Cette situation montre clairement que les fonds activistes sont continuellement à la recherche de talents uniques et qu’ils sont prêts à miser des fortunes pour bénéficier de l’expertise incontestable d’un PDG.

In an unexpected turn of events, Canadian Pacific Railway announced the early departure of its CEO, Hunter Harrison, a few minutes before a conference call planned for analysts on Jan. 18. Instead of retiring as planned, Harrison leaves CP at age 72 for a new challenge, running another railway company (almost certainly CSX) on behalf of Mantle Ridge LP, a newly established hedge fund run by Paul Hilal. In his prior role at Pershing Square Capital, Hilal was instrumental in backing its investment in CP and installing Harrison’s management team.

CSX: Hunter Harrison Wants to Run His Fourth Railroad

Harrison thus forfeited all benefits and perquisites that he was entitled to receive from CP, including his pension, and he has agreed to surrender for cancellation almost all of his vested and unvested equity awards. Evidently the hedge fund will make him whole for the loss of this package, valued at approximately $118 million.

What makes Hunter Harrison so valuable? In the enchanted world of finance, there are of course no limits to what someone gets paid as long as it is a fraction of what the payer will gain. Still, one would think that a hedge fund manager looking for someone capable of turning around a poorly performing U.S. company would have an abundance of candidates to choose from. After all, the operating tricks that Harrison has come up with to make railroads more efficient have been described in minute detail in books he’s written. Dozens of seasoned railroad executives have worked with him and for him over the years. They must have learned quite a bit about Harrison’s recipe.

The answer to the $118-million question appears to reside in the fact that the successful transformation of these railroads (CN and CP) was the result, yes, of operational improvements, but more so of a fundamental cultural change. Harrison is a formidable change agent, a transformational leader in the truest meaning of that tired expression.

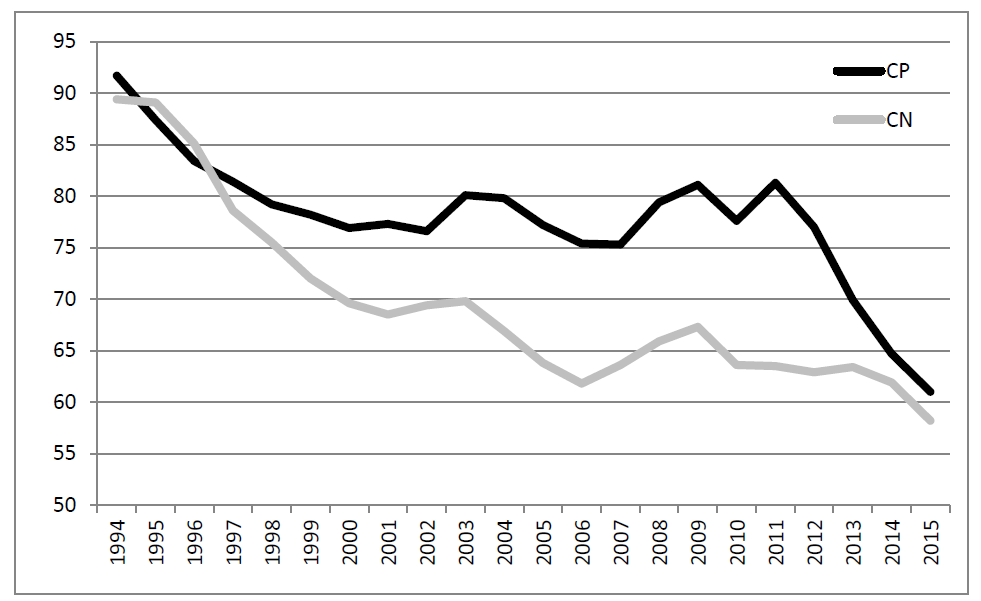

He claims to have invented a principle called “precision railroading,” which he implemented at three major railroads: Illinois Central, CN, and CP, the last with spectacular results, bringing the operating ratio (operating costs as a percentage of revenue, with a lower ratio being better) to 58.6 per cent for fiscal year 2016, down from 81.3 per cent in 2011, the last full year before Harrison’s took over.

Precision railroading, if it was easily learned from a book and replicated, would have been applied with success long ago at every North American railroad. Yet Harrison still seems to bring something that can make a difference over and above the techniques he developed and implemented. That something seems to be his skill at changing the culture of the railroad, a most difficult skill to imitate.

As a lifetime railroader himself, his decisions and actions display a deep understanding of the daily reality of the operators. He spends time meeting with the workers on the field and communicates profusely about the importance of asset optimization and the control of costs. At CP, he took many symbolic actions to instill in the whole organization the need to think and act like a railroader. For example, he relocated the corporate glass-towered headquarters to a rail yard, a move that was meant partly to cut costs but mostly to keep the employees’ focus on freight operations, and remind them daily of what the business is all about.

Managing a strategic turnaround is not an easy task. The softer, cultural element of it is often neglected, overlooked, and difficult to implement. That is where Harrison excels and why a hedge fund manager is prepared to pay big bucks to get that talent working for him.

But is money really the sole motivation for Harrison to start over at another railroad company at 72? In fact, at this stage of his career, he has more to lose reputation-wise if he fails than anything he can really earn in monetary terms.

The Memphis, Tenn. native, whose career began over five decades ago as an 18-year-old carman-oiler, may be driven by the determination to prove that the theory he has developed is replicable, no matter where. And determined to push his legacy to a new level — that of a railroad industry legend.

__________________________________

*Yvan Allaire est professeur émérite de stratégie à l’Université du Québec à Montréal (UQAM) et président exécutif de l’Institut de la gouvernance des organisations privées et publiques (IGOPP), François Dauphin est directeur de la recherche à l’IGOPP et chargé d’enseignement à l’UQAM.

Aujourd’hui, je partage avec vous la liste des dix thèmes majeurs en gouvernance que les auteurs Kerry E. Berchem* et Rick L. Burdick* ont identifiés pour l’année 2017.

Vous êtes assurément au fait de la plupart de ces dimensions, mais il faut noter l’importance accrue à porter aux questions stratégiques, aux changements politiques, aux relations avec les actionnaires, à la cybersécurité, aux nouvelles réglementations de la SEC, à la composition du CA, à l’établissement de la rémunération et aux répercussions possibles des changements climatiques.

Afin de mieux connaître l’ampleur de ces priorités de gouvernance pour les administrateurs de sociétés, je vous invite à lire l’ensemble du rapport publié par Akin Gump.

1. Corporate strategy: Oversee the development of the corporate strategy in an increasingly uncertain and volatile world economy with new and more complex risks

Directors will need to continue to focus on strategic planning, especially in light of significant anticipated changes in U.S. government policies, continued international upheaval, the need for productive shareholder relations, potential changes in interest rates, uncertainty in commodity prices and cybersecurity risks, among other factors.

2. Political changes: Monitor the impact of major political changes, including the U.S. presidential and congressional elections and Brexit

Many uncertainties remain about how the incoming Trump administration will govern, but President-elect Trump has stated that he will pursue vast changes in diverse regulatory sectors, including international trade, health care, energy and the environment. These changes are likely to reshape the legal landscape in which companies conduct their business, both in the United States and abroad.

With respect to Brexit, although it is clear that the United Kingdom will, very probably, leave the European Union, there is no certainty as to when exactly this will happen or what the U.K.’s future relationship, if any, with the EU will be. Once the negotiations begin, boards will need to be quick to assess the likely shape of any deal between the U.K. and the EU and to consider how to adjust their business model to mitigate the threats and take advantage of the opportunities that may present themselves.

3. Shareholder relations: Foster shareholder relations and assess company vulnerabilities to prepare for activist involvement

The current environment demands that directors of public companies remain mindful of shareholder relations and company vulnerabilities by proactively engaging with shareholders, addressing shareholder concerns and performing a self-diagnostic analysis. Directors need to understand their company’s vulnerabilities, such as a de-staggered board or the lack of access to a poison pill, and be mindful of them in any engagement or negotiation process.

4. Cybersecurity: Understand and oversee cybersecurity risks to prepare for increasingly sophisticated and frequent attacks

As cybercriminals raise the stakes with escalating ransomware attacks and hacking of the Internet of Things, companies will need to be even more diligent in their defenses and employee training. In addition, cybersecurity regulation will likely increase in 2017. The New York State Department of Financial Services has enacted a robust cybersecurity regulation, with heightened encryption, log retention and certification requirements, and other regulators have issued significant guidance. Multinational companies will continue implementation of the EU General Data Protection Regulation requirements, which will be effective in May 2018. EU-U.S. Privacy Shield will face a significant legal challenge, particularly in light of concerns regarding President-elect Trump’s protection of privacy. Trump has stated that the government needs to be “very, very tough on cyber and cyberwarfare” and has indicated that he will form a “cyber review team” to evaluate cyber defenses and vulnerabilities.

5. SEC scrutiny: Monitor the SEC’s increased scrutiny and more frequent enforcement actions, including whistleblower developments, guidance on non-GAAP measures and tougher positions on insider trading

2016 saw the Securities and Exchange Commission (SEC) award tens of millions of dollars to whistleblowers and bring first-of-a-kind cases applying new rules flowing from the protections now afforded to whistleblowers of potential violations of the federal securities laws. The SEC was also active in its review of internal accounting controls and their ability to combat cyber intrusions and other modern-day threats to corporate infrastructure. The SEC similarly continued its comprehensive effort to police insider trading schemes and other market abuses, and increased its scrutiny of non-GAAP (generally accepted accounting principles) financial measure disclosures. 2017 is expected to bring the appointment of three new commissioners, including a new chairperson to replace outgoing chair Mary Jo White, which will retilt the scales at the commissioner level to a 3-2 majority of Republican appointees. 2017 may also bring significant changes to rules promulgated previously under Dodd-Frank.

6. CFIUS: Account for CFIUS risks in transactions involving non-U.S. investments in businesses with a U.S. presence

Over the past year, the interagency Committee on Foreign Investment in the United States (CFIUS) has been particularly active in reviewing—and, at times, intervening in—non-U.S. investments in U.S. businesses to address national security concerns. CFIUS has the authority to impose mitigation measures on a transaction before it can proceed, and may also recommend that the President block a pending transaction or order divestiture of a U.S. business in a completed transaction. Companies that have not sufficiently accounted for CFIUS risks may face significant hurdles in successfully closing a deal. With the incoming Trump administration, there is also the potential for an expanded role for CFIUS, particularly in light of campaign statements opposing certain foreign investments.

7. Board composition: Evaluate and refresh board composition to help achieve the company’s goals, increase diversity and manage turnover

In order to promote fresh, dynamic and engaged perspectives in the boardroom and help the company achieve its goals, a board should undertake focused reassessments of its underlying composition and skills, including a review and analysis of board tenure, continuity and diversity in terms of upbringing, educational background, career expertise, gender, age, race and political affiliation.

8. Executive compensation: Determine appropriate executive compensation against the background of an increased focus on CEO pay ratios

Executive compensation will continue to be a hot topic for directors in 2017, especially given that public companies will soon have to start complying with the CEO pay ratio disclosure rules. Recent developments suggest that such disclosure might not be as burdensome or harmful to relations with employees and the public as was initially feared.

The SEC’s final rules allow for greater flexibility and ease in making this calculation, and a survey of companies that have already estimated their ratios indicates that the ratio might not be as high, on average, as previously reported.

9. Antitrust scrutiny: Monitor the increased scrutiny of the antitrust authorities and the implications on various proposed combinations

Despite the promise of synergies and the potential to transform a company’s future, antitrust regulators have become increasingly hostile toward strategic transactions, with the Department of Justice and Federal Trade Commission suing to block 12 transactions since 2015. Although directors should brace for a longer antitrust review, to help navigate the regulatory climate, work upfront can dramatically improve prospects for success. Company directors should develop appropriate deal rationales and, with the benefit of upfront work, allocate antitrust risk in the merger agreement. Merger and acquisition activity may also benefit from the Trump administration, taking, at least for certain industries, a less-aggressive antitrust enforcement stance.

10. Environmental disasters and contagious diseases: Monitor the impact of increasingly volatile weather events and contagious disease outbreaks on risk management processes, employee needs and logistics planning

While the causes of climate change remain a political sticking point, it cannot be debated that volatile weather events, environmental damage and a rise in the diseases that tend to follow, are having increasingly adverse impacts on businesses and markets. Businesses will need to account for, or transfer the risk of, the increasing likelihood of these impacts. The SEC recently announced investigations into climate-risk disclosures within the oil and gas sector to ensure that they adequately allow investors to account for these effects on the bottom line. The growing number of shareholder resolutions and suits addressing climate change confirm that investors want this information, regardless of the position of the next administration.

*Kerry E. Berchem is partner and head of the corporate practice, and Rick L. Burdick is partner and chair of the Global Energy & Transactions group, at Akin Gump Strauss Hauer & Feld LLP.

Yvan Allaire*, président exécutif de l’Institut de la gouvernance des organisations privées et publiques (IGOPP), vient de me transmettre une synthèse de l’analyse de la saga CP-Ackman-Pershing Square, portant sur les leçons à tirer de cet épisode d’agression par un fonds « activiste ».

Cet article a été publié sur le site du Harvard Law School Forum on Corporate Governance and Financial Regulation le 23 décembre 2016.

Comme le disent les auteurs, l’une des leçons à retirer de cette saga est que les conseils d’administration de l’avenir doivent agir comme des activistes, en ce sens qu’ils doivent être continuellement à la recherche d’informations susceptibles de questionner leurs stratégies et leur modèle d’affaires. Sinon, certains fonds activistes seront bien tentés par l’aventure…

Le texte complet du cas est accessible en cliquant sur « here » en fin de texte.

Pershing Square Capital Management, an activist hedge fund owned and managed by Bill Ackman, began hostile maneuvers against the board of CP Rail in September 2011 and ended its association with CP in August 2016, having netted a profit of $2.6 billion for his fund. This Canadian saga, in many ways, an archetype of what hedge fund activism is all about, illustrates the dynamics of these campaigns and the reasons why this particular intervention turned out to be a spectacular success… thus far.

In 2009, the Chairman of the board of the Canadian Pacific Railway (CP) asserted that the company had put in place the best practices of corporate governance; that year, CP was awarded the Governance Gavel Award for Director Disclosure by the Canadian Coalition for Good Governance. Then, in 2011, CP ranked 4th out of some 250 Canadian companies in the Globe & Mail Corporate Governance Ranking. [1] Yet, this stellar corporate governance was no insurance policy against shareholder discontent.

Pershing Square began purchasing shares of CP on September 23, 2011. They filed a 13D form on October 28th showing a stock holding of 12.2%; by December 12, 2011, their holding had reached 14.2% of CP voting shares, thus making Pershing Square the largest shareholder of the company.

On February 6, 2012, Ackman, with Hunter S. Harrison (retired CEO of CN—direct competitor of CP and leader in efficiency among Class 1 North American railways—and his candidate for CEO of CP) by his side, made a fact-based presentation about the shortcomings and failings of the CP board and management. Harrison and Ackman stated that their goal for CP was to achieve an operating ratio of 65 for 2015 (down from 81.3 in 2011—the lower the ratio, the better the performance).

The Board qualified Harrison’s (and Ackman’s) targets of “shot in the dark”, showing a lack of research and a profound misunderstanding of CP’s reality. Relying on an independent consultant report (Oliver Wyman Group), Green mentioned that Harrison’s target for CP’s operating ratio was not achievable since CP’s network was characterized by steeper grades and greater curvature thus adding close to 6.7% to the operating ratio compared to its competitors. [2]

On April 4th 2012, Bill Ackman came out swinging in a scathing letter to CP shareholders disparaging CP’s Board of directors in general, and its CEO, Fred Green, in particular. According to Mr. Ackman, “under the direction of the Board and Mr. Green, CP’s total return to shareholders from the inception of Mr. Green’s CEO tenure to the day prior to Pershing Square’s investment was negative 18% while the other Class I North American railways delivered strong positive total returns to shareholders of 22% to 93%.” [3] Thus, according to him, “Fred Green’s and the Board’s poor decisions, ineffective leadership and inadequate stewardship have destroyed shareholder value.” [4]

A few hours before the annual meeting, CP issued a press release in which it stated that Fred Green had resigned as CEO, and that five other directors, including the Chairman of the Board, John Cleghorn, would not stand for re-election at the company’s shareholder meeting.

Pershing Square had won the proxy fight; all the nominees proposed by Ackman were elected.

Almost exactly five years after first buying shares of CP, Ackman confirmed in August 2016 that Pershing Square would sell its remaining shares of CP, thus formally exiting the “target.” Over those five years, CP has generated a compounded annualized total shareholder return of 45.39% (between September 23, 2011 and August 31, 2016), a performance well above the CN and the S&P/TSX 60 index (CP is a constituent of that index). Pershing Square pocketed an estimated $2.6 billion in profits for its venture into CP.

With massive reductions in the workforce, a transformation of the operations and a radical change of the CP’s organizational culture, CP is undoubtedly a different company from what it was before the proxy fight. In early September 2016, Bill Ackman resigned from CP’s Board, officially concluding this episode.

Lessons in corporate governance

In this day and age, the CP case teaches us that no matter its size or the nature of its business, a company is always at risk of being challenged by dissident shareholders, and most particularly by those funds which make a business of these sorts of operations, the activist hedge funds. Of course, a number of critical features of this saga can be singled out to explain the particular success of this intervention, but this is not the focal point of this post. [5] After all, a widely held company with weak financial results and a stagnating stock price will inevitably attract the attention of these funds.

But the puzzling question and it is an unresolved dilemma of corporate governance remains: how come the board did not know earlier what became apparent very quickly after the Ackman/Harrison takeover? Why would the board not call on independent experts to assess management’s claim that structural differences made it impossible for CP to achieve a performance similar to that of other railroads? The gap in operating ratio between CP and CN had not always been as wide. In fact, as shown in Figure 1, CP had a lower operating ratio than CN during a period of time in the 1990s (Of course, CN was a Crown corporation at that time). The gap eventually widened, reaching unprecedented levels during Fred Green’s tenure (the last full year of operating ratios attributable to Green was in 2011).

Figure 1. Evolution of the operating ratio (%—left scale) for the CP and CN (1994-2015)

How could the board have known that performances far superior to those targeted by the CEO could be swiftly achieved?

Lurking behind these questions is the fundamental flaw of corporate governance: the asymmetry of information, of knowledge and time invested between the governors and the governed, between the board of directors and management. In CP’s case, the directors, as per the norms of “good” fiduciary governance, relied on the information provided by management, believed the plans submitted by management to be adequate and challenging, and based the executives’ lavish compensation on the achievement of these plans. The Chairman, on behalf of the Board, did “extend our appreciation to Fred Green and his management team for aggressively and successfully implementing our Multi-Year plan and creating superior value for our shareholders and customers.” [6] That form of governance is being challenged by activist investors of all stripes.

Their claim, a demonstrable one in the case of CP, is that with the massive amount of information now accessible about a publicly listed company and its competitors, it is possible for dedicated shareholders to spot poor strategies and call for drastic changes. If push comes to shove, these funds will make their case directly to other shareholders via a proxy contest for board membership.

Corporate boards of the future will have to act as “activists” in their quest for information and their ability to question strategies and performances.

5The case analysis identified four factors that are rarely present in other cases of activism, a fact which explains why few of these interventions achieve the level of success of the CP case.(go back)

6Cleghorn, John. Chairman’s letter to shareholders, CP’s Annual Information Form 2011.(go back)

__________________________________

*Yvan Allaire is Emeritus professor of strategy at Université du Québec à Montréal (UQAM) and Executive Chair of the Institute for Governance of Private and Public Organizations (IGOPP); François Dauphin is Director of Research of IGOPP and a lecturer at UQAM. This post is based on their recent paper.

Voici un cas de gouvernance, publié en décembre sur le site de Julie Garland McLellan* qui illustre comment la direction d’une société publique peut se retrouver en situation d’irrégularité malgré une culture du conseil d’administration axée sur la conformité.

L’investigation du vérificateur général (VG) a révélé plusieurs failles dans les procédures internes de la société. De ce fait, Kyle le président du comité d’audit, risque et conformité, est interpellé par le président du conseil afin d’aider la direction à trouver des solutions durables pour remédier à la situation.

Même si Kyle est conscient qu’il ne possède pas l’autorité requise pour régler les problèmes constatés par le VG, il comprend qu’il est impératif que son message passe.

Le cas présente la situation de manière assez succincte, mais explicite ; puis, trois experts en gouvernance se prononcent sur le dilemme qui se présente aux personnes qui vivent des situations similaires.

Bonne lecture ! Vos commentaires sont toujours les bienvenus.

Kyle is chairman on the Audit, Risk and Compliance committee of a government authority board which is subject to a Public Access to Information Act. The auditor general has just completed an audit of several authorities bound by that Act and Kyle’s authority was found to have several breeches of the Act, in particular;

– some contracts valued at $150,000 or more were not recorded in the contracts register

– some contracts were not entered into the register within 45 working days of the contracts becoming effective

– there were instances where inaccurate information was recorded in the register when compared with the contracts, and

– additional information required for certain classes of contracts was not disclosed in some registers.

The Board Chairman is rightly concerned that this has happened in what all directors believed to be a well governed authority with a strong culture of compliance. The Board Chairman has asked Kyle to oversee management’s response to the Auditor General and the development of systems to ensure that these breeches do not reoccur. Kyle is mindful that he remains a non-executive and has no authority within the chain of management command. He is keen to help and knows that the CEO is struggling with the complexity of her role and will need assistance with any increase in workload.

How can Kyle help without getting embroiled in management affairs?

Raz’s Answer

The issue I spot here, is one which I’ve encountered myself – as a seasoned professional, you have the internal urge to roll your sleeves and get right into it, and solve the problem. From the details disclosed in this dilemma, there’s evidence that the authority’s internal culture is compliant, therefore it’s hard to believe there’s foul play which caused these discrepancies in the reports. I would have guessed that there are some legacy processes, or even old technology, which needs to be looked at and discover where the gap is.

The CEO is under immense pressure to fix this issue, being exposed to public scrutiny, but with the government’s limited resources at her disposal, the pressure is even higher. Making decisions under such pressure, especially when a board member, the chair of the Audit, Risk and Compliance Committee is looking over her shoulder, will likely to force her to make mistakes.

Kyle’s dilemma is simple to explain, but more delicate to handle: « How do I fix this, without sticking my nose into the operations? »

As a NED, what Kyle needs to be is a guide to the CEO, providing a calm and supportive environment for the CEO to operate in. Kyle needs to consult with the CEO, and get her on side, to ensure she’ll devote whichever resources she does have, to deal with this issue. This won’t be a Band-Aid solution, but a solution which will require collaboration of several parts of the organisations, orchestrated by the CEO herself.

Raz Chorev is Partner at Orange Sky and Managing Director at CXC Global. He is based in Sydney, Australia.

Julie’s Answer

The Auditor General has asked management to respond and board oversight of management should be done by and through the CEO.

Kyle cannot help without putting his fingers (or intellect) into the organisation. To do that without causing upset he will need to inform the CEO of the Chairman’s request, offer to help and make sure that he reports to her before he reports elsewhere. Handled sensitively the CEO, who appears to be struggling, should welcome any assistance with the task. Handled insensitively this could be a major issue because the statutory definitions of directors’ roles in public sector companies are less fluid than those in the private sector.

Kyle should also take this as a wake-up call – he assumes a culture of compliance and good governance but that is obviously not correct. The audit committee should regularly review the regulatory and legislative compliance framework and verify that all is as it should be; that has clearly not happened and Kyle should work with the company secretary or chief compliance/legal officer to review the entire framework and make sure nothing else is missing from the regular schedule of reviews. The committee must ask for what it needs to oversight effectively not just read what they are given.

The prevailing attitude should be one of thankfulness that the issue has been found and can be corrected. If Kyle detects a cultural rejection of the need to comply and cooperate with the AG in establishing good governance then Kyle must report to the whole board so remedial action can be planned.

Once management have responded to the AG with their proposed actions to remedy the matter. The audit committee should review to check that the actions have been implemented and that they effectively lead to compliance with the requirements. Likely remedies include amending the position descriptions of staff doing tendering or those setting up vendors in the payments system to include entry of details to the register, training in compliance, design of an internal audit system for routine review of registers and comparison to workloads to ensure that nothing has ‘dropped between the cracks’, and regular reporting of register completion and audit to the board audit committee.

Sean’s Answer

The Audit Risk and Compliance Committee (« Committee ») is to assist the Board in fulfilling its corporate governance and oversight responsibilities in relation to the bodies’ financial reporting, internal control structure, risk management systems, compliance and the external audit function.

The external auditors are responsible for auditing the bodies’ financial reports and for reviewing the unaudited interim financial reports. The Financial Management and Accountability Act 1997 calls for auditing financial statements and performance reviews by the Auditor General.

As Committee Chairman Kyle must be independent and must have leadership experience and a strong finance, accounting or business background. So too must the CEO and CFO have appropriate and sufficient qualifications, knowledge, competence, experience and integrity and other personal attributes to undertake their roles.

It should be the responsibility of the Committee to maintain free and open communication between the Committee, external auditors and management. The Committee’s function is principally oversight and review.

The appointment and ongoing assessment, mentoring and discipline of the CEO rests with the board but the delegation of this authority in relation to compliance often rests with the Committee and Board Chairs.

Kyle may invite members of management (CFO and maybe the CEO) or others to attend meetings and the Committee should have authority, within the scope of its responsibilities, to seek information it requires, and assistance from any employee or external party. Inviting the CFO and or CEO to the Committee allows visibility and a holistic and independent forum where deficiencies may be isolated and functions (but not responsibility) delegated to others.

There is a disconnect or deficiency in one or more functions; Kyle should ensure that the Committee holistically review its own charter, discuss with management and the external auditors the adequacy and effectiveness of the internal controls and reporting functions (including the Bodies’s policies and procedures to assess, monitor and manage these controls), as well as a review of the internal quality control procedures (because these are also suspected to be deficient).

It will rapidly become apparent to management, the Committee, Kyle, the board and the Chairman where the deficiencies lie or did lie, and how they have been corrected. Underlying behavioural problems and or abilities to function will also become apparent and with these appropriately addressed similar deficiencies in other areas of the body may be contemporaneously corrected and all reported to the Auditor General.

Sean Rothsey is Chairman and Founder of the Merkin Group. He is based in Cooroy, Queensland, Australia.

Voici le rapport annuel toujours très attendu de Spencer Stuart*.

Ce document présente un compte rendu très détaillé de l’état de la gouvernance dans les grandes sociétés publiques américaines (S&P 500).

On y découvre les résultats des changements dans le domaine de la gouvernance aux É.U. en 2016, ainsi que certaines tendances pour 2017.

Les thèmes abordés sont les suivants :

La composition des Boards

L’indépendance du président du CA

Les mandats des administrateurs et les limites aux nombres de mandats

L’âge de la retraite des administrateurs

L’évaluation des Boards

La nature des relations du Boards et de la direction avec les actionnaires

L’amélioration de la performance des Boards

Diverses informations, notamment :

Only 19% of new independent directors are active CEOs, chairs, presidents and chief operating officers, compared with 24% in 2011, 29% in 2006 and 49% in 1998, the first year we looked at this data for S&P 500 companies.

Active executives with financial backgrounds (CFOs, other financial executives, as well as investors and bankers) represent 15% of new independent directors this year, an increase from 12% last year. Another 10% of new directors are retired finance and public accounting executives.

On average, S&P 500 directors have 2.1 outside corporate board affiliations, although most directors aren’t restricted from serving on more.

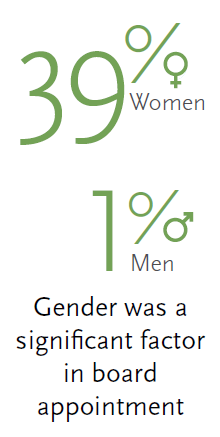

The number of boards with no female directors dropped to the lowest level we have seen; six S&P 500 boards (1%) have no women, a noteworthy decline from 2006, when 52 boards (11%) included no female members. Women now constitute 21% of all S&P 500 directors.

Among the boards of the 200 largest S&P companies, the total number of minority directors has held steady at 15% since 2011. 88% of the top 200 companies have at least one minority director, the same as 10 years ago.

Only 43% of S&P 500 CEOs serve on one or more outside corporate boards in addition to their own board, the same as in 2015. In 2006, 55% of CEOs served on at least one outside board.

Boards met an average of 8.4 times for regularly scheduled and special meetings, up from 8.1 last year and 8.2 five years ago. The median number of meetings rose from 7.0 last year to 8.0.

The average annual total compensation for S&P 500 directors, excluding the chairman’s compensation, is $280,389.

Over time, the compensation mix for directors has evolved, with more stock grants and fewer stock options. Today, stock grants represent 54% of total director compensation, versus 48% five years ago, while stock options represent 6% of compensation today, down from 10% five years ago. Cash accounts for 38% of director compensation, versus 39% in 2011.

95% of the independent chairmen of S&P 500 boards receive an additional fee, averaging $165,112. Nearly two-thirds of lead and presiding directors, 65%, receive additional compensation. The average premium paid to lead and presiding directors is $33,354.

Investor attention to board performance and governance continues to escalate, and, increasingly, it’s large institutional investors—so-called “passive” investors—who are making known their expectations in areas such as board composition, disclosure and shareholder engagement. Long-term investors have shifted their posture to taking positions on good governance, and are increasingly demonstrating common ground with activists on governance topics.

Board composition is a particular area of focus, as traditional institutional investors have become more explicit in demanding that boards demonstrate that they are being thoughtful about who is sitting around the board table and that directors are contributing. They are looking more closely at disclosures related to board refreshment, board performance and assessment practices, in some cases establishing voting policies on governance.

Boards are taking notice. Directors want to ensure that their boards contribute at the highest level, aligning with shareholder interests and expectations. In response, boards are enhancing their disclosures on board composition and leadership, reviewing governance practices and establishing protocols for engaging with investors. Here are some of the trends we are seeing in the key areas of investor concern.

Board composition

The composition of the board—who the directors are, the skills and expertise they bring, and how they interact—is critical for long-term value creation, and an area of governance where investors increasingly expect greater transparency. Shareholders are looking for a well-explained rationale for why the group of people sitting around the board table are the right ones based on the strategic priorities of the business. They want to know that the board has the processes in place to review and evolve board composition in light of emerging needs, and that the board regularly evaluates the contributions and tenure of current board members and the relevance of their experience.

Acknowledging investor interest in their composition, more boards are reviewing how to best communicate their thinking about the types of expertise needed in the board—and how individual directors provide that expertise. More than one-third of the 96 corporate secretaries responding to our annual governance survey, conducted each year as part of the research for the Spencer Stuart Board Index, said their board has changed the way it reports director bios/qualifications; among those that have not yet made changes, 15% expect the board to change how they present director qualifications in the future.

What’s happening to board composition in practice after all of the talk about increasing board turnover? In 2016, we actually saw a small decline in the number of new independent directors elected to S&P 500 boards. S&P 500 boards included in our index elected 345 new independent directors during the 2016 proxy year—averaging 0.72 new directors per board. Last year, S&P 500 boards added a total of 376 new directors (0.78 new directors per board).

Nearly one-third (32%) of the new independent directors on S&P 500 boards are serving on their first outside corporate board. Women account for 32% of new directors, the highest rate of female representation since we began tracking this data for the S&P 500. This year’s class of new directors, however, includes fewer minority directors (defined as African-American, Hispanic/Latino and Asian); 15% of the 345 new independent directors are minorities, a decrease from 18% in 2015.

With the rise of shareholder activism, we’ve also seen an increase in investors and investment managers on boards. This year, 12% of new independent directors are investors, compared with 4% in 2011 and 6% in 2006.

Independent board leadership

Boards continue to feel pressure from some shareholders to separate the chair and CEO roles and name an independent chairman. And, indeed, 27% of S&P 500 boards, versus 21% in 2011, have an independent chair. An independent chair is defined as an independent director or a former executive who has met applicable NYSE or NASDAQ rules for independence over time. This actually represents a small decline from 29% last year. Meanwhile, naming a lead director remains the most common form of independent board leadership: 87% of S&P 500 boards report having a lead or presiding director, nearly all of whom (98%) are identified by name in the proxy.

In our governance survey, 12% of respondents said their board has recently separated the roles of chairman and CEO, while 33% said their board has discussed whether to split the roles within the next five years. Among boards that expect to or have recently separated the chair and CEO roles, 72% cite a CEO transition as the reason, while 20% believe the chair/CEO split represents the best governance.

In response to investor interest in board leadership structure—and sometimes demands for an independent chairman—more boards are discussing their leadership structure in their proxies, for example, explaining the rationale for maintaining a combined chair/CEO role and delineating the responsibilities of the lead director. Among the lead director responsibilities boards highlight: approving the agenda for board meetings, calling meetings and executive sessions of independent directors, presiding over executive sessions, providing board feedback to the CEO following executive sessions, leading the performance evaluation of the CEO and the board assessment, and meeting with major shareholders or other external parties, when necessary. Some proxies include a letter to shareholders from the lead independent director.

Tenure and term limits

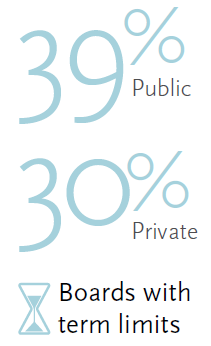

Director tenure continues to be a hot topic for some shareholders. While some rating agencies and investors have questioned the independence of directors with “excessive” tenure, there are no specific regulations or listing standards in the U.S. that speak to director independence based on tenure. And, in fact, most companies do not have governance rules limiting tenure; only 19 S&P 500 boards (4%) set an explicit term limit for non-executive directors, a modest increase from 2015 when 13 boards (3%) had director term limits.

Just 3% of survey respondents said their boards are considering establishing director term limits, but many boards are disclosing more in their proxies about director tenure. Specifically, boards are describing their efforts to ensure a balance between short-tenured and long-tenured directors. And several companies have included a short summary of the board’s average tenure accompanied by a pie chart breaking down the tenure of directors on the board (e.g., directors with less than five years tenure, between five and 10 years, and more than 10 years tenure on the board).

Among S&P 500 boards overall, the average board tenure is 8.3 years, a slight decrease from 8.7 five years ago. The median tenure has declined as well in that time, from 8.4 to 8.0. The majority of boards, 63%, have an average tenure between six and 10 years, but 19% of boards have an average tenure of 11 or more years.

We also looked this year at the tenure of individual directors: 35% of independent directors have served on their boards for five years or less, 28% have served for six to 10 years, and 22% for 11 to 15 years. Fifteen percent of independent directors have served on their boards for 16 years or more.

Mandatory retirement

In the absence of term or tenure limits, most S&P 500 boards rely on mandatory retirement ages to promote turnover. About three-quarters (73%) of S&P 500 boards report having a mandatory retirement age for directors. Eleven percent report that they do not have a mandatory retirement age, and 16% do not discuss mandatory retirement in their proxies.

Retirement ages have crept up in recent years, as boards have raised them to allow experienced directors to serve longer. Thirty-nine percent of boards have mandatory retirement ages of 75 or older, compared with 20% in 2011 and just 9% in 2006. Four boards have a retirement age of 80. The most common mandatory retirement age is 72, set by 45% of S&P 500 boards.

As retirement ages have increased, so has the average age of independent directors. The average age of S&P 500 independent directors is 63 today, two years older than a decade ago. In that same period, the median age rose from 61 to 64. Meanwhile, the number of older boards has increased; 37% of S&P 500 boards have an average age of 64 or older, compared with 19% a decade ago, and 15 of today’s boards (3%) have an average age of 70 or greater, versus four (1%) a decade ago.

Board evaluations

Another topic on which large institutional investors have become more vocal is board performance evaluations. Shareholders are seeking greater transparency about how boards address their own performance and the suitability of individual directors—and whether they are using assessments as a catalyst for refreshing the board as new needs arise.

We have seen a growing trend in support of individual director assessments as part of the board effectiveness assessment—not to grade directors, but to provide constructive feedback that can improve performance. Yet the pace of adoption of individual director assessments has been measured. Today, roughly one-third (32%) of S&P 500 boards evaluate the full board, committees and individual directors annually, an increase from 29% in 2011.

In our survey of corporate secretaries, respondents said evaluations are most often conducted by a director, typically the chairman, lead director or a committee chair. A wide range of internal and external parties are also tapped to conduct board assessments, including in-house and external legal counsel, the corporate secretary and board consulting firms. Thirty-five percent use director self-assessments, and 15% include peer reviews. According to proxies, a small number of boards, but more than in the past, disclose that they used an outside consultant to facilitate all or a portion of the evaluation process.

Shareholder engagement

In light of investors’ growing desire for direct engagement with directors, more boards have established frameworks for shareholders to raise questions and engage in meaningful, two-way discussions with the board. In addition to improving disclosures about board composition, assessment and other key governance areas, some boards include in their proxies a summary of their shareholder outreach efforts. For example, they detail the number of investors the board met with, the issues discussed and how the company and board responded. A few boards facilitate direct access to the board by providing contact information for individual directors, including the lead director and audit committee chair.

Going further, many boards now proactively reach out to their company’s largest shareholders. In our survey, 83% of respondents said management or the board contacted the company’s large institutional investors or largest shareholders, an increase from 70% the year prior. The most common topic about which companies engaged with shareholders was proxy access (52%), an increase from 33% in 2015. Other topics included “say on pay” (51%), CEO compensation (40%), director tenure (30%), board refreshment (27%), shareholder engagement approach (27%) and chairman independence (24%). Survey respondents also wrote in more than a dozen additional topics, including majority/cumulative voting, disclosure enhancements, environmental issues and gender pay equity.

Enhancing board performance

The topic of board refreshment can be a highly charged one for boards. But having the right skills around the table is critical for the board’s ability to provide the appropriate guidance and oversight of management. Furthermore, the capabilities and perspectives that a board needs evolve over time as the business context changes. Boards can ensure that they have the right perspectives around the table and are well-equipped to address the issues that drive shareholder value—which, after all, is what investors are looking for—by doing the following:

Viewing director recruitment in terms of ongoing board succession planning, not one-off replacements. Boards should periodically review the skills and expertise on the board to identify gaps in skills or expertise based on changes in strategy or the business context.

Proactively communicating the skill sets and expertise in the boardroom—and the roadmap for future succession. Publishing the board’s skill matrix and sharing the board’s thinking about the types of expertise that are needed on the board—and how individual directors provide that expertise—signals to investors that the board is thoughtful about board succession.

Setting expectations for appropriate tenure both at the aggregate and individual levels. By setting term expectations when new directors join, boards can combat the perceived stigma attached to leaving a board before the mandatory retirement age. Ideally, boards will create an environment where directors are willing to acknowledge when the board would benefit from bringing on different expertise.

Thinking like an activist and identifying vulnerabilities in board renewal and performance. Proactive boards conduct board evaluations annually to identify weaknesses in expertise or performance. They periodically engage third parties to manage the process and are disciplined about identifying and holding themselves accountable for action items stemming from the assessment.

Establishing a framework for engaging with investors. This starts with proactive and useful disclosure, which demonstrates that the board has thought about its composition, performance and other specific issues. In addition, it is valuable to have a protocol in place enumerating responsibilities related to shareholder engagement.

*Note: The Spencer Stuart Board Index (SSBI) is based on our analysis of the most recent proxy reports from the S&P 500, plus an extensive supplemental survey. The complete publication draws on the latest proxy statements from 482 companies filed between May 15, 2015, and May 15, 2016, and responses from 96 companies to our governance survey conducted in the second quarter of 2016. Survey respondents are typically corporate secretaries, general counsel or chief governance officers. Proxy and survey data have been supplemented with information compiled in Spencer Stuart’s proprietary database.

The complete publication, including footnotes, is available here.

Voici un article publié sur le site de la HLS par Michael McCauley* qui montre comment la Florida State Board of Administration (SBA) évalue la gouvernance des entreprises dans laquelle elle investit.

Il m’apparaît utile de comprendre le processus décisionnel des investisseurs institutionnels, si l’on veut connaître les variables de la gouvernance dont elles tiennent compte.

L’auteur explique la méthodologie utilisée par la SBA dans sa quête d’information sur les entreprises visées.

The Florida SBA’s annual corporate governance summary explains how the Board makes proxy voting decisions, describes the process and policies used to analyze corporate governance practices, and details significant market issues affecting global corporate governance practices at owned companies. The SBA acts as a strong advocate and fiduciary for Florida Retirement System (FRS) members and beneficiaries, retirees, and other non-pension clients to strengthen shareowner rights .and promote leading corporate governance practices at U.S. and international companies in which the SBA holds stock.

The SBA’s corporate governance activities are focused on enhancing share value and ensuring that public companies are accountable to their shareowners with independent boards of directors, transparent disclosures, accurate financial reporting, and ethical business practices designed to protect the SBA’s investments.

The SBA’s annual corporate governance summary is designed to provide transparency of investment management activities involving responsible investment practices, proxy voting conduct, and engagement with owned companies. The report broadly conforms to the main principles for external responsibilities endorsed by the International Corporate Governance Network’s (ICGN) Global Stewardship Principles, most recently updated in June 2016. The ICGN Global Stewardship Principles provide a framework to implement stewardship practices in fulfilling an investor’s fiduciary obligations to beneficiaries or clients.

In addition to comprehensive data and information on corporate engagement, proxy voting, and regulatory issues, the complete 2016 report includes four topical sections detailed below:

Governance Patterns in the U.S. Banking Sector—market events this year demonstrate how a company’s governance regime can interact with its reputation and value.

CFOs serving on Boards in the UK—why is the British market so conducive for executives, including the CFO, to serve on their own boards?

Rule 14a-8 Governing Shareowner Resolutions—is it time for a more efficient way to make shareowner proposals during annual meetings?

UK Compensation Revolt—along with votes targeted at individual board members, investor votes on executive compensation exhibited high levels of dissent at many UK companies.

Annual Voting Review

During the 2016 proxy season, the SBA cast votes at over 10,300 public companies, voting more than 97,000 individual ballot items. The SBA actively engages portfolio companies throughout the year, addressing corporate governance concerns and seeking opportunities to improve alignment with the interests of our beneficiaries. Highlights from the 2016 proxy season included the continued record adoption of proxy access by U.S. companies, record high votes of dissent on pay packages for executives in the United Kingdom, and strong improvements in the level of independence among Japanese boards of directors. While SBA voting principles and guidelines are not pre-disposed to agree or disagree with management recommendations, some management positions may not be in the best interest of all shareowners. On behalf of participants and beneficiaries, the SBA emphasizes the fiduciary responsibility to analyze and evaluate all management recommendations very closely.

Across all voting items, the SBA voted 76.5 percent “For,” 20.2 percent “Against,” 3.1 percent “Withheld,” and 0.2 percent “Abstained” or “Did Not Vote” (due to various local market regulations or liquidity restrictions placed on voted shares). Of all votes cast, 22.2 percent were “Against” the management-recommended-vote (up from 19.4 percent during the same period last year). Among all global proxy votes, the SBA cast at least one dissenting vote at 7,689 annual shareowner meetings, or 74.6 percent of all meetings.

Director Elections

In uncontested director elections among all companies in the United States that are part of the Russell 3000 stock index, over 16,000 nominees received 96.1 percent average support from investors. This year’s figure was within two tenths of one percent from 2015’s statistic. Only 46 director nominees, or less than 0.3 percent, failed to receive a majority level of support from investors. Only two directors at large-capitalization companies within the Standard & Poor’s (S&P) 500 stock index failed to receive a majority level of support. Board elections represent one of the most critical areas in voting because shareowners rely on the board to monitor management. The SBA supported 78.5 percent of individual nominees for boards of directors, voting against the remaining portion of directors due to concerns about candidate independence, qualifications, attendance, or overall board performance. The SBA’s policy is to withhold support from directors who fail to observe good corporate governance practices or demonstrate a disregard for the interests of investors.

Executive Compensation

During the 2016 proxy season, the SBA utilized compensation research from Equilar, Inc., Glass, Lewis & Co., and Institutional Shareholder Services to assist in evaluating the proxy voting decisions on executive compensation share plans and general say-on-pay ballot items. Across all global equity markets, the SBA voted to approve approximately 55 percent of all remuneration reports, whereas in the U.S. market all other investors provided an average support level of 91.5 percent with only 1.5 percent of all advisory votes failing to achieve a majority. ISS found that over half of all U.S. companies conducting annual pay votes have received investor support of at least 90 percent in each of the last five years since the Dodd-Frank Act instituted advisory say-on-pay shareowner votes.

Among all U.S. companies, the average level of investor support for equity plan proposals stayed about the same year over year at approximately 88 percent. However, the number of individual equity plans that failed to garner majority support rose by 50 percent, from 6 to 9 plans. Given the extremely low number of equity plans that fail each year, investor support for individual plans is almost universal. Less than one percent of equity plans failed during the last year, which also marked a five-year low for the number of compensation-related investor proposals with not a single proposal receiving majority support. Over the last fiscal year, the SBA supported 51.2 percent of all non-salary (equity) compensation items, 60.8 percent of executive incentive bonus plans, and 25.2 percent of management proposals to approve omnibus stock plans in which company executives would participate (and 19.3 percent support for the amendment of such plans). Omnibus stock plan ballot items typically include ratification of more than one equity plan beyond a company’s long-term incentive plan (LTIP).

Asset Owner/Asset Manager Peer Benchmarking

In May 2016, the SBA completed an international benchmarking survey on the costs of corporate governance activities at seventeen large public pension funds and global asset managers. The information helped SBA staff to assess the Investment Programs & Governance (IP&G) unit’s cost structure and service utilization across a large number of direct peers. When total research and voting services costs were calculated, SBA had the second lowest dollar-cost per proxy vote among public fund peers and asset managers. The SBA also ranked among the top three funds and well ahead of the fourteen remaining peers with respect to the proxy votes cast per full-time employee. The benchmarking showed that SBA’s corporate governance program uses similar services to peers, but does so at considerably lower cost and with greater efficacy. Our overall program costs and activity levels, particularly when standardized by assets under management, were very favorable compared to peers.

Active Ownership

The SBA actively engages portfolio companies throughout the year, addressing corporate governance concerns and seeking opportunities to improve alignment with the interests of our beneficiaries. During the 2016 fiscal year, SBA staff conducted engagements with over 100 companies owned within Florida Retirement System portfolios, including Compass Group PLC, Microsoft, Coca-Cola, Prudential, Bank of Yokohama, Chevron, Bank of America, ENI, Amgen, Ethan Allen, Oracle, The Goldman Sachs Group, JPMorgan, RTI Surgical, Boeing, Terna Group SpA, Regions Financial Corporation, Red Electrica, and Time Warner. As part of evaluating voting decisions for several proxy contests, SBA staff also met with a number of activist hedge funds, including Red Mountain Capital (proxy campaign at iRobot), Harvest Capital (proxy campaign at Green Dot), and SilverArrow Capital (proxy campaign at Rofin-Sinar Technologies).

Notable Votes

There were numerous significant votes during the 2016 global proxy season, including proxy contests at iRobot Corporation in May and Ashford Hospitality Prime in June, the Facebook share reclassification in June, and the Stada Arzneimitell AG meeting in August. The SBA makes informed and independent voting decisions at investee companies, applying due care, intelligence, and judgment. The SBA makes all proxy voting decisions independently, casting votes based on written, internally-developed corporate governance principles and proxy voting guidelines that cover all expected ballot issues. More detail on each of these votes and the related SBA analysis is contained in the ‘Highlighted Proxy Votes’ section of the 2016 Annual Summary.

The SBA prepares additional reports on corporate governance topics and significant market developments, covering a wide range of shareowner issues. Historical information can be found within the governance section of the SBA’s website. (www.sbafla.com)

The complete publication is available on the SBA’s website here and can also be viewed here using the Issuu e-reader tool.

*Michael McCauley is Senior Officer, Investment Programs & Governance, of the Florida State Board of Administration (the “SBA”). This post is based on an excerpt from the SBA’s 2016 Corporate Governance Report written by Mike McCauley, Jacob Williams, Tracy Stewart, Hugh Brown, and Logan Rand.

La scène de l’activisme actionnarial a drastiquement évolué au cours des vingt dernières années. Ainsi, la perception négative de l’implication des « hedge funds » dans la gouvernance des organisations a pris une tout autre couleur au fil des ans.

Les fonds institutionnels détiennent maintenant 63 % des actions des corporations publiques. Dans les années 1980, ceux-ci ne détenaient qu’environ 50 % du marché des actions.

L’engagement actif des fonds institutionnels avec d’autres groupes d’actionnaires activistes est maintenant un phénomène courant. Les entreprises doivent continuer à perfectionner leur préparation en vue d’un assaut éventuel des actionnaires activistes.

L’article de Merritt Moran* publié sur le site du Harvard Law School Forum on Corporate Governance, est d’un grand intérêt pour mieux comprendre les changements amenés par les actionnaires activistes, c’est-à-dire ceux qui s’opposent à certaines orientations stratégiques des conseils d’administration, ainsi qu’à la toute-puissance des équipes de direction des entreprises.

L’auteure présente dix activités que les entreprises doivent accomplir afin de décourager les activistes, les incitant ainsi à aller voir ailleurs !

Voici la liste des étapes à réaliser afin d’être mieux préparé à faire face à l’adversité :

Préparez un plan d’action concret ;

Établissez de bonnes relations avec les investisseurs institutionnels et avec les actionnaires ;

La direction doit entretenir une constante communication avec le CA ;

Mettez en place de solides pratiques de divulgations ;

Informez et éduquez les parties prenantes ;

Faites vos devoirs et analysez les menaces et les vulnérabilités susceptibles d’inviter les actionnaires activistes ;

Communiquez avec les actionnaires activistes et tentez de comprendre les raisons de leurs intérêts pour le changement ;

Comprenez bien tous les aspects juridiques relatifs à une cause ;

Explorez les différentes options qui s’offrent à l’entreprise ciblée ;

Apprenez à connaître le rôle des autorités réglementaires.

J’espère vous avoir sensibilisé à l’importance de la préparation stratégique face à d’éventuels actionnaires activistes.

Shareholder activism is a powerful term. It conjures the image of a white knight, which is ironic because these investors were called “corporate raiders” in the 1980s. A corporate raider conjures a much different image. As much as that change in terminology may seem like semantics, it is critical to understanding how to deal with proxy fights or hostile takeovers. The way someone is described and the language used are crucial to how that person is perceived. The perception of these so-called shareholder activists has changed so dramatically that, even though most companies’ goals are still the same, the playbook for dealing with activists is different than the playbook for corporate raiders. As such, a corresponding increase in the number of activist encounters has made that playbook required reading for all public company officers and directors. In fact, there have been more than 200 campaigns at U.S. public companies with market capitalizations greater than $1 billion in the last 10 quarters alone. [1]

It’s not just the terminology concerning activists that has changed, though. Technologies, trading markets and the relationships activists have with other players in public markets have changed as well. Yet, some things have not changed.

The 1980s had arbitrageurs that would often jump onto any opportunity to buy the stock of a potential target company and support the plans and proposals raiders had to “maximize shareholder value.” Inside information was a critical component of how arbs made money. Ivan Boesky is a classic example of this kind of trading activity—so much so that he spent two years in prison for insider trading, and is permanently barred from the securities business. Arbs have now been replaced by hedge funds, some of which comprise the 10,000 or so funds that are currently trying to generate alpha for their investors. While arbitrageurs typically worked inside investment banks, which were highly regulated institutions, hedge funds now are capable of operating independently and are often willing allies of the 60 to 80 full time “sophisticated” activist funds. [2] Information is just as critical today as it was in the 1980s.

Institutions now occupy a far greater percentage of total share ownership today, with institutions holding about 63% of shares outstanding of the U.S. corporate equity market. In the 1980s, institutional ownership never crossed 50% of shares outstanding. [3] Not only has this resulted in an associated increase of voting power for institutions by the same amount, but also a change in their behavior and posture toward the companies in which they invest, at least in some cases. Thirty years ago, the idea that a large institutional investor would publicly side with an activist (formerly known as a “corporate raider”) would be a rare event. Today, major institutions have frequently sided with shareholder activists, and in some cases privately issued a “Request for Activism”, or “RFA” for a portfolio company, as it has become known in the industry.

It seldom, if ever, becomes clear as to whether institutions are seeking change at a company or whether an activist fund identifies a target and then seeks institutional support for its agenda. What is clear is that in today’s form of shareholder activism, the activist no longer needs to have a large stake in the target in order to provoke and drive major changes.

For example, in 2013, ValueAct Capital held less than 1% of Microsoft’s outstanding shares. Yet, ValueAct President, G. Mason Morfit forced his way onto the board of one of the world’s largest corporations and purportedly helped force out longtime CEO Steve Ballmer. How could a relatively low-profile activist—at the time at least—affect such dramatic change? ValueAct had powerful allies, which held many more shares of Microsoft than the fund itself who were willing to flex their voting muscle, if necessary.

The challenge of shareholder activism is similar to, yet different from, that which companies faced in the 1980s. Although public markets have changed tremendously since the 1980s, market participants are still subject to the same kinds of incentives today as they were 30 years ago.

It has been said that even well performing companies, complete with a strong balance sheet, excellent management, a disciplined capital allocation record and operating performance above its peers are not immune. In our experience, this is true. When the amount of capital required to drive change, perhaps unhealthy change, is much less costly than it is to acquire a material equity position for an activist, management teams and boards of directors must navigate carefully.

Below are 10 building blocks that we believe will help position a company to better equip itself to handle the stresses and pressures from the universe of activist investors and hostile acquirers, which may encourage the activists to instead knock at the house next door.

Building Block 1: Be Prepared

Develop a written plan before the activist shows up. By the time a Schedule 13-D is filed, an activist already has the benefit of sufficient time to study a target company, develop a view of its weaknesses and build a narrative that can be used to put a management team and board of directors on the defensive. Therefore, a company’s plan must have balance and must contemplate areas that require attention and improvement. While some activists are akin to 1980s-style corporate raiders with irrational ideas designed only to bump up the stock over a very short period, there are also very sophisticated activists who are savvy and have developed constructive, helpful ideas. A company’s plan and response protocol need to be well thought through and in place before an activist appears. In some cases, the activist response plan can be built into a company’s strategic plan.

The plan needs inclusion and buy-in from the board of directors and senior management. Some subset of this group needs to be involved in developing the plan, not only substantively, but also in the tactical aspects of implementing the plan and communicating with shareholders, including activists, if and when an activist appears.

This preparatory building block extends beyond simply having a process in place to react to shareholder activism. It should complement the company’s business plan and include the charter and bylaws and consideration of traditional takeover defense strategies. It should provide for an advisory team, including lawyers, bankers, a public relations firm and a forensic accounting firm. We believe that the plan should go to a level of detail that includes which members of management and the board are authorized by the board to communicate with the activist and how those communications should occur.

Building Block 2: Promote Good Shareholder Relations with Institutions and Individual Shareholders

If the lesson of the first block was “put your own house in order,” then the second lesson is, “know your tenants, what they want, and how they prefer to live in your building.” This goes well beyond the typical investor relations function. This is where in-depth shareholder research comes into play. We recommend conducting a detailed perception study that can give boards and management teams a clear picture of what the current shareholder base wants, as well as how former and prospective shareholders’ perceptions of the company might differ from the way management and the board see the company itself.

In a takeover battle or proxy contest, facts are ammunition. Suppositions and assumptions of what management thinks shareholders want are dangerous. It is critical to understand how shareholders feel about the dividend policy and the capital allocation plans, for example. Understand how they view the executive compensation or the independence of the board. Do not assume. Ask candidly and revise periodically.

Building Block 3: Inform, Teach and Consult with the Board

Good governance is not something that can be achieved in a reactive sort of manner or when it becomes known that an activist is building a position. Without shareholder-friendly corporate governance practices, the odds of securing good shareholder relations in a contest for control drops significantly and creates the wrong optics.

There are governance issues that can cause institutional shareholders to act, or at least think, akin to activists. Recently, there have been various shareholder rebellions against excessive executive compensation packages—or say-on-pay votes. In fact, Norges, the world’s largest sovereign wealth fund, has launched a public campaign targeting what it views as excessive executive compensation. The fund’s chief executive told the Financial Times that, “We are looking at how to approach this issue in the public space.” He is speaking for an $870 billion dollar fund. The way those votes are cast can mean the difference between victory and defeat in a proxy contest.

Building Block 4: Maintain Transparent Disclosure Practices

While this building block relates to maintaining good shareholder relations, it also recognizes that activists are smart, well informed, motivated and relentless. If a company makes a mistake, and no company is perfect, the activist will likely find it. Companies have write-downs, impairments, restatements, restructurings, events of change or challenges that affect operating performance. While any one of these events may invite activist attention, once a contest for control begins, an activist will find and use every mistake the company ever made and highlight the material ones to the marketplace.

A company cannot afford surprises. One “whoops” event can be all it takes to turn the tide of a proxy vote or a hostile takeover. That is why it is critical to disclose the good and the bad news before the contest begins rather than during the takeover attempt. It may be painful at the time, but with a history of transparency, the marketplace will trust a company that tells them the activist is in it for its own personal benefit and that the proposal the activist is making will not maximize shareholder value, but will only increase the activist’s short-term profit for its investors. Developing that kind of trust and integrity over time can be a critical factor in any contest for corporate control, especially when research shows that the activist has not been transparent in its prior transactions or has misled investors prior to or after achieving its intended result.

When a company has established good corporate governance policies, has been open and transparent, has financial statements consistent with GAAP and effective internal control over financial reporting and knows its shareholder base cold, what is the next step in preparing for the challenge of an activist shareholder?

Building Block 5: Educate Third Parties

Prominent sell-side analysts and financial journalists can, and do, move markets. In a contest for corporate control, or even in a short slate proxy contest, they can be invaluable allies or intractable adversaries. As with the company’s shareholder base, one must know the key players, have established relationships and trust long before a dispute, and have the confidence that the facts are on the company’s side. But winning them over takes time and research, and is another area where an independent forensic accounting firm can be of assistance.

For example, when our client, Allergan, was fighting off a hostile bid from Valeant and Pershing Square, we identified that Valeant’s “double-digit” sales growth came from excluding discontinued products and those with declining sales from its calculation. This piece of information served as key fodder for journalists, who almost unanimously sided against Valeant for this and other reasons. Presentations, investor letters and analyst days can make the difference in creating a negative perception of the adversary and spreading a company’s message.

Building Block 6: Do Your Homework

Before an activist appears, a company needs to understand what vulnerabilities might attract an activist in the first place. This is where independent third parties can be crucial. Retained by a law firm to establish the privilege, they can do a vulnerability assessment of the company compared to its peers.

This is a different sort of assessment than what building block two entails, essentially asking shareholders to identify perceived weaknesses. Here, a company needs to look for the types of vulnerabilities that institutional shareholders might not see—but that an activist surely will. When these vulnerabilities such as accounting practices or obscure governance structures are not addressed, an activist will use them on the offensive. Even worse are the vulnerabilities that are not immediately apparent. In any activist engagement, it is best to minimize surprises as much as possible.

Building Block 7: Communicate With the Activist

Before deciding whether to communicate, know the other players.

This includes a deep dive into the activist’s history—what level of success has the activist had in the past? Have they targeted similar companies? What strategies have they used? How do they negotiate? How have other companies reacted and what successes or failures have they experienced?

If the activist commences a proxy contest or a consent solicitation, turn that intelligence apparatus on the slate of board nominees the activist is proposing. Find out about their vulnerabilities and paint the full picture of their business record. Do they know the industry? Are they responsible fiduciaries? What is their personal track record? These are important questions that investigators can help answer.

Armed with information about the activist and having consulted with management, the board has to decide whether to communicate with the activist, and if so, what the rules of the road are for doing so. What are the objectives and goals and what are the pros and cons of even starting that communication process? If a decision is made to start communications with the activist, make sure to pick the time to do so and not just respond to what the media hype might be promoting. Poison pills can provide breathing room to make these determinations.

Always keep in mind that communications can lead to discussions, which in turn can lead to negotiations, which may result in a deal.

Before reaching a settlement deal, a company must be sure to have completed the preceding due diligence. More companies seem to be choosing to appease activists by signing voting agreements and/or granting board seats. Although this will likely buy more time to deal with the activist in private, it may simply delay an undesirable outcome rather than circumvent the issue. Whether or not the company signs a voting agreement with the activist, management and the board of directors should know the activist’s track record and current activities with other companies in great detail as the initial step in considering whether to reach any accommodation with the activist.

Building Block 8: Understand the Role of Litigation

Most of the building blocks thus far have involved making a business case to the marketplace and supporting that case with candid communications. But in many activist campaigns—especially the really adversarial ones—there will come a time when the company needs to make its case to a court or a regulator or both.

As with other building blocks, litigation goes to one of the most valuable commodities in a contest for corporate control: TIME. In most situations, the more time the target has to maintain the campaign, the better. The company’s legal team needs to work with the forensic accountants to understand and identify issues that relate to the activist’s prior transactions and business activities, while ensuring that the company is not living in a glass house when it throws stones. Armed with the facts, lawyers will do the legal analysis to determine whether the activist has complied with or broken state, federal or international law or regulation. If there are causes of action, then one way to resolve them is to litigate.

Building Block 9: Factor in Contingencies and Options

Contingencies can include additional activists, M&A and small issues that can become big issues. This building block is about understanding the environment in which the company is operating.