frustration and missed opportunities, not to mention a reduced likelihood that it can get an audience again.

Every investor meeting is an opportunity to better refine or explain your corporate growth story. Walk into every meeting with clear goals in mind. Better yet, get the investor to articulate their own agenda as well. Know exactly what each of you wants to get out of the meeting and then get down to business. Be upfront and honest about why you are requesting the meeting. Governance investors are far more engaged when companies walk in with stated goals in mind. Surface potential problems and your solution to them, before they emerge.

Making the effort

Even with this level of planning, large companies can still find their requests for engagement on governance topics unheeded. Many of the large, institutional investors have installed various thresholds, generally predicated to a company’s size, that companies need to meet to receive an audience. But that does not mean companies should give up. Continue to work the contacts you do have within each institution. Tell your best story in routine discussions, such as earnings calls or conference presentations. Those are too often missed opportunities. Look for other opportunities to get in front of investors.

Conferences can be great forums, as can organisations, such as the Society of Corporate Governance, Council for Institutional Investors or National Association of Corporate Directors. Every time you communicate externally, it is a chance to tell your story and make the right disclosures. History is littered with companies that waited too long to do so, came under attack and lost control of their own destiny. Don’t waste any opportunity to make your best case to whomever is listening.

Voici la version 4.0 du document australien de KPMG, très bien conçu, qui répond clairement aux questions que tous les administrateurs de sociétés se posent dans le cours de leurs mandats.

Même si la publication est dédiée à l’auditoire australien de KPMG, je crois que la réalité réglementaire nord-américaine est trop semblable pour se priver d’un bon « kit » d’outils qui peut aider à constituer un Board efficace.

C’est un formidable document électronique interactif. Voyez la table des matières ci-dessous.

J’ai demandé à KPMG de me procurer une version française du même document, mais il ne semble pas en exister.

Now in its fourth edition, this comprehensive guide is in a user friendly electronic format. It is designed to assist directors to more effectively discharge their duties and improve board performance and decision-making.

Key topics

Duties and responsibilities of a director

Oversight of strategy and governance

Managing shareholder and stakeholder expectations

Structuring an effective board and sub-committees

Enabling key executive appointments

Managing productive meetings

Better practice terms of reference, charters and agendas

Establishing new boards.

What’s new in 2017

In this latest version, we have included newly updated sections on:

managing cybersecurity risks

human rights in the supply chain.

Register

Register here for your free copy of the Directors’ Toolkit.

Selon le modèle de gouvernance des entreprises privées canadiennes et américaines, le PDG (CEO) relève du conseil d’administration (CA) de l’entreprise. En effet, ce sont les actionnaires qui, lors de l’assemblée générale annuelle (AGA), votent pour des administrateurs dont la responsabilité fiduciaire est de les représenter sur le conseil d’administration de l’entreprise.

Ainsi, lors des AGA des entreprises publiques (cotées en bourse), les actionnaires sont appelés à voter sur une recommandation du CA développée par le comité de gouvernance. Il existe également des règles qui permettent aux actionnaires de faire inscrire des candidats sur la liste présentée par le CA.

Michael Sabia, PDG de la Caisse de dépôt et placement et Robert Tessier, président du conseil d’administration

Le CA a la responsabilité de veiller aux intérêts supérieurs des actionnaires tout en considérant les intérêts des diverses parties prenantes.

Les actionnaires ne votent pas pour un PDG (CEO) ; ils votent pour des représentants en qui ils ont confiance dans la supervision de leurs affaires, notamment dans le choix du premier dirigeant (PDG – CEO).

Il est clair pour tous que c’est le CA qui a la responsabilité d’embaucher le PDG (CEO), de l’orienter, de le rémunérer, de l’évaluer et de mettre en place un processus de relève et de transition.

Personnellement, je ne crois pas approprié que le PDG soit aussi un administrateur au sein du CA, bien qu’il doive y assister à titre de premier dirigeant, mais sans droit de vote.

Cette prise de position implique, a fortiori, que le PDG ne soit pas désigné comme président (Chairman of the Board) du CA.

Bien que notre mode de gouvernance semble exclure le cumul des fonctions de président du conseil et de PDG, il n’existe aucune obligation juridique à le faire.

En fait, on suppose que la séparation des fonctions, entre la présidence du conseil et la présidence de l’entreprise (CEO), est généralement bénéfique à l’exercice de la responsabilité de fiduciaire des administrateurs, c’est-à-dire que des pouvoirs distincts permettent d’éviter les conflits d’intérêts, tout en rassurant les actionnaires.

Cependant, cette pratique cède trop souvent sa place à la volonté bien arrêtée de plusieurs PDG d’exercer le pouvoir absolu, comme c’est encore le cas pour plusieurs entreprises américaines.

Le Canadian Spencer Stuart Board Index estime qu’une majorité de 85 % des 100 plus grandes entreprises canadiennes cotées en bourse a opté pour la dissociation entre les deux fonctions.

Aux États-Unis, en 2013, 45 % des entreprises de l’indice S&P500 dissociaient les rôles de PDG et de président du conseil. Plus de 50 % de ces entreprises combinent les deux fonctions !

L’article d’Yvan Allaire, publié dans le journal Les Affaires du 21 novembre 2016, mentionne « deux arguments invoqués pour appuyer la séparation des rôles » :

1- Le PDG relève du conseil qui doit en évaluer la performance, établir sa rémunération, le remplacer si cette performance est inadéquate, proposer de nouveaux membres pour le conseil ; comment peut-on, comme PDG, présider également le conseil, lequel doit prendre ces décisions critiques pour le PDG ;

Environ 50 % des grandes sociétés américaines sont présidées par un administrateur indépendant, comparativement à 23 % il y a 15 ans.

Toute la question du bien-fondé de la dualité des rôles PDG/Chairman est encore ambiguë, même si les experts de la gouvernance et les actionnaires activistes sont généralement d’accord avec la séparation des fonctions.

2- En notre époque alors que la gouvernance est plus exigeante, plus prenante de temps et d’énergie pour la société ouverte cotée en Bourse, comment une même personne peut-elle s’acquitter de ces deux rôles sans que l’un soit négligé au profit de l’autre ? Dans le nouveau contexte de gouvernance, postérieur à Sarbanes-Oxley, les exigences pour le PCA sont telles qu’il n’est pas souhaitable qu’une même personne assume ces deux fonctions (PCA et PDG).

En conséquence, 85 % des 100 plus grandes entreprises canadiennes cotées en Bourse se sont donné un président du conseil distinct du PDG, mais dans 38 % des cas ce président du conseil ne se qualifiait pas comme indépendant. (Spencer Stuart, février 2012).

La situation n’est certainement pas limpide, mais la tendance est évidente. L’indépendance du président du conseil ainsi que la séparation du pouvoir entre Chairperson du CA et CEO devrait, selon moi, trouver son application dans tous les types d’organisations : OBNL, sociétés d’État, petites et moyennes entreprises, et coopératives.

Évidemment, chaque organisation a ses particularités, lesquelles sont ancrées dans des pratiques de gouvernance assez diverses. La séparation des rôles n’est pas une panacée; c’est une meilleure assurance d’une saine gouvernance.

Aujourd’hui, je partage avec vous la liste des dix thèmes majeurs en gouvernance que les auteurs Kerry E. Berchem* et Rick L. Burdick* ont identifiés pour l’année 2017.

Vous êtes assurément au fait de la plupart de ces dimensions, mais il faut noter l’importance accrue à porter aux questions stratégiques, aux changements politiques, aux relations avec les actionnaires, à la cybersécurité, aux nouvelles réglementations de la SEC, à la composition du CA, à l’établissement de la rémunération et aux répercussions possibles des changements climatiques.

Afin de mieux connaître l’ampleur de ces priorités de gouvernance pour les administrateurs de sociétés, je vous invite à lire l’ensemble du rapport publié par Akin Gump.

1. Corporate strategy: Oversee the development of the corporate strategy in an increasingly uncertain and volatile world economy with new and more complex risks

Directors will need to continue to focus on strategic planning, especially in light of significant anticipated changes in U.S. government policies, continued international upheaval, the need for productive shareholder relations, potential changes in interest rates, uncertainty in commodity prices and cybersecurity risks, among other factors.

2. Political changes: Monitor the impact of major political changes, including the U.S. presidential and congressional elections and Brexit

Many uncertainties remain about how the incoming Trump administration will govern, but President-elect Trump has stated that he will pursue vast changes in diverse regulatory sectors, including international trade, health care, energy and the environment. These changes are likely to reshape the legal landscape in which companies conduct their business, both in the United States and abroad.

With respect to Brexit, although it is clear that the United Kingdom will, very probably, leave the European Union, there is no certainty as to when exactly this will happen or what the U.K.’s future relationship, if any, with the EU will be. Once the negotiations begin, boards will need to be quick to assess the likely shape of any deal between the U.K. and the EU and to consider how to adjust their business model to mitigate the threats and take advantage of the opportunities that may present themselves.

3. Shareholder relations: Foster shareholder relations and assess company vulnerabilities to prepare for activist involvement

The current environment demands that directors of public companies remain mindful of shareholder relations and company vulnerabilities by proactively engaging with shareholders, addressing shareholder concerns and performing a self-diagnostic analysis. Directors need to understand their company’s vulnerabilities, such as a de-staggered board or the lack of access to a poison pill, and be mindful of them in any engagement or negotiation process.

4. Cybersecurity: Understand and oversee cybersecurity risks to prepare for increasingly sophisticated and frequent attacks

As cybercriminals raise the stakes with escalating ransomware attacks and hacking of the Internet of Things, companies will need to be even more diligent in their defenses and employee training. In addition, cybersecurity regulation will likely increase in 2017. The New York State Department of Financial Services has enacted a robust cybersecurity regulation, with heightened encryption, log retention and certification requirements, and other regulators have issued significant guidance. Multinational companies will continue implementation of the EU General Data Protection Regulation requirements, which will be effective in May 2018. EU-U.S. Privacy Shield will face a significant legal challenge, particularly in light of concerns regarding President-elect Trump’s protection of privacy. Trump has stated that the government needs to be “very, very tough on cyber and cyberwarfare” and has indicated that he will form a “cyber review team” to evaluate cyber defenses and vulnerabilities.

5. SEC scrutiny: Monitor the SEC’s increased scrutiny and more frequent enforcement actions, including whistleblower developments, guidance on non-GAAP measures and tougher positions on insider trading

2016 saw the Securities and Exchange Commission (SEC) award tens of millions of dollars to whistleblowers and bring first-of-a-kind cases applying new rules flowing from the protections now afforded to whistleblowers of potential violations of the federal securities laws. The SEC was also active in its review of internal accounting controls and their ability to combat cyber intrusions and other modern-day threats to corporate infrastructure. The SEC similarly continued its comprehensive effort to police insider trading schemes and other market abuses, and increased its scrutiny of non-GAAP (generally accepted accounting principles) financial measure disclosures. 2017 is expected to bring the appointment of three new commissioners, including a new chairperson to replace outgoing chair Mary Jo White, which will retilt the scales at the commissioner level to a 3-2 majority of Republican appointees. 2017 may also bring significant changes to rules promulgated previously under Dodd-Frank.

6. CFIUS: Account for CFIUS risks in transactions involving non-U.S. investments in businesses with a U.S. presence

Over the past year, the interagency Committee on Foreign Investment in the United States (CFIUS) has been particularly active in reviewing—and, at times, intervening in—non-U.S. investments in U.S. businesses to address national security concerns. CFIUS has the authority to impose mitigation measures on a transaction before it can proceed, and may also recommend that the President block a pending transaction or order divestiture of a U.S. business in a completed transaction. Companies that have not sufficiently accounted for CFIUS risks may face significant hurdles in successfully closing a deal. With the incoming Trump administration, there is also the potential for an expanded role for CFIUS, particularly in light of campaign statements opposing certain foreign investments.

7. Board composition: Evaluate and refresh board composition to help achieve the company’s goals, increase diversity and manage turnover

In order to promote fresh, dynamic and engaged perspectives in the boardroom and help the company achieve its goals, a board should undertake focused reassessments of its underlying composition and skills, including a review and analysis of board tenure, continuity and diversity in terms of upbringing, educational background, career expertise, gender, age, race and political affiliation.

8. Executive compensation: Determine appropriate executive compensation against the background of an increased focus on CEO pay ratios

Executive compensation will continue to be a hot topic for directors in 2017, especially given that public companies will soon have to start complying with the CEO pay ratio disclosure rules. Recent developments suggest that such disclosure might not be as burdensome or harmful to relations with employees and the public as was initially feared.

The SEC’s final rules allow for greater flexibility and ease in making this calculation, and a survey of companies that have already estimated their ratios indicates that the ratio might not be as high, on average, as previously reported.

9. Antitrust scrutiny: Monitor the increased scrutiny of the antitrust authorities and the implications on various proposed combinations

Despite the promise of synergies and the potential to transform a company’s future, antitrust regulators have become increasingly hostile toward strategic transactions, with the Department of Justice and Federal Trade Commission suing to block 12 transactions since 2015. Although directors should brace for a longer antitrust review, to help navigate the regulatory climate, work upfront can dramatically improve prospects for success. Company directors should develop appropriate deal rationales and, with the benefit of upfront work, allocate antitrust risk in the merger agreement. Merger and acquisition activity may also benefit from the Trump administration, taking, at least for certain industries, a less-aggressive antitrust enforcement stance.

10. Environmental disasters and contagious diseases: Monitor the impact of increasingly volatile weather events and contagious disease outbreaks on risk management processes, employee needs and logistics planning

While the causes of climate change remain a political sticking point, it cannot be debated that volatile weather events, environmental damage and a rise in the diseases that tend to follow, are having increasingly adverse impacts on businesses and markets. Businesses will need to account for, or transfer the risk of, the increasing likelihood of these impacts. The SEC recently announced investigations into climate-risk disclosures within the oil and gas sector to ensure that they adequately allow investors to account for these effects on the bottom line. The growing number of shareholder resolutions and suits addressing climate change confirm that investors want this information, regardless of the position of the next administration.

*Kerry E. Berchem is partner and head of the corporate practice, and Rick L. Burdick is partner and chair of the Global Energy & Transactions group, at Akin Gump Strauss Hauer & Feld LLP.

Voici un excellent résumé des principales tendances en gouvernance à l’échelle internationale. L’article paru sur le site de la Harvard Law School Forum est le fruit des recherches effectuées par Rusty O’Kelley, membre de CEO and Board Services Practice, et Anthony Goodman, membre de Board Effectiveness Practice de Russell Reynolds Associates.

Les auteurs ont interviewé plusieurs investisseurs activistes et institutionnels ainsi que des administrateurs de sociétés publiques et des experts de la gouvernance afin d’appréhender les tendances qui se dessinent pour les entreprises cotées en 2017.

Parmi les conclusions de l’étude, notons :

Le besoin de se coller plus étroitement à des normes de gouvernance universellement acceptées ;

La nécessité de bien se préparer aux nouveaux risques et aux nouvelles opportunités amenées par la montée des gouvernements populistes de droite ;

Une responsabilité accrue des administrateurs de sociétés pour la création de valeur à long terme ;

L’importance d’une solide compréhension des changements globaux eu égard à l’exercice d’une bonne gouvernance, notamment dans les états suivants :

– États-Unis

– Union européenne

– Japon

– Inde

– Brésil

Cette lecture nous donne une perspective globale des défis qui attendent les administrateurs et les CA de grandes sociétés publiques en 2017.

Russell Reynolds Associates recently interviewed numerous institutional and activist investors, pension fund managers, public company directors and other governance professionals about the trends and challenges that public company boards will face in 2017. Our conversations yielded a wide array of perspectives about the forces that are driving change in the corporate governance landscape.

The changing pressures and dynamics that boards will face in the coming year are diverse and significant in their impact. Institutional investors will continue their push for more uniform standards of corporate governance globally, while also increasing their expectations of the role that boards should play in responsibly representing shareholders. Political uncertainty and the surprise results of the US Presidential and “Brexit” votes may require that boards take a more active role in scenario planning and helping management to navigate increasingly costly risks. The movement for companies and investors to adopt a more long-term orientation has gained momentum, with several large institutional investors now pressuring boards to demonstrate that they are actively involved in guiding a company’s strategy for long-term value creation.

Higher Expectations and Greater Alignment Around Corporate Governance Norms

Continuing the trend from last year, large institutional investors and pension funds are pushing for more aligned approaches to corporate governance across borders to support long-term value creation. Regulators are responding, particularly in emerging economies and those with nascent corporate governance regimes. Recent reforms in Japan, India and Brazil have borrowed heavily from the US or UK models. Where regulators have not yet caught up to or agreed with investor expectations, institutional investors are engaging companies directly to advocate for the governance reforms they want to see. These investors also expect more from their boards than ever before and are increasingly willing to intervene when they do not feel they are being responsibly represented in the boardroom.

Corporate Governance in an Era of Political Uncertainty

Populist political movements have gained broad support in several countries around the world, contributing to uncertainty about the future regulatory and political environments of two of the world’s five largest economies. In the UK, the Conservative government has signaled potential support for shareholder influence over executive pay and disclosure of the CEO-employee pay ratio. In the US, President-elect Trump has demonstrated a willingness to “name and shame” specific companies that he perceives to have benefited unfairly from trade deals or moved jobs overseas. Boards must be prepared to navigate these new reputational risks and intense media scrutiny, and review management’s assumptions about the political implications of certain decisions.

Increasing Board Accountability for Long-Term Value Creation

Efforts to encourage a more long-term market orientation have intensified in recent years, with several prominent business leaders and investors, most notably Larry Fink, Chairman and CEO of BlackRock, urging companies to focus on sustained value creation rather than maximizing short-term earnings. In his 2016 letter to chief executives of S&P 500 companies and large European corporations, Mr. Fink specifically called for increased board oversight of a company’s strategy for long-term value creation, noting that BlackRock’s corporate governance team would be looking for assurances of this oversight when engaging with companies.

Global and Regional Trends in Corporate Governance in 2017

Based on our global experience as a firm and our interviews with experts around the world, we believe that public companies will likely face the following trends in 2017:

Increasing expectations around the oversight role of the board, to include greater oversight of strategy and scenario planning, investor engagement, and executive succession planning.

Continued focus on board refreshment and composition, with particular attention being paid to directors’ skill profiles, the currency of directors’ knowledge, director overboarding, diversity, and robust mechanisms for board refreshment that go beyond box-ticking exercises.

Greater scrutiny of company plans for sustained value creation, as concerns increase that activist settlements and other market forces are causing short-term priorities to compromise long-term interests.

Greater focus on Environmental, Social and Governance (ESG) issues, and in particular those related to climate change and sustainability, as industries beyond the extractive sector begin to feel investor pressure in this area.

We explore these trends and their implications for five key regions and markets: the United States, the European Union, India, Japan and Brazil.

United States

The surprise election of Donald Trump has increased regulatory and legislative uncertainty. Certain industries, such as financial services, natural resources and healthcare, may face less pressure and government scrutiny. We expect nominees to the Securities and Exchange Commission (SEC) to be less supportive of the increased disclosure requirements around executive pay and diversity. However, public pension funds and institutional investors will continue to push governance issues through increased specific engagement with individual companies.

Investors continue to push boards to demonstrate that they are taking a strategic and proactive approach to board refreshment. In particular, they are looking for indicators that boards are adding directors with the skill sets necessary to complement the company’s strategic direction, and ensuring a diversity of backgrounds and perspectives to guide that strategy. Some investors see tenure and age limits as too blunt an instrument, preferring internal or external board evaluations to ensure that every director is contributing effectively. Several large institutional investors will continue to push boards to conduct external board evaluations by third parties to increase the quality of feedback and improve governance.

Ongoing fallout from the Wells Fargo scandal will increase pressure on boards to split the CEO/Chair role, particularly in the financial services sector. Given investor pressure, particularly from pension funds, we also anticipate increased demand for clawbacks, a trend that is likely to go beyond the banking sector.

We expect that 2017 will be a significant year for ESG issues, and in particular those related to climate change and sustainability. Industries beyond the extractive sector will begin to feel investor pressure in this area. While this pressure is being exerted by a number of stakeholder groups, the degree to which the baton has been picked up by mainstream institutional investors is notable.

Increased attention on climate risk is also changing the way many companies and investors think about materiality and disclosure, which will have significant implications for audit committees. Michael Bloomberg is currently leading the Financial Stability Board’s Task Force on Climate-related Financial Disclosures, which will seek to develop consistent, voluntary standards for companies to provide information about climate-related financial risk. The Task Force’s recommendations are expected in mid-2017.

Boards will increasingly be expected to ensure sufficient succession planning not just at the CEO level but in other key C-suite roles as well, as investors want to know that boards are actively monitoring the pipeline of talent. Additionally, there is a relatively new trend of some boards conducting crisis management exercises as a supplement to the activism risk assessment we have seen over the past couple of years.

In the event that all or parts of the Dodd-Frank regulations are repealed, investors will likely turn to private ordering—seeking to persuade companies to change their by-laws—to keep the elements that are most important to them (e.g. “say on pay”). Current SEC rules require that companies begin disclosing their CEO-employee pay ratio in 2018, but we believe this to be a likely target for repeal.

European Union

Across many countries in Europe, the push for board and management diversity will continue apace in 2017. Executive pay continues to be the focus of government, investor and media attention with various proposals for reining in compensation. Work being done in the UK on board oversight of corporate culture has the potential to spill across European borders and travel farther afield over the next few years.

Many countries in Europe continue to push ahead with encouraging gender diversity at the board level, as national laws regulating the number of female directors proliferate. In the UK, the Hampton-Alexander Review recommended that the Corporate Governance Code be amended to require FTSE 350 companies to disclose the gender balance of their executive committees in their annual report.

After ebbing slightly in 2014, activism has made a comeback in Europe: whereas 51 companies were targeted in 2014, 64 were targeted in the first half of 2016 alone. We anticipate that European activists will continue to apply less aggressive and more collaborative tactics than those seen in the US. Additionally, we expect to see US and European institutional investors to be supportive of European activist investors, particularly those who are self-described “constructive activists”, who take a less aggressive approach than their US counterparts.

The EU is expected to amend its Shareholder Rights Directive in 2017 to include an EU-wide “say on pay” framework that would give shareholders the right to regular votes on prospective and retrospective remuneration. While these votes are not expected to be binding, the directive does require that pay be based on a shareholder-approved policy and that issuers must address failed votes. Germany saw a sharp increase in dissents on “say on pay” proposals this year, jumping from 8% to over 20%. In France, the government is currently debating whether to make “say on pay” votes binding, spurred by the public outcry about the Renault board’s decision to confirm the CEO’s 2015 compensation, despite a rejection by a majority of shareholders.

The UK government is expected to continue its push for compensation practice reform in 2017, having recently published a series of proposed policies, including mandatory disclosure of the CEO pay ratio, employee representation in executive compensation decisions, and making shareholder votes on executive compensation binding. We also expect continued strong media coverage and related public opposition to large public company pay packages, which could put UK boards in the spotlight.

In Germany, the ongoing fallout from the Volkswagen scandal is the likely impetus for proposed amendments to the corporate governance code that would underscore boards’ obligations to adhere to ethical business practices. The proposed amendments also acknowledge the increasingly common practice of investor engagement with the supervisory board, and recommend that the supervisory board chair be prepared to discuss relevant topics with investors.

In the UK, boards will be focused on implementing the recommendations of the recent Financial Reporting Council (FRC) report on corporate culture and the role of boards, which makes the case that long-term value creation is directly linked to company culture and the role of business in society.

India

Indian boards continue to struggle with the implementation of many of the major changes to corporate governance practices required by the 2013 Companies Act, but reform is progressing. While the complete fallout from the recent Tata leadership imbroglio is not yet clear, it will almost certainly reverberate through the Indian corporate governance landscape for years to come.

Recent regulatory changes have increased the scope of responsibilities for the Nomination and Remuneration Committee, requiring boards to ensure that directors have the right set of skills to deliver on these new responsibilities. Increased emphasis on CEO succession planning and board evaluations have necessitated that Committee members become more fluent in these governance processes and methodologies, particularly as the requirement to report on them annually has increased the spotlight on the board’s role in these processes.

The introduction in 2013 of a mandatory minimum of at least one female director for most listed companies has increased India’s gender diversity at the board level to one of the highest rates in Asia, with 14% of all directorships currently held by women. However, concerns persist about the potential for “tokenism”, as a sizeable portion of the women appointed come from the controlling families of the company.

India has also attempted to integrate ESG and Corporate Social Responsibility (CSR) issues at the board level, having mandated that every board establish a CSR committee and that the company spend 2% of net profits on CSR activities. However, companies will need to ensure that their approach to CSR amounts to more than a box-ticking exercise if they want to attract the support of the growing cadre of ESG-focused investors.

Boards are increasingly expected to take a more active role in risk management, particularly cybersecurity risks. Boards should also ensure that their companies are adequately anticipating and responding to cybersecurity threats.

Changes to the 2013 Companies Act have considerably enhanced the duties and liabilities of directors, along with strict penalties for any breach of these duties and the potential for class action lawsuits against individual directors. While potentially helpful in increasing director accountability, these changes also significantly increase the personal risk that a director assumes when joining a board.

Japan

Japan’s Corporate Governance Code was reformulated in 2015, as part of the “Abenomics” push for structural reforms. Japanese companies continue to implement the corporate governance principles resulting from the new regulations, with many hoping that the adoption of more Western norms will help prompt the return of foreign investors.

The overhaul of Japan’s corporate governance model in 2015 has begun to yield significant results, as 96% of Japanese boards now have at least one outside director and 78% have at least two. However, Japan’s famously deferential corporate culture may make it difficult for boards to unlock the value of these independent perspectives, as seniority and family ownership often still take precedence.

Increasing investor interest in the Japanese market is likely to increase pressure on boards to adopt more Western norms of corporate governance. CalPERS, the California public pension fund, recently began an explicit program of engagement in Japan, their second-largest equity market, in order to encourage the adoption of more Western norms, including increased board independence and diversity, defining narrower standards of independence, and increasing the disclosure of director qualifications.

Gender diversity remains a challenge for Japanese boards, with only 3% of directorships held by women. However, women account for 22% of outside directors, suggesting that gender diversity on boards will likely continue to increase as the appointment of independent directors becomes more common. A new law, introduced in April 2016, now requires companies with more than 300 employees to publish data on the number of women they employ and how many hold management positions. We anticipate this increased scrutiny at all levels of the company to have a knock-on effect for boards.

While other elements of the new Corporate Governance Code have seen near unanimous compliance, only 55% of listed companies have complied with the stipulation to conduct formal board evaluations. Moreover, the quality and format of the evaluations that are occurring vary significantly, with many adopting a self-evaluation process that amounts to little more than a box-ticking exercise.

The common Japanese practice of former executives and chairs remaining in “advisor” roles beyond the end of their formal tenure is now coming under increasing scrutiny. ISS will now generally vote against amendments to create new advisory positions, unless the advisors will serve on the board and therefore be held accountable to shareholders.

Brazil

Brazil’s corporate governance regime has evolved significantly in the last decade, as various regulatory entities have sought to apply greater protections for minority shareholders and better align standards with other Western models to attract greater foreign investment.

As Brazil continues to navigate the fallout of the Petrobras scandal, many are questioning how the mechanisms for encouraging and enforcing investor stewardship and corporate governance can be strengthened.

AMEC, Brazil’s association of institutional investors, recently released the country’s first Investor Stewardship Code, calling on investors to adhere to seven principles, including implementing mechanisms to manage conflicts of interest, taking ESG issues into account, and being active and diligent in the exercise of voting rights.

In an effort to address the high levels of absenteeism among institutional investors at general meetings, Brazil’s Security and Exchange Commission (CVM) will, beginning in 2017, require that listed companies allow shareholders to vote by mail or email, rather than requiring that they (or their proxy) be physically present to cast their vote. Brazilian companies, and their boards, should be prepared for the increased requests for investor engagement that are likely to result from the more active participation of institutional investors in the voting process.

New regulations for the country’s Novo Mercado segment of listed companies will be announced in 2017. Highlights of the proposed changes include the required establishment of audit, compensation and appointment committees, a minimum of two independent directors, and more stringent disclosure of directors’ relationships to related companies and other parties.

Yvan Allaire*, président exécutif de l’Institut de la gouvernance des organisations privées et publiques (IGOPP), vient de me transmettre une synthèse de l’analyse de la saga CP-Ackman-Pershing Square, portant sur les leçons à tirer de cet épisode d’agression par un fonds « activiste ».

Cet article a été publié sur le site du Harvard Law School Forum on Corporate Governance and Financial Regulation le 23 décembre 2016.

Comme le disent les auteurs, l’une des leçons à retirer de cette saga est que les conseils d’administration de l’avenir doivent agir comme des activistes, en ce sens qu’ils doivent être continuellement à la recherche d’informations susceptibles de questionner leurs stratégies et leur modèle d’affaires. Sinon, certains fonds activistes seront bien tentés par l’aventure…

Le texte complet du cas est accessible en cliquant sur « here » en fin de texte.

Pershing Square Capital Management, an activist hedge fund owned and managed by Bill Ackman, began hostile maneuvers against the board of CP Rail in September 2011 and ended its association with CP in August 2016, having netted a profit of $2.6 billion for his fund. This Canadian saga, in many ways, an archetype of what hedge fund activism is all about, illustrates the dynamics of these campaigns and the reasons why this particular intervention turned out to be a spectacular success… thus far.

In 2009, the Chairman of the board of the Canadian Pacific Railway (CP) asserted that the company had put in place the best practices of corporate governance; that year, CP was awarded the Governance Gavel Award for Director Disclosure by the Canadian Coalition for Good Governance. Then, in 2011, CP ranked 4th out of some 250 Canadian companies in the Globe & Mail Corporate Governance Ranking. [1] Yet, this stellar corporate governance was no insurance policy against shareholder discontent.

Pershing Square began purchasing shares of CP on September 23, 2011. They filed a 13D form on October 28th showing a stock holding of 12.2%; by December 12, 2011, their holding had reached 14.2% of CP voting shares, thus making Pershing Square the largest shareholder of the company.

On February 6, 2012, Ackman, with Hunter S. Harrison (retired CEO of CN—direct competitor of CP and leader in efficiency among Class 1 North American railways—and his candidate for CEO of CP) by his side, made a fact-based presentation about the shortcomings and failings of the CP board and management. Harrison and Ackman stated that their goal for CP was to achieve an operating ratio of 65 for 2015 (down from 81.3 in 2011—the lower the ratio, the better the performance).

The Board qualified Harrison’s (and Ackman’s) targets of “shot in the dark”, showing a lack of research and a profound misunderstanding of CP’s reality. Relying on an independent consultant report (Oliver Wyman Group), Green mentioned that Harrison’s target for CP’s operating ratio was not achievable since CP’s network was characterized by steeper grades and greater curvature thus adding close to 6.7% to the operating ratio compared to its competitors. [2]

On April 4th 2012, Bill Ackman came out swinging in a scathing letter to CP shareholders disparaging CP’s Board of directors in general, and its CEO, Fred Green, in particular. According to Mr. Ackman, “under the direction of the Board and Mr. Green, CP’s total return to shareholders from the inception of Mr. Green’s CEO tenure to the day prior to Pershing Square’s investment was negative 18% while the other Class I North American railways delivered strong positive total returns to shareholders of 22% to 93%.” [3] Thus, according to him, “Fred Green’s and the Board’s poor decisions, ineffective leadership and inadequate stewardship have destroyed shareholder value.” [4]

A few hours before the annual meeting, CP issued a press release in which it stated that Fred Green had resigned as CEO, and that five other directors, including the Chairman of the Board, John Cleghorn, would not stand for re-election at the company’s shareholder meeting.

Pershing Square had won the proxy fight; all the nominees proposed by Ackman were elected.

Almost exactly five years after first buying shares of CP, Ackman confirmed in August 2016 that Pershing Square would sell its remaining shares of CP, thus formally exiting the “target.” Over those five years, CP has generated a compounded annualized total shareholder return of 45.39% (between September 23, 2011 and August 31, 2016), a performance well above the CN and the S&P/TSX 60 index (CP is a constituent of that index). Pershing Square pocketed an estimated $2.6 billion in profits for its venture into CP.

With massive reductions in the workforce, a transformation of the operations and a radical change of the CP’s organizational culture, CP is undoubtedly a different company from what it was before the proxy fight. In early September 2016, Bill Ackman resigned from CP’s Board, officially concluding this episode.

Lessons in corporate governance

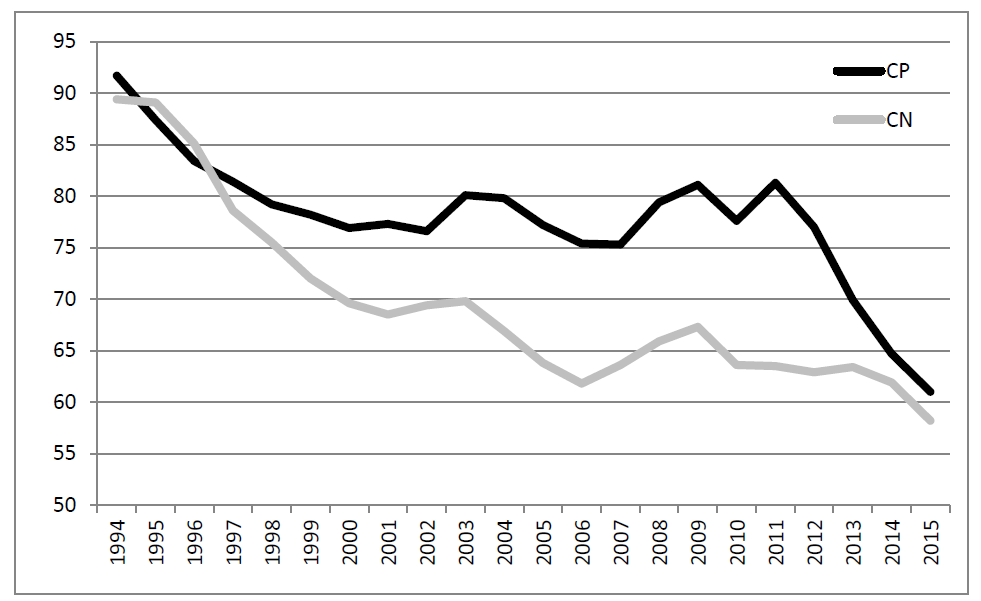

In this day and age, the CP case teaches us that no matter its size or the nature of its business, a company is always at risk of being challenged by dissident shareholders, and most particularly by those funds which make a business of these sorts of operations, the activist hedge funds. Of course, a number of critical features of this saga can be singled out to explain the particular success of this intervention, but this is not the focal point of this post. [5] After all, a widely held company with weak financial results and a stagnating stock price will inevitably attract the attention of these funds.

But the puzzling question and it is an unresolved dilemma of corporate governance remains: how come the board did not know earlier what became apparent very quickly after the Ackman/Harrison takeover? Why would the board not call on independent experts to assess management’s claim that structural differences made it impossible for CP to achieve a performance similar to that of other railroads? The gap in operating ratio between CP and CN had not always been as wide. In fact, as shown in Figure 1, CP had a lower operating ratio than CN during a period of time in the 1990s (Of course, CN was a Crown corporation at that time). The gap eventually widened, reaching unprecedented levels during Fred Green’s tenure (the last full year of operating ratios attributable to Green was in 2011).

Figure 1. Evolution of the operating ratio (%—left scale) for the CP and CN (1994-2015)

How could the board have known that performances far superior to those targeted by the CEO could be swiftly achieved?

Lurking behind these questions is the fundamental flaw of corporate governance: the asymmetry of information, of knowledge and time invested between the governors and the governed, between the board of directors and management. In CP’s case, the directors, as per the norms of “good” fiduciary governance, relied on the information provided by management, believed the plans submitted by management to be adequate and challenging, and based the executives’ lavish compensation on the achievement of these plans. The Chairman, on behalf of the Board, did “extend our appreciation to Fred Green and his management team for aggressively and successfully implementing our Multi-Year plan and creating superior value for our shareholders and customers.” [6] That form of governance is being challenged by activist investors of all stripes.

Their claim, a demonstrable one in the case of CP, is that with the massive amount of information now accessible about a publicly listed company and its competitors, it is possible for dedicated shareholders to spot poor strategies and call for drastic changes. If push comes to shove, these funds will make their case directly to other shareholders via a proxy contest for board membership.

Corporate boards of the future will have to act as “activists” in their quest for information and their ability to question strategies and performances.

5The case analysis identified four factors that are rarely present in other cases of activism, a fact which explains why few of these interventions achieve the level of success of the CP case.(go back)

6Cleghorn, John. Chairman’s letter to shareholders, CP’s Annual Information Form 2011.(go back)

__________________________________

*Yvan Allaire is Emeritus professor of strategy at Université du Québec à Montréal (UQAM) and Executive Chair of the Institute for Governance of Private and Public Organizations (IGOPP); François Dauphin is Director of Research of IGOPP and a lecturer at UQAM. This post is based on their recent paper.