Voici un récent article publié par Julie Hembrock Daum, directrice à Spencer Stuart et Susan Stauberg, PDG à Fondation WomenCorporateDirectors.

Cet article a été publié dans le Harvard Law School Forum aujourd’hui et il présente l’état de la gouvernance à l’échelle internationale (60 pays) en mettant particulièrement l’accent sur la diversité et les différences de perception entre les hommes et les femmes qui occupent des postes d’administrateurs de grandes sociétés privées ou publiques.

On me demande souvent de proposer des références en relation avec la gouvernance globale. Les gens veulent connaître les tendances et les progrès des efforts entrepris dans le domaine de la diversité dans le monde.

L’enquête citée ci-dessous fournit des données actuelles sur les principaux enjeux concernant les Board.

Je crois que tous les gestionnaires seront intéressés par la présentation succincte, claire et bien illustrée des données de la mondialisation de la gouvernance.

The growing demands on corporate boards are transforming boardrooms globally, with directors taking on a more strategic, dynamic and responsive role to help steer their companies through a hypercompetitive and volatile business environment. Economic and political uncertainties make long-term planning more difficult. The proliferation of cyber attacks—and their consequences for business in financial olosses and reputational damage—increases the scope of risk oversight. A rise in institutional and activist shareholder activity requires boards to identify vulnerabilities in board renewal and performance and, in some cases, establish protocols for engagement. And all of these demands have pushed issues around board composition and diversity to the fore, as boards cannot afford to have directors around the table who aren’t delivering value.

Boardroom presentation

In this context, Spencer Stuart, the WomenCorporateDirectors (WCD) Foundation, Professor Boris Groysberg and doctoral candidate Yo-Jud Cheng of Harvard Business School and researcher Deborah Bell partnered together on the 2016 Global Board of Directors Survey, one of the most comprehensive surveys of corporate directors around the world.

We received responses from more than 4,000 male and female directors from 60 countries, providing a comprehensive snapshot of the business climate and strategic priorities as seen from the boardroom of many of the world’s top public and large, privately held companies.

The survey explores in depth how boards think and operate. It captures in detail the governance practices, strategic priorities and views on board effectiveness of corporate directors around the world. It also confirmed many of our observations from working with boards. The economy is top of mind, and many directors are uncertain about economic prospects and not seeing growth in the future. At the same time, directors are responding proactively to the many new demands they face, looking for opportunities to enhance composition and improve board performance.

Findings compare and contrast the views between male and female corporate board directors, and highlight similarities and differences between public and private companies and among directors from different regions in five key areas:

Political and economic landscape

Company strategy and risks

Board governance and effectiveness

Board diversity and quotas

Director identification and recruitment

This post highlights key findings around these topics, providing directors an overview of how their peers view their own boards and the challenges that their companies face. In subsequent reports, we will dive deeper into specific governance areas and explore additional perspectives on board composition, risk areas, and strengths and weaknesses in boardrooms today.

Key Findings

Political and Economic Landscape: Uncertainty dominates boardroom outlook.

Our survey finds that directors around the world are uncertain about global growth prospects, with directors in North America and Western Europe least confident about the prospects for growth. Sixty-three percent of directors in these regions see uncertain economic conditions, compared with 36% in Asia and 40% in Africa.

Only 2% of directors across all regions predict a period of strong global growth over the next three years, while 16% expect a global slowdown. “This pessimism about growth is one of the most surprising findings of our survey,” said Boris Groysberg of Harvard Business School. “It seems that the market volatility and low prospects for growth as well as the unpredictable economic outlook are what keep board members awake at night.”

More than one-third of directors of companies headquartered in Asia and roughly one-quarter of directors of companies in Australia/New Zealand expect relatively faster growth in emerging economies versus developed countries.

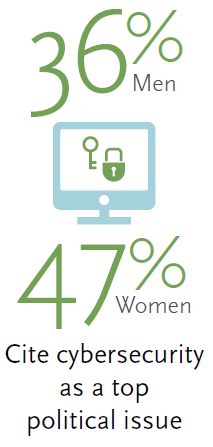

Political and Economic Landscape: Economy, regulations and cybersecurity top issues for directors.

Across all industries and regions, directors rank the economy and the regulatory environment as the political issues most relevant to them. Cybersecurity is an increasingly important issue in many regions. More than one-third of directors of companies in Australia/New Zealand, North America and Western Europe say cybersecurity is a top issue. “Cybersecurity continues to be a leading issue on the agenda from a regulatory, reputational and contingency standpoint,” says Julie Hembrock Daum, head of Spencer Stuart’s North American Board Practice.

“We see boards considering a number of different approaches to getting smart about the broader impact of technology on the business. In certain cases they have added a director with a strong digital or security background. However, the board should not isolate cybersecurity responsibility with just this one board member, but continue to view cybersecurity as a full board priority.”

Political instability is a concern in several regions. In Central and South America, one-half of directors cite political instability as an issue. Corporate tax rates are an issue particularly in North America.

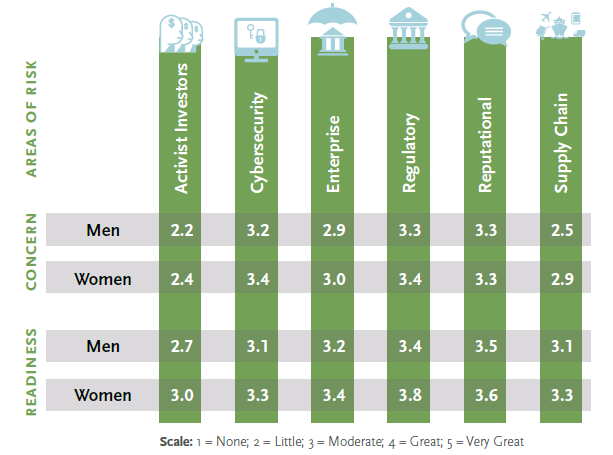

Company Risks: Women directors report higher concerns about risk than male directors.

Directors globally express the most concern about regulatory and reputational risks, followed by cybersecurity, and less about activist investors and supply chain risks. In general, directors report that their companies are prepared to handle the most important risks, with companies’ level of readiness matching the most concerning areas of risk. However, directors of private companies systematically rank their boards as being less prepared versus public company boards when it comes to such risks.

Nearly across the board, female directors report a higher level of concern about various risks to a company than their male peers—from concerns about activist investors and cybersecurity to regulatory risk and the supply chain. However, female directors also feel that their companies have a higher level of readiness to address these risks than do their male cohorts.

Susan Stautberg, chairman and CEO of the WCD Foundation, believes that women directors may be educating themselves more about the potential risks:

“We believe that women in particular bring a real thirst for knowledge and curiosity to their board service, and this includes getting up-to-speed on what the real risks are to an organization. All good directors do this, but we think being relatively new to the boardroom can create a greater sense of urgency to learn.”

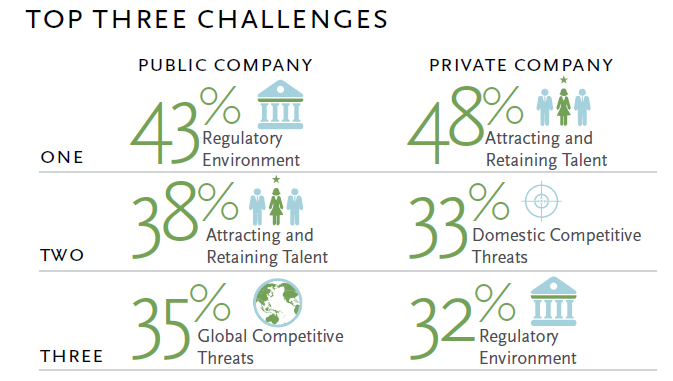

Strategy: Top challenges differ for public and private companies.

Talent, regulations, global and domestic competition, and innovation are seen by directors as the top impediments to achieving their companies’ strategic objectives. How those challenges rank specifically depends in part on whether directors are serving public or private companies.

Nearly half of private company directors (versus 38% of public company directors) rate attracting and retaining talent as a key challenge to achieving their company’s strategic objectives. This is followed by domestic competitive threats, the regulatory environment, innovation and global competitive threats. Among public companies, 43% of directors (versus 32% of private company directors) say the regulatory environment is a top challenge, followed by attracting and retaining talent, global competitive threats, innovation and domestic competitive threats.

“This was interesting because we do see in larger, more established public companies a greater maturity in their HR processes and deeper resources invested in talent management and development,” says Daum. “Identifying and recruiting individuals who fit the culture, bring impact to the organization and endure is a high priority for nearly all companies. However, many private companies, which tend to be smaller and have less brand awareness as a whole, often have less robust HR structures to attract the level of talent across the organization.”

Perceived challenges also differ somewhat by industry and region, with the regulatory environment being more concerning for companies in the energy/utilities, financials/professional services and healthcare industries, and in Asia, Australia/New Zealand, North America and Western Europe. Global competitive threats are the leading concern for companies in the industrials and materials sectors, and in Western Europe.

Interestingly, while cybersecurity is viewed as an important risk, few directors consider it a major challenge to achieving strategic objectives. Similarly, activist shareholders, compensation, cost of commodities and supply chain risk are not perceived as challenges to achieving strategic goals.

Boardroom Grades: Directors consider boards weaker in people-related processes.

On average, directors rate their board’s overall performance as being slightly above average (3.7 out of 5). Directors see their boards as having the strongest processes related to staying current on the company and the industry, compliance, financial planning and board composition, and weakest in cybersecurity, the evaluation of individual directors, CEO succession planning and HR/talent management.

“These ratings underscore directors’ views that attracting and retaining top talent is a common challenge, and underline the need for these HR competencies on boards,” says Stautberg. Harvard Business School doctoral candidate Yo-Jud Cheng adds, “Despite the fact that directors recognize their weaknesses in these areas, boards continue to prioritize more conventional areas of expertise, such as industry knowledge and auditing, in their appointments of new directors.”

Public company directors rate their overall board performance slightly higher than private company directors (3.8 versus 3.4) and give themselves higher marks for creating effective board structures, evaluation of individual directors, cybersecurity and compliance. We also see some variation across regions.

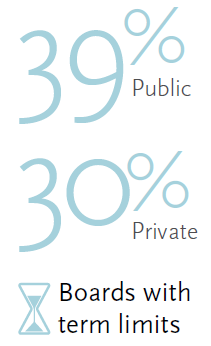

Board Turnover: Directors—especially women—favor tools to trigger change.

A little more than one-third of boards have term limits for directors, averaging six years, while approximately one-quarter of boards have a mandatory retirement age, averaging 72 years. Boards in Western Europe are most likely to have term limits, and boards in North America are least likely to set term limits. However, boards in North America are more likely to have a mandatory retirement age than boards in Western Europe (34% versus 18%). We also see a stark contrast between public and private companies in both term limits (39% versus 30%) and mandatory retirement ages (33% versus 12%).

While these tools for triggering director turnover generally have not been widely adopted, the survey indicates that directors favor adoption of such mechanisms. Sixty percent of directors think that boards should have mandatory term limits for directors, and 45% think that there should be a mandatory retirement age. Even in private companies, which are considerably less likely to adopt these practices today, directors shared similar opinions as compared to their counterparts in public companies. Female directors even more strongly support triggers for turnover; 68% (versus 56% of men) favor director term limits and 57% (versus 39% of men) support mandatory retirement ages.

“It was encouraging to see the majority of respondents in favor of retirement ages and term limits. Turnover among S&P 500 companies has trended at 5% to 7%—roughly 300 to 350 seats a year. Boards need tools they can use to ensure that new perspectives and thinking are regularly being brought to the boardroom,” says Daum. “This isn’t just an issue tied to activist shareholders, but something institutional shareholders are asking about as well: what are boards doing to ensure independent and fresh thinking?”

Not surprisingly, 43% of directors believe that a director loses his or her independence after about 10 years. Respondents from North America are less likely to tie director independence to years served, with only one-third agreeing that a director loses independence after a certain amount of time on the board.

Public companies represented in the survey have larger boards than private companies—on average 8.9 directors versus 7.6—and a larger representation of independent directors, 74% versus 54%. Yet, public and private company boards are similar in terms of the representation of women, minorities and new directors. On average, 18% of board members are women, 7% are ethnic minorities and 13% have been appointed in the past 12 months.

“This finding was very interesting. There has been much debate about the use and effectiveness of quotas. To see the relative parity of diversity among public and private companies reinforces that the tone needs to come from the top regarding bringing a fresh, diverse perspective representative of the company’s stakeholders and interests,” says Daum. Groysberg adds, “Although we are hearing more talk about the importance of diversity from boards, it’s not necessarily translating into numbers. Unfortunately, we haven’t seen as much progress as we were hoping for compared to our past survey on the diversity of boards.”

Boards are largest in the financials/professional services sector (9.1 directors) and smallest in the IT/telecom sector (7.5 directors). Female representation is highest (20% or more) in the consumer staples, financial services/professional services and consumer discretionary sectors, and lowest in IT/telecom (13%).

Looking across regions, board size is smallest in Australia/New Zealand, where boards average 6.7 members, as compared to the global average of 8.5 members. Boards in Australia/New Zealand and North America have the highest proportion of independent directors, and boards in Asia have the lowest proportion. Female representation is lowest in Central and South America and Asia.

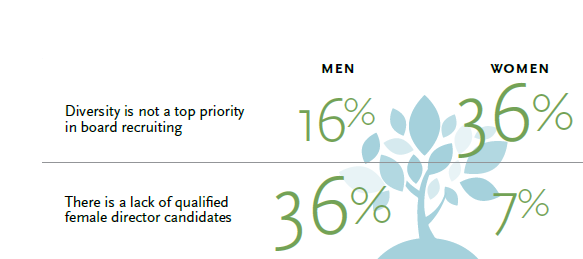

Boardroom Diversity: Why isn’t the number of women on boards increasing?

As the percentage of women on boards remains stagnant, there is both a gender divide and a generation divide on why this is. Male directors, especially older respondents, report the “lack of qualified female candidates,” while women directors most often cite the fact that diversity is not a priority in board recruiting and that traditional networks tend to be male-dominated. Younger male directors surveyed (those 55 and younger) are inclined to agree with women that traditional networks tend to be male-dominated. “Men in the younger generation, I think, just see their qualified female colleagues out there, but know that the traditional board networks still tend to be male,” says Stautberg. “It’s often hard to see an informal ‘network’ if you are in the middle of it, but you can see it very clearly when you’re on the outside.”

Boardroom Diversity: Quotas not supported overall.

Nearly 75% of surveyed directors do not personally support boardroom diversity quotas, but support for quotas varies significantly by gender and, to a lesser degree, by age. Forty-nine percent of female directors support diversity quotas, but only 9% of male directors do. Older women are less likely to favor quotas than younger women; 67% of female directors ages 55 and younger personally support boardroom quotas, compared with 36% of female directors over 55 (the majority of male directors, of any age, do not support quotas). Female directors also are more likely to be in favor of government regulatory agencies requiring boards to disclose specific practices/steps being taken to seat diverse candidates (43% versus 14% of male directors).

If quotas aren’t the answer, what do directors think would increase board diversity? Male and female directors agree that having board leadership that champions board diversity is the most effective way to build diverse corporate boards. Men feel more strongly than women that efforts to develop a pipeline of diverse board candidates through director advocacy, mentorship and training is an effective way to increase diversity.

Directors as a whole agree that shareholder pressure and board targets are less effective tools for increasing board diversity.

Boardroom Diversity: Search firms have been successful in expanding the talent pool of qualified female directors.

Directors take a variety of pathways to the boardroom: in roughly equal measures, directors were known to the board or another director, recruited by a search firm or known by the CEO. Public company directors are more likely to be recruited by an executive search firm than private company directors, while private company directors are more likely to have been appointed by a major shareholder.

The survey highlights gender differences, as well, in the paths to the boardroom. Female directors are more likely than their male counterparts to have been recruited by an executive search firm, while male directors are more likely to have been appointed by a major shareholder. “Search firms may be able to open doors that networking opportunities may not have been doing until relatively recently, at least for women,” says Stautberg. “Building up networks and getting known is something that women directors are engaging in much more actively now.”

And, indeed, 39% of female directors report that their gender was a significant factor in their board appointment, versus 1% of men.

Conclusion

Corporate boards face no shortage of challenges—from economic uncertainty to strategic and competitive shifts to a dynamic set of risks. Investor attention to board performance and governance has also escalated, and many boards are holding themselves to higher standards. Directors want to ensure that their boards contribute at the highest level, incorporating diverse perspectives, aligning with shareholder interests and setting a positive tone at the top for the organization.

Yet our research has revealed a gap between best practice and reality, especially in areas such as board diversity, HR/talent management, CEO succession planning and director evaluations. But the study provides hope that boards will make progress, as directors support practices that can help promote change. Future research is needed to track progress on these fronts and to study the impact of measures such as quotas and diversity on board performance.

Amid the many challenges confronting corporations—and the growing expectations on corporate boards—directors must be thoughtful about defining the skill sets needed around the board table and diligent in recruiting the right directors, planning for CEO succession and evaluating their own performance. In this way, they will be best positioned to contribute at the high levels which they are demanding of themselves, and to which others are holding them accountable.

*Julie Hembrock Daum leads the North American Board Practice at Spencer Stuart, and Susan Stautberg is the Chairman and CEO of the WomenCorporateDirectors Foundation. This post relates to the 2016 Global Board of Directors Survey, a co-publication from Spencer Stuart and the WCD Foundation authored by Ms. Daum; Ms. Stautberg; Dr. Boris Groysberg, Richard P. Chapman Professor of Business Administration at Harvard Business School; Yo-Jud Cheng, doctoral candidate at Harvard Business School; and Deborah Bell, researcher.

Voici un cas de gouvernance publié sur le site de Julie Garland McLellan* qui concerne les relations entre la présidente du conseil et sa fille nouvellement nommée comme CEO de cette entreprise privée de taille moyenne.

Le cas illustre le processus de transition familiale et les efforts à exercer afin de ne pas interférer avec les affaires de l’entreprise.

Il s’agit d’un cas très fréquent dans les entreprises familiales. Comment Hannah peut-elle continuer à faire profiter sa fille de ses conseils tout en s’assurant de ne pas empiéter sur ses responsabilités ?

Le cas présente la situation de manière assez succincte, mais explicite ; puis, trois experts en gouvernance se prononcent sur le dilemme qui se présente aux personnes qui vivent des situations similaires.

Bonne lecture ! Vos commentaires sont toujours les bienvenus.

Hannah prepared for the transition. She did a course of director education and understands her duties as a non-executive. She loves her daughter, trusts her judgement as CEO and genuinely wants to see her succeed. Nothing is going wrong but Hannah can’t help interfering. She is bored and longs for the days when she could visit customers or sit and strategise with her management team.

Once a week she has a formal meeting with the CEO in her office. In between times she is in frequent contact. Although by mutual agreement these contacts should be purely social or family oriented Hannah finds herself talking business and is hurt when her daughter suggests they leave it for the weekly meeting or put it onto the board agenda.

Over the past few months Hannah has improved governance, record-keeping, training and succession planning systems but she is running out of projects she can do without undermining her daughter. She also recognises that, as a medium sized unlisted business, the company does not need any more governance structures.

How can Hannah find fulfilment in her new role?

Paul’s Answer …..

Julie’s Answer ….

Jakob’s Answer ….

*Julie Garland McLellan is a practising non-executive director and board consultant based in Sydney, Australia.

Nous publions ici un quatrième billet de Danielle Malboeuf* laquelle nous a soumis ses réflexions sur les grands enjeux de la gouvernance des institutions d’enseignement collégial les 23 et 27 novembre 2013, à titre d’auteure invitée.

Dans un premier billet, publié le 23 novembre 2013 sur ce blogue, on insistait sur l’importance, pour les CA des Cégep, de se donner des moyens pour assurer la présence d’administrateurs compétents dont le profil correspond à celui recherché.

D’où les propositions adressées à la Fédération des cégeps et aux CA pour préciser un profil de compétences et pour faire appel à la Banque d’administrateurs certifiés du Collège des administrateurs de sociétés (CAS), le cas échéant. Un autre enjeu identifié dans ce billet concernait la remise en question de l’indépendance des administrateurs internes.

Le deuxième billet publié le 27 novembre 2013 abordait l’enjeu entourant l’exercice de la démocratie par différentes instances au moment du dépôt d’avis au conseil d’administration.

Le troisième billet portait sur l’efficacité du rôle du président du conseil d’administration (PCA).

Ce quatrième billet est une mise à jour de son dernier article portant sur le rôle du président de conseil.

Voici donc l’article en question, reproduit ici avec la permission de l’auteure.

Vos commentaires sont appréciés. Bonne lecture.

________________________________________

LE RÔLE DU PRÉSIDENT DU CONSEIL D’ADMINISTRATION | LE CAS DES INSTITUTIONS D’ENSEIGNEMENT COLLÉGIAL

par Danielle Malboeuf*

Il y a deux ans, je publiais un article sur le rôle du président du conseil d’administration (CA) [1]. J’y rappelais le rôle crucial et déterminant du président du CA et j’y précisais, entre autres, les compétences recherchées chez cette personne et l’enrichissement attendu de son rôle.

Depuis, on peut se réjouir de constater qu’un nombre de plus en plus élevé de présidents s’engagent dans de nouvelles pratiques qui améliorent la gouvernance des institutions collégiales. Ils ne se limitent plus à jouer un rôle d’animateurs de réunions, comme on pouvait le constater dans le passé.

Notons, entre autres, que les présidents visent de plus en plus à bien s’entourer, en recherchant des personnes compétentes comme administrateurs. D’ailleurs, à cet égard, les collèges vivent une situation préoccupante. La Loi sur les collèges d’enseignement général et professionnel prévoit que le ministre [2] nomme les administrateurs externes. Ainsi, en plus de connaître des délais importants pour la nomination de nouveaux administrateurs, les collèges ont peu d’influence sur leur choix.

Présentement, les présidents et les directions générales cherchent donc à l’encadrer. Ils peuvent s’inspirer, à cet égard, des démarches initiées par d’autres organisations publiques en établissant, entre autres, un profil de compétences recherchées qu’ils transmettent au ministre. Ils peuvent ainsi tenter d’obtenir une complémentarité d’expertise dans le groupe d’administrateurs.

Une fois les administrateurs nommés, les présidents doivent se préoccuper d’assurer leur formation continue pour développer les compétences recherchées. Ils se donnent ainsi l’assurance que ces personnes comprennent bien leur rôle et leurs responsabilités et qu’elles sont outillées pour remplir le mandat qui leur est confié. De plus, ils doivent s’assurer que les administrateurs connaissent bien l’organisation, qu’ils adhèrent à sa mission et qu’ils partagent les valeurs institutionnelles. En présence d’administrateurs compétents, éclairés, et dont l’expertise est reconnue, il est plus facile d’assurer la légitimité et la crédibilité du CA et de ses décisions.

Un président performant démontrera aussi de grandes qualités de leadership. Il fera connaître à toutes les instances du milieu le mandat confié au CA. Il travaillera à mettre en place un climat de confiance au sein du CA et avec les gestionnaires de l’organisation. Il cherchera à exploiter l’ensemble des compétences et à faire jouer au CA un rôle qui va au-delà de celui de fiduciaire, soit celui de contribuer significativement à la mission première du cégep : donner une formation pertinente et de qualité où l’étudiant et sa réussite éducative sont au cœur des préoccupations.

Plusieurs ont déjà fait le virage… c’est encourageant ! Les approches préconisées par l’Institut sur la gouvernance des organismes publics et privés (IGOPP) et le Collège des administrateurs de sociétés (CAS) puis reprises dans la loi sur la gouvernance des sociétés d’État ne sont sûrement pas étrangères à cette évolution. En fournissant aux présidents de CA le soutien, la formation et les outils appropriés pour améliorer leur gouvernance, le Centre collégial des services regroupés (CCSR) [3] contribue à assurer le développement des institutions collégiales dans un contexte de saine gestion.

Un CA performant est guidé par un président compétent.

*Danielle Malboeuf est consultante et formatrice en gouvernance ; elle possède une grande expérience dans la gestion des CEGEP et dans la gouvernance des institutions d’enseignement collégial et universitaire. Elle est CGA-CPA, MBA, ASC, Gestionnaire et administratrice retraité du réseau collégial et consultante.

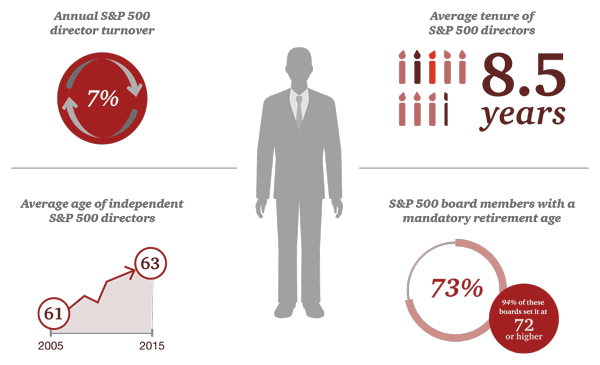

Les investisseurs et les actionnaires reconnaissent le rôle prioritaire que les administrateurs de sociétés jouent dans la gouvernance et, conséquemment, ils veulent toujours plus d’informations sur le processus de nomination des administrateurs et sur la composition du conseil d’administration.

L’article qui suit, paru sur le Forum du Harvard Law School, a été publié par Paula Loop, directrice du centre de la gouvernance de PricewaterhouseCoopers. Il s’agit essentiellement d’un compte rendu sur l’évolution des facteurs clés de la composition des conseils d’administration. La présentation s’appuie sur une infographie remarquable.

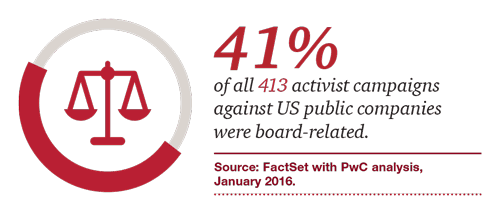

Ainsi, on apprend que 41 % des campagnes menées par les activistes étaient reliées à la composition des CA, et que 20 % des CA ont modifié leur composition en réponse aux activités réelles ou potentielles des activistes.

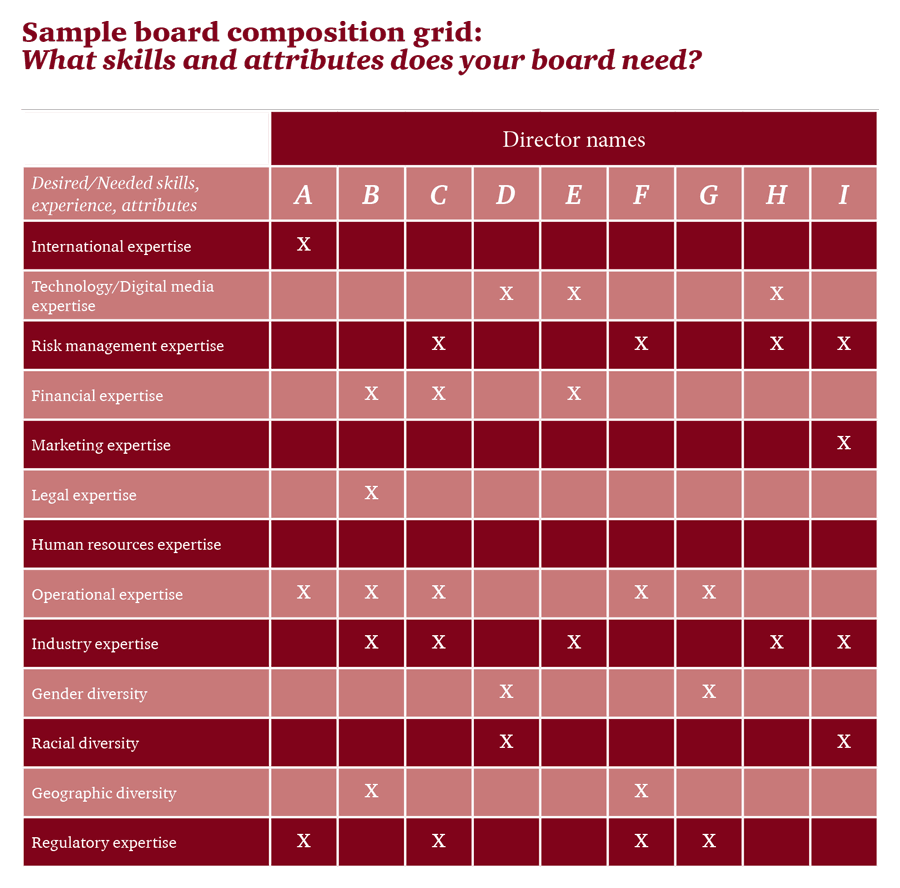

L’article s’attarde sur la grille de composition des conseils relative aux compétences et habiletés requises. Également, on présente les arguments pour une plus grande diversité des CA et l’on s’interroge sur la situation actuelle.

Enfin, l’article revient sur les questions du nombre de mandats des administrateurs et de l’âge de la retraite de ceux-ci ainsi que sur les préoccupations des investisseurs eu égard au renouvellement et au rajeunissement des CA.

Le travail de renouvellement du conseil ne peut se faire sans la mise en place d’un processus d’évaluation complet du fonctionnement du CA et des administrateurs.

À mon avis, c’est certainement un article à lire pour bien comprendre toutes les problématiques reliées à la composition des conseils d’administration.

In today’s business environment, companies face numerous challenges that can impact success—from emerging technologies to changing regulatory requirements and cybersecurity concerns. As a result, the expertise, experience, and diversity of perspective in the boardroom play a more critical role than ever in ensuring effective oversight. At the same time, many investors and other stakeholders are seeking influence on board composition. They want more information about a company’s director nominees. They also want to know that boards and their nominating and governance committees are appropriately considering director tenure, board diversity and the results of board self-evaluations when making director nominations. All of this is occurring within an environment of aggressive shareholder activism, in which board composition often becomes a central focus.

Shareholder activism and board composition

At the same time, a growing number of companies are adopting proxy access rules—allowing shareholders that meet certain ownership criteria to submit a limited number of director candidates for inclusion on the company’s annual proxy. It has become a top governance issue over the last two years, with many shareholders viewing it as a step forward for shareholder rights. And it’s another factor causing boards to focus more on their makeup.

So within this context, how should directors and investors be thinking about board composition, and what steps should be taken to ensure boards are adequately refreshing themselves?

Assessing what you have–and what you need

In a rapidly changing business climate, a high-performing board requires agile directors who can grasp concepts quickly. Directors need to be fiercely independent thinkers who consciously avoid groupthink and are able to challenge management—while still contributing to a productive and collegial boardroom environment. A strong board includes directors with different backgrounds, and individuals who understand how the company’s strategy is impacted by emerging economic and technological trends.

Sample board composition grid: What skills and attributes does your board need?

In assessing their composition, boards and their nominating and governance committees need to think critically about what skills and attributes the board currently has, and how they tie to oversight of the company. As companies’ strategies change and their business models evolve, it is imperative that board composition be evaluated regularly to ensure that the right mix of skills are present to meet the company’s current needs. Many boards conduct a gap analysis that compares current director attributes with those that it has identified as critical to effective oversight. They can then choose to fill any gaps by recruiting new directors with such attributes or by consulting external advisors. Some companies use a matrix in their proxy disclosures to graphically display to investors the particular attributes of each director nominee.

Board diversity is a hot-button issue

Diversity is a key element of any discussion of board composition. Diversity includes not only gender, race, and ethnicity, but also diversity of skills, backgrounds, personalities, opinions, and experiences. But the pace of adding more gender and ethnic diversity to public company boards has been only incremental over the past five years. For example, a December 2015 report from the US Government Accountability Office estimates that it could take four decades for the representation of women on US boards to be the same as men. [1] Some countries, including Norway, Belgium, and Italy, have implemented regulatory quotas to increase the percentage of women on boards.

Even if equal proportions of women and men joined boards each year beginning in 2015, GAO estimated that it could take more than four decades for women’s representation on boards to be on par with that of men’s.

—US Government Accountability Office, December 2015

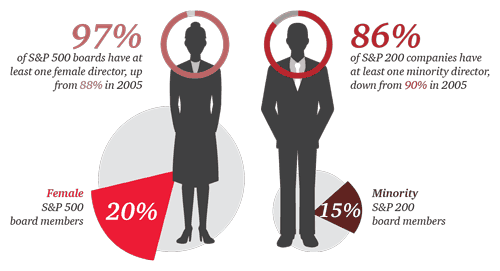

According to PwC’s 2015 Annual Corporate Directors Survey, more than 80% of directors believe board diversity positively impacts board and company performance. But more than 70% of directors say there are impediments to increasing board diversity. [2] One of the main impediments is that many boards look to current or former CEOs as potential director candidates. However, only 4% of S&P 500 CEOs are female, [3] less than 2% of the Fortune 500 CEOs are Hispanic or Asian, and only 1% of the Fortune 500 CEOs are African-American. [4] So in order to get boards to be more diverse, the pool of potential director candidates needs to be expanded.

Is there diversity on US boards?

Source: Spencer Stuart US Board Index 2015, November 2015.

SEC rules require companies to disclose the backgrounds and qualifications of director nominees and whether diversity was a nomination consideration. In January 2016, SEC Chair Mary Jo White included diversity as a priority for the SEC’s 2016 agenda and suggested that the SEC’s disclosure rules pertaining to board diversity may be enhanced.

While those who aspire to become directors must play their part, the drive to make diversity a priority really has to come from board leadership: CEOs, lead directors, board chairs, and nominating and governance committee chairs. These leaders need to be proactive and commit to making diversity part of the company and board culture. In order to find more diverse candidates, boards will have to look in different places. There are often many untapped, highly qualified, and diverse candidates just a few steps below the C-suite, people who drive strategies, run large segments of the business, and function like CEOs.

How long is too long? Director tenure and mandatory retirement

The debate over board tenure centers on whether lengthy board service negatively impacts director independence, objectivity, and performance. Some investors believe that long-serving directors can become complacent over time—making it less likely that they will challenge management. However, others question the virtue of forced board turnover. They argue that with greater tenure comes good working relationships with stakeholders and a deep knowledge of the company. One approach to this issue is to strive for diversity of board tenure—consciously balancing the board’s composition to include new directors, those with medium tenures, and those with long-term service.

This debate has heated up in recent years, due in part to attention from the Council of Institutional Investors (the Council). In 2013, the Council introduced a revised policy statement on board tenure. While the policy “does not endorse a term limit,” [5] the Council noted that directors with extended tenures should no longer be considered independent. More recently, the large pension fund CalPERS has been vocal about tenure, stating that extended board service could impede objectivity. CalPERS updated its 2016 proxy voting guidelines by asking companies to explain why directors serving for over twelve years should still be considered independent.

We believe director independence can be compromised at 12 years of service—in these situations a company should carry out rigorous evaluations to either classify the director as non-independent or provide a detailed annual explanation of why the director can continue to be classified as independent.

— CalPERS Global Governance Principles, second reading, March 14, 2016

Factors in the director tenure and age debate

Source: Spencer Stuart US Board Index 2015, November 2015.

Many boards have a mandatory retirement age for their directors. However, the average mandatory retirement age has increased in recent years. Of the 73% of S&P 500 boards that have a mandatory retirement age in place, 97% set that age at 72 or older—up from 57% that did so ten years ago. Thirty-four percent set it at 75 or older. [6] Others believe that director term limits may be a better way to encourage board refreshment, but only 3% of S&P 500 boards have such policies. [7]

Investor concern

Some institutional investors have expressed concern about board composition and refreshment, and this increased scrutiny could have an impact on proxy voting decisions.

What are investors saying about board composition and refreshment?

Sources: BlackRock, Proxy voting guidelines for U.S. securities, February 2015; California Public Employees’ Retirement System, Statement of Investment Policy for Global Governance, March 16, 2015; State Street Global Advisors’ US Proxy Voting and Engagement Guidelines, March 2015.

Proxy advisors’ views on board composition—recent developments

Proxy advisory firm Institutional Shareholder Services’s (ISS) governance rating system QuickScore 3.0 views tenure of more than nine years as potentially compromising director independence. ISS’s 2016 voting policy updates include a clarification that a “small number” of long-tenured directors (those with more than nine years of board service) does not negatively impact the company’s QuickScore governance rating, though ISS does not provide specifics on the acceptable quantity.

Glass Lewis’ updated 2016 voting policies address nominating committee performance. Glass Lewis may now recommend against the nominating and governance committee chair “where the board’s failure to ensure the board has directors with relevant experience, either through periodic director assessment or board refreshment, has contributed to a company’s poor performance.” Glass Lewis believes that shareholders are best served when boards are diverse on the basis of age, race, gender and ethnicity, as well as on the basis of geographic knowledge, industry experience, board tenure, and culture.

How can directors proactively address board refreshment?

The first step in refreshing your board is deciding whether to add a new board member and determining which director attributes are most important. One way to do this is to conduct a self-assessment. Directors also have a number of mechanisms to address board refreshment. For one, boards can consider new ways of recruiting director candidates. They can take charge of their composition through active and strategic succession planning. And they can also use robust self-assessments to gauge individual director performance—and replace directors who are no longer contributing.

Act on the results of board assessments. Boards should use their annual self-assessment to help spark discussions about board refreshment. Having a robust board assessment process can offer insights into how the board is functioning and how individual directors are performing. The board can use this process to identify directors that may be underperforming or whose skills may no longer match what the company needs. It’s incumbent upon the board chair or lead director and the chair of the nominating and governance committee to address any difficult matters that may arise out of the assessment process, including having challenging conversations with underperforming directors. In addition, some investors are asking about the results of board assessments. CalPERS and CalSTRS have both called on boards to disclose more information about the impact of their self-assessments on board composition decisions. [8]

Take a strategic approach to director succession planning. Director succession planning is essential to promoting board refreshment. But, less than half of directors “very much” believe their board is spending enough time on director succession. [9] In board succession planning, it’s important to think about the current state of the board, the tenure of current members, and the company’s future needs. Boards should identify possible director candidates based upon anticipated turnover and director retirements.

Broaden the pool of candidates. Often, boards recruit directors by soliciting recommendations from other sitting directors, which can be a small pool. Forward-looking boards expand the universe of potential qualified candidates by looking outside of the C-suite, considering investor recommendations, and by looking for candidates outside the corporate world—from the retired military, academia, and large non-profits. This will provide a broader pool of individuals with more diverse backgrounds who can be great board contributors.

In sum, evaluating board composition and refreshing the board may be challenging at times, but it’s increasingly a topic of concern for many investors, and it’s critical to the board’s ability to stay current, effective, and focused on enhancing long-term shareholder value.

The complete publication, including footnotes and appendix, is available here.

Endnotes:

[1] United States Government Accountability Office, “Corporate Boards: Strategies to Address Representation of Women Include Federal Disclosure Requirements,” December 2015. (go back)

*Paula Loop is Leader of the Governance Insights Center at PricewaterhouseCoopers LLP. This post is based on a PwC publication by Ms. Loop and Paul DeNicola. The complete publication, including footnotes and appendix, is available here.

Très bonnes réflexions d’Yvan Allaire sur le dogme de la séparation des rôles entre PCA et PDG. À lire sur le blogue Les Affaires .com.

Rien à rajouter à ce billet de l’expert en gouvernance qui , comme moi, cherche des réponses à plusieurs théories sur la gouvernance. Plus de recherches dans le domaine de la gouvernance serait grandement indiquées… Le CAS et la FSA de l’Université Laval mettront sur pied un programme de recherche dont le but est de répondre à ce type de questionnement.

« Parmi les dogmes de la bonne gouvernance, la séparation des rôles du PCA et du PDG vient au deuxième rang immédiatement derrière « l’indépendance absolue et inviolable » de la majorité des administrateurs. … Bien que les études empiriques aient grande difficulté à démontrer de façon irréfutable la valeur de ces deux dogmes, ceux-ci sont, semble-t-il, incontournables. Dans le cas de la séparation des rôles, le sujet a pris une certaine importance récemment chez Research in Motion ainsi que chez Air Transat. Le compromis d’un administrateur en chef (lead director) pour compenser pour le fait que le PCA et le PDG soit la même personne ne satisfait plus; le dogme demande que le président du conseil soit indépendant de la direction ».

Voici le point de vue de Liam McGee paru récemment dans la section Leadership de la revue du Harvard Business School (HBR). L’auteur relate son expérience alors qu’il était le président et chef de la direction (PCD) de la Hartford Financial Services Group.

Selon lui, tous les présidents de conseils d’administration tentent de « gérer leur CA » en utilisant diverses approches basées sur le contrôle et le pouvoir de l’information. Cependant, depuis une dizaine d’années, les conseils d’administration ont progressivement repris leurs droits ! Ils cherchent à maintenir une plus grande distance entre leurs rôles de fiduciaires et ceux qui incombent à la direction de l’organisation.

Pour l’auteur, il n’y a qu’une façon de réconcilier les deux parties : le partenariat. Celui-ci est fondé sur la confiance, et la confiance ne s’acquiert pas du jour au lendemain ! Il faut élaborer une stratégie et mettre en œuvre des mécanismes qui renforceront graduellement la confiance entre le CA et la haute direction. Selon lui, il vital que le PCD ait confiance en son CA.

Toute la carrière de l’auteur a été consacrée à l’établissement de liens de confiance essentiels aux bonnes pratiques de gouvernance. C’est de son expérience dont il est question dans ce bref extrait. Bonne lecture !

It’s understandable that most CEOs try to manage their boards. With directors often attempting to take a more active role in decisions these days, CEOs naturally feel a bit threatened. They’re trying to lead a group of people who typically lack the time or expertise to fully understand what’s going on — but who have real power.

At most companies, despite all the best intentions, managing the board usually means keeping directors at arm’s length. Most CEOs I’ve known are inclined to give out just enough information to satisfy their fiduciary obligations, often in highly structured meetings that leave little to chance. They hold off on revealing the deeper challenges or complexities that might provoke tough questions.

But as I learned over the course of my career, there’s a better approach with boards. A CEO can work in partnership with directors without sacrificing his or her authority — and thereby accomplish far more than is possible with an arm’s-length relationship. It’s all a matter of developing trust. In my five years as CEO of The Hartford, a Fortune 100 insurer, winning trust was crucial to turning around the company in the aftermath of the global financial crisis.

Building trust can be a delicate thing, but it isn’t magic. You don’t need special charisma. All you really need is courage and self-confidence.

The first step is to show that you trust your directors. In practical terms, that means not trying to stage-manage board interactions. When I took over at The Hartford, the management team took up most of our board meetings going through long slide decks. I got rid of that barrier. We distilled the most important information into pre-reads for the directors to study in advance. The meetings themselves, aside from the CFO’s report on financials, focused on discussions of the main issues. Real transparency, I learned, isn’t so much in the numbers, but in open conversation.

That wasn’t easy at first for my executives, who were used to wielding their slide decks to control their presentations. I had to coach them not to worry and to remember that directors were genuinely interested in their businesses and in getting to know them as managers. So they should just be open to the discussions that came up.

These unscripted meetings not only freed directors to ask more questions, but also gave them more of a window into the company. They got to see the other executives in action, including my potential successors.

It’s important to remember that boards see only a small part of you, and even less of the company. They visit for a day or two and get a snapshot. How you work with them is often as important as the substance of what you say. If you give the board unfettered access to executives, you’ll build trust with the directors as well as with your management team. Openness and transparency in board meetings over time can go a long way toward making everyone comfortable with everyone else.

Still, those steps weren’t enough for me to build a strong basis of trust. It’s one thing to allow open discussion on the usual company topics. But what about the issues that involved me personally? How could I get the directors to trust me on my own performance? Obviously a CEO will want to maintain some discretion here. But openness on even these issues can pay off enormously.

A year into my tenure, a senior executive quit abruptly and, on the way out, criticized my management style to the board. I was concerned enough to get a coach, who conducted a full 360-degree feedback process for me. But instead of just telling the directors about the coaching, I decided to give them an overview of my coach’s findings. Her report was generally positive, but it had some tough parts in it, and I decided to discuss these openly. It may have been risky, but it helped to break the ice. The board members felt relaxed enough to give me some feedback of their own. My lead director even became something of a second coach. All of this was invaluable, and it wouldn’t have happened if I hadn’t made myself vulnerable in the first place.

That trust made a big difference in 2012, when an activist investor challenged us to restructure the company. We were still in the process of developing our new strategy, and the stock price was disappointingly low. The controversy could have led to my departure and, more important, a costly delay in the company’s revival. Instead the board stayed unified and we stuck to our plan, which turned out to be a better approach than the strategy the activist was pushing.

All along the way, as we developed trust, I grew to welcome the board members’ tough questions. I could see they were focused on helping me protect and improve the company. A CEO’s job is hard enough. One of your biggest responsibilities is to avoid making dumb decisions. Wouldn’t you want all the directors to feel comfortable challenging you and each other?

*Liam McGee was chairman and CEO of the Hartford Financial Services Group (“The Hartford”) from 2009 to June of 2014. He died in February 2015.

Ce billet présente la proposition de la Securities and Exchange Commission (SEC) eu égard à l’utilisation d’un bulletin de vote dit universel dans le cas d’élections contestées lors de l’assemblée annuelle.

En fait, la SEC veut revoir le mode d’élection des administrateurs en obligeant les parties à solliciter les votes pour leurs candidats (la « slate »), mais à la condition d’inclure les noms de tous les autres candidats-administrateurs sur leur bulletin de vote.

Les actionnaires auront ainsi la possibilité de choisir parmi tous les candidats, plutôt que de choisir une « slate » ou une autre.

Cet article a été publié dans Harvard Law School Forum par Ron Cami, Joseph A. Hall, Phillip R. Mills, Ning Chiu, et Rebecca E. Crosby de la firme Davis Polk & Wardwell LLP ; il présente tous les arguments pour une telle proposition tout en montrant les différences avec l’accès au bulletin de vote (« proxy access ») par les groupes d’actionnaires possédant plus de 3 % du capital sur la période des trois dernières années.

On October 26, the Securities and Exchange Commission proposed long-expected changes to the proxy rules in order to mandate the use of universal proxy cards in contested elections at annual meetings. The proposal is designed to address the current inability of shareholders to vote for the combination of board nominees of their choice in an election involving a proxy contest. Under the proposal, each party in a contested election—management and one or more dissident shareholders—would continue to distribute its own proxy materials and use its own proxy card to solicit votes for its preferred slate of nominees. However, each party’s proxy card would be required to include the nominees of all parties, and thus enable the proxy voter to select its preferred combination of candidates.

The proposal would—

mandate the use of universal proxy cards for most contested director elections,

establish notice and filing requirements for both companies and dissidents,

require dissidents to undertake a minimum solicitation effort, and

prescribe form and presentation criteria for the proxy card.

What seems clear to us is that the universal proxy would ultimately move the balance of corporate power further from the board and closer to the shareholders. As the SEC observed in the proposing release, “[i]f the proposed amendments result in additional dissident representation, it is difficult to predict whether such additional dissident representation would enhance or detract from board effectiveness and shareholder value.” The SEC is seeking comment from all affected constituencies, including companies, on this critical question. The deadline for comments on the proposal is expected to fall in late December 2016, 60 days after publication of the proposal in the Federal Register. Given the timing of the proposal and comment period, there is little chance that a universal proxy card would be required for the 2017 proxy season.

Why Is the SEC Acting?

Currently, a shareholder voting by proxy in a contested election is effectively required to choose between the slate of nominees put forward by management and the slate put forward by the dissident. By contrast, a shareholder who attends a meeting in person can pick and choose between directors nominated by management and directors nominated by dissidents. In the SEC’s view this creates a kink in the proxy plumbing, the overarching goal of which is to make proxy voting as close as possible to voting at a shareholder meeting, due to the interplay between two rules—

– “Bona fide nominee” rule—Under the SEC’s rules, one party’s director nominee may not be included on the opposing party’s proxy card unless the nominee gives his or her consent to the opposing party. Since this rarely happens, the bona fide nominee rule usually results in two separate proxy cards, forcing a shareholder voting by proxy to choose one slate or the other.

– “Last in time” rule—Delaware and other state corporate laws generally provide that the latest proxy revokes any earlier proxy executed by a shareholder. The last-in-time rule therefore effectively stymies a shareholder’s attempt to submit multiple proxy cards to vote for a combination of nominees from different slates, even if the aggregate number of nominees selected is the same as the number of seats up for election. In 1992, the SEC introduced a modification to the bona-fide-nominee rule to permit a dissident to propose a “short slate” of nominees—that is, a slate where the dissident nominees would constitute a minority of the board—and then to “round out” the dissident proxy card by identifying management nominees that the dissident would not vote for, resulting in a proxy voter’s remaining votes being cast for the unnamed management nominees. While the short-slate rule allows proxy voters to vote for a combination of dissident and management nominees, albeit in a roundabout way, the shareholder is still unable to mix and match as it sees fit, since the combination of dissident and management nominees is dictated by the dissident.

Key Features of the Proposal

Mandatory use. The proposal would require universal proxy cards for most contested director elections at annual meetings. Each soliciting party would continue to distribute its own proxy materials and its own version of the universal proxy card. The proposal would not require the cards to be identical; rather, each party would be permitted to design its own card so long as the content, format and presentation comply with the proposal’s criteria.

Mandatory use only applies to solicitations that involve a contested election where a dissident is proposing a competing slate of director candidates. However, with the amendment to the bona-fide-nominee rule, a dissident could name all of management’s nominees on a proxy card in order to solicit against their election, or to seek their removal, even without a universal proxy card. A dissident could also solicit for a proposal other than an election of directors but name all of management’s nominees in order to have a proxy card that could be used for all matters to be voted on at the meeting.

Mandatory use also would not apply to “exempt solicitations” under the proxy rules or to registered investment companies or business development companies.

Revision of the bona-fide-nominee rule. The proposal would define a “bona fide nominee” as a person who has consented to being named in any proxy statement relating to the company’s next meeting of shareholders for the election of directors. The proposal would retain the requirement that a nominee intend to serve, if elected. If a nominee intends to serve only if his or her nominating party’s slate is elected, the proxy statement would need to disclose that fact.

Elimination of the short-slate rule. The proposal would eliminate the short-slate rule because universal proxy cards obviate the need for dissidents to round out partial slates with management nominees. Dissidents would however retain the ability to recommend their preferred management nominees in their proxy materials.

Notice and filing. The proposal would require a dissident shareholder to provide the company with notice of its intent to solicit proxies and the names of its nominees at least 60 days before the anniversary of the previous year’s annual meeting, or about two to four weeks prior to the time the company would typically mail its proxy statement. The company would then be required to provide the dissident with the names of management’s nominees at least 50 days before that anniversary. The dissident would need to file its proxy statement by the later of 25 days before the meeting date or five days after management files its proxy statement.

Minimum solicitation effort. Dissidents would be obligated to solicit holders of shares representing at least a majority of the company’s voting power, which would mean a dissident must expend its own resources in order to trigger use of the mandatory universal proxy card. However, because dissidents would not be required to solicit all shareholders, many shareholders (such as retail investors) may not receive proxy statements containing information about the dissident nominees—thereby decreasing the financial burden on the dissident. The SEC is seeking comment on whether dissidents should be required to solicit all shareholders.

Presentation and formatting. The proposal prescribes formatting and presentation criteria intended to ensure that information is presented clearly and fairly.

A universal proxy card would be required to—

clearly distinguish between management nominees, dissident nominees, and any proxy access nominees,

within each group of nominees, list the nominees in alphabetical order,

use the same font type, style and size to present all nominees,

disclose the maximum number of nominees for which authority to vote can be granted, and

disclose the treatment of a proxy executed in a manner that grants authority to vote for more, or fewer, nominees than the number of directors being elected, or does not grant authority to vote for any nominees. A universal proxy card would be permitted to offer the ability to vote for all management nominees as a group or all dissident nominees as a group, but only if both parties have proposed a full slate of nominees and there are no proxy access candidates.

Voting Standards Disclosure and Voting Options

The SEC has proposed additional rules governing all meetings, not just contested situations, for the election of directors. Due to concerns that some company proxy statements have ambiguous or inaccurate disclosures about voting standards in director elections, the proposal would mandate changes to proxy cards and the disclosure of those voting standards in the proxy statement.

If a company uses a majority vote standard for the election of directors and a vote cast against a nominee would have legal effect under state law, the proxy card would be required to include the options to vote “against” the nominee and to “abstain” from voting. The company would not be permitted to offer an option to “withhold” against a director.

A company that applies plurality voting standards for director elections, including a plurality voting standard with a director resignation policy (often known as “plurality plus”), would need to disclose in its proxy statement the treatment and effect of a “withhold” vote in the election—namely, that “withholds” have no legal effect.

How Is This Different From Proxy Access?

Over the past two years, many companies have adopted “proxy access” bylaws that permit shareholders, typically those who have held at least 3% of the company’s shares for at least three years, to nominate candidates for inclusion in the proxy materials distributed by the company.

The SEC acknowledged that some are concerned that a universal proxy card could be viewed as a substitute for proxy access. However, the SEC indicated that significant differences exist. Unlike proxy access, using a universal proxy card would not require a company to include in its proxy materials the names of the nominating shareholder’s nominees, disclosure about the nominating shareholder and its nominees and a supporting statement from the nominating shareholder. Shareholders making nominations under proxy access can rely on the company’s proxy materials and are not required to prepare and file their own proxy materials, disseminate those materials and use them to solicit shareholders.

With universal proxy cards, by contrast, dissidents would need to spend the time and effort and incur the costs to develop their own proxy statements and solicit shareholders. A company need only include dissident nominees on the universal proxy card it uses, and can choose to provide no other information in the company’s proxy materials about the dissident’s nominees.

What’s Next?

The SEC nodded to concerns that have been raised over allowing universal proxy cards, including the potential for investor confusion and the implication that the soliciting party endorses the other party’s nominees. Though it believes its proposal addresses these issues, the SEC acknowledged that other unknowns remain, including whether universal proxy cards would have an impact on the number of dissident nominees elected, whether they would increase the frequency of contested elections, and what the impact of these developments would be on board effectiveness and, ultimately, shareholder value. The SEC is seeking comment on all of these questions, and the responses it receives could shape any final rules in ways that differ materially from the proposal.

We expect the proposal to generate a lively debate among companies, institutional investors and shareholder advocates. The timing of the proposal, coming in the final days of the Obama Administration, suggests that any definitive action on universal proxy cards may be left to an SEC composed largely of newly appointed members, who may have priorities and concerns that differ from the current commissioners.

Whether or not the SEC adopts its proposal, it would make sense for companies to review their disclosure about voting standards and voting options on their proxy cards for the upcoming proxy season. The SEC staff has expressed concerns that some proxy statements contain ambiguities or inaccuracies under existing law and the Division of Corporation Finance may issue comments in advance of the final rules when it thinks companies may be making inaccurate disclosures.

Aujourd’hui, je cède la parole à Mme Nicolle Forget*, certainement l’une des administratrices de sociétés les plus chevronnées au Québec (sinon au Canada), qui nous présente sa vision de la gouvernance « réglementée » ainsi que celle du rôle des administrateurs dans ce processus.

L’allocution qui suit a été prononcée dans le cadre du Colloque sur la gouvernance organisée par la Chaire de recherche en gouvernance de sociétés le 6 juin 2014. Je pensais tout d’abord faire un résumé de son texte, mais, après une lecture attentive, j’en ai conclu que celui-ci exposait une problématique de fond et constituait une prise de position fondamentale en gouvernance. Il me semblait essentiel de vous faire partager son article au complet.

Nous avons souvent abordé les conséquences non anticipées de la réglementation, principalement celles découlant des exigences de divulgation en matière de rémunération. Cependant, dans son allocution, l’auteure apporte un éclairage nouveau, inédit et audacieux sur l’exercice de la gouvernance dans les sociétés publiques.

Elle présente une solide argumentation et expose clairement certains malaises vécus par les administrateurs eu égard à la lourdeur des mécanismes réglementaires de gouvernance. Les questionnements présentés en conclusion de l’article sont, en grande partie, fondés sur sa longue expérience comme membre de nombreux conseils d’administration.

Comment réagissez-vous aux constats que fait Mme Forget ? Les autorités réglementaires vont-elles trop loin dans la prescription des obligations de divulgation ? Pouvons-nous éviter les effets pervers de certaines dispositions sans pour autant nuire au processus de divulgation d’informations importantes pour les actionnaires et les parties prenantes.

Vos commentaires sont les bienvenus. Je vous souhaite une bonne lecture.

MALAISE AU CONSEIL | Les effets pervers de l’obligation de divulgation en matière de rémunération

par

Nicolle Forget*

Merci aux organisateurs de ce colloque de me donner l’occasion de partager avec vous quelques constatations et interrogations qui m’habitent depuis quatre ou cinq ans concernant diverses obligations imposées aux entreprises à capital ouvert (inscrites en Bourse). Je souligne d’entrée de jeu que la présentation qui suit n’engage que moi.

Depuis l’avènement de quelques grands scandales financiers, ici et ailleurs, on en a mis beaucoup sur le dos des administrateurs de sociétés. On voudrait qu’un administrateur soit un expert en semblable matière. Il ne l’est pas. Il arrive avec son bagage, c’est pourquoi on l’a choisi. On lui prépare un programme de formation pour lui permettre de comprendre l’entreprise au conseil de laquelle il a accepté de siéger, mais il n’en saura jamais autant que la somme des savoirs de l’entreprise. C’est utopique de s’attendre au contraire. Même un administrateur qui ne ferait que cela, siéger au conseil de cette entreprise, ne le pourrait pas.

Des questions reviennent constamment dans l’actualité : où étaient les administrateurs ? N’ont-ils rien vu venir ou rien vu tout court? Ont-ils rempli leur devoir fiduciaire? Tout juste si on ne conclut pas qu’ils sont tous des incompétents. Les administrateurs étaient là. Ils savaient ce que l’on a bien voulu leur faire savoir. (ex. Saccage de la Baie-James. Les administrateurs de la SEBJ, convoqués en Commission parlementaire à Québec, au printemps 1983, ont appris, par un avocat venu y témoigner, l’existence d’un avis juridique qu’il avait préparé à la demande de la direction. La SEBJ poursuivait alors les responsables du saccage et un très long procès était sur le point de commencer. Avoir eu connaissance de son contenu, au moment où il a été livré au PDG, aurait eu un impact sur nos décisions. J’étais alors membre du conseil d’administration).

Posons tout de suite que la meilleure gouvernance qui soit n’empêchera jamais des dirigeants qui veulent cacher au conseil certains actes d’y parvenir — surtout si ces actes sont frauduleux. Même avec de belles politiques et de beaux codes d’éthique, plusieurs directions d’entreprise trouvent encore qu’un conseil d’administration n’est rien d’autre qu’un mal nécessaire. Les administrateurs sont parfois perçus comme s’ingérant dans les affaires de la direction ou dans les décisions qu’elle prend. Aussi, ces dirigeants ont-ils tendance à placer les conseils devant des faits accomplis ou des dossiers tellement bien ficelés qu’il est difficile d’y trouver une fissure par laquelle entrevoir une faille dans l’argumentation au soutien de la décision à prendre. Pourtant, et nous le verrons plus loin, en vertu de la loi, le conseil « exerce tous les pouvoirs nécessaires pour gérer les activités et les affaires internes de la société ou en surveiller l’exécution ».

Les conseils d’administration, comme les entreprises et leurs dirigeants, sont soumis à quantité de législations, réglementations, annexes à celles-ci, avis, lignes directrices et autres exigences émanant d’autorités multiples — et davantage les entreprises œuvrent dans un secteur d’activités qui dépasse les frontières d’une province ou d’un pays. Et, selon ce que l’on entend, il faudrait que l’administrateur ait toujours tout vu, tout su…

Malaise!

En 2007, Yvan Allaire écrivait que « … la gouvernance par les conseils d’administration est devenue pointilleuse et moins complaisante, mais également plus tatillonne, coûteuse et litigieuse ; les dirigeants se plaignent de la bureaucratisation de leur entreprise, du temps consacré pour satisfaire aux nouvelles exigences » 1. Denis Desautels, lui, signalait que « Certains prétendent que le souci de la conformité aux lois et aux règlements l’emporte sur les discussions stratégiques et sur la création de valeur. Et d’autres, que l’adoption ou l’endossement des nouvelles normes n’est pas toujours sincère et, qu’au fond, la culture de l’entreprise n’a pas réellement changé » 2.

Pour mémoire, voyons quelques obligations (de base) d’un administrateur de sociétés.

Au Québec, la Loi sur les sociétés par actions (L.r.Q., c. S-31.1) prévoit que les affaires de la société sont administrées par un conseil d’administration qui « exerce tous les pouvoirs nécessaires pour gérer les activités et les affaires internes de la société ou en surveiller l’exécution » (art. 112) et que, « Sauf dans la mesure prévue par la loi, l’exercice de ces pouvoirs ne nécessite pasl’approbation des actionnaires et ceux-ci peuvent être délégués à un administrateur, à un dirigeant ou à un ou plusieurs comités du conseil. »

De façon générale, les administrateurs de sociétés sont soumis aux obligations auxquelles est assujetti tout administrateur d’une personne morale en vertu du Code civil. « En conséquence, les administrateurs sont notamment tenus envers la société, dans l’exercice de leurs fonctions, d’agir avec prudence et diligence de même qu’avec honnêteté et loyauté dans son intérêt » (art. 119). L’intérêt de la société, pas l’intérêt de l’actionnaire. La loi fédérale présente des concepts semblables. (La Cour Suprême du Canada a d’ailleurs rappelé dans l’affaire BCE qu’il n’existe pas au Canada de principe selon lequel les intérêts d’une partie — les actionnaires, par exemple — doivent avoir priorité sur ceux des autres parties.)

Si la société fait appel publiquement à l’épargne, elle devient un émetteur assujetti. Alors s’ajoutent les règles de la Bourse concernant les exigences d’inscription initiale ainsi que celles concernant le maintien de l’inscription. S’ajoutent aussi les obligations édictées dans la Loi sur les valeursmobilières (L.R.Q., c. V-1.1), de même que les règlements qui en découlent, et dont l’Autorité des marchés financiers (AMF) est chargée de l’application. L’émetteur assujetti est tenu aux obligations d’information continue. Si vous êtes un administrateur ou un haut dirigeant d’un tel émetteur ou même d’une filiale d’un tel émetteur, vous êtes un initié avec des obligations particulières.

L’article 73 de cette Loi stipule que tel émetteur « … fournit, conformément aux conditions et modalités déterminées par règlement, l’information périodique au sujet de son activité et de ses affaires internes, dont ses pratiques en matière de gouvernance, l’information occasionnelle au sujet d’un changement important et toute autre information prévue par règlement. ». «L’émetteur assujetti doit organiser ses affaires conformément aux règles établies par règlement en matière de gouvernance». (art.73.1)

La mission de l’Autorité, (entendre ici AMF) telle qu’énoncée à l’article 276.1 de la Loi sur lesvaleurs mobilières se décline comme suit :

Favoriser le bon fonctionnement du marché des valeurs mobilières ;

Assurer la protection des épargnants contre les pratiques déloyales, abusives et frauduleuses ;

Régir l’information des porteurs de valeurs mobilières et du public sur les personnes qui font publiquement appel à l’épargne et sur les valeurs émises par celles-ci ;

Encadrer l’activité des professionnels des valeurs mobilières et des organismes chargés d’assurer le fonctionnement d’un marché des valeurs mobilières.

Dans sa loi constituante, l’Autorité a une mission plus élaborée qui reprend sensiblement les mêmes thèmes, mais en appuyant davantage sur la protection des consommateurs de produits et utilisateurs de services financiers. (art.4, L.R.Q., c. A-33.2)

Aux termes de la législation en vigueur, « L’Autorité exerce la discrétion qui lui est conférée en fonction de l’intérêt public» (art.316, L.R.Q., c. V-1.1) et un règlement pris en vertu de la présente loi confère un pouvoir discrétionnaire à l’Autorité » (art.334). En outre, toujours selon cette Loi, « Les instructions générales sont réputées constituer des règlements dans la mesure où elles portent sur un sujet pour lequel la loi nouvelle prévoit une habilitation réglementaire et qu’elles sont compatibles avec cette loi et les règlements pris pour son application. »

Je vous fais grâce du Règlement sur les valeurs mobilières (Décret 660-83 ; 115 G.O.2, 1511) ; quant à l’Annexe (51-102A5), portant sur la Circulaire de sollicitation de procuration par la direction, et celle (51-102A6) portant spécifiquement sur la Déclaration de la rémunération de la haute direction, j’y reviendrai plus loin.

Ceci pour une société qui ne fait affaire qu’au Québec, et à l’exclusion de toutes les autres législations et les nombreux règlements portant sur un secteur d’activité en particulier. Pensons juste aux activités qui peuvent affecter l’environnement, même de loin. Alors, si une société fait affaire ailleurs au Canada et aux É.-U. ou sur plusieurs continents — ajoutez des obligations, des modes différents de divulgation de l’information — et cela peut vous donner une petite idée de « l’industrie » qu’est devenue la gouvernance d’entreprise avec l’obligation de livrer l’information en continu et sous une forme de plus en plus détaillée. Et les administrateurs devraient tout savoir, avoir tout vu…

Les très nombreuses informations que nous publions rencontrent-elles l’objectif à l’origine de ces exigences ? Carol Liao soutient que « les autorités réglementaires sont par définition orientées vers l’actionnaire ce qui aurait mené à une augmentation des droits de ces derniers, bien au-delà de ce que les lois canadiennes (sur les sociétés) envisageaient. » On a vu plus haut que la Loi sur les sociétés par actions édicte que « les administrateurs sont notamment tenus envers la société dans l’exercice de leurs fonctions, d’agir avec prudence et diligence de même qu’avec honnêteté et loyauté dans son intérêt ». Se pourrait-il que « ce qui est dans l’intérêt supérieur des actionnaires ne coïncide pas avec une meilleure gouvernance ? (doesn’t align with better governance – that’s where the practice falls down »3.)

J’aime à croire que l’origine de l’obligation qui est faite aux entreprises de dire qui elles sont, ce qu’elles font, comment elles le font, et avec qui elles le font, est la protection du petit investisseur — vous et moi qui plaçons nos économies en prévision de nos vieux jours — comme disaient les anciens.

À moins d’y être obligé par son travail, qui comprend le contenu des circulaires de sollicitation de procuration par la direction, émises à l’intention des actionnaires ? Les Notices annuelles ? D’abord, qui les lit? Chaque fois que l’occasion m’en est donnée, je pose la question – et partout le même commentaire : si je n’avais pas les lire je ne les lirais pas. La quantité de papier rebute en partant ; la complexité des informations à publier en la forme prescrite est difficile à comprendre pour un non-expert, alors imaginez pour un petit investisseur. Si même il s’aventure à lire le document.

Donc, si tant est que les circulaires et les notices ne soient pratiquement lues que par ceux qui n’ont pas le choix de le faire, il serait peut-être temps de se demander à quoi, ou plutôt, à qui elles servent ? Et à quels coûts pour l’entreprise. A-t-on une idée de combien d’experts s’affairent avec le personnel de l’entreprise à préparer ces documents sans compter les réunions des comités d’Audit, de Ressources humaines, de Gouvernance et du conseil qui se pencheront sur diverses versions des mêmes documents ?

Encore une fois, pour quoi ? Pour qui ?

Pourquoi pas aux activistes de toutes origines ?

La dernière crise financière (2008/2009) semble avoir été l’accélérateur de l’activisme de groupes, autour des actionnaires, de même que l’arrivée d’experts de toutes sortes en gouvernance d’entreprise. Une industrie venait de naître! Le Rapport sur la gouvernance 2013, de Davies Ward Phillips & Vineberg, s.e. n.c. r. l., soutient qu’il s’agit d’une tendance alimentée surtout « par le nombre accru d’occasions d’activisme découlant de certaines tendances actuelles de la législation et des pratiques à vouloir que plus de questions soient soumises à l’approbation des actionnaires » 4.

Mais, l’a-t-on oublié ? Les administrateurs ont un devoir de fiduciaire envers la société, pas juste envers les actionnaires. Ils doivent assurer la pérennité de l’entreprise et pas juste afficher un rendement à court terme qui entraîne des effets pervers sur la gestion des ressources humaines et ne tient pas suffisamment compte d’une saine gestion des risques. Question : est-ce que la mesure de l’efficacité consiste en une reddition de compte trimestrielle ? Est-ce que cette reddition de compte, toute formatée, n’est pas en train de remplacer la responsabilité et l’engagement personnel des hauts dirigeants ? La pression mise sur les conseils d’administration, par certains activistes (d’ailleurs pas toujours actionnaires de l’entreprise !), et de leurs conseillers divers, pour discuter avec le président du conseil et le président du comité de ressources humaines est perçue comme une tentative de la part de ces activistes d’imposer leur programme — au détriment des autres actionnaires et de l’intérêt même de l’émetteur. Et comme certains fournisseurs de ces activistes (agences de conseils en vote) produisent des analyses pour leur clientèle en vue d’une recommandation de vote lors d’une assemblée annuelle — cette démarche peut être interprétée comme une pression à la limite de l’intimidation.