Voici le rapport annuel toujours très attendu de Spencer Stuart*.

Ce document présente un compte rendu très détaillé de l’état de la gouvernance dans les grandes sociétés publiques américaines (S&P 500).

On y découvre les résultats des changements dans le domaine de la gouvernance aux É.U. en 2016, ainsi que certaines tendances pour 2017.

Les thèmes abordés sont les suivants :

La composition des Boards

L’indépendance du président du CA

Les mandats des administrateurs et les limites aux nombres de mandats

L’âge de la retraite des administrateurs

L’évaluation des Boards

La nature des relations du Boards et de la direction avec les actionnaires

L’amélioration de la performance des Boards

Diverses informations, notamment :

Only 19% of new independent directors are active CEOs, chairs, presidents and chief operating officers, compared with 24% in 2011, 29% in 2006 and 49% in 1998, the first year we looked at this data for S&P 500 companies.

Active executives with financial backgrounds (CFOs, other financial executives, as well as investors and bankers) represent 15% of new independent directors this year, an increase from 12% last year. Another 10% of new directors are retired finance and public accounting executives.

On average, S&P 500 directors have 2.1 outside corporate board affiliations, although most directors aren’t restricted from serving on more.

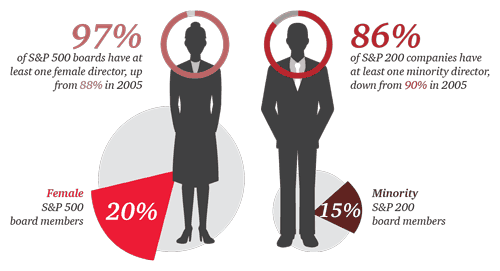

The number of boards with no female directors dropped to the lowest level we have seen; six S&P 500 boards (1%) have no women, a noteworthy decline from 2006, when 52 boards (11%) included no female members. Women now constitute 21% of all S&P 500 directors.

Among the boards of the 200 largest S&P companies, the total number of minority directors has held steady at 15% since 2011. 88% of the top 200 companies have at least one minority director, the same as 10 years ago.

Only 43% of S&P 500 CEOs serve on one or more outside corporate boards in addition to their own board, the same as in 2015. In 2006, 55% of CEOs served on at least one outside board.

Boards met an average of 8.4 times for regularly scheduled and special meetings, up from 8.1 last year and 8.2 five years ago. The median number of meetings rose from 7.0 last year to 8.0.

The average annual total compensation for S&P 500 directors, excluding the chairman’s compensation, is $280,389.

Over time, the compensation mix for directors has evolved, with more stock grants and fewer stock options. Today, stock grants represent 54% of total director compensation, versus 48% five years ago, while stock options represent 6% of compensation today, down from 10% five years ago. Cash accounts for 38% of director compensation, versus 39% in 2011.

95% of the independent chairmen of S&P 500 boards receive an additional fee, averaging $165,112. Nearly two-thirds of lead and presiding directors, 65%, receive additional compensation. The average premium paid to lead and presiding directors is $33,354.

Investor attention to board performance and governance continues to escalate, and, increasingly, it’s large institutional investors—so-called “passive” investors—who are making known their expectations in areas such as board composition, disclosure and shareholder engagement. Long-term investors have shifted their posture to taking positions on good governance, and are increasingly demonstrating common ground with activists on governance topics.

Board composition is a particular area of focus, as traditional institutional investors have become more explicit in demanding that boards demonstrate that they are being thoughtful about who is sitting around the board table and that directors are contributing. They are looking more closely at disclosures related to board refreshment, board performance and assessment practices, in some cases establishing voting policies on governance.

Boards are taking notice. Directors want to ensure that their boards contribute at the highest level, aligning with shareholder interests and expectations. In response, boards are enhancing their disclosures on board composition and leadership, reviewing governance practices and establishing protocols for engaging with investors. Here are some of the trends we are seeing in the key areas of investor concern.

Board composition

The composition of the board—who the directors are, the skills and expertise they bring, and how they interact—is critical for long-term value creation, and an area of governance where investors increasingly expect greater transparency. Shareholders are looking for a well-explained rationale for why the group of people sitting around the board table are the right ones based on the strategic priorities of the business. They want to know that the board has the processes in place to review and evolve board composition in light of emerging needs, and that the board regularly evaluates the contributions and tenure of current board members and the relevance of their experience.

Acknowledging investor interest in their composition, more boards are reviewing how to best communicate their thinking about the types of expertise needed in the board—and how individual directors provide that expertise. More than one-third of the 96 corporate secretaries responding to our annual governance survey, conducted each year as part of the research for the Spencer Stuart Board Index, said their board has changed the way it reports director bios/qualifications; among those that have not yet made changes, 15% expect the board to change how they present director qualifications in the future.

What’s happening to board composition in practice after all of the talk about increasing board turnover? In 2016, we actually saw a small decline in the number of new independent directors elected to S&P 500 boards. S&P 500 boards included in our index elected 345 new independent directors during the 2016 proxy year—averaging 0.72 new directors per board. Last year, S&P 500 boards added a total of 376 new directors (0.78 new directors per board).

Nearly one-third (32%) of the new independent directors on S&P 500 boards are serving on their first outside corporate board. Women account for 32% of new directors, the highest rate of female representation since we began tracking this data for the S&P 500. This year’s class of new directors, however, includes fewer minority directors (defined as African-American, Hispanic/Latino and Asian); 15% of the 345 new independent directors are minorities, a decrease from 18% in 2015.

With the rise of shareholder activism, we’ve also seen an increase in investors and investment managers on boards. This year, 12% of new independent directors are investors, compared with 4% in 2011 and 6% in 2006.

Independent board leadership

Boards continue to feel pressure from some shareholders to separate the chair and CEO roles and name an independent chairman. And, indeed, 27% of S&P 500 boards, versus 21% in 2011, have an independent chair. An independent chair is defined as an independent director or a former executive who has met applicable NYSE or NASDAQ rules for independence over time. This actually represents a small decline from 29% last year. Meanwhile, naming a lead director remains the most common form of independent board leadership: 87% of S&P 500 boards report having a lead or presiding director, nearly all of whom (98%) are identified by name in the proxy.

In our governance survey, 12% of respondents said their board has recently separated the roles of chairman and CEO, while 33% said their board has discussed whether to split the roles within the next five years. Among boards that expect to or have recently separated the chair and CEO roles, 72% cite a CEO transition as the reason, while 20% believe the chair/CEO split represents the best governance.

In response to investor interest in board leadership structure—and sometimes demands for an independent chairman—more boards are discussing their leadership structure in their proxies, for example, explaining the rationale for maintaining a combined chair/CEO role and delineating the responsibilities of the lead director. Among the lead director responsibilities boards highlight: approving the agenda for board meetings, calling meetings and executive sessions of independent directors, presiding over executive sessions, providing board feedback to the CEO following executive sessions, leading the performance evaluation of the CEO and the board assessment, and meeting with major shareholders or other external parties, when necessary. Some proxies include a letter to shareholders from the lead independent director.

Tenure and term limits

Director tenure continues to be a hot topic for some shareholders. While some rating agencies and investors have questioned the independence of directors with “excessive” tenure, there are no specific regulations or listing standards in the U.S. that speak to director independence based on tenure. And, in fact, most companies do not have governance rules limiting tenure; only 19 S&P 500 boards (4%) set an explicit term limit for non-executive directors, a modest increase from 2015 when 13 boards (3%) had director term limits.

Just 3% of survey respondents said their boards are considering establishing director term limits, but many boards are disclosing more in their proxies about director tenure. Specifically, boards are describing their efforts to ensure a balance between short-tenured and long-tenured directors. And several companies have included a short summary of the board’s average tenure accompanied by a pie chart breaking down the tenure of directors on the board (e.g., directors with less than five years tenure, between five and 10 years, and more than 10 years tenure on the board).

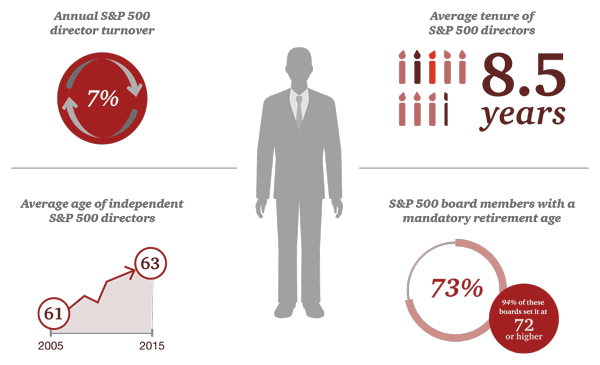

Among S&P 500 boards overall, the average board tenure is 8.3 years, a slight decrease from 8.7 five years ago. The median tenure has declined as well in that time, from 8.4 to 8.0. The majority of boards, 63%, have an average tenure between six and 10 years, but 19% of boards have an average tenure of 11 or more years.

We also looked this year at the tenure of individual directors: 35% of independent directors have served on their boards for five years or less, 28% have served for six to 10 years, and 22% for 11 to 15 years. Fifteen percent of independent directors have served on their boards for 16 years or more.

Mandatory retirement

In the absence of term or tenure limits, most S&P 500 boards rely on mandatory retirement ages to promote turnover. About three-quarters (73%) of S&P 500 boards report having a mandatory retirement age for directors. Eleven percent report that they do not have a mandatory retirement age, and 16% do not discuss mandatory retirement in their proxies.

Retirement ages have crept up in recent years, as boards have raised them to allow experienced directors to serve longer. Thirty-nine percent of boards have mandatory retirement ages of 75 or older, compared with 20% in 2011 and just 9% in 2006. Four boards have a retirement age of 80. The most common mandatory retirement age is 72, set by 45% of S&P 500 boards.

As retirement ages have increased, so has the average age of independent directors. The average age of S&P 500 independent directors is 63 today, two years older than a decade ago. In that same period, the median age rose from 61 to 64. Meanwhile, the number of older boards has increased; 37% of S&P 500 boards have an average age of 64 or older, compared with 19% a decade ago, and 15 of today’s boards (3%) have an average age of 70 or greater, versus four (1%) a decade ago.

Board evaluations

Another topic on which large institutional investors have become more vocal is board performance evaluations. Shareholders are seeking greater transparency about how boards address their own performance and the suitability of individual directors—and whether they are using assessments as a catalyst for refreshing the board as new needs arise.

We have seen a growing trend in support of individual director assessments as part of the board effectiveness assessment—not to grade directors, but to provide constructive feedback that can improve performance. Yet the pace of adoption of individual director assessments has been measured. Today, roughly one-third (32%) of S&P 500 boards evaluate the full board, committees and individual directors annually, an increase from 29% in 2011.

In our survey of corporate secretaries, respondents said evaluations are most often conducted by a director, typically the chairman, lead director or a committee chair. A wide range of internal and external parties are also tapped to conduct board assessments, including in-house and external legal counsel, the corporate secretary and board consulting firms. Thirty-five percent use director self-assessments, and 15% include peer reviews. According to proxies, a small number of boards, but more than in the past, disclose that they used an outside consultant to facilitate all or a portion of the evaluation process.

Shareholder engagement

In light of investors’ growing desire for direct engagement with directors, more boards have established frameworks for shareholders to raise questions and engage in meaningful, two-way discussions with the board. In addition to improving disclosures about board composition, assessment and other key governance areas, some boards include in their proxies a summary of their shareholder outreach efforts. For example, they detail the number of investors the board met with, the issues discussed and how the company and board responded. A few boards facilitate direct access to the board by providing contact information for individual directors, including the lead director and audit committee chair.

Going further, many boards now proactively reach out to their company’s largest shareholders. In our survey, 83% of respondents said management or the board contacted the company’s large institutional investors or largest shareholders, an increase from 70% the year prior. The most common topic about which companies engaged with shareholders was proxy access (52%), an increase from 33% in 2015. Other topics included “say on pay” (51%), CEO compensation (40%), director tenure (30%), board refreshment (27%), shareholder engagement approach (27%) and chairman independence (24%). Survey respondents also wrote in more than a dozen additional topics, including majority/cumulative voting, disclosure enhancements, environmental issues and gender pay equity.

Enhancing board performance

The topic of board refreshment can be a highly charged one for boards. But having the right skills around the table is critical for the board’s ability to provide the appropriate guidance and oversight of management. Furthermore, the capabilities and perspectives that a board needs evolve over time as the business context changes. Boards can ensure that they have the right perspectives around the table and are well-equipped to address the issues that drive shareholder value—which, after all, is what investors are looking for—by doing the following:

Viewing director recruitment in terms of ongoing board succession planning, not one-off replacements. Boards should periodically review the skills and expertise on the board to identify gaps in skills or expertise based on changes in strategy or the business context.

Proactively communicating the skill sets and expertise in the boardroom—and the roadmap for future succession. Publishing the board’s skill matrix and sharing the board’s thinking about the types of expertise that are needed on the board—and how individual directors provide that expertise—signals to investors that the board is thoughtful about board succession.

Setting expectations for appropriate tenure both at the aggregate and individual levels. By setting term expectations when new directors join, boards can combat the perceived stigma attached to leaving a board before the mandatory retirement age. Ideally, boards will create an environment where directors are willing to acknowledge when the board would benefit from bringing on different expertise.

Thinking like an activist and identifying vulnerabilities in board renewal and performance. Proactive boards conduct board evaluations annually to identify weaknesses in expertise or performance. They periodically engage third parties to manage the process and are disciplined about identifying and holding themselves accountable for action items stemming from the assessment.

Establishing a framework for engaging with investors. This starts with proactive and useful disclosure, which demonstrates that the board has thought about its composition, performance and other specific issues. In addition, it is valuable to have a protocol in place enumerating responsibilities related to shareholder engagement.

*Note: The Spencer Stuart Board Index (SSBI) is based on our analysis of the most recent proxy reports from the S&P 500, plus an extensive supplemental survey. The complete publication draws on the latest proxy statements from 482 companies filed between May 15, 2015, and May 15, 2016, and responses from 96 companies to our governance survey conducted in the second quarter of 2016. Survey respondents are typically corporate secretaries, general counsel or chief governance officers. Proxy and survey data have been supplemented with information compiled in Spencer Stuart’s proprietary database.

The complete publication, including footnotes, is available here.

Nous publions ici un cinquième billet de Danielle Malboeuf* laquelle nous a soumis ses réflexions sur les grands enjeux de la gouvernance des institutions d’enseignement collégial les 23 et 27 novembre 2013, le 24 novembre 2014 et le 4 septembre 2015, à titre d’auteure invitée.

Dans un premier article, publié le 23 novembre 2013 sur ce blogue, on insistait sur l’importance, pour les CA des Cégeps, de se donner des moyens pour assurer la présence d’administrateurs compétents dont le profil correspond à celui qui est recherché. D’où les propositions adressées à la Fédération des cégeps et aux CA pour élaborer un profil de compétences et pour faire appel à la Banque d’administrateurs certifiés du Collège des administrateurs de sociétés (CAS), le cas échéant. Un autre enjeu identifié dans ce billet concernait la remise en question de l’indépendance des administrateurs internes.

Le deuxième article publié le 27 novembre 2013 abordait l’enjeu entourant l’exercice de la démocratie par différentes instances au moment du dépôt d’avis au conseil d’administration.

Le troisième article portait sur l’efficacité du rôle du président du conseil d’administration (PCA).

Le quatrièmebillet abordait les qualités et les caractéristiques des bons administrateurs dans le contexte du réseau collégial québécois (CÉGEP)

Dans ce cinquième billet, l’auteure réagit aux préoccupations actuelles de la ministre de l’Enseignement supérieur eu égard à la gouvernance des CÉGEPS.

La gouvernance des CÉGEPS | Une responsabilité partagée

par

Danielle Malboeuf*

Dans les suites du rapport de la vérificatrice générale portant sur la gestion administrative des Cégeps, la ministre de l’Enseignement supérieur, madame Hélène David a demandé au ministère un plan d’action pour améliorer la gouvernance dans le réseau collégial. Voici un point de vue qui pourrait enrichir sa réflexion.

Rappelons que pour atteindre de haut standard d’excellence, les collèges doivent compter sur un conseil d’administration (CA) performant dont les membres font preuve d’engagement, de curiosité et de courage tout en possédant les qualifications suivantes : crédibles, compétents, indépendants, informés et outillés.

Considérant l’importance des décisions prises par les administrateurs, il est essentiel que ces personnes possèdent des compétences et une expertise pertinente. Parmi les bonnes pratiques en gouvernance, les CA devraient d’ailleurs élaborer un profil de compétences recherchées pour ses membres et l’utiliser au moment de la sélection des administrateurs. Au moment de solliciter la nomination d’un administrateur externe auprès du gouvernement, ce profil devrait être fortement recommandé. Sachant que chacun des 48 CA des Collèges d’enseignement général et professionnel compte sept personnes nommées par la ministre pour un mandat de trois ans renouvelable, il est important de lui rappeler l’importance d’en tenir compte.

Il est également essentiel qu’elle procède à ces nominations dans les meilleurs délais. À l’heure actuelle, on constate que, dans certains cas, le délai pour nommer et remplacer des administrateurs externes peut être de plusieurs mois. Cette situation est doublement préoccupante quand plusieurs membres quittent le CA en même temps. Sachant qu’il existe une banque de candidats dûment formés par le Collège des administrateurs de sociétés et des membres de plusieurs ordres professionnels qui répondent au profil de compétences recherchées par les collèges, il serait pertinent de recruter des candidats parmi ces personnes.

De plus, pour être en présence d’administrateurs performants, il est essentiel que ces personnes soient au fait de leurs rôles et responsabilités. Des formations devraient donc leur être offertes. Toutefois, cette formation ne doit pas se limiter à leur faire connaître les obligations légales et financières qui s’appliquent au réseau collégial, mais les bonnes pratiques de gouvernance doivent également leur être enseignées. À ce sujet, il faut se réjouir du souhait formulé par madame David afin d’offrir des formations en ce sens.

Signalons aussi que les administrateurs ne devraient pas se retrouver en situation de conflit d’intérêts. Ainsi, il faut s’assurer, entre autres, que les administrateurs internes ne subissent pas de pressions des groupes d’employés dont ils proviennent. Les conseils d’administration des collèges comptent quatre membres du personnel qui enrichissent les échanges par leurs expériences pertinentes. La Loi sur les collèges prévoit que ces administrateurs internes sont élus par leurs pairs. Dans plusieurs collèges, le processus de sélection est confié au syndicat qui procède à l’élection de leur représentant au conseil d’administration lors d’une assemblée syndicale. Ces personnes peuvent subir des pressions surtout quand certains syndicats inscrivent dans leur statut et règlement que ces personnes doivent représenter l’assemblée syndicale et y faire rapport. D’autres collèges ont prévu des modalités qui respectent beaucoup mieux l’esprit de la loi. On confie au secrétaire général, le mandat de recevoir les candidatures et de procéder dans le cadre de processus convenu à la sélection de ces personnes. Cette dernière pratique devrait être encouragée.

Considérant les pouvoirs du CA qui agit tant sur les aspects financiers et légaux que sur les orientations du collège, il est essentiel que la direction fasse preuve de transparence et transmette aux membres toutes les informations pertinentes. Pour permettre aux administrateurs de porter des jugements adéquats et de juger de la pertinence et de l’efficacité de sa gestion, le collège doit aussi leur fournir des indicateurs. Sachant que des indicateurs sont présents dans le plan stratégique, les administrateurs devraient, donc porter une attention toute particulière à ces indicateurs, et ce, sur une base régulière.

Par ailleurs, les administrateurs ne doivent pas hésiter à poser des questions et à demander des informations additionnelles, le cas échéant. Le président du CA peut, dans ce sens, jouer un rôle essentiel. Il doit, entre autres, porter un regard critique sur les documents qui sont transmis avant les rencontres et encourager la création de sous-comités pour enrichir les réflexions. Considérant le rôle qui lui est confié dans la Loi, les présidents de CA pourraient être tentés de se limiter à jouer un rôle d’animateur de réunions, ce qui n’est pas suffisant.

En résumé, la présence de CA performant dans les Cégeps exige une évolution des pratiques et idéalement, des modifications législatives qui mettront à contribution chacun des acteurs du réseau collégial.

_______________________

*Danielle Malboeuf est consultante et formatrice en gouvernance ; elle possède une grande expérience dans la gestion des CÉGEPS et dans la gouvernance des institutions d’enseignement collégial et universitaire. Elle est CGA-CPA, MBA, ASC, Gestionnaire et administratrice retraitée du réseau collégial et consultante.

___________________________

Articles sur la gouvernance des CÉGEPS publiés sur mon blogue par l’auteure :

Je suis tout à fait d’accord avec la teneur de l’article de l’IGOPP, publié par Yvan Allaire* intitulé « Six mesures pour améliorer la gouvernance des organismes publics au Québec», lequel dresse un état des lieux qui soulève des défis considérables pour l’amélioration de la gouvernance dans le secteur public et propose des mesures qui pourraient s’avérer utiles. Celui-ci fut a été soumis au journal Le Devoir, pour publication.

L’article soulève plusieurs arguments pour des conseils d’administration responsables, compétents, légitimes et crédibles aux yeux des ministres responsables.

Même si la Loi sur la gouvernance des sociétés d’État a mis en place certaines dispositions qui balisent adéquatement les responsabilités des C.A., celles-ci sont poreuses et n’accordent pas l’autonomie nécessaire au conseil d’administration, et à son président, pour effectuer une véritable veille sur la gestion de ces organismes.

Selon l’auteur, les ministres contournent allègrement les C.A., et ne les consultent pas. La réalité politique amène les ministres responsables à ne prendre principalement avis que du PDG ou du président du conseil : deux postes qui sont sous le contrôle et l’influence du ministère du conseil exécutif ainsi que des ministres responsables des sociétés d’État (qui ont trop souvent des mandats écourtés !).

Rappelons, en toile de fond à l’article, certaines dispositions de la loi :

– Au moins les deux tiers des membres du conseil d’administration, dont le président, doivent, de l’avis du gouvernement, se qualifier comme administrateurs indépendants.

– Le mandat des membres du conseil d’administration peut être renouvelé deux fois

– Le conseil d’administration doit constituer les comités suivants, lesquels ne doivent être composés que de membres indépendants :

1 ° un comité de gouvernance et d’éthique ;

2 ° un comité d’audit ;

3 ° un comité des ressources humaines.

– Les fonctions de président du conseil d’administration et de président-directeur général de la société ne peuvent être cumulées.

– Le ministre peut donner des directives sur l’orientation et les objectifs généraux qu’une société doit poursuivre.

– Les conseils d’administration doivent, pour l’ensemble des sociétés, être constitués à parts égales de femmes et d’hommes.

Yvan a accepté d’agir en tant qu’auteur invité dans mon blogue en gouvernance. Voici donc son article.

Six mesures pour améliorer la gouvernance des organismes publics au Québec

par Yvan Allaire*

La récente controverse à propos de la Société immobilière du Québec a fait constater derechef que, malgré des progrès certains, les espoirs investis dans une meilleure gouvernance des organismes publics se sont dissipés graduellement. Ce n’est pas tellement les crises récurrentes survenant dans des organismes ou sociétés d’État qui font problème. Ces phénomènes sont inévitables même avec une gouvernance exemplaire comme cela fut démontré à maintes reprises dans les sociétés cotées en Bourse. Non, ce qui est remarquable, c’est l’acceptation des limites inhérentes à la gouvernance dans le secteur public selon le modèle actuel.

En fait, propriété de l’État, les organismes publics ne jouissent pas de l’autonomie qui permettrait à leur conseil d’administration d’assumer les responsabilités essentielles qui incombent à un conseil d’administration normal : la nomination du PDG par le conseil (sauf pour la Caisse de dépôt et placement, et même pour celle-ci, la nomination du PDG par le conseil est assujettie au veto du gouvernement), l’établissement de la rémunération des dirigeants par le conseil, l’élection des membres du conseil par les « actionnaires » sur proposition du conseil, le conseil comme interlocuteur auprès des actionnaires.

Ainsi, le C.A. d’un organisme public, dépouillé des responsabilités qui donnent à un conseil sa légitimité auprès de la direction, entouré d’un appareil gouvernemental en communication constante avec le PDG, ne peut que difficilement affirmer son autorité sur la direction et décider vraiment des orientations stratégiques de l’organisme.

Pourtant, l’engouement pour la « bonne » gouvernance, inspirée par les pratiques de gouvernance mises en place dans les sociétés ouvertes cotées en Bourse, s’était vite propagé dans le secteur public. Dans un cas comme dans l’autre, la notion d’indépendance des membres du conseil a pris un caractère mythique, un véritable sine qua non de la « bonne » gouvernance. Or, à l’épreuve, on a vite constaté que l’indépendance qui compte est celle de l’esprit, ce qui ne se mesure pas, et que l’indépendance qui se mesure est sans grand intérêt et peut, en fait, s’accompagner d’une dangereuse ignorance des particularités de l’organisme à gouverner.

Ce constat des limites des conseils d’administration que font les ministres et les ministères devrait les inciter à modifier ce modèle de gouvernance, à procéder à une sélection plus serrée des membres de conseil, à prévoir une formation plus poussée des membres de C.A. sur les aspects substantifs de l’organisme dont ils doivent assumer la gouvernance.

Or, l’État manifeste plutôt une indifférence courtoise, parfois une certaine hostilité, envers les conseils et leurs membres que l’on estime ignorants des vrais enjeux et superflus pour les décisions importantes.

Évidemment, le caractère politique de ces organismes exacerbe ces tendances. Dès qu’un organisme quelconque de l’État met le gouvernement dans l’embarras pour quelque faute ou erreur, les partis d’opposition sautent sur l’occasion, et les médias aidant, le gouvernement est pressé d’agir pour que le « scandale » s’estompe, que la « crise » soit réglée au plus vite. Alors, les ministres concernés deviennent préoccupés surtout de leur contrôle sur ce qui se fait dans tous les organismes sous leur responsabilité, même si cela est au détriment d’une saine gouvernance.

Ce brutal constat fait que le gouvernement, les ministères et ministres responsables contournent les conseils d’administration, les consultent rarement, semblent considérer cette agitation de gouvernance comme une obligation juridique, un mécanisme pro-forma utile qu’en cas de blâme à partager.

Prenant en compte ces réalités qui leur semblent incontournables, les membres des conseils d’organismes publics, bénévoles pour la plupart, se concentrent alors sur les enjeux pour lesquels ils exercent encore une certaine influence, se réjouissent d’avoir cette occasion d’apprentissage et apprécient la notoriété que leur apporte dans leur milieu ce rôle d’administrateur.

Cet état des lieux, s’il est justement décrit, soulève des défis considérables pour l’amélioration de la gouvernance dans le secteur public. Les mesures suivantes pourraient s’avérer utiles :

Relever considérablement la formation donnée aux membres de conseil en ce qui concerne les particularités de fonctionnement de l’organisme, ses enjeux, ses défis et critères de succès. Cette formation doit aller bien au-delà des cours en gouvernance qui sont devenus quasi-obligatoires. Sans une formation sur la substance de l’organisme, un nouveau membre de conseil devient une sorte de touriste pendant un temps assez long avant de comprendre suffisamment le caractère de l’organisation et son fonctionnement.

Accorder aux conseils d’administration un rôle élargi pour la nomination du PDG de l’organisme ; par exemple, le conseil pourrait, après recherche de candidatures et évaluation de celles-ci, recommander au gouvernement deux candidats pour le choix éventuel du gouvernement. Le conseil serait également autorisé à démettre un PDG de ses fonctions, après consultation du gouvernement.

De même, le gouvernement devrait élargir le bassin de candidats et candidates pour les conseils d’administration, recevoir l’avis du conseil sur le profil recherché.

Une rémunération adéquate devrait être versée aux membres de conseil ; le bénévolat en ce domaine prive souvent les organismes de l’État du talent essentiel au succès de la gouvernance.

Rendre publique la grille de compétences pour les membres du conseil dont doivent se doter la plupart des organismes publics ; fournir une information détaillée sur l’expérience des membres du conseil et rapprocher l’expérience/expertise de chacun de la grille de compétences établie. Cette information devrait apparaître sur le site Web de l’organisme.

Au risque de trahir une incorrigible naïveté, je crois que l’on pourrait en arriver à ce que les problèmes qui surgissent inévitablement dans l’un ou l’autre organisme public soient pris en charge par le conseil d’administration et la direction de l’organisme. En d’autres mots, en réponse aux questions des partis d’opposition et des médias, le ministre responsable indique que le président du conseil de l’organisme en cause et son PDG tiendront incessamment une conférence de presse pour expliquer la situation et présenter les mesures prises pour la corriger. Si leur intervention semble insuffisante, alors le ministre prend en main le dossier et en répond devant l’opinion publique.

_______________________________________________

*Yvan Allaire, Ph. D. (MIT), MSRC Président exécutif du conseil, IGOPP Professeur émérite de stratégie, UQÀM

La question que pose l’auteur Robyn Bew, directeur à la National Association of Corporate Directors (NACD), est directe et d’une grande importance : Les Boards sont-ils prêts pour affronter les changements des 20 dernières années ?

En effet, cela fait déjà vingt ans que le rapport du NACD (Blue Ribbon Commission on Director Professionalism) a fait ses recommandations sur les principes de saine gouvernance.

Cet article nous invite à revisiter les règles de gouvernance à la lumière des changements significatifs survenus depuis 20 ans.

Il ne s’agit pas de rafraîchir la composition du CA, mais plutôt de s’assurer que ce dernier constitue un actif stratégique durable.

L’article a été publié aujourd’hui sur le site du Harvard Law School Forum on Corporate Governance.

In 1996, the Report of the NACD Blue Ribbon Commission on Director Professionalism made recommendations on issues including establishing mechanisms for appropriate director turnover/tenure limitations, evaluation of the full board and of individual directors, and ongoing director education. [1] It stated, “the primary goal of director selection is to nominate individuals who, as a group, offer a range of specialized knowledge, skills, and expertise that can contribute to the successful operation of the company,” and advocated that boards must “[expand] the pool of potential nominees considered to include a more diverse range of qualified candidates who meet established criteria.”[2]

Twenty years later, the world in which boards operate has been transformed in fundamental ways, including increased complexity in the business environment; rapidly changing technology; volatility in global politics as well as in international economic and trade flows; the proliferation of information; the presence of major threats such as cyberattacks; higher levels of engagement between companies, boards, and investors of all stripes, including activists; new regulatory requirements; and greater levels of scrutiny from the press and the public. The velocity of the changes directors are facing shows no signs of slowing down.

The NACD 2016 Blue Ribbon Commission began its dialogue by asking whether boards are keeping up, and concluded that there is no single answer. It is clear that advancing director ages and tenures, coupled with low boardroom turnover, are external symptoms that are of increasing concern to investors and other stakeholders. But equally—if not more—significant is the question of whether a board’s composition, director skill sets, and core board processes remain fit-for-purpose in a world where the board’s mandate is evolving in fundamental ways, including but not limited to earlier involvement in strategy-setting discussions with management and greater engagement between designated board members and major investors. This new mandate places substantially different demands on directors, and boards need to ask themselves, “Are we ready?”

Many stakeholders are focused on encouraging higher levels of director turnover—often termed “board refreshment”—through the use of tenure-limiting mechanisms. We believe that such mechanisms can help to drive needed change in the boardroom, but alone they are not sufficient to ensure that boards truly remain fit for-purpose over time. We are encouraging directors to think more holistically, and more ambitiously. Business as-usual approaches will not be sufficient.

As a starting point, directors should review the organization’s corporate governance guidelines, including the board’s mission and key operating principles. Are all board members familiar with them? How often are they reviewed and updated? How rigorously have they been implemented? Do they help to foster a culture of continuous improvement and ongoing learning?

Boards are unique entities. While (in the case of public companies) they are elected by and accountable to shareholders, they are self-constituting, self-evaluating, self-compensating, and self-perpetuating: that is, in the normal course of business, they control their own composition and succession planning. This also means that boards are equipped to take action to elevate their performance on an entirely self-directed, voluntary basis—and they should do so. Otherwise, if board leadership appears to be passive or slow to act in the face of a challenging competitive environment and greater scrutiny from all angles, directors should prepare for the possibility of “shock treatments” imposed from the outside, in the form of activist challenges, regulatory mandates, or quotas. Put another way, without sufficient and timely evolution, boards could face revolution.

Beyond “Board Refreshment”: Building a Strategic-Asset Board

Too many companies still view changes in their boardrooms as necessary primarily on an incremental basis and from the standpoint of director replacement—i.e., responding to the loss of directors due to age or other reasons for departure in a fairly reactive, one-off manner. And while (as noted above) the idea of “board refreshment” has attracted increasing attention in the corporate governance community, as well as with regulators and the press, in the words of one Commissioner, “the current definition [of board refreshment] can still be somewhat limiting—it can imply change for the sake of change.”

The Commission advocates a more ambitious approach, centered on proactive measures that help to build a strategic-asset board. Characteristics of this approach include:

A focus on continuous improvement of overall board composition, individual director skills, and boardroom processes—collectively aimed at achieving and maintaining a high-performance board—rather than a primarily reactive or event-driven approach to board change. One indicator of well-established continuous-improvement processes is that they are used in times of good performance, not just when the company is in a down cycle or facing external challenge

Using the company’s current and future needs as the starting point for determining board composition. Such an approach will certainly include considerations about maintaining an appropriate level of continuity and institutional memory in the boardroom—but in the words of Vanguard CEO Bill McNabb, “To be frank, board members cannot be more worried about their own seats than they are about the future of the company they oversee.”[3]

A set of tools and processes that works together as a system for continuous improvement—avoiding what one Commissioner called the “formulaic approach” of overreliance on automatic tenure-limiting mechanism

While outcomes will be specific to individual boards, in general, we expect to see improvements such as the following:

Boards that are composed of directors who collectively have the right skills and insights to support the formulation and execution of the organization’s strategy—in other words, boards where it is clear that the whole is greater than the sum of the parts

Boards that have the ability to adapt and retool themselves over time, so that they are able to maintain a superior level of oversight and guidance and evolve as the organization’s strategy and competitive environment evolve

Boards that are transparent in their communications with investors and other stakeholders about who they are and how they operate

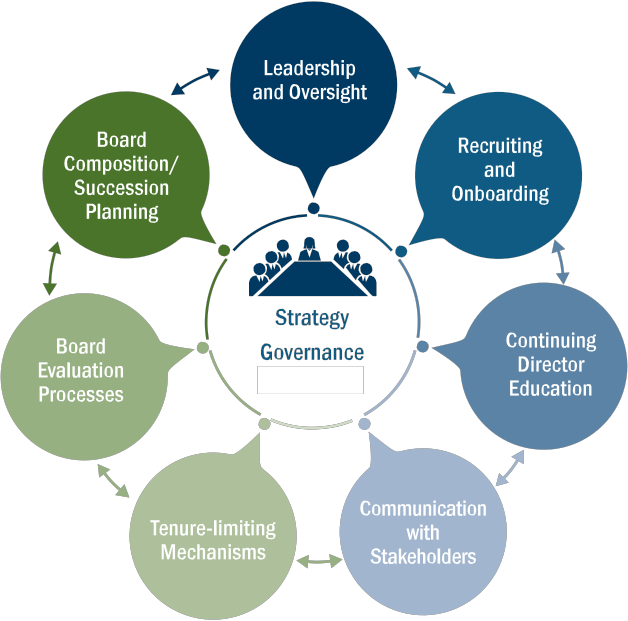

SECTION 1 of the report describes the ways in which the board’s mandate has evolved in response to external factors and strategic imperatives, and outlines the ways in which the Commission believes boards must respond: by moving beyond traditional approaches to “board refreshment” and establishing a system for continuous improvement in the boardroom.

SECTION 2 explores the key dimensions of continuous improvement, focusing on seven areas in particular: board leadership and oversight responsibilities; board composition and succession planning; recruiting and onboarding new directors; processes for board evaluation; continuing education; tenure-limiting mechanisms; and communication with shareholders and stakeholders.

SECTION 3 summarizes the Commission’s recommendations, and the Appendices provide tools and related resources to help boards implement the recommendations.

NACD has characterized the mission of the board as “[becoming] a strategic asset of the company measured by the contributions we make—collectively and individually—to the long-term success of the enterprise.” [4] We believe this report will help directors in organizations of all sizes and in all sectors to do exactly that.

Recommendations of the 2016 NACD Blue Ribbon Commission

Boards should review their governance principles on a regular basis (at least every other year) to ensure they are complete, up-to-date, and fully understood by current members and director candidates. Governance principles should incorporate a definition of director responsibilities, including a commitment to ongoing learning and the belief that service on the board should not be considered to be a permanent appointment.

The nominating and governance committee should oversee the board’s processes for continuous improvement, working in close coordination with the nonexecutive chair or lead director and with the endorsement of the full board.

Director renominations should not be a default decision, but an annual consideration based on a number of factors, including an assessment of current and future skill sets and leadership styles that are needed on the board.

Nominating and governance committees should develop a “clean-sheet” assessment of the board’s needs in terms of director skill sets and experience at least every two to three years, and use it as an input in continuous-improvement efforts (including recruitment and director education).

The director recruitment process should have a time horizon that matches the organization’s long-term strategy, typically three to five years or more. The process should be designed to include candidates from diverse backgrounds.

Recruiting and onboarding processes should familiarize prospective and new directors with the board’s governance principles and set expectations regarding criteria for renomination, ongoing director education, and other aspects of continuous improvement as defined by the board.

Conduct annual evaluations at the full-board level, and evaluations of committees and individual directors at least once every two years. Use a qualified independent third party on a periodic basis, to encourage candor and add a neutral perspective.

Participation in continuing education should be a requirement for all directors, regardless of experience level or length of board tenure.

Tenure is an important aspect of boardroom diversity. Nominating and governance committees should strive for a mix of tenures on the board—for example, maintaining a composition that includes at least one director with <5, 5–10, and >10 years of service.

High-performance boards will not need to rely exclusively on tenure-limiting mechanisms to ensure appropriate board turnover and composition. However, boards that use such policies should consider replacing or combining retirement age with a maximum term of service.

Communications with investors and other key stakeholders should include a detailed explanation of the link between the organization’s strategic needs and the board’s composition and skill sets, as well as information about the board’s continuous-improvement processes.

Tools for Directors

The report’s 12 appendices enable boards to benchmark their current practices and implement the report’s recommendations. Examples of appendix content are below.

Early Engagement: Going Beyond Traditional Board Succession Planning

A reference list of more than 25 questions to help directors evaluate the board’s ability to manage succession planning as a portfolio, instead of as a series of one-off replacements of individual directors; the strength of the board’s search capabilities, including early-engagement activities and the depth of the candidate pipeline; and the role that board and company culture play in succession planning.

Considerations for Upgrading Board Evaluation Processes

The appendix provides guidance to help boards

establish effective, ongoing rhythms for evaluation processes;

avoid “evaluation fatigue”;

inform the use of third-party facilitators;

make evaluations more holistic by incorporating input from management; and

act on evaluation results.

Guidelines for Developing Board and Individual-Director Learning Agendas

The appendix includes frameworks and questions to help inform full-board and individual-director education activities:

Suggested categories and topic areas for education, with sourcing strategies

A personal learning and development checklist for directors

Outline of a “lifecycle approach” to learning and development for the board, with components of a global director leadership profile

Tools, Templates, and Examples

Multiyear board succession planning matrix

Sample board and committee-level evaluation questions

New-director onboarding checklist

Examples of effective disclosures of director skills, board evaluations, and director education

Examples of corporate governance principles and board tenure policies

* * *

The complete publication is available exclusively to NACD members and is available for download here.

Endnotes:

1NACD, Report of the Blue Ribbon Commission on Director Professionalism, 2011 ed. (Washington, DC: NACD, 2011), pp. 12, 5, 15, 10.(go back)

4NACD, Report of the Blue Ribbon Commission on Board Evaluation: Improving Director Effectiveness, 3rd ed. (Washington, DC: NACD, 2010), p. 2.(go back)

Le rapport annuel de Davies est toujours très attendu car il brosse un tableau très complet de l’évolution de la gouvernance au Canada durant la dernière année.

Le document qui vient de sortir est en anglais mais la version française devrait suivre dans peu de temps.

Je vous invite donc à en prendre connaissance en lisant le court résumé ci-dessous et, si vous voulez en savoir plus sur les thèmes abordés, vous pouvez télécharger le document de 100 pages sur le site de l’entreprise.

Davies Governance Insights 2016, provides analysis of the top governance trends and issues important to Canadian boards, senior management and governance observers.

The 2016 edition provides readers with our take on important topics ranging from shareholder engagement and activism to leadership diversity and the rise in issues facing boards and general counsel. We also provide practical guidance for boards and senior management of public companies and their investors on these and many other corporate governance topics that we expect will remain under focus in the 2017 proxy season.

On me demande souvent de proposer un livre qui fait le tour de la question eu égard à ce qui est connu comme statistiquementvalide sur les relations entre la gouvernance et le succès des organisations (i.e. la performance financière !)

Le volume publié par David F. Larckeret Brian Tayan, professeurs au Graduate School de l’Université Stanford, en est à sa deuxième édition et il donne l’heure juste sur l’efficacité des principes de gouvernance.

Je vous recommande donc vivement ce volume.

Également, je profite de l’occasion pour vous indiquer que je viens de recevoir la dernière version des Principes de gouvernance d’entreprise du G20 et de l’OCDEen français et j’ai suggéré au Collège des administrateurs de sociétés (CAS) d’inclure cette publication dans la section Nouveauté du site du CAS.

Il s’agit d’une publication très attendue dans le monde de la gouvernance. La documentation des organismes internationaux est toujours d’abord publiée en anglais. Ce document en français de l’OCDE sur les principes de gouvernance est la bienvenue !

Voici une brève présentation du volume de Larcker. Bonne lecture !

This is the most comprehensive and up-to-date reference for implementing and sustaining superior corporate governance. Stanford corporate governance experts David Larcker and Bryan Tayan carefully synthesize current academic and professional research, summarizing what is known and unknown, and where the evidence remains inconclusive.

Corporate Governance Matters, Second Edition reviews the field’s newest research on issues including compensation, CEO labor markets, board structure, succession, risk, international governance, reporting, audit, institutional and activist investors, governance ratings, and much more. Larcker and Tayan offer models and frameworks demonstrating how the components of governance fit together, with updated examples and scenarios illustrating key points. Throughout, their balanced approach is focused strictly on two goals: to “get the story straight,” and to provide useful tools for making better, more informed decisions.

This edition presents new or expanded coverage of key issues ranging from risk management and shareholder activism to alternative corporate governance structures. It also adds new examples, scenarios, and classroom elements, making this text even more useful in academic settings. For all directors, business leaders, public policymakers, investors, stakeholders, and MBA faculty and students concerned with effective corporate governance.

Selected Editorial Reviews

An outstanding work of unique breadth and depth providing practical advice supported by detailed research.

Alan Crain, Jr., Senior Vice President and General Counsel, Baker Hughes

Extensively researched, with highly relevant insights, this book serves as an ideal and practical reference for corporate executives and students of business administration.

Narayana N.R. Murthy, Infosys Technologies

Corporate Governance Matters is a comprehensive, objective, and insightful analysis of academic and professional research on corporate governance.

Professor Katherine Schipper, Duke University, and former member of the Financial Accounting Standards Board

Voici un récent article publié par Julie Hembrock Daum, directrice à Spencer Stuart et Susan Stauberg, PDG à Fondation WomenCorporateDirectors.

Cet article a été publié dans le Harvard Law School Forum aujourd’hui et il présente l’état de la gouvernance à l’échelle internationale (60 pays) en mettant particulièrement l’accent sur la diversité et les différences de perception entre les hommes et les femmes qui occupent des postes d’administrateurs de grandes sociétés privées ou publiques.

On me demande souvent de proposer des références en relation avec la gouvernance globale. Les gens veulent connaître les tendances et les progrès des efforts entrepris dans le domaine de la diversité dans le monde.

L’enquête citée ci-dessous fournit des données actuelles sur les principaux enjeux concernant les Board.

Je crois que tous les gestionnaires seront intéressés par la présentation succincte, claire et bien illustrée des données de la mondialisation de la gouvernance.

The growing demands on corporate boards are transforming boardrooms globally, with directors taking on a more strategic, dynamic and responsive role to help steer their companies through a hypercompetitive and volatile business environment. Economic and political uncertainties make long-term planning more difficult. The proliferation of cyber attacks—and their consequences for business in financial olosses and reputational damage—increases the scope of risk oversight. A rise in institutional and activist shareholder activity requires boards to identify vulnerabilities in board renewal and performance and, in some cases, establish protocols for engagement. And all of these demands have pushed issues around board composition and diversity to the fore, as boards cannot afford to have directors around the table who aren’t delivering value.

Boardroom presentation

In this context, Spencer Stuart, the WomenCorporateDirectors (WCD) Foundation, Professor Boris Groysberg and doctoral candidate Yo-Jud Cheng of Harvard Business School and researcher Deborah Bell partnered together on the 2016 Global Board of Directors Survey, one of the most comprehensive surveys of corporate directors around the world.

We received responses from more than 4,000 male and female directors from 60 countries, providing a comprehensive snapshot of the business climate and strategic priorities as seen from the boardroom of many of the world’s top public and large, privately held companies.

The survey explores in depth how boards think and operate. It captures in detail the governance practices, strategic priorities and views on board effectiveness of corporate directors around the world. It also confirmed many of our observations from working with boards. The economy is top of mind, and many directors are uncertain about economic prospects and not seeing growth in the future. At the same time, directors are responding proactively to the many new demands they face, looking for opportunities to enhance composition and improve board performance.

Findings compare and contrast the views between male and female corporate board directors, and highlight similarities and differences between public and private companies and among directors from different regions in five key areas:

Political and economic landscape

Company strategy and risks

Board governance and effectiveness

Board diversity and quotas

Director identification and recruitment

This post highlights key findings around these topics, providing directors an overview of how their peers view their own boards and the challenges that their companies face. In subsequent reports, we will dive deeper into specific governance areas and explore additional perspectives on board composition, risk areas, and strengths and weaknesses in boardrooms today.

Key Findings

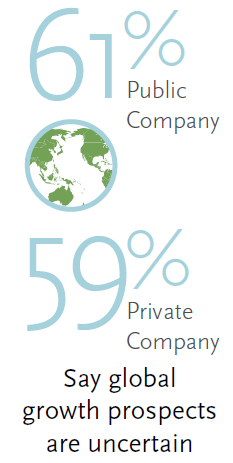

Political and Economic Landscape: Uncertainty dominates boardroom outlook.

Our survey finds that directors around the world are uncertain about global growth prospects, with directors in North America and Western Europe least confident about the prospects for growth. Sixty-three percent of directors in these regions see uncertain economic conditions, compared with 36% in Asia and 40% in Africa.

Only 2% of directors across all regions predict a period of strong global growth over the next three years, while 16% expect a global slowdown. “This pessimism about growth is one of the most surprising findings of our survey,” said Boris Groysberg of Harvard Business School. “It seems that the market volatility and low prospects for growth as well as the unpredictable economic outlook are what keep board members awake at night.”

More than one-third of directors of companies headquartered in Asia and roughly one-quarter of directors of companies in Australia/New Zealand expect relatively faster growth in emerging economies versus developed countries.

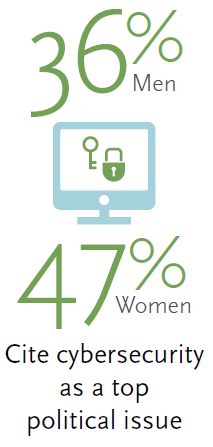

Political and Economic Landscape: Economy, regulations and cybersecurity top issues for directors.

Across all industries and regions, directors rank the economy and the regulatory environment as the political issues most relevant to them. Cybersecurity is an increasingly important issue in many regions. More than one-third of directors of companies in Australia/New Zealand, North America and Western Europe say cybersecurity is a top issue. “Cybersecurity continues to be a leading issue on the agenda from a regulatory, reputational and contingency standpoint,” says Julie Hembrock Daum, head of Spencer Stuart’s North American Board Practice.

“We see boards considering a number of different approaches to getting smart about the broader impact of technology on the business. In certain cases they have added a director with a strong digital or security background. However, the board should not isolate cybersecurity responsibility with just this one board member, but continue to view cybersecurity as a full board priority.”

Political instability is a concern in several regions. In Central and South America, one-half of directors cite political instability as an issue. Corporate tax rates are an issue particularly in North America.

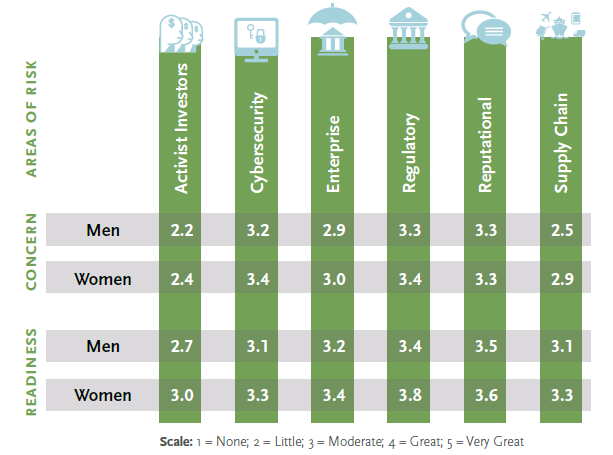

Company Risks: Women directors report higher concerns about risk than male directors.

Directors globally express the most concern about regulatory and reputational risks, followed by cybersecurity, and less about activist investors and supply chain risks. In general, directors report that their companies are prepared to handle the most important risks, with companies’ level of readiness matching the most concerning areas of risk. However, directors of private companies systematically rank their boards as being less prepared versus public company boards when it comes to such risks.

Nearly across the board, female directors report a higher level of concern about various risks to a company than their male peers—from concerns about activist investors and cybersecurity to regulatory risk and the supply chain. However, female directors also feel that their companies have a higher level of readiness to address these risks than do their male cohorts.

Susan Stautberg, chairman and CEO of the WCD Foundation, believes that women directors may be educating themselves more about the potential risks:

“We believe that women in particular bring a real thirst for knowledge and curiosity to their board service, and this includes getting up-to-speed on what the real risks are to an organization. All good directors do this, but we think being relatively new to the boardroom can create a greater sense of urgency to learn.”

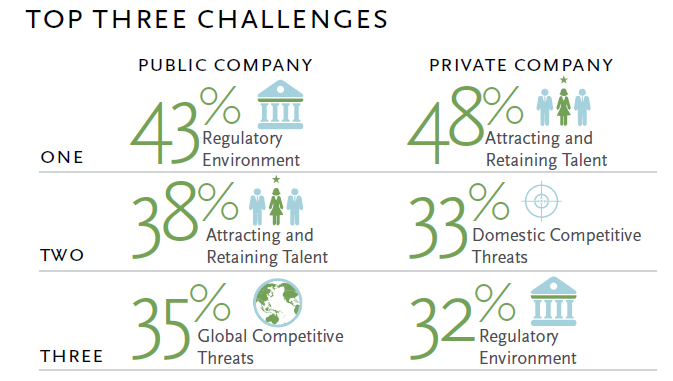

Strategy: Top challenges differ for public and private companies.

Talent, regulations, global and domestic competition, and innovation are seen by directors as the top impediments to achieving their companies’ strategic objectives. How those challenges rank specifically depends in part on whether directors are serving public or private companies.

Nearly half of private company directors (versus 38% of public company directors) rate attracting and retaining talent as a key challenge to achieving their company’s strategic objectives. This is followed by domestic competitive threats, the regulatory environment, innovation and global competitive threats. Among public companies, 43% of directors (versus 32% of private company directors) say the regulatory environment is a top challenge, followed by attracting and retaining talent, global competitive threats, innovation and domestic competitive threats.

“This was interesting because we do see in larger, more established public companies a greater maturity in their HR processes and deeper resources invested in talent management and development,” says Daum. “Identifying and recruiting individuals who fit the culture, bring impact to the organization and endure is a high priority for nearly all companies. However, many private companies, which tend to be smaller and have less brand awareness as a whole, often have less robust HR structures to attract the level of talent across the organization.”

Perceived challenges also differ somewhat by industry and region, with the regulatory environment being more concerning for companies in the energy/utilities, financials/professional services and healthcare industries, and in Asia, Australia/New Zealand, North America and Western Europe. Global competitive threats are the leading concern for companies in the industrials and materials sectors, and in Western Europe.

Interestingly, while cybersecurity is viewed as an important risk, few directors consider it a major challenge to achieving strategic objectives. Similarly, activist shareholders, compensation, cost of commodities and supply chain risk are not perceived as challenges to achieving strategic goals.

Boardroom Grades: Directors consider boards weaker in people-related processes.

On average, directors rate their board’s overall performance as being slightly above average (3.7 out of 5). Directors see their boards as having the strongest processes related to staying current on the company and the industry, compliance, financial planning and board composition, and weakest in cybersecurity, the evaluation of individual directors, CEO succession planning and HR/talent management.

“These ratings underscore directors’ views that attracting and retaining top talent is a common challenge, and underline the need for these HR competencies on boards,” says Stautberg. Harvard Business School doctoral candidate Yo-Jud Cheng adds, “Despite the fact that directors recognize their weaknesses in these areas, boards continue to prioritize more conventional areas of expertise, such as industry knowledge and auditing, in their appointments of new directors.”

Public company directors rate their overall board performance slightly higher than private company directors (3.8 versus 3.4) and give themselves higher marks for creating effective board structures, evaluation of individual directors, cybersecurity and compliance. We also see some variation across regions.

Board Turnover: Directors—especially women—favor tools to trigger change.

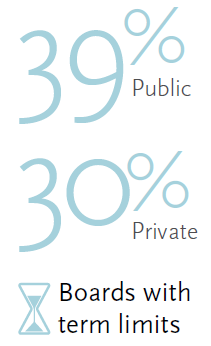

A little more than one-third of boards have term limits for directors, averaging six years, while approximately one-quarter of boards have a mandatory retirement age, averaging 72 years. Boards in Western Europe are most likely to have term limits, and boards in North America are least likely to set term limits. However, boards in North America are more likely to have a mandatory retirement age than boards in Western Europe (34% versus 18%). We also see a stark contrast between public and private companies in both term limits (39% versus 30%) and mandatory retirement ages (33% versus 12%).

While these tools for triggering director turnover generally have not been widely adopted, the survey indicates that directors favor adoption of such mechanisms. Sixty percent of directors think that boards should have mandatory term limits for directors, and 45% think that there should be a mandatory retirement age. Even in private companies, which are considerably less likely to adopt these practices today, directors shared similar opinions as compared to their counterparts in public companies. Female directors even more strongly support triggers for turnover; 68% (versus 56% of men) favor director term limits and 57% (versus 39% of men) support mandatory retirement ages.

“It was encouraging to see the majority of respondents in favor of retirement ages and term limits. Turnover among S&P 500 companies has trended at 5% to 7%—roughly 300 to 350 seats a year. Boards need tools they can use to ensure that new perspectives and thinking are regularly being brought to the boardroom,” says Daum. “This isn’t just an issue tied to activist shareholders, but something institutional shareholders are asking about as well: what are boards doing to ensure independent and fresh thinking?”

Not surprisingly, 43% of directors believe that a director loses his or her independence after about 10 years. Respondents from North America are less likely to tie director independence to years served, with only one-third agreeing that a director loses independence after a certain amount of time on the board.

Public companies represented in the survey have larger boards than private companies—on average 8.9 directors versus 7.6—and a larger representation of independent directors, 74% versus 54%. Yet, public and private company boards are similar in terms of the representation of women, minorities and new directors. On average, 18% of board members are women, 7% are ethnic minorities and 13% have been appointed in the past 12 months.

“This finding was very interesting. There has been much debate about the use and effectiveness of quotas. To see the relative parity of diversity among public and private companies reinforces that the tone needs to come from the top regarding bringing a fresh, diverse perspective representative of the company’s stakeholders and interests,” says Daum. Groysberg adds, “Although we are hearing more talk about the importance of diversity from boards, it’s not necessarily translating into numbers. Unfortunately, we haven’t seen as much progress as we were hoping for compared to our past survey on the diversity of boards.”

Boards are largest in the financials/professional services sector (9.1 directors) and smallest in the IT/telecom sector (7.5 directors). Female representation is highest (20% or more) in the consumer staples, financial services/professional services and consumer discretionary sectors, and lowest in IT/telecom (13%).

Looking across regions, board size is smallest in Australia/New Zealand, where boards average 6.7 members, as compared to the global average of 8.5 members. Boards in Australia/New Zealand and North America have the highest proportion of independent directors, and boards in Asia have the lowest proportion. Female representation is lowest in Central and South America and Asia.

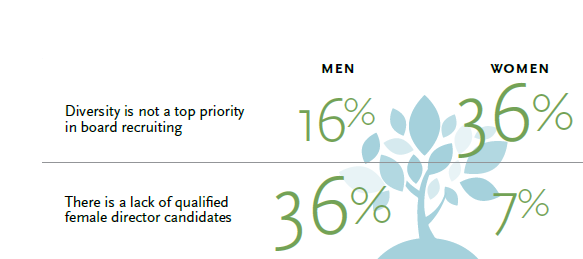

Boardroom Diversity: Why isn’t the number of women on boards increasing?

As the percentage of women on boards remains stagnant, there is both a gender divide and a generation divide on why this is. Male directors, especially older respondents, report the “lack of qualified female candidates,” while women directors most often cite the fact that diversity is not a priority in board recruiting and that traditional networks tend to be male-dominated. Younger male directors surveyed (those 55 and younger) are inclined to agree with women that traditional networks tend to be male-dominated. “Men in the younger generation, I think, just see their qualified female colleagues out there, but know that the traditional board networks still tend to be male,” says Stautberg. “It’s often hard to see an informal ‘network’ if you are in the middle of it, but you can see it very clearly when you’re on the outside.”

Boardroom Diversity: Quotas not supported overall.

Nearly 75% of surveyed directors do not personally support boardroom diversity quotas, but support for quotas varies significantly by gender and, to a lesser degree, by age. Forty-nine percent of female directors support diversity quotas, but only 9% of male directors do. Older women are less likely to favor quotas than younger women; 67% of female directors ages 55 and younger personally support boardroom quotas, compared with 36% of female directors over 55 (the majority of male directors, of any age, do not support quotas). Female directors also are more likely to be in favor of government regulatory agencies requiring boards to disclose specific practices/steps being taken to seat diverse candidates (43% versus 14% of male directors).

If quotas aren’t the answer, what do directors think would increase board diversity? Male and female directors agree that having board leadership that champions board diversity is the most effective way to build diverse corporate boards. Men feel more strongly than women that efforts to develop a pipeline of diverse board candidates through director advocacy, mentorship and training is an effective way to increase diversity.

Directors as a whole agree that shareholder pressure and board targets are less effective tools for increasing board diversity.

Boardroom Diversity: Search firms have been successful in expanding the talent pool of qualified female directors.

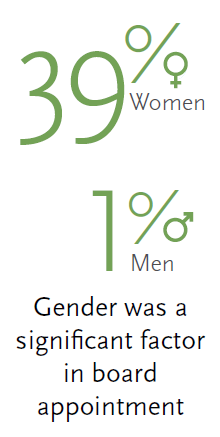

Directors take a variety of pathways to the boardroom: in roughly equal measures, directors were known to the board or another director, recruited by a search firm or known by the CEO. Public company directors are more likely to be recruited by an executive search firm than private company directors, while private company directors are more likely to have been appointed by a major shareholder.

The survey highlights gender differences, as well, in the paths to the boardroom. Female directors are more likely than their male counterparts to have been recruited by an executive search firm, while male directors are more likely to have been appointed by a major shareholder. “Search firms may be able to open doors that networking opportunities may not have been doing until relatively recently, at least for women,” says Stautberg. “Building up networks and getting known is something that women directors are engaging in much more actively now.”

And, indeed, 39% of female directors report that their gender was a significant factor in their board appointment, versus 1% of men.

Conclusion

Corporate boards face no shortage of challenges—from economic uncertainty to strategic and competitive shifts to a dynamic set of risks. Investor attention to board performance and governance has also escalated, and many boards are holding themselves to higher standards. Directors want to ensure that their boards contribute at the highest level, incorporating diverse perspectives, aligning with shareholder interests and setting a positive tone at the top for the organization.

Yet our research has revealed a gap between best practice and reality, especially in areas such as board diversity, HR/talent management, CEO succession planning and director evaluations. But the study provides hope that boards will make progress, as directors support practices that can help promote change. Future research is needed to track progress on these fronts and to study the impact of measures such as quotas and diversity on board performance.

Amid the many challenges confronting corporations—and the growing expectations on corporate boards—directors must be thoughtful about defining the skill sets needed around the board table and diligent in recruiting the right directors, planning for CEO succession and evaluating their own performance. In this way, they will be best positioned to contribute at the high levels which they are demanding of themselves, and to which others are holding them accountable.

*Julie Hembrock Daum leads the North American Board Practice at Spencer Stuart, and Susan Stautberg is the Chairman and CEO of the WomenCorporateDirectors Foundation. This post relates to the 2016 Global Board of Directors Survey, a co-publication from Spencer Stuart and the WCD Foundation authored by Ms. Daum; Ms. Stautberg; Dr. Boris Groysberg, Richard P. Chapman Professor of Business Administration at Harvard Business School; Yo-Jud Cheng, doctoral candidate at Harvard Business School; and Deborah Bell, researcher.

Nous publions ici un quatrième billet de Danielle Malboeuf* laquelle nous a soumis ses réflexions sur les grands enjeux de la gouvernance des institutions d’enseignement collégial les 23 et 27 novembre 2013, à titre d’auteure invitée.

Dans un premier billet, publié le 23 novembre 2013 sur ce blogue, on insistait sur l’importance, pour les CA des Cégep, de se donner des moyens pour assurer la présence d’administrateurs compétents dont le profil correspond à celui recherché.

D’où les propositions adressées à la Fédération des cégeps et aux CA pour préciser un profil de compétences et pour faire appel à la Banque d’administrateurs certifiés du Collège des administrateurs de sociétés (CAS), le cas échéant. Un autre enjeu identifié dans ce billet concernait la remise en question de l’indépendance des administrateurs internes.

Le deuxième billet publié le 27 novembre 2013 abordait l’enjeu entourant l’exercice de la démocratie par différentes instances au moment du dépôt d’avis au conseil d’administration.

Le troisième billet portait sur l’efficacité du rôle du président du conseil d’administration (PCA).

Ce quatrième billet est une mise à jour de son dernier article portant sur le rôle du président de conseil.

Voici donc l’article en question, reproduit ici avec la permission de l’auteure.

Vos commentaires sont appréciés. Bonne lecture.

________________________________________

LE RÔLE DU PRÉSIDENT DU CONSEIL D’ADMINISTRATION | LE CAS DES INSTITUTIONS D’ENSEIGNEMENT COLLÉGIAL

par Danielle Malboeuf*

Il y a deux ans, je publiais un article sur le rôle du président du conseil d’administration (CA) [1]. J’y rappelais le rôle crucial et déterminant du président du CA et j’y précisais, entre autres, les compétences recherchées chez cette personne et l’enrichissement attendu de son rôle.

Depuis, on peut se réjouir de constater qu’un nombre de plus en plus élevé de présidents s’engagent dans de nouvelles pratiques qui améliorent la gouvernance des institutions collégiales. Ils ne se limitent plus à jouer un rôle d’animateurs de réunions, comme on pouvait le constater dans le passé.

Notons, entre autres, que les présidents visent de plus en plus à bien s’entourer, en recherchant des personnes compétentes comme administrateurs. D’ailleurs, à cet égard, les collèges vivent une situation préoccupante. La Loi sur les collèges d’enseignement général et professionnel prévoit que le ministre [2] nomme les administrateurs externes. Ainsi, en plus de connaître des délais importants pour la nomination de nouveaux administrateurs, les collèges ont peu d’influence sur leur choix.

Présentement, les présidents et les directions générales cherchent donc à l’encadrer. Ils peuvent s’inspirer, à cet égard, des démarches initiées par d’autres organisations publiques en établissant, entre autres, un profil de compétences recherchées qu’ils transmettent au ministre. Ils peuvent ainsi tenter d’obtenir une complémentarité d’expertise dans le groupe d’administrateurs.

Une fois les administrateurs nommés, les présidents doivent se préoccuper d’assurer leur formation continue pour développer les compétences recherchées. Ils se donnent ainsi l’assurance que ces personnes comprennent bien leur rôle et leurs responsabilités et qu’elles sont outillées pour remplir le mandat qui leur est confié. De plus, ils doivent s’assurer que les administrateurs connaissent bien l’organisation, qu’ils adhèrent à sa mission et qu’ils partagent les valeurs institutionnelles. En présence d’administrateurs compétents, éclairés, et dont l’expertise est reconnue, il est plus facile d’assurer la légitimité et la crédibilité du CA et de ses décisions.

Un président performant démontrera aussi de grandes qualités de leadership. Il fera connaître à toutes les instances du milieu le mandat confié au CA. Il travaillera à mettre en place un climat de confiance au sein du CA et avec les gestionnaires de l’organisation. Il cherchera à exploiter l’ensemble des compétences et à faire jouer au CA un rôle qui va au-delà de celui de fiduciaire, soit celui de contribuer significativement à la mission première du cégep : donner une formation pertinente et de qualité où l’étudiant et sa réussite éducative sont au cœur des préoccupations.

Plusieurs ont déjà fait le virage… c’est encourageant ! Les approches préconisées par l’Institut sur la gouvernance des organismes publics et privés (IGOPP) et le Collège des administrateurs de sociétés (CAS) puis reprises dans la loi sur la gouvernance des sociétés d’État ne sont sûrement pas étrangères à cette évolution. En fournissant aux présidents de CA le soutien, la formation et les outils appropriés pour améliorer leur gouvernance, le Centre collégial des services regroupés (CCSR) [3] contribue à assurer le développement des institutions collégiales dans un contexte de saine gestion.

Un CA performant est guidé par un président compétent.

*Danielle Malboeuf est consultante et formatrice en gouvernance ; elle possède une grande expérience dans la gestion des CEGEP et dans la gouvernance des institutions d’enseignement collégial et universitaire. Elle est CGA-CPA, MBA, ASC, Gestionnaire et administratrice retraité du réseau collégial et consultante.

Les investisseurs et les actionnaires reconnaissent le rôle prioritaire que les administrateurs de sociétés jouent dans la gouvernance et, conséquemment, ils veulent toujours plus d’informations sur le processus de nomination des administrateurs et sur la composition du conseil d’administration.

L’article qui suit, paru sur le Forum du Harvard Law School, a été publié par Paula Loop, directrice du centre de la gouvernance de PricewaterhouseCoopers. Il s’agit essentiellement d’un compte rendu sur l’évolution des facteurs clés de la composition des conseils d’administration. La présentation s’appuie sur une infographie remarquable.

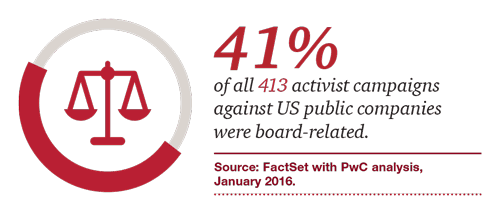

Ainsi, on apprend que 41 % des campagnes menées par les activistes étaient reliées à la composition des CA, et que 20 % des CA ont modifié leur composition en réponse aux activités réelles ou potentielles des activistes.

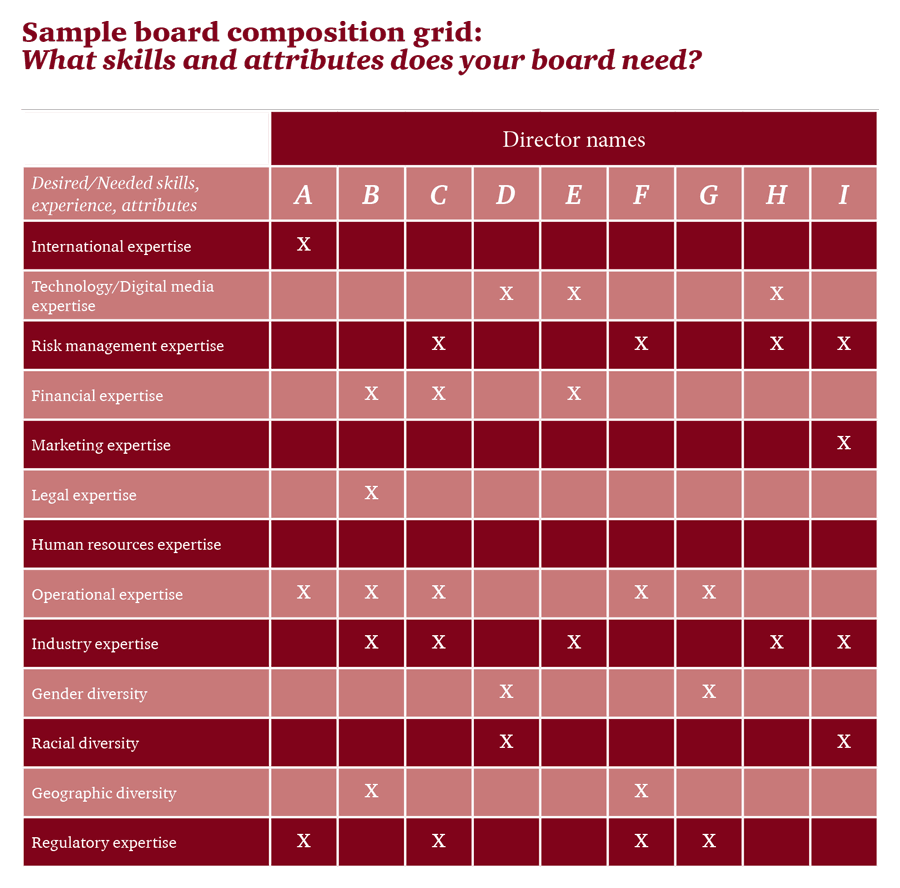

L’article s’attarde sur la grille de composition des conseils relative aux compétences et habiletés requises. Également, on présente les arguments pour une plus grande diversité des CA et l’on s’interroge sur la situation actuelle.