Je partage avec vous une excellente prise de position d’Yvan Allaire et de Michel Nadeau, respectivement président et directeur général de l’Institut de la gouvernance (IGOPP), que j’appuie totalement. Cet article a été publié dans Le Devoir du 6 janvier 2018.

Il est impératif que le conseil d’administration, qui est le fiduciaire des parties intéressées, conserve son rôle de gardien de la bonne gouvernance des organisations. Les règles de gouvernance sont fondées sur le fait que le conseil d’administration est l’instance souveraine.

Comme le disent clairement les auteurs : « La gouvernance des sociétés repose sur une pierre angulaire : le conseil d’administration, qui tire sa légitimité et sa crédibilité de son élection par les membres, les actionnaires ou les sociétaires de l’organisation. Il est l’ultime organe décisionnel, l’instance responsable de l’imputabilité et de la reddition de comptes. Tous les comités du conseil créés à des fins spécifiques sont consultatifs pour le conseil ».

Cet article est court et précis ; il met l’accent sur certaines caractéristiques du projet de loi 141 qui mine la légitimité du conseil d’administration et qui sont potentiellement dommageable pour la cohésion et la responsabilisation des membres du conseil.

Je vous en souhaite bonne lecture ; n’hésitez pas à nous faire connaître votre opinion.

Le texte de 488 pages soulèvera de nombreuses questions, notamment chez les intermédiaires financiers lors de la commission parlementaire des 16 et 17 janvier prochains. En tant qu’experts en gouvernance, nous sommes très préoccupés par certains articles du projet de loi qui enlèvent aux conseils d’administration des institutions des pouvoirs qui leur sont reconnus par la loi québécoise et canadienne sur les sociétés par actions. De plus, certaines propositions du projet de loi risquent de semer la confusion quant au devoir de loyauté des membres du conseil envers l’organisation.

La gouvernance des sociétés repose sur une pierre angulaire : le conseil d’administration, qui tire sa légitimité et sa crédibilité de son élection par les membres, les actionnaires ou les sociétaires de l’organisation. Il est l’ultime organe décisionnel, l’instance responsable de l’imputabilité et de la reddition de comptes. Tous les comités du conseil créés à des fins spécifiques sont consultatifs pour le conseil.

Arrangements insoutenables

De façon sans précédent, le projet de loi 141 impose aux conseils d’administration l’obligation de « confier à certains administrateurs qu’il désigne ou à un comité de ceux-ci les responsabilités de veiller au respect des saines pratiques commerciales et des pratiques de gestion saine et prudente et à la détection des situations qui leur sont contraires ».

À quelles informations ce « comité » aurait-il accès, lesquelles ne seraient pas connues d’un comité d’audit normal ? En quoi cette responsabilité dévolue à un nouveau comité est-elle différente de la responsabilité qui devrait incomber au comité d’audit ?

Le projet de loi stipule que dès que le comité prévu prend connaissance d’une situation qui entraîne une détérioration de la situation financière (un fait qui aurait échappé au comité d’audit ?), qui est contraire aux pratiques de gestion saine et prudente ou qui est contraire aux saines pratiques commerciales, il doit en aviser le conseil d’administration par écrit. Le conseil d’administration doit alors voir à remédier promptement à la situation. Si la situation mentionnée à cet avis n’a pas été corrigée selon le jugement de l’administrateur ou du comité, celui-ci doit transmettre à l’Autorité une copie de cet avis.

Le conseil d’administration pourrait, soudainement et sans avoir été prévenu, apprendre que l’AMF frappe à la porte de l’institution parce que certains de leurs membres sont d’avis que le conseil dans son ensemble n’a pas corrigé à leur satisfaction certaines situations jugées inquiétantes.

Ces nouveaux arrangements de gouvernance sont insoutenables. Ils créent une classe d’administrateurs devant agir comme chiens de garde du conseil et comme délateurs des autres membres du conseil. Une telle gouvernance rendrait impossibles la nécessaire collégialité et l’égalité entre les membres d’un même conseil.

Cette forme de gouvernance, inédite et sans précédent, soulève la question fondamentale de la confiance dont doit jouir un conseil quant à sa capacité et à sa volonté de corriger d’éventuelles situations préoccupantes.

Comité d’éthique

Le projet de loi 141 semble présumer qu’un comportement éthique requiert la création d’un comité d’éthique. Ce comité devra veiller à l’adoption de règles de comportement et de déontologie, lesquelles seront transmises à l’AMF. Le comité avise, par écrit et sans délai, le conseil d’administration de tout manquement à celles-ci.

Le projet de loi 141 obligera le comité d’éthique à transmettre annuellement à l’Autorité des marchés un rapport de ses activités, incluant la liste des situations de conflit d’intérêts, les mesures prises pour veiller à l’application des règles et les manquements observés. Le texte de ce projet de loi devrait plutôt se lire ainsi : « Le Comité d’éthique soumet son rapport annuel au conseil d’administration, qui en fait parvenir copie à l’AMF dans les deux mois suivant la clôture de l’exercice. »

Encore une fois, c’est vraiment mal comprendre le travail des comités que d’imputer à ceux-ci des responsabilités « décisionnelles » qui ne devraient relever que du conseil dans son ensemble.

L’ensemble des textes législatifs sur la gouvernance des organisations ne laisse place à aucune ambiguïté : la loyauté d’un membre du conseil est d’abord envers son organisme. Or, le projet de loi instaure un mécanisme de dénonciation auprès de l’AMF. Insatisfait d’une décision de ses collègues ou de leur réaction à une situation donnée, un administrateur devrait ainsi renoncer à son devoir de loyauté et de confidentialité pour choisir la route de la dénonciation en solo.

L’administrateur ne devrait pas se prévaloir de ce régime de dénonciation, mais livrer bataille dans le cadre prévu à cette fin : le conseil. Agir autrement est ouvrir la porte à des manœuvres douteuses qui mineront la cohésion et la solidarité nécessaire au sein de l’équipe du CA. Si la majorité des administrateurs ne partagent pas l’avis de ce valeureux membre, celui-ci pourra démissionner du conseil en informant l’Autorité des motifs de sa démission, comme l’exige le projet de loi 141.

Le projet de loi 141 doit être amendé pour conserver aux conseils d’administration l’entière responsabilité du fonctionnement de la bonne gouvernance des organismes visés par le projet de loi.

Denis Lefort, CPA, expert-conseil en gouvernance, audit et contrôle, porte à ma connaissance un rapport de recherche de l’IIA qui concerne « les indicateurs de mesure de la performance des fonctions d’audit interne ».

Encore aujourd’hui, les indicateurs utilisés sont souvent centrés sur la performance en interne de la fonction et non sur son réel impact sur l’organisation.

Par exemple, peu de services d’audit interne évaluent leur performance par la réduction des cas de fraude dans l’entreprise, par une meilleure gestion des risques, etc.

On utilise plutôt les indicateurs habituels comme le taux de recommandations implantées, la réalisation du plan d’audit, etc.

Voici, ci-dessous, l’introduction au document de l’IIA. Pour consulter le rapport détaillé, cliquez sur le titre du document.

Bonne lecture. Vos commentaires sont les bienvenus

In 2010, The IIA recognized a need to capture a simple, memorable, and straightforward way to help internal auditors convey the value of their efforts to important stakeholders, such as boards of directors, audit committees, management, and clients. To that end, the association introduced the Value Proposition for Internal Auditing, which characterizes internal audit’s value as an amalgam of three elements: assurance, insight, and objectivity.

But identifying the conceptual elements of value is only part of what needs to be done. How does that construct look in the workplace? What activities does internal audit undertake that deliver the most value? What should be measured to determine that the organization’s expectations of value are being met? How does internal audit organize and structure the information that populates the metrics? And, most critically, do the answers to all these questions align; that is, does internal audit’s perception of its value, as measured and tracked, correlate with what the organization wants and needs from the internal audit function? (Exhibit 1)

Exhibit 1

The Internal Audit Value Proposition

1. ASSURANCE = Governance, Risk, Control

Internal audit provides assurance on the organization’s governance, risk management, and control processes to help the organization achieve its strategic, operational, financial, and compliance objectives.

2. INSIGHT = Catalyst, Analyses, Assessments

Internal audit is a catalyst for improving an organization’s effectiveness and efficiency by providing insight and recommendations based on analyses and assessments of data and business process.

With commitment to integrity and accountability, internal audit provides value to governing bodies and senior management as an objective source of independent advice.

These are the kinds of questions the CBOK 2015 global practitioner survey posed to chief audit executives (CAEs) from around the world. The activities these CAEs believe bring value to the organization are consistent with the three elements of The IIA’s value proposition. In fact, the nine activities identified by CAEs as adding the most value can be mapped directly to the three elements, as shown in exibit 2

However, in looking at the performance measures and tools used by the organization and the internal audit function, a gap appears to form between value-adding activities and the ways performance is measured. This report explores that gap in greater detail and clarifies the respondents’ view of value-adding activities, preferred performance measures, and the methodologies and tools most commonly used to support internal audit’s quality and performance processes. Where appropriate, responses tabulated by geographic regions and organization types are examined.

Finally, based on the findings, the final chapter of the report provides a series of practical steps that practitioners at all levels can implement to help their internal audit department deliver on its value proposition of assurance, insight, and objectivity.

Exhibit 2

The Internal Audit Value Proposition (mapped to response options from the CBOK Survey)

ASSURANCE ACTIVITIES

Assuring the adequacy and effectiveness of the internal control system

Assuring the organization’s risk management processes

Voici une recherche de Daniel Taylor qui concerne les informations privées sur le processus d’audit qui peuvent faire l’objet de transactions privées.

Les conclusions sont assez claires à cet égard ; elles suggèrent plusieurs moyens pour se prémunir contre les conséquences indésirables.

The results suggest the audit process provides insiders with a temporary information advantage, and that insiders opportunistically time their trades to exploit this advantage.

La recherche est utile aux chercheurs en gouvernance qui se questionnent sur les transactions équitables pour les actionnaires et pour toutes les parties prenantes.

Également, l’auteur souhaite que les conseils d’administration restreignent les transactions de tous les administrateurs et des personnes impliquées dans le processus d’audit, aussi longtemps que les résultats ne soient pas divulgués publiquement.

Enfin, l’auteur formule certaines recommandations aux autorités de réglementation

Cet article est paru sur le site du Harvard Law School on Corporate Governance.

Bonne lecture !

Our paper examines insider trading in conjunction with the audit process. Audit reports—and the requirement that public companies file audited financial statements—are a cornerstone of modern financial reporting. While it is generally accepted that financial statement audits mitigate agency conflicts, managers and directors (hereafter “corporate insiders”) are typically aware of the contents of the audit report well in advance of the general public. Thus, although a key purpose of financial statement audits is to protect shareholders, an unintended consequence of the audit process is that it endows corporate insiders with a temporary information advantage. In this study, we examine whether corporate insiders exploit this advantage for personal gain and trade based on private information about audit findings.

The audit process represents a negotiation between the external auditor, management, and the board of directors. A typical audit entails planning and interim procedures during the year, year-end fieldwork around the earnings announcement, and culminates with the preparation of the final audit report. Throughout the audit process, the auditor is in frequent contact with management and the board, and provides continuous updates regarding preliminary findings, audit adjustments, and potential modifications to a standard unqualified audit report. The auditor formally briefs the board on the contents of the final report close to the date that the audit is finalized, or “audit report date” (PCAOB AS 1301). Importantly, this date is not known to the public until the audit findings are subsequently disclosed in the firm’s 10-K filing. Thus, by the very nature of the audit process, corporate insiders will be in possession of material non-public information related to audit findings prior to the 10-K filing.

We examine whether corporate insiders trade based on private information about audit findings using a standard short-window event study around the audit report date. The audit report date signifies the end of the audit, and serves as a reasonable proxy for the latest possible date at which corporate insiders are aware of the final audit findings (PCAOB AS 1301, 3110). Our tests focus on a subset of firms where the audit report date occurs after the earnings announcement and more than ten days prior to the 10-K filing. We focus on audit report dates after the earnings announcement in order to cleanly separate insider trading in conjunction with the audit report from insider trading in conjunction with the earnings announcement. We focus on audit report dates more than ten days prior to the 10-K to ensure insiders’ have the opportunity to trade prior to the public disclosure of the audit findings.

By examining insider trading in a tight window around the audit report date, our event study tests mitigate concerns that our results are attributable to either (a) the audit findings themselves being influenced by insider trading, or (b) omitted firm characteristics correlated with the audit findings. Evidence of a change in insider trading activity in a short window around the audit report date—when audit findings are known to insiders but not to the market—suggests insiders are trading based on private information about the contents of the audit report itself.

We find a pronounced spike in insider trading volume around the audit report date, and that audit reports containing a modified opinion trigger intense insider selling. Highlighting the non-public nature of the audit findings on the audit report date, we find no evidence of a capital market reaction on this date. The presence of significant insider trading activity, coupled with the absence of a capital market reaction, confirms that—in our sample—the audit report date represents a significant internal, non-public, information event.

We conduct an extensive battery of sensitivity tests. For example, we repeat our tests focusing exclusively on withinfirm-quarter variation in insider trading. To the extent that an omitted variable does not vary within agiven firm-quarter (e.g., within Firm A’s 2009-Q4), this analysis controls for the omitted variable (e.g., quarterly performance, governance, growth opportunities, audit quality, reporting complexity, etc.). Focusing exclusively on the timing of trades within the firm-quarter, we continue to find that modified audit opinions trigger intense insider selling around the audit report. Although we cannot definitively rule out the possibility of a correlated omitted variable, we view this as highly unlikely—to explain these results, an omitted variable would have to (i) vary with the timing of insider trades within a given firm-quarter, (ii) vary with the timing of the audit report date within the firm-quarter, and (iii) vary with the audit opinion.

Collectively, our results are consistent with corporate insiders trading based on private information about audit findings. The results suggest the audit process provides insiders with a temporary information advantage, and that insiders opportunistically time their trades to exploit this advantage.

Our research question and findings should be of interest to academics, practitioners, and regulators. With respect to academics, our study extends a long line of auditing research. Our results provide novel evidence that corporate insiders exploit features of the audit process for personal gain. In this regard, our findings suggest a more nuanced understanding of the audit process and the extent to which it protects shareholders and mitigates agency conflicts.

With respect to practitioners—specifically boards and legal counsel—our findings underscore the need for meaningful insider trading policies that effectively limit the key personnel to trade prior to the public disclosure of the audit findings. For example, most firms have insider trading policies that restrict trading around the earnings announcement, but nonetheless allow trading in the intervening period between the earnings announcement and the public disclosure of the audit findings (e.g., Jagolinzer, Larcker, and Taylor, 2011). Boards might want to consider restricting the trade of all officers and directors involved with the audit until the audit findings are publicly disclosed.

With respect to regulators, the Securities and Exchange Commission (SEC) and Public Company Audit Oversight Board (PCAOB) are charged with protecting the interests of individual investors. Consequently, empirical evidence on how audits affect insider trading represents an important consideration in ongoing deliberations on auditing standards and auditing procedures. Our evidence highlights a potentially unintended consequence of audit standards aimed at improving the informativeness of audit reports—as the audit report becomes more informative, the incentives for insiders to front-run the report also increase. Our findings are particularly salient in the context of the new auditing standard that takes effect in fiscal 2019 (PCAOB-2017-01) and changes the audit report from a standardized opinion to one that includes detailed engagement-specific disclosures. We encourage auditors, boards, and regulators to scrutinize insider trades placed in conjunction with corporate audits.

Je vous invite à prendre connaissance du futur code de gouvernance du Royaume-Uni (R.-U.).

À cet effet, voici un billet de Martin Lipton*, paru sur le site de Harvard Law School Forum on Corporate Governance, qui présente un aperçu des points saillants.

Bonne lecture !

The Financial Reporting Council today [July 16, 2018] issued a revised corporate governance code and announced that a revised investor stewardship code will be issued before year-end. The code and related materials are available at www.frc.org.uk.

The revised code contains two provisions that will be of great interest. They will undoubtedly be relied upon in efforts to update the various U.S. corporate governance codes. They will also be used to further the efforts to expand the sustainability and stakeholder concerns of U.S. boards.

First, the introduction to the code makes note that shareholder primacy needs to be moderated and that the concept of the “purpose” of the corporation, as long put forth in the U.K. by Colin Mayer and recently popularized in the U.S. by Larry Fink in his 2018 letter to CEO’s, is the guiding principle for the revised code:

Companies do not exist in isolation. Successful and sustainable businesses underpin our economy and society by providing employment and creating prosperity. To succeed in the long-term, directors and the companies they lead need to build and maintain successful relationships with a wide range of stakeholders. These relationships will be successful and enduring if they are based on respect, trust and mutual benefit. Accordingly, a company’s culture should promote integrity and openness, value diversity and be responsive to the views of shareholders and wider stakeholders.

Second, the code provides that the board is responsible for policies and practices which reinforce a healthy culture and that the board should engage:

with the workforce through one, or a combination, of a director appointed from the workforce, a formal workforce advisory panel and a designated non-executive director, or other arrangements which meet the circumstances of the company and the workforce.

It will be interesting to see how this provision will be implemented and whether it gains any traction in the U.S.

Martin Lipton* is a founding partner of Wachtell, Lipton, Rosen & Katz, specializing in mergers and acquisitions and matters affecting corporate policy and strategy. This post is based on a Wachtell Lipton memorandum by Mr. Lipton.

Une bonne relation entre le Président du comité d’Audit et le Vice-président Finance (CFO) est absolument essentielle pour une gestion financière éclairée, fidèle et intègre.

Les auteurs sont liés au Centre for Board Effectiveness de Deloitte. Dans cette publication, parue dans le Wall Street Journal, ils énoncent les sept attentes que les comités d’audit ont envers les chefs des finances.

Cet article sera certainement très utile aux membres de conseils, notamment aux membres des comtés d’audit ainsi qu’à la direction financière de l’entreprise.

Bonne lecture ! Vos commentaires sont les bienvenus.

The evolution of the CFO’s role is effecting a shift in the audit committee’s expectations for the working relationship between the two. By considering their response to seven commonly held expectations audit committees have of CFOs, CFOs can begin to lay the groundwork for a more effective working relationship with their organization’s audit committee.

Typically, CFOs play four key roles within their organizations, but the amount of time CFOs allocate to each role is changing rapidly. “For CFOs high integrity of work, accuracy, and timely financial reporting are table stakes, but increasingly they are being expected to be Strategists and Catalysts in their organization,” says Ajit Kambil, global research director for Deloitte’s CFO Program. “In fact, our research indicates that CFOs are spending about 60% to 70% of their time in those roles, and that shift is both reflecting and driving higher expectations from the CEO as well as the board.”

As in any relationship, a degree of trust between CFOs and audit committee chairs serves as a foundation to an effective communication on critical issues. “In high-functioning relationships between CFOs and audit committee chairs, trust and dialogue are critical. Challenges can occur if a CFO comes to an audit committee meeting unprepared or presents a surprising conclusion to the audit committee without having sought the audit committee chair’s opinion, leaving the audit committee chair without the ability to influence that conclusion,” says Henry Phillips, vice chairman and national managing partner, Center for Board Effectiveness, Deloitte & Touche LLP.

Common Expectations Audit Committee Have of CFOs

Following are seven key expectations audit committees have of CFOs for both new and established CFOs to bear in mind.

(1) No Surprises:

Audit committees do not welcome any surprises. Or, if surprises occur, the audit committee will want to be apprised of the issue very quickly. Surprises may be inevitable, but the audit committee expects CFOs to take precautions against known issues and to manage the avoidable ones and to inform them very early on when something unexpected occurs. In order to do this well, it is important for the CFO and the audit committee chair — perhaps some of the other board members — to set a regular cadence of meetings, so that they have a relationship and a context within which to work together when challenging issues arise. Don’t leave these meetings to chance. “If the audit committee chair or committee members are hearing about something of significance for the first time in a meeting, that’s problematic. Rather, the CFO should be apprising the audit committee chair as much in advance of a committee meeting as possible and talk through the issues so the audit committee chair is not surprised in the meeting,” says Phillips.

(2) Strong partnering with the CEO and other leaders:

Audit committees want to see the CFO as an effective partner with the CEO, as well as with their peer executives. “The audit committee is carefully observing the CFO and how he or she interacts across the C-suite. At the same time, the audit committee also wants the CFO to be objective and to provide to the board independent perspectives on financial and business issues and not be a ‘yes’ person,” says Deb DeHaas, vice chair and national managing partner, Center for Board Effectiveness at Deloitte. A key for the CFO is to proactively manage CEO and peer relations — especially if there are challenging issues that may be brought up to the board. In that case, the CFO should be prepared to take a clear position on what the board needs to hear from management.

(3) Confidence in finance organization talent:

Audit committees want visibility into the finance organization to ensure that it has the appropriate skills and experience. They also are looking to ensure that the finance organization will be stable over time, that there will be solid succession plans in place and that talent is being developed to create the strongest possible finance organization. CFOs might consider approaching these goals in several ways. One way is to provide key finance team members an opportunity to brief the audit committee on a special topic, for example, a significant accounting policy, a special analysis or another topic that’s on the board agenda. “While I encourage CFOs to give their team members an opportunity to present to the committee, it’s critical to make sure they’re well prepared and ready to address questions,” Phillips notes.

‘An outside-in view from audit committee members can bring significant value to the CFO — and to the organization.’

(4) Command of key accounting, finance and business issues:

Audit committees want CFOs to have a strong command of the key accounting issues that might be facing the organization, and given that many CFOs are not CPAs, such command is even more critical for the CFO to demonstrate. Toward that end, steps the CFO can take might include scheduling deep dives with management, the independent auditor, the chief accounting officer and others to receive briefings in order to better understand the organization’s critical issues from an accounting perspective, as well as to get trained up on those issues. In addition, CFOs should demonstrate a deep understanding of the business issues that the organization is confronting. There again, CFOs can leverage both internal and external resources to help them master these issues. Industry briefings are also important, particularly for CFOs who are new to an industry.

(5) Insightful forecasting and earnings guidance:

Forecasts and earnings guidance will likely not always be precise. However, audit committees expect CFOs to not only deliver reliable forecasts, but also to articulate the underlying drivers of the company’s future performance, as well as how those drivers might impact outcomes. When CFOs lack a thorough understanding of critical assumptions and drivers, they can begin to lose support of key audit committee members. For that reason, it is important that CFOs have an experienced FP&A group to support them. In addition,audit committees and boards want to deeply understand the guidance that is being put forward, the ranges, and confidence levels. As audit committee members read earnings releases and other information in the public domain, they tend to focus on whether the information merely meets the letter of the law in terms of disclosures, or does it tell investors what they need to know to make informed decisions. This is where an outside-in view from audit committee members can bring significant value to the CFO — and to the organization. Moreover, audit committees are increasingly interested in the broader macroeconomic issues that can impact the organization, such as interest rates, oil prices, and geographic instability.

(6) Effective risk management:

CFOs are increasingly held accountable for risk management, even when there is a chief risk officer. Further, audit committees want CFOs to provide leadership not only on traditional financial accounting and compliance risk matters, but also on some of the enterprise operational macro-risk issues — and to show how that might impact the financial statement. It is important for CFOs to set the tone at the top for compliance and ethics, oversee the control environment and ensure that from a compensation perspective, the appropriate incentives and structures are in place to mitigate risk. A key to the CFO’s effectiveness at this level is to find time to have strategic risk conversations at the highest level of management, as well as with the board.

(7) Clear and concise stakeholder communications:

Audit committees want CFOs to be very effective on how they communicate with key stakeholders, which extend beyond the board and the audit committees. They want CFOs to be able to articulate the story behind the numbers and provide insights and future trends around the business, and to effectively communicate to the Street. CFOs can expect board members to listen to earnings calls and to observe how they interact with the CEOs, demonstrate mastery of the company’s financial and business issues, and communicate those to the Street. Moreover, a CFO who is very capable from an accounting and finance perspective should exercise the communication skills that are necessary to be effective with different stakeholders.

“Communication is the cornerstone for a strong CFO-audit committee chair relationship,” notes DeHaas. “Although the CFO might be doing other things very well, if there is not effective communication and a trusting relationship with the audit committee, the CFO will likely not be as effective.”

Voici un article-choc publié par Chris Hughes dans la revue Bloomberg qui porte sur l’indépendance (ou le manque d’indépendance) des quatre grandes firmes d’audit dans le monde.

Il y a une sérieuse polémique eu égard à l’indépendance réelle des grandes firmes d’audit.

Cet article donne les grandes lignes de la problématique et il esquisse des avenues de solution.

Shareholders need to be the client, not company executives.

L’une des quatre grandes firmes

British lawmakers are pushing for a full-blown antitrust probe into the country’s four big accountancy firms following the demise of U.K. construction group Carillion Plc.

The current domination of KPMG, PricewaterhouseCoopers, EY and Deloitte isn’t working for shareholders. But creating more competition among the bean counters won’t be enough on its own. The fundamental problem is who the client is. The thrust of reform should be on making auditors see that their client is the investor and not the company executive. Randgold Resources is the only FTSE 100 company not to be audited by one of the Big Four !

Carillion’s accounts weren’t completely useless. Recent annual reports contained red flags of the company’s deteriorating financial health that were apparent to the smart money. Some long funds cut their holdings and hedge funds took large short positions, as my colleague Chris Bryant points out.

If the evidence was there to those who looked hard, it’s odd that the company was given a clean bill of health from accountancy firm KPMG months before it went bust. The impression is that auditors are on the side of the company rather than the shareholder. (KPMG says it believes it conducted its audit appropriately.)

Would more competition have made a difference? Companies may have only one accountant available if the few competing firms are already working for a rival. A lack of choice in any market usually leads to lower quality.

One response would be to force the Big Four to shed clients to mid-tier firms, creating a Big Five or Big Six. The risk is this greater competition just leads to a race to the bottom on fees with no improvement in quality. Other remedies are needed first.

The combination of audit and more lucrative consultancy work has long been chided – with good reason. Consultancy creates a client-pleasing culture. That’s at odds with the auditor’s role in challenging the assumptions behind company statements.

Opponents of a separation say combining the two services helps attract talent. This is a weak argument. Further lowering the current cap on consultancy fees, or completely separating audit and consultancy, is hard to argue with.

The accountancy firm should clearly serve the non-executive directors on the company’s audit committee which, in turn, is charged with looking out for shareholders. The risk is that the auditor’s main point of contact is the executive in the form of the chief financial officer.

Shareholders already have a vote on the appointment of the auditor. But annual reports could provide more useful disclosure on the frequency and depth of the last year’s contact between the firm and the audit committee, and between the latter and shareholders.

Now consider the nature of the job itself. Companies present the accounts, auditors check them. Out pops a financial statement that gives the false impression of extreme precision. Numbers that are the based on assumptions might be better presented as a range, accompanied by a critique of the judgments applied by the company.

Creating more big audit firms may create upward pressure on quality. But so long as they aren’t incentivized to have shareholders front of mind, it won’t be a long wait for the next Carillion.

Le récent rapport de KPMG sur les grandes tendances en audit présente sept défis que les membres des CA, notamment les membres des comités d’audit, doivent considérer afin de bien s’acquitter de leurs responsabilités dans la gouvernance des sociétés.

Le rapport a été rédigé par des professionnels en audit de la firme KPMG ainsi que par le Conference Board du Canada.

Les sept défis abordés dans le rapport sont les suivants :

– talent et capital humain ;

– technologie et cybersécurité ;

– perturbation des modèles d’affaires ;

– paysage réglementaire en évolution ;

– incertitude politique et économique ;

– évolution des attentes en matière de présentation de l’information ;

– environnement et changements climatiques.

Je vous invite à consulter le rapport complet ci-dessous pour de plus amples informations sur chaque enjeu.

Alors que l’innovation technologique et la cybersécurité continuent d’avoir un impact croissant sur le monde des finances et des affaires à l’échelle mondiale, tant les comités d’audit que les chefs des finances reconnaissent le besoin de compter sur des talents de haut calibre pour contribuer à affronter ces défis et à en tirer parti.

Le rôle du comité d’audit est de s’assurer que l’organisation dispose des bonnes personnes possédant l’expérience et les connaissances requises, tant au niveau de la gestion et des opérations qu’au sein même de sa constitution. Il ne s’agit que de l’un des nombreux défis à avoir fait surface dans le cadre de ce troisième numéro du rapport Tendances en audit.

Les comités d’audit d’aujourd’hui ont la responsabilité d’aider les organisations à s’orienter parmi les nombreux enjeux et défis plus complexes que jamais auxquels ils font face, tout en remplissant leur mandat traditionnel de conformité et de présentation de l’information. Alors que les comités d’audit sont pleinement conscients de cette nécessité, notre rapport indique que les comités d’audit et les chefs des finances se demandent dans quelle mesure leur organisation est bien positionnée pour faire face à la gamme complète des tendances actuelles et émergentes.

Pour mettre en lumière cette préoccupation et d’autres enjeux clés, le rapport Tendances en audit se penche sur les sept défis qui suivent :

talent et capital humain;

technologie et cybersécurité;

perturbation des modèles d’affaires;

paysage réglementaire en évolution;

incertitude politique et économique;

évolution des attentes en matière de présentation de l’information;

environnement et changements climatiques.

Au fil de l’évolution des mandats et des responsabilités, ce rapport se révélera être une ressource précieuse pour l’ensemble des parties prenantes en audit.

Je partage avec vous une excellente prise de position d’Yvan Allaire et de Michel Nadeau, respectivement président et directeur général de l’Institut de la gouvernance (IGOPP), que j’appuie totalement. Cet article a été publié dans Le Devoir du 6 janvier 2018.

Il est impératif que le conseil d’administration, qui est le fiduciaire des parties intéressées, conserve son rôle de gardien de la bonne gouvernance des organisations. Les règles de gouvernance sont fondées sur le fait que le conseil d’administration est l’instance souveraine.

Comme le disent clairement les auteurs : « La gouvernance des sociétés repose sur une pierre angulaire : le conseil d’administration, qui tire sa légitimité et sa crédibilité de son élection par les membres, les actionnaires ou les sociétaires de l’organisation. Il est l’ultime organe décisionnel, l’instance responsable de l’imputabilité et de la reddition de comptes. Tous les comités du conseil créés à des fins spécifiques sont consultatifs pour le conseil ».

Cet article est court et précis ; il met l’accent sur certaines caractéristiques du projet de loi 141 qui mine la légitimité du conseil d’administration et qui sont potentiellement dommageable pour la cohésion et la responsabilisation des membres du conseil.

Je vous en souhaite bonne lecture ; n’hésitez pas à nous faire connaître votre opinion.

Le texte de 488 pages soulèvera de nombreuses questions, notamment chez les intermédiaires financiers lors de la commission parlementaire des 16 et 17 janvier prochains. En tant qu’experts en gouvernance, nous sommes très préoccupés par certains articles du projet de loi qui enlèvent aux conseils d’administration des institutions des pouvoirs qui leur sont reconnus par la loi québécoise et canadienne sur les sociétés par actions. De plus, certaines propositions du projet de loi risquent de semer la confusion quant au devoir de loyauté des membres du conseil envers l’organisation.

La gouvernance des sociétés repose sur une pierre angulaire : le conseil d’administration, qui tire sa légitimité et sa crédibilité de son élection par les membres, les actionnaires ou les sociétaires de l’organisation. Il est l’ultime organe décisionnel, l’instance responsable de l’imputabilité et de la reddition de comptes. Tous les comités du conseil créés à des fins spécifiques sont consultatifs pour le conseil.

Arrangements insoutenables

De façon sans précédent, le projet de loi 141 impose aux conseils d’administration l’obligation de « confier à certains administrateurs qu’il désigne ou à un comité de ceux-ci les responsabilités de veiller au respect des saines pratiques commerciales et des pratiques de gestion saine et prudente et à la détection des situations qui leur sont contraires ».

À quelles informations ce « comité » aurait-il accès, lesquelles ne seraient pas connues d’un comité d’audit normal ? En quoi cette responsabilité dévolue à un nouveau comité est-elle différente de la responsabilité qui devrait incomber au comité d’audit ?

Le projet de loi stipule que dès que le comité prévu prend connaissance d’une situation qui entraîne une détérioration de la situation financière (un fait qui aurait échappé au comité d’audit ?), qui est contraire aux pratiques de gestion saine et prudente ou qui est contraire aux saines pratiques commerciales, il doit en aviser le conseil d’administration par écrit. Le conseil d’administration doit alors voir à remédier promptement à la situation. Si la situation mentionnée à cet avis n’a pas été corrigée selon le jugement de l’administrateur ou du comité, celui-ci doit transmettre à l’Autorité une copie de cet avis.

Le conseil d’administration pourrait, soudainement et sans avoir été prévenu, apprendre que l’AMF frappe à la porte de l’institution parce que certains de leurs membres sont d’avis que le conseil dans son ensemble n’a pas corrigé à leur satisfaction certaines situations jugées inquiétantes.

Ces nouveaux arrangements de gouvernance sont insoutenables. Ils créent une classe d’administrateurs devant agir comme chiens de garde du conseil et comme délateurs des autres membres du conseil. Une telle gouvernance rendrait impossibles la nécessaire collégialité et l’égalité entre les membres d’un même conseil.

Cette forme de gouvernance, inédite et sans précédent, soulève la question fondamentale de la confiance dont doit jouir un conseil quant à sa capacité et à sa volonté de corriger d’éventuelles situations préoccupantes.

Comité d’éthique

Le projet de loi 141 semble présumer qu’un comportement éthique requiert la création d’un comité d’éthique. Ce comité devra veiller à l’adoption de règles de comportement et de déontologie, lesquelles seront transmises à l’AMF. Le comité avise, par écrit et sans délai, le conseil d’administration de tout manquement à celles-ci.

Le projet de loi 141 obligera le comité d’éthique à transmettre annuellement à l’Autorité des marchés un rapport de ses activités, incluant la liste des situations de conflit d’intérêts, les mesures prises pour veiller à l’application des règles et les manquements observés. Le texte de ce projet de loi devrait plutôt se lire ainsi : « Le Comité d’éthique soumet son rapport annuel au conseil d’administration, qui en fait parvenir copie à l’AMF dans les deux mois suivant la clôture de l’exercice. »

Encore une fois, c’est vraiment mal comprendre le travail des comités que d’imputer à ceux-ci des responsabilités « décisionnelles » qui ne devraient relever que du conseil dans son ensemble.

L’ensemble des textes législatifs sur la gouvernance des organisations ne laisse place à aucune ambiguïté : la loyauté d’un membre du conseil est d’abord envers son organisme. Or, le projet de loi instaure un mécanisme de dénonciation auprès de l’AMF. Insatisfait d’une décision de ses collègues ou de leur réaction à une situation donnée, un administrateur devrait ainsi renoncer à son devoir de loyauté et de confidentialité pour choisir la route de la dénonciation en solo.

L’administrateur ne devrait pas se prévaloir de ce régime de dénonciation, mais livrer bataille dans le cadre prévu à cette fin : le conseil. Agir autrement est ouvrir la porte à des manœuvres douteuses qui mineront la cohésion et la solidarité nécessaire au sein de l’équipe du CA. Si la majorité des administrateurs ne partagent pas l’avis de ce valeureux membre, celui-ci pourra démissionner du conseil en informant l’Autorité des motifs de sa démission, comme l’exige le projet de loi 141.

Le projet de loi 141 doit être amendé pour conserver aux conseils d’administration l’entière responsabilité du fonctionnement de la bonne gouvernance des organismes visés par le projet de loi.

Denis Lefort, CPA, expert-conseil en gouvernance, audit et contrôle, porte à ma connaissance un rapport de recherche de l’IIA qui concerne « les indicateurs de mesure de la performance des fonctions d’audit interne ».

Encore aujourd’hui, les indicateurs utilisés sont souvent centrés sur la performance en interne de la fonction et non sur son réel impact sur l’organisation.

Par exemple, peu de services d’audit interne évaluent leur performance par la réduction des cas de fraude dans l’entreprise, par une meilleure gestion des risques, etc.

On utilise plutôt les indicateurs habituels comme le taux de recommandations implantées, la réalisation du plan d’audit, etc.

Voici, ci-dessous, l’introduction au document de l’IIA. Pour consulter le rapport détaillé, cliquez sur le titre du document.

Bonne lecture. Vos commentaires sont les bienvenus

In 2010, The IIA recognized a need to capture a simple, memorable, and straightforward way to help internal auditors convey the value of their efforts to important stakeholders, such as boards of directors, audit committees, management, and clients. To that end, the association introduced the Value Proposition for Internal Auditing, which characterizes internal audit’s value as an amalgam of three elements: assurance, insight, and objectivity.

But identifying the conceptual elements of value is only part of what needs to be done. How does that construct look in the workplace? What activities does internal audit undertake that deliver the most value? What should be measured to determine that the organization’s expectations of value are being met? How does internal audit organize and structure the information that populates the metrics? And, most critically, do the answers to all these questions align; that is, does internal audit’s perception of its value, as measured and tracked, correlate with what the organization wants and needs from the internal audit function? (Exhibit 1)

Exhibit 1

The Internal Audit Value Proposition

1. ASSURANCE = Governance, Risk, Control

Internal audit provides assurance on the organization’s governance, risk management, and control processes to help the organization achieve its strategic, operational, financial, and compliance objectives.

2. INSIGHT = Catalyst, Analyses, Assessments

Internal audit is a catalyst for improving an organization’s effectiveness and efficiency by providing insight and recommendations based on analyses and assessments of data and business process.

With commitment to integrity and accountability, internal audit provides value to governing bodies and senior management as an objective source of independent advice.

These are the kinds of questions the CBOK 2015 global practitioner survey posed to chief audit executives (CAEs) from around the world. The activities these CAEs believe bring value to the organization are consistent with the three elements of The IIA’s value proposition. In fact, the nine activities identified by CAEs as adding the most value can be mapped directly to the three elements, as shown in exibit 2

However, in looking at the performance measures and tools used by the organization and the internal audit function, a gap appears to form between value-adding activities and the ways performance is measured. This report explores that gap in greater detail and clarifies the respondents’ view of value-adding activities, preferred performance measures, and the methodologies and tools most commonly used to support internal audit’s quality and performance processes. Where appropriate, responses tabulated by geographic regions and organization types are examined.

Finally, based on the findings, the final chapter of the report provides a series of practical steps that practitioners at all levels can implement to help their internal audit department deliver on its value proposition of assurance, insight, and objectivity.

Exhibit 2

The Internal Audit Value Proposition (mapped to response options from the CBOK Survey)

ASSURANCE ACTIVITIES

Assuring the adequacy and effectiveness of the internal control system

Assuring the organization’s risk management processes

Quels sont les bénéfices d’une solide culture organisationnelle ?

C’est précisément la question abordée par William C. Dudley,président et CEO de la Federal Reserve Bank de New York, dans une allocution présentée à la Banking Standards Board de Londres.

Dans sa présentation, il évoque trois éléments fondamentaux pour l’amélioration de la culture organisationnelle des entreprises du secteur financier :

Définir la raison d’être et énoncer des objectifs clairs puisque ceux-ci sont nécessaires à l’évaluation de la performance ;

Mesurer la performance de la firme et la comparer aux autres du même secteur ;

S’assurer que les mesures incitatives mènent à des comportements en lien avec les buts que l’organisation veut atteindre.

Selon M. Dudley, il y a plusieurs avantages à intégrer des pratiques de bonne culture dans la gestion de l’entreprise. Il présente clairement les nombreux bénéfices à retirer lorsque l’organisation a une saine culture.

Vous trouverez, ci-dessous, les principales raisons pour lesquelles il est important de se soucier de cette dimension à long terme. Je n’avais encore jamais vu ces raisons énoncées aussi explicitement dans un texte.

L’article a paru aujourd’hui sur le site de la Harvard Law School Forum on Corporate Governance.

I am convinced that a good or ethical culture that is reflected in your firm’s strategy, decision-making processes, and products is also in your economic best interest, for a number of reasons:

Good culture means fewer incidents of misconduct, which leads to lower internal monitoring costs.

Good culture means that employees speak up so that problems get early attention and tend to stay small. Smaller problems lead to less reputational harm and damage to franchise value. And, habits of speaking up lead to better exchanges of ideas—a hallmark of successful organizations.

Good culture means greater credibility with prosecutors and regulators—and fewer and lower fines.

Good culture helps to attract and retain good talent. This creates a virtuous circle of higher performance and greater innovation, and less pressure to cut ethical corners to generate the returns necessary to stay in business.

Good culture builds a strong organizational story that is a source of pride and that can be passed along through generations of employees. It is also attractive to clients.

Good culture helps to rebuild public trust in finance, which could, in turn, lead to a lower burden imposed by regulation over time. Regulation and compliance are expensive substitutes for good stewardship.

Good culture is, in short, a necessary condition for the long-term success of individual firms. Therefore, members of the industry must be good stewards and should seek to make progress on reforming culture in the near term.

Voici un excellent résumé des caractéristiques de la nouvelle cuvée d’administrateurs indépendants en 2016.

Cet article, publié sur le site de Harvard Law School Forum, est basé sur une publication du EY Center for Board Matters.

La recherche porte sur les nouveaux administrateurs recensés dans le Fortune 100.

L’article présente les 10 expertises les plus recherchées, les caractéristiques de la diversité, l’expérience antérieure des nouveaux administrateurs, la distribution des âges et l’appartenance à l’un ou l’autre des trois principaux comités du CA.

J’aimerais connaître vos réactions en réponse à cette recherche d’Ernst Young (EY).

Croyez-vous que cette étude américaine peut se transposer à la situation des conseils d’administration au Canada ?

Today’s boards are navigating disruptive changes, a dynamic geopolitical and regulatory environment, shifting consumer and workforce demographics, and shareholder activist activity amid a push by leading investors for a more long-term strategic focus. These demands highlight the critical role boards play in helping companies manage risk and seize strategic opportunities.

To see how boards are keeping current and strategically aligning board composition to company needs, we reviewed the qualifications and characteristics of independent directors who were elected to Fortune 100 boards for the first time in 2016 (Fortune 100 Class of 2016). We also looked at some of the same data for the Russell 3000, and we highlight those findings at the end of this post.

This post highlights five key findings about the Fortune 100 Class of 2016; but first it’s worth noting that nearly 60% of Fortune 100 companies added at least one independent director following the company’s 2015 annual meeting. These boards added an average of 1.8 directors—and close to one-fifth of these boards added three or more directors.

The Fortune 100 Class of 2016 brings a wide range of strengths into the boardroom

Based on the qualifications highlighted in corporate disclosures, expertise in corporate finance or accounting was most frequently cited. More than half of directors assigned to the audit committee were recognized as financial experts. Companies also highlighted leadership positions in multinational corporations, managing global operations or detailed knowledge of certain markets of particular interest to company strategy. Board experience (public or private) or corporate governance expertise also was commonly cited.

Top 10 skills and expertise of Fortune 100 Class of 2016

The Fortune 100 Class of 2016 enhances gender diversity

Nearly 40% of the Fortune 100 Class of 2016 are women, compared to less than a quarter of incumbents and less than one-fifth of the exiting directors. Newly appointed women directors also are slightly younger than male counterparts (57 compared to 59).

Distribution of Fortune 100 female directorships

Only about half of the Fortune 100 Class of 2016 are current or former CEOs

While experience as a CEO is often cited as a historical first cut for search firms, about half of the Fortune 100 class of 2016 have non-CEO backgrounds as corporate executives or have non-corporate backgrounds (e.g., scientists, academics and former government officials). Ten percent worked at an institutional investor, an experience which was highlighted to communicate the company’s interest in shareholder perspectives. Another 9% were described as bringing experience in innovation or having the capability to drive innovation. It’s also notable that 17% of the entering class appear to be joining a public company board for the first time.

Fortune 100 Class of 2016 director backgrounds (% of directors)

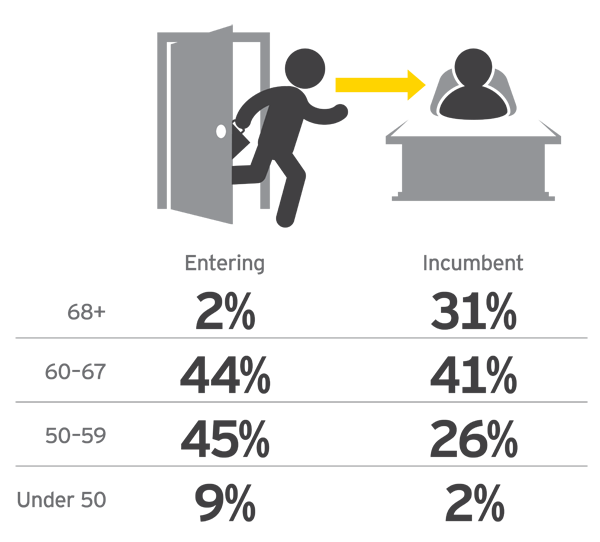

The Fortune 100 Class of 2016 tends to be younger than their director counterparts

The average age of entering directors was 58, compared to 64 for incumbents and 68 for the exiting group. Although most directors are between 50 and 67, nearly 10% of the entering class was under 50 compared to 1% of incumbent directors. Over half of exiting directors were age 68 or older.

Distribution of Fortune 100 directorships by age

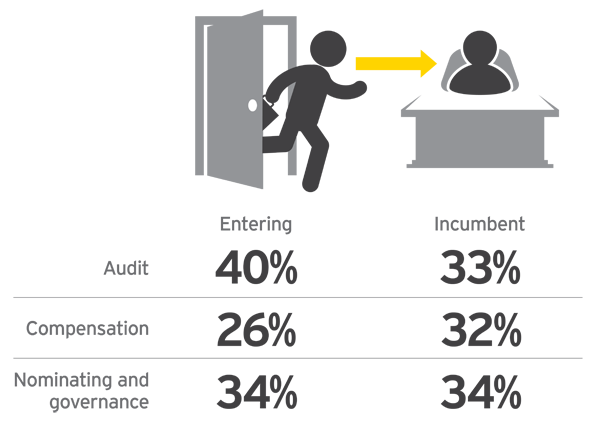

Members of the Fortune 100 Class of 2016 are mainly being added to audit committees

Entering directors are more likely to join the audit committee during their first year on the board. While the committee service of incumbent directors appears to be fairly evenly distributed, the exiting group was most likely to hold positions on the nominating and governance committees.

Distribution of Fortune 100 key committee membership

How does the Russell 3000 Class of 2016 compare?

Significantly fewer Russell 3000 companies added at least one independent director following the company’s 2015 annual meeting, and those that did added fewer independent directors. The Russell 3000 Class of 2016 independent directors tend to be slightly younger than the Fortune 100 Class of 2016, and when it comes to key committee membership, they’re also most likely to join the audit committee in their first year on the board. Just around a quarter is female, however, showing that smaller company boards have a steeper climb ahead to achieve gender parity.

Questions for the nominating and governance committee to consider

How current and relevant are the skills of incumbent directors to the company’s long-term strategy?

Given increasing attention to director qualifications, including by shareholder activists, do existing company disclosures effectively communicate the strengths of incumbent directors?

How diverse is the board—defined as including considerations such as age, gender, race, ethnicity, nationality—in addition to skills and expertise?

How can the board’s existing succession planning efforts and approach to considering director candidates be enhanced?

Quels sont les bénéfices d’une solide culture organisationnelle ?

C’est précisément la question abordée par William C. Dudley,président et CEO de la Federal Reserve Bank de New York, dans une allocution présentée à la Banking Standards Board de Londres.

Dans sa présentation, il évoque trois éléments fondamentaux pour l’amélioration de la culture organisationnelle des entreprises du secteur financier :

Définir la raison d’être et énoncer des objectifs clairs puisque ceux-ci sont nécessaires à l’évaluation de la performance ;

Mesurer la performance de la firme et la comparer aux autres du même secteur ;

S’assurer que les mesures incitatives mènent à des comportements en lien avec les buts que l’organisation veut atteindre.

Selon M. Dudley, il y a plusieurs avantages à intégrer des pratiques de bonne culture dans la gestion de l’entreprise. Il présente clairement les nombreux bénéfices à retirer lorsque l’organisation a une saine culture.

Vous trouverez, ci-dessous, les principales raisons pour lesquelles il est important de se soucier de cette dimension à long terme. Je n’avais encore jamais vu ces raisons énoncées aussi explicitement dans un texte.

L’article a paru aujourd’hui sur le site de la Harvard Law School Forum on Corporate Governance.

I am convinced that a good or ethical culture that is reflected in your firm’s strategy, decision-making processes, and products is also in your economic best interest, for a number of reasons:

Good culture means fewer incidents of misconduct, which leads to lower internal monitoring costs.

Good culture means that employees speak up so that problems get early attention and tend to stay small. Smaller problems lead to less reputational harm and damage to franchise value. And, habits of speaking up lead to better exchanges of ideas—a hallmark of successful organizations.

Good culture means greater credibility with prosecutors and regulators—and fewer and lower fines.

Good culture helps to attract and retain good talent. This creates a virtuous circle of higher performance and greater innovation, and less pressure to cut ethical corners to generate the returns necessary to stay in business.

Good culture builds a strong organizational story that is a source of pride and that can be passed along through generations of employees. It is also attractive to clients.

Good culture helps to rebuild public trust in finance, which could, in turn, lead to a lower burden imposed by regulation over time. Regulation and compliance are expensive substitutes for good stewardship.

Good culture is, in short, a necessary condition for the long-term success of individual firms. Therefore, members of the industry must be good stewards and should seek to make progress on reforming culture in the near term.

Nous publions ici un billet de Danielle Malboeuf* qui fait état des recommandations du vérificateur général eu égard à la gouvernance des CÉGEP.

Comme à l’habitude Danielle nous propose son article à titre d’auteure invitée.

Je vous souhaite bonne lecture. Vos commentaires sont appréciés.

La gouvernance des Cégeps et le rapport du Vérificateur général du Québec

par

Danielle Malboeuf*

À l’automne 2016, le Vérificateur général du Québec produisait un rapport d’audit concernant la gestion administrative de cinq cégeps. Ses travaux ont porté plus précisément sur la gestion des contrats, la gestion des bâtiments, les services autofinancés ainsi que sur la rémunération du personnel d’encadrement et les frais engagés par celui-ci.

Parmi les recommandations formulées à l’endroit des cégeps audités, on en retrouve une qui concerne plus précisément la gouvernance : « S’assurer que les instances de gouvernance reçoivent une information suffisante et en temps opportun afin qu’elles puissent exercer leur rôle quant aux décisions stratégiques et à la surveillance de l’efficacité des contrôles…»[1]

À la lecture de ce rapport et des constats de ces travaux d’audit, on ne peut qu’être qu’en accord avec cette recommandation qui invite les administrateurs à exercer leur rôle. Mais justement, quel rôle ont-ils ? Du point de vue légal, la Loi sur les collèges d’enseignement général et professionnel est peu éclairante à ce sujet. Contrairement à la Loi sur la gouvernance des sociétés d’État qui précise clairement les fonctions qui sont confiées au conseil d’administration (CA), dont l’obligation d’évaluer l’intégrité des contrôles internes. On y exige également la création de trois sous-comités dont le comité de vérification ou d’audit à qui on confie entre autres, la responsabilité de mettre en place des mécanismes de contrôle interne. De plus, ce sous-comité doit compter sur la présence d’au moins une personne ayant une compétence en matière comptable ou financière.

À mon avis, la gouvernance d’un cégep devrait s’apparenter à celle des sociétés d’État. À ce sujet, dans son rapport publié en mai 2011 soumettant un bilan de l’implantation de la Loi sur la gouvernance des sociétés d’État, l’auteur de ce rapport, l’Institut sur la gouvernance des organismes publics et privés (IGOPP) allait dans le même sens. Il formulait comme première recommandation : « Imposer les nouvelles règles de gouvernance aux nombreux organismes du gouvernement qui ne sont pas inclus dans la loi actuelle sur la gouvernance. »[2]

Malgré le fait que les cégeps n’ont pas l’obligation légale de créer un comité d’audit, plusieurs l’ont fait dans un souci de transparence et afin d’être soutenu par les administrateurs dans leur effort pour assurer une utilisation optimale des ressources financières de l’organisation. Toutefois, le mandat qui leur est confié se limite dans la majorité des cas à une analyse des prévisions budgétaires et des états financiers. Ce n’est pas suffisant !

Considérant la recommandation du vérificateur général, il serait tout à fait approprié d’élargir ce mandat. En plus d’examiner les états financiers et d’en recommander leur approbation au CA, le comité d’audit devrait entre autres, veiller à ce que des mécanismes de contrôle interne soient mis en place et de s’assurer qu’ils soient adéquats et efficaces ainsi que de s’assurer que soit mis en place un processus de gestion des risques.[3]Sachant que les cégeps ne comptent pas de vérificateur interne, il est d’autant plus important de mettre en place un tel comité et de lui confier des fonctions de contrôle financier et de gestion des risques.

Une fois le comité d’audit mis en place, il devrait se pencher prioritairement sur la surveillance du processus de gestion contractuelle. Rappelons que les étapes du processus de gestion contractuelle sont : l’établissement des besoins et l’estimation des coûts, la préparation de l’appel d’offres et la sollicitation des fournisseurs, la sélection du fournisseur et l’attribution du contrat, le suivi du contrat et l’évaluation des biens et des services reçus[4].

À ce sujet, le Vérificateur général, dans son rapport, nous fait part de ses préoccupations. Il a identifié des lacunes dans les modes de sollicitation et constaté des dépassements de coûts et des prolongations dans les délais d’exécution, et ce, sans pénalité. Il précise que «Des activités prévues dans le processus de gestion contractuelle des cégeps audités ne sont pas effectuées de façon rigoureuse.»[5] En jouant son rôle, le comité d’audit du CA pourrait s’assurer que le processus mis en place et le partage des responsabilités retenu sont adéquats et efficaces. Il ne devrait d’ailleurs pas hésiter à faire appel à des ressources externes pour évaluer la performance du Cégep à l’égard de sa gestion contractuelle, le cas échéant.

En terminant, rappelons l’importance de retrouver sur le comité d’audit des administrateurs compétents qui ont une connaissance approfondie de la structure, des politiques, directives et exigences réglementaires. Ils doivent avoir la capacité d’assurer l’efficacité des mécanismes de contrôle interne et de la gestion des risques (un sujet que je développerai dans un article ultérieur).

En présence de telles compétences, il sera plus facile d’assurer la crédibilité du CA et de ses décisions. Il s’agit d’un atout précieux pour toutes institutions collégiales.

_____________________________________

[1] Rapport du Vérificateur général du Québec à l’Assemblée nationale pour l’année 2016-2017, p.35.

[2] Gouvernance des sociétés d’État, bilan et suggestions, IGOPP, p.48.

[3]Loi sur la gouvernance des sociétés d’État, art 24, 3.

[4] Rapport du Vérificateur général du Québec à l’Assemblée nationale pour l’année 2016-2017, annexe 4.

[5] Rapport du Vérificateur général du Québec à l’Assemblée nationale pour l’année 2016-2017, p.9.

_____________________________________

*Danielle Malboeuf est consultante et formatrice en gouvernance ; elle possède une grande expérience dans la gestion des CÉGEPS et dans la gouvernance des institutions d’enseignement collégial et universitaire. Elle est CGA-CPA, MBA, ASC, Gestionnaire et administratrice retraitée du réseau collégial et consultante.

Articles sur la gouvernance des CÉGEPS publiés sur mon blogue par l’auteure :

Voici un cas de gouvernance, publié en décembre sur le site de Julie Garland McLellan* qui illustre comment la direction d’une société publique peut se retrouver en situation d’irrégularité malgré une culture du conseil d’administration axée sur la conformité.

L’investigation du vérificateur général (VG) a révélé plusieurs failles dans les procédures internes de la société. De ce fait, Kyle le président du comité d’audit, risque et conformité, est interpellé par le président du conseil afin d’aider la direction à trouver des solutions durables pour remédier à la situation.

Même si Kyle est conscient qu’il ne possède pas l’autorité requise pour régler les problèmes constatés par le VG, il comprend qu’il est impératif que son message passe.

Le cas présente la situation de manière assez succincte, mais explicite ; puis, trois experts en gouvernance se prononcent sur le dilemme qui se présente aux personnes qui vivent des situations similaires.

Bonne lecture ! Vos commentaires sont toujours les bienvenus.

Kyle is chairman on the Audit, Risk and Compliance committee of a government authority board which is subject to a Public Access to Information Act. The auditor general has just completed an audit of several authorities bound by that Act and Kyle’s authority was found to have several breeches of the Act, in particular;

– some contracts valued at $150,000 or more were not recorded in the contracts register

– some contracts were not entered into the register within 45 working days of the contracts becoming effective

– there were instances where inaccurate information was recorded in the register when compared with the contracts, and

– additional information required for certain classes of contracts was not disclosed in some registers.

The Board Chairman is rightly concerned that this has happened in what all directors believed to be a well governed authority with a strong culture of compliance. The Board Chairman has asked Kyle to oversee management’s response to the Auditor General and the development of systems to ensure that these breeches do not reoccur. Kyle is mindful that he remains a non-executive and has no authority within the chain of management command. He is keen to help and knows that the CEO is struggling with the complexity of her role and will need assistance with any increase in workload.

How can Kyle help without getting embroiled in management affairs?

Raz’s Answer

The issue I spot here, is one which I’ve encountered myself – as a seasoned professional, you have the internal urge to roll your sleeves and get right into it, and solve the problem. From the details disclosed in this dilemma, there’s evidence that the authority’s internal culture is compliant, therefore it’s hard to believe there’s foul play which caused these discrepancies in the reports. I would have guessed that there are some legacy processes, or even old technology, which needs to be looked at and discover where the gap is.

The CEO is under immense pressure to fix this issue, being exposed to public scrutiny, but with the government’s limited resources at her disposal, the pressure is even higher. Making decisions under such pressure, especially when a board member, the chair of the Audit, Risk and Compliance Committee is looking over her shoulder, will likely to force her to make mistakes.

Kyle’s dilemma is simple to explain, but more delicate to handle: « How do I fix this, without sticking my nose into the operations? »

As a NED, what Kyle needs to be is a guide to the CEO, providing a calm and supportive environment for the CEO to operate in. Kyle needs to consult with the CEO, and get her on side, to ensure she’ll devote whichever resources she does have, to deal with this issue. This won’t be a Band-Aid solution, but a solution which will require collaboration of several parts of the organisations, orchestrated by the CEO herself.

Raz Chorev is Partner at Orange Sky and Managing Director at CXC Global. He is based in Sydney, Australia.

Julie’s Answer

The Auditor General has asked management to respond and board oversight of management should be done by and through the CEO.

Kyle cannot help without putting his fingers (or intellect) into the organisation. To do that without causing upset he will need to inform the CEO of the Chairman’s request, offer to help and make sure that he reports to her before he reports elsewhere. Handled sensitively the CEO, who appears to be struggling, should welcome any assistance with the task. Handled insensitively this could be a major issue because the statutory definitions of directors’ roles in public sector companies are less fluid than those in the private sector.

Kyle should also take this as a wake-up call – he assumes a culture of compliance and good governance but that is obviously not correct. The audit committee should regularly review the regulatory and legislative compliance framework and verify that all is as it should be; that has clearly not happened and Kyle should work with the company secretary or chief compliance/legal officer to review the entire framework and make sure nothing else is missing from the regular schedule of reviews. The committee must ask for what it needs to oversight effectively not just read what they are given.

The prevailing attitude should be one of thankfulness that the issue has been found and can be corrected. If Kyle detects a cultural rejection of the need to comply and cooperate with the AG in establishing good governance then Kyle must report to the whole board so remedial action can be planned.

Once management have responded to the AG with their proposed actions to remedy the matter. The audit committee should review to check that the actions have been implemented and that they effectively lead to compliance with the requirements. Likely remedies include amending the position descriptions of staff doing tendering or those setting up vendors in the payments system to include entry of details to the register, training in compliance, design of an internal audit system for routine review of registers and comparison to workloads to ensure that nothing has ‘dropped between the cracks’, and regular reporting of register completion and audit to the board audit committee.

Sean’s Answer

The Audit Risk and Compliance Committee (« Committee ») is to assist the Board in fulfilling its corporate governance and oversight responsibilities in relation to the bodies’ financial reporting, internal control structure, risk management systems, compliance and the external audit function.

The external auditors are responsible for auditing the bodies’ financial reports and for reviewing the unaudited interim financial reports. The Financial Management and Accountability Act 1997 calls for auditing financial statements and performance reviews by the Auditor General.

As Committee Chairman Kyle must be independent and must have leadership experience and a strong finance, accounting or business background. So too must the CEO and CFO have appropriate and sufficient qualifications, knowledge, competence, experience and integrity and other personal attributes to undertake their roles.

It should be the responsibility of the Committee to maintain free and open communication between the Committee, external auditors and management. The Committee’s function is principally oversight and review.

The appointment and ongoing assessment, mentoring and discipline of the CEO rests with the board but the delegation of this authority in relation to compliance often rests with the Committee and Board Chairs.

Kyle may invite members of management (CFO and maybe the CEO) or others to attend meetings and the Committee should have authority, within the scope of its responsibilities, to seek information it requires, and assistance from any employee or external party. Inviting the CFO and or CEO to the Committee allows visibility and a holistic and independent forum where deficiencies may be isolated and functions (but not responsibility) delegated to others.

There is a disconnect or deficiency in one or more functions; Kyle should ensure that the Committee holistically review its own charter, discuss with management and the external auditors the adequacy and effectiveness of the internal controls and reporting functions (including the Bodies’s policies and procedures to assess, monitor and manage these controls), as well as a review of the internal quality control procedures (because these are also suspected to be deficient).

It will rapidly become apparent to management, the Committee, Kyle, the board and the Chairman where the deficiencies lie or did lie, and how they have been corrected. Underlying behavioural problems and or abilities to function will also become apparent and with these appropriately addressed similar deficiencies in other areas of the body may be contemporaneously corrected and all reported to the Auditor General.

Sean Rothsey is Chairman and Founder of the Merkin Group. He is based in Cooroy, Queensland, Australia.

Si l’on pouvait identifier les variables qui contribuent à créer une culture d’entreprise corrompue, pourrait-on prévoir les comportements corporatifs fautifs ?

C’est essentiellement la question de recherche à laquelle Xiaoding Liu, professeur de finance à University of Oregon’s Lundquist College of Business, a tenté de répondre dans un article utilisant une méthodologie originale et une solide analyse.

L’auteur avance qu’une culture d’entreprise souffrant d’un certain degré de corruption, c’est-à-dire ayant une culture interne plus tolérante envers le manque d’éthique, est plus susceptible de mener à des manquements corporatifs significatifs eu égard aux malversations, aux conflits d’intérêts et aux comportements organisationnels «opportunistes».

In particular, they ask whether a firm’s inherent tendency to behave opportunistically is deeply rooted in its corporate culture, commonly defined as the shared values and beliefs of a firm’s employees.

Cet article montre qu’il y a un lien significatif entre une culture interne basée sur de faibles valeurs éthiques et la probabilité d’inconduite de la direction.

De plus, l’article montre que les comportements des employés basés sur de faibles valeurs éthiques sont transmissibles à d’autres organisations et que ces conclusions s’appliquent tout autant à la direction.

C’est la raison pour laquelle les conseils d’administration doivent se préoccuper de la culture de l’entreprise, s’assurer d’avoir le pouls du climat interne et être vigilants eu égard aux manquements à l’éthique.

Il est également crucial de s’assurer d’avoir une équipe d’auditeurs internes indépendants et bien outillés qui se rapporte au comité d’audit de l’entreprise.

À la suite de ce compte rendu, vous aurez sûrement des questions d’ordre méthodologique. Si vous voulez en savoir davantage sur la démarche de l’auteur, je vous encourage fortement, même si c’est ardu, de lire l’article au complet.

A key question in corporate governance is how to control problems arising from conflicts of interest between agents and principals. The existing literature has extensively investigated traditional ways of dealing with agency problems such as hostile takeovers, the board of directors, and institutional investors, and has found mixed evidence regarding their effectiveness. Acknowledging the difficulty in designing effective governance rules to curb corporate scandals and bank failures, regulators and academics have recently turned their attention inward to the firm’s employees. In particular, they ask whether a firm’s inherent tendency to behave opportunistically is deeply rooted in its corporate culture, commonly defined as the shared values and beliefs of a firm’s employees.