Voici un article publié sur le site de la HLS par Michael McCauley* qui montre comment la Florida State Board of Administration (SBA) évalue la gouvernance des entreprises dans laquelle elle investit.

Il m’apparaît utile de comprendre le processus décisionnel des investisseurs institutionnels, si l’on veut connaître les variables de la gouvernance dont elles tiennent compte.

L’auteur explique la méthodologie utilisée par la SBA dans sa quête d’information sur les entreprises visées.

Bonne lecture et joyeux temps des fêtes !

2016 Corporate Governance Annual Summary

The Florida SBA’s annual corporate governance summary explains how the Board makes proxy voting decisions, describes the process and policies used to analyze corporate governance practices, and details significant market issues affecting global corporate governance practices at owned companies. The SBA acts as a strong advocate and fiduciary for Florida Retirement System (FRS) members and beneficiaries, retirees, and other non-pension clients to strengthen shareowner rights .and promote leading corporate governance practices at U.S. and international companies in which the SBA holds stock.

The SBA’s corporate governance activities are focused on enhancing share value and ensuring that public companies are accountable to their shareowners with independent boards of directors, transparent disclosures, accurate financial reporting, and ethical business practices designed to protect the SBA’s investments.

The SBA’s annual corporate governance summary is designed to provide transparency of investment management activities involving responsible investment practices, proxy voting conduct, and engagement with owned companies. The report broadly conforms to the main principles for external responsibilities endorsed by the International Corporate Governance Network’s (ICGN) Global Stewardship Principles, most recently updated in June 2016. The ICGN Global Stewardship Principles provide a framework to implement stewardship practices in fulfilling an investor’s fiduciary obligations to beneficiaries or clients.

In addition to comprehensive data and information on corporate engagement, proxy voting, and regulatory issues, the complete 2016 report includes four topical sections detailed below:

Governance Patterns in the U.S. Banking Sector—market events this year demonstrate how a company’s governance regime can interact with its reputation and value.

CFOs serving on Boards in the UK—why is the British market so conducive for executives, including the CFO, to serve on their own boards?

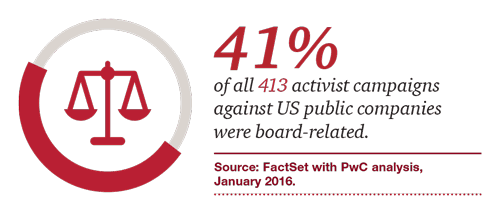

Rule 14a-8 Governing Shareowner Resolutions—is it time for a more efficient way to make shareowner proposals during annual meetings?

UK Compensation Revolt—along with votes targeted at individual board members, investor votes on executive compensation exhibited high levels of dissent at many UK companies.

Annual Voting Review

During the 2016 proxy season, the SBA cast votes at over 10,300 public companies, voting more than 97,000 individual ballot items. The SBA actively engages portfolio companies throughout the year, addressing corporate governance concerns and seeking opportunities to improve alignment with the interests of our beneficiaries. Highlights from the 2016 proxy season included the continued record adoption of proxy access by U.S. companies, record high votes of dissent on pay packages for executives in the United Kingdom, and strong improvements in the level of independence among Japanese boards of directors. While SBA voting principles and guidelines are not pre-disposed to agree or disagree with management recommendations, some management positions may not be in the best interest of all shareowners. On behalf of participants and beneficiaries, the SBA emphasizes the fiduciary responsibility to analyze and evaluate all management recommendations very closely.

Across all voting items, the SBA voted 76.5 percent “For,” 20.2 percent “Against,” 3.1 percent “Withheld,” and 0.2 percent “Abstained” or “Did Not Vote” (due to various local market regulations or liquidity restrictions placed on voted shares). Of all votes cast, 22.2 percent were “Against” the management-recommended-vote (up from 19.4 percent during the same period last year). Among all global proxy votes, the SBA cast at least one dissenting vote at 7,689 annual shareowner meetings, or 74.6 percent of all meetings.

Director Elections

In uncontested director elections among all companies in the United States that are part of the Russell 3000 stock index, over 16,000 nominees received 96.1 percent average support from investors. This year’s figure was within two tenths of one percent from 2015’s statistic. Only 46 director nominees, or less than 0.3 percent, failed to receive a majority level of support from investors. Only two directors at large-capitalization companies within the Standard & Poor’s (S&P) 500 stock index failed to receive a majority level of support. Board elections represent one of the most critical areas in voting because shareowners rely on the board to monitor management. The SBA supported 78.5 percent of individual nominees for boards of directors, voting against the remaining portion of directors due to concerns about candidate independence, qualifications, attendance, or overall board performance. The SBA’s policy is to withhold support from directors who fail to observe good corporate governance practices or demonstrate a disregard for the interests of investors.

Executive Compensation

During the 2016 proxy season, the SBA utilized compensation research from Equilar, Inc., Glass, Lewis & Co., and Institutional Shareholder Services to assist in evaluating the proxy voting decisions on executive compensation share plans and general say-on-pay ballot items. Across all global equity markets, the SBA voted to approve approximately 55 percent of all remuneration reports, whereas in the U.S. market all other investors provided an average support level of 91.5 percent with only 1.5 percent of all advisory votes failing to achieve a majority. ISS found that over half of all U.S. companies conducting annual pay votes have received investor support of at least 90 percent in each of the last five years since the Dodd-Frank Act instituted advisory say-on-pay shareowner votes.

Among all U.S. companies, the average level of investor support for equity plan proposals stayed about the same year over year at approximately 88 percent. However, the number of individual equity plans that failed to garner majority support rose by 50 percent, from 6 to 9 plans. Given the extremely low number of equity plans that fail each year, investor support for individual plans is almost universal. Less than one percent of equity plans failed during the last year, which also marked a five-year low for the number of compensation-related investor proposals with not a single proposal receiving majority support. Over the last fiscal year, the SBA supported 51.2 percent of all non-salary (equity) compensation items, 60.8 percent of executive incentive bonus plans, and 25.2 percent of management proposals to approve omnibus stock plans in which company executives would participate (and 19.3 percent support for the amendment of such plans). Omnibus stock plan ballot items typically include ratification of more than one equity plan beyond a company’s long-term incentive plan (LTIP).

Asset Owner/Asset Manager Peer Benchmarking

In May 2016, the SBA completed an international benchmarking survey on the costs of corporate governance activities at seventeen large public pension funds and global asset managers. The information helped SBA staff to assess the Investment Programs & Governance (IP&G) unit’s cost structure and service utilization across a large number of direct peers. When total research and voting services costs were calculated, SBA had the second lowest dollar-cost per proxy vote among public fund peers and asset managers. The SBA also ranked among the top three funds and well ahead of the fourteen remaining peers with respect to the proxy votes cast per full-time employee. The benchmarking showed that SBA’s corporate governance program uses similar services to peers, but does so at considerably lower cost and with greater efficacy. Our overall program costs and activity levels, particularly when standardized by assets under management, were very favorable compared to peers.

Active Ownership

The SBA actively engages portfolio companies throughout the year, addressing corporate governance concerns and seeking opportunities to improve alignment with the interests of our beneficiaries. During the 2016 fiscal year, SBA staff conducted engagements with over 100 companies owned within Florida Retirement System portfolios, including Compass Group PLC, Microsoft, Coca-Cola, Prudential, Bank of Yokohama, Chevron, Bank of America, ENI, Amgen, Ethan Allen, Oracle, The Goldman Sachs Group, JPMorgan, RTI Surgical, Boeing, Terna Group SpA, Regions Financial Corporation, Red Electrica, and Time Warner. As part of evaluating voting decisions for several proxy contests, SBA staff also met with a number of activist hedge funds, including Red Mountain Capital (proxy campaign at iRobot), Harvest Capital (proxy campaign at Green Dot), and SilverArrow Capital (proxy campaign at Rofin-Sinar Technologies).

Notable Votes

There were numerous significant votes during the 2016 global proxy season, including proxy contests at iRobot Corporation in May and Ashford Hospitality Prime in June, the Facebook share reclassification in June, and the Stada Arzneimitell AG meeting in August. The SBA makes informed and independent voting decisions at investee companies, applying due care, intelligence, and judgment. The SBA makes all proxy voting decisions independently, casting votes based on written, internally-developed corporate governance principles and proxy voting guidelines that cover all expected ballot issues. More detail on each of these votes and the related SBA analysis is contained in the ‘Highlighted Proxy Votes’ section of the 2016 Annual Summary.

The SBA prepares additional reports on corporate governance topics and significant market developments, covering a wide range of shareowner issues. Historical information can be found within the governance section of the SBA’s website. (www.sbafla.com)

The complete publication is available on the SBA’s website here and can also be viewed here using the Issuu e-reader tool.

*Michael McCauley is Senior Officer, Investment Programs & Governance, of the Florida State Board of Administration (the “SBA”). This post is based on an excerpt from the SBA’s 2016 Corporate Governance Report written by Mike McCauley, Jacob Williams, Tracy Stewart, Hugh Brown, and Logan Rand.