Quels sont les bénéfices d’une solide culture organisationnelle ?

C’est précisément la question abordée par William C. Dudley,président et CEO de la Federal Reserve Bank de New York, dans une allocution présentée à la Banking Standards Board de Londres.

Dans sa présentation, il évoque trois éléments fondamentaux pour l’amélioration de la culture organisationnelle des entreprises du secteur financier :

Définir la raison d’être et énoncer des objectifs clairs puisque ceux-ci sont nécessaires à l’évaluation de la performance ;

Mesurer la performance de la firme et la comparer aux autres du même secteur ;

S’assurer que les mesures incitatives mènent à des comportements en lien avec les buts que l’organisation veut atteindre.

Selon M. Dudley, il y a plusieurs avantages à intégrer des pratiques de bonne culture dans la gestion de l’entreprise. Il présente clairement les nombreux bénéfices à retirer lorsque l’organisation a une saine culture.

Vous trouverez, ci-dessous, les principales raisons pour lesquelles il est important de se soucier de cette dimension à long terme. Je n’avais encore jamais vu ces raisons énoncées aussi explicitement dans un texte.

L’article a paru aujourd’hui sur le site de la Harvard Law School Forum on Corporate Governance.

I am convinced that a good or ethical culture that is reflected in your firm’s strategy, decision-making processes, and products is also in your economic best interest, for a number of reasons:

Good culture means fewer incidents of misconduct, which leads to lower internal monitoring costs.

Good culture means that employees speak up so that problems get early attention and tend to stay small. Smaller problems lead to less reputational harm and damage to franchise value. And, habits of speaking up lead to better exchanges of ideas—a hallmark of successful organizations.

Good culture means greater credibility with prosecutors and regulators—and fewer and lower fines.

Good culture helps to attract and retain good talent. This creates a virtuous circle of higher performance and greater innovation, and less pressure to cut ethical corners to generate the returns necessary to stay in business.

Good culture builds a strong organizational story that is a source of pride and that can be passed along through generations of employees. It is also attractive to clients.

Good culture helps to rebuild public trust in finance, which could, in turn, lead to a lower burden imposed by regulation over time. Regulation and compliance are expensive substitutes for good stewardship.

Good culture is, in short, a necessary condition for the long-term success of individual firms. Therefore, members of the industry must be good stewards and should seek to make progress on reforming culture in the near term.

Selon le modèle de gouvernance des entreprises privées canadiennes et américaines, le PDG (CEO) relève du conseil d’administration (CA) de l’entreprise. En effet, ce sont les actionnaires qui, lors de l’assemblée générale annuelle (AGA), votent pour des administrateurs dont la responsabilité fiduciaire est de les représenter sur le conseil d’administration de l’entreprise.

Ainsi, lors des AGA des entreprises publiques (cotées en bourse), les actionnaires sont appelés à voter sur une recommandation du CA développée par le comité de gouvernance. Il existe également des règles qui permettent aux actionnaires de faire inscrire des candidats sur la liste présentée par le CA.

Michael Sabia, PDG de la Caisse de dépôt et placement et Robert Tessier, président du conseil d’administration

Le CA a la responsabilité de veiller aux intérêts supérieurs des actionnaires tout en considérant les intérêts des diverses parties prenantes.

Les actionnaires ne votent pas pour un PDG (CEO) ; ils votent pour des représentants en qui ils ont confiance dans la supervision de leurs affaires, notamment dans le choix du premier dirigeant (PDG – CEO).

Il est clair pour tous que c’est le CA qui a la responsabilité d’embaucher le PDG (CEO), de l’orienter, de le rémunérer, de l’évaluer et de mettre en place un processus de relève et de transition.

Personnellement, je ne crois pas approprié que le PDG soit aussi un administrateur au sein du CA, bien qu’il doive y assister à titre de premier dirigeant, mais sans droit de vote.

Cette prise de position implique, a fortiori, que le PDG ne soit pas désigné comme président (Chairman of the Board) du CA.

Bien que notre mode de gouvernance semble exclure le cumul des fonctions de président du conseil et de PDG, il n’existe aucune obligation juridique à le faire.

En fait, on suppose que la séparation des fonctions, entre la présidence du conseil et la présidence de l’entreprise (CEO), est généralement bénéfique à l’exercice de la responsabilité de fiduciaire des administrateurs, c’est-à-dire que des pouvoirs distincts permettent d’éviter les conflits d’intérêts, tout en rassurant les actionnaires.

Cependant, cette pratique cède trop souvent sa place à la volonté bien arrêtée de plusieurs PDG d’exercer le pouvoir absolu, comme c’est encore le cas pour plusieurs entreprises américaines.

Le Canadian Spencer Stuart Board Index estime qu’une majorité de 85 % des 100 plus grandes entreprises canadiennes cotées en bourse a opté pour la dissociation entre les deux fonctions.

Aux États-Unis, en 2013, 45 % des entreprises de l’indice S&P500 dissociaient les rôles de PDG et de président du conseil. Plus de 50 % de ces entreprises combinent les deux fonctions !

L’article d’Yvan Allaire, publié dans le journal Les Affaires du 21 novembre 2016, mentionne « deux arguments invoqués pour appuyer la séparation des rôles » :

1- Le PDG relève du conseil qui doit en évaluer la performance, établir sa rémunération, le remplacer si cette performance est inadéquate, proposer de nouveaux membres pour le conseil ; comment peut-on, comme PDG, présider également le conseil, lequel doit prendre ces décisions critiques pour le PDG ;

Environ 50 % des grandes sociétés américaines sont présidées par un administrateur indépendant, comparativement à 23 % il y a 15 ans.

Toute la question du bien-fondé de la dualité des rôles PDG/Chairman est encore ambiguë, même si les experts de la gouvernance et les actionnaires activistes sont généralement d’accord avec la séparation des fonctions.

2- En notre époque alors que la gouvernance est plus exigeante, plus prenante de temps et d’énergie pour la société ouverte cotée en Bourse, comment une même personne peut-elle s’acquitter de ces deux rôles sans que l’un soit négligé au profit de l’autre ? Dans le nouveau contexte de gouvernance, postérieur à Sarbanes-Oxley, les exigences pour le PCA sont telles qu’il n’est pas souhaitable qu’une même personne assume ces deux fonctions (PCA et PDG).

En conséquence, 85 % des 100 plus grandes entreprises canadiennes cotées en Bourse se sont donné un président du conseil distinct du PDG, mais dans 38 % des cas ce président du conseil ne se qualifiait pas comme indépendant. (Spencer Stuart, février 2012).

La situation n’est certainement pas limpide, mais la tendance est évidente. L’indépendance du président du conseil ainsi que la séparation du pouvoir entre Chairperson du CA et CEO devrait, selon moi, trouver son application dans tous les types d’organisations : OBNL, sociétés d’État, petites et moyennes entreprises, et coopératives.

Évidemment, chaque organisation a ses particularités, lesquelles sont ancrées dans des pratiques de gouvernance assez diverses. La séparation des rôles n’est pas une panacée; c’est une meilleure assurance d’une saine gouvernance.

Cette situation montre clairement que les fonds activistes sont continuellement à la recherche de talents uniques et qu’ils sont prêts à miser des fortunes pour bénéficier de l’expertise incontestable d’un PDG.

In an unexpected turn of events, Canadian Pacific Railway announced the early departure of its CEO, Hunter Harrison, a few minutes before a conference call planned for analysts on Jan. 18. Instead of retiring as planned, Harrison leaves CP at age 72 for a new challenge, running another railway company (almost certainly CSX) on behalf of Mantle Ridge LP, a newly established hedge fund run by Paul Hilal. In his prior role at Pershing Square Capital, Hilal was instrumental in backing its investment in CP and installing Harrison’s management team.

CSX: Hunter Harrison Wants to Run His Fourth Railroad

Harrison thus forfeited all benefits and perquisites that he was entitled to receive from CP, including his pension, and he has agreed to surrender for cancellation almost all of his vested and unvested equity awards. Evidently the hedge fund will make him whole for the loss of this package, valued at approximately $118 million.

What makes Hunter Harrison so valuable? In the enchanted world of finance, there are of course no limits to what someone gets paid as long as it is a fraction of what the payer will gain. Still, one would think that a hedge fund manager looking for someone capable of turning around a poorly performing U.S. company would have an abundance of candidates to choose from. After all, the operating tricks that Harrison has come up with to make railroads more efficient have been described in minute detail in books he’s written. Dozens of seasoned railroad executives have worked with him and for him over the years. They must have learned quite a bit about Harrison’s recipe.

The answer to the $118-million question appears to reside in the fact that the successful transformation of these railroads (CN and CP) was the result, yes, of operational improvements, but more so of a fundamental cultural change. Harrison is a formidable change agent, a transformational leader in the truest meaning of that tired expression.

He claims to have invented a principle called “precision railroading,” which he implemented at three major railroads: Illinois Central, CN, and CP, the last with spectacular results, bringing the operating ratio (operating costs as a percentage of revenue, with a lower ratio being better) to 58.6 per cent for fiscal year 2016, down from 81.3 per cent in 2011, the last full year before Harrison’s took over.

Precision railroading, if it was easily learned from a book and replicated, would have been applied with success long ago at every North American railroad. Yet Harrison still seems to bring something that can make a difference over and above the techniques he developed and implemented. That something seems to be his skill at changing the culture of the railroad, a most difficult skill to imitate.

As a lifetime railroader himself, his decisions and actions display a deep understanding of the daily reality of the operators. He spends time meeting with the workers on the field and communicates profusely about the importance of asset optimization and the control of costs. At CP, he took many symbolic actions to instill in the whole organization the need to think and act like a railroader. For example, he relocated the corporate glass-towered headquarters to a rail yard, a move that was meant partly to cut costs but mostly to keep the employees’ focus on freight operations, and remind them daily of what the business is all about.

Managing a strategic turnaround is not an easy task. The softer, cultural element of it is often neglected, overlooked, and difficult to implement. That is where Harrison excels and why a hedge fund manager is prepared to pay big bucks to get that talent working for him.

But is money really the sole motivation for Harrison to start over at another railroad company at 72? In fact, at this stage of his career, he has more to lose reputation-wise if he fails than anything he can really earn in monetary terms.

The Memphis, Tenn. native, whose career began over five decades ago as an 18-year-old carman-oiler, may be driven by the determination to prove that the theory he has developed is replicable, no matter where. And determined to push his legacy to a new level — that of a railroad industry legend.

__________________________________

*Yvan Allaire est professeur émérite de stratégie à l’Université du Québec à Montréal (UQAM) et président exécutif de l’Institut de la gouvernance des organisations privées et publiques (IGOPP), François Dauphin est directeur de la recherche à l’IGOPP et chargé d’enseignement à l’UQAM.

Yvan Allaire*, président exécutif de l’Institut de la gouvernance des organisations privées et publiques (IGOPP), vient de me transmettre une synthèse de l’analyse de la saga CP-Ackman-Pershing Square, portant sur les leçons à tirer de cet épisode d’agression par un fonds « activiste ».

Cet article a été publié sur le site du Harvard Law School Forum on Corporate Governance and Financial Regulation le 23 décembre 2016.

Comme le disent les auteurs, l’une des leçons à retirer de cette saga est que les conseils d’administration de l’avenir doivent agir comme des activistes, en ce sens qu’ils doivent être continuellement à la recherche d’informations susceptibles de questionner leurs stratégies et leur modèle d’affaires. Sinon, certains fonds activistes seront bien tentés par l’aventure…

Le texte complet du cas est accessible en cliquant sur « here » en fin de texte.

Pershing Square Capital Management, an activist hedge fund owned and managed by Bill Ackman, began hostile maneuvers against the board of CP Rail in September 2011 and ended its association with CP in August 2016, having netted a profit of $2.6 billion for his fund. This Canadian saga, in many ways, an archetype of what hedge fund activism is all about, illustrates the dynamics of these campaigns and the reasons why this particular intervention turned out to be a spectacular success… thus far.

In 2009, the Chairman of the board of the Canadian Pacific Railway (CP) asserted that the company had put in place the best practices of corporate governance; that year, CP was awarded the Governance Gavel Award for Director Disclosure by the Canadian Coalition for Good Governance. Then, in 2011, CP ranked 4th out of some 250 Canadian companies in the Globe & Mail Corporate Governance Ranking. [1] Yet, this stellar corporate governance was no insurance policy against shareholder discontent.

Pershing Square began purchasing shares of CP on September 23, 2011. They filed a 13D form on October 28th showing a stock holding of 12.2%; by December 12, 2011, their holding had reached 14.2% of CP voting shares, thus making Pershing Square the largest shareholder of the company.

On February 6, 2012, Ackman, with Hunter S. Harrison (retired CEO of CN—direct competitor of CP and leader in efficiency among Class 1 North American railways—and his candidate for CEO of CP) by his side, made a fact-based presentation about the shortcomings and failings of the CP board and management. Harrison and Ackman stated that their goal for CP was to achieve an operating ratio of 65 for 2015 (down from 81.3 in 2011—the lower the ratio, the better the performance).

The Board qualified Harrison’s (and Ackman’s) targets of “shot in the dark”, showing a lack of research and a profound misunderstanding of CP’s reality. Relying on an independent consultant report (Oliver Wyman Group), Green mentioned that Harrison’s target for CP’s operating ratio was not achievable since CP’s network was characterized by steeper grades and greater curvature thus adding close to 6.7% to the operating ratio compared to its competitors. [2]

On April 4th 2012, Bill Ackman came out swinging in a scathing letter to CP shareholders disparaging CP’s Board of directors in general, and its CEO, Fred Green, in particular. According to Mr. Ackman, “under the direction of the Board and Mr. Green, CP’s total return to shareholders from the inception of Mr. Green’s CEO tenure to the day prior to Pershing Square’s investment was negative 18% while the other Class I North American railways delivered strong positive total returns to shareholders of 22% to 93%.” [3] Thus, according to him, “Fred Green’s and the Board’s poor decisions, ineffective leadership and inadequate stewardship have destroyed shareholder value.” [4]

A few hours before the annual meeting, CP issued a press release in which it stated that Fred Green had resigned as CEO, and that five other directors, including the Chairman of the Board, John Cleghorn, would not stand for re-election at the company’s shareholder meeting.

Pershing Square had won the proxy fight; all the nominees proposed by Ackman were elected.

Almost exactly five years after first buying shares of CP, Ackman confirmed in August 2016 that Pershing Square would sell its remaining shares of CP, thus formally exiting the “target.” Over those five years, CP has generated a compounded annualized total shareholder return of 45.39% (between September 23, 2011 and August 31, 2016), a performance well above the CN and the S&P/TSX 60 index (CP is a constituent of that index). Pershing Square pocketed an estimated $2.6 billion in profits for its venture into CP.

With massive reductions in the workforce, a transformation of the operations and a radical change of the CP’s organizational culture, CP is undoubtedly a different company from what it was before the proxy fight. In early September 2016, Bill Ackman resigned from CP’s Board, officially concluding this episode.

Lessons in corporate governance

In this day and age, the CP case teaches us that no matter its size or the nature of its business, a company is always at risk of being challenged by dissident shareholders, and most particularly by those funds which make a business of these sorts of operations, the activist hedge funds. Of course, a number of critical features of this saga can be singled out to explain the particular success of this intervention, but this is not the focal point of this post. [5] After all, a widely held company with weak financial results and a stagnating stock price will inevitably attract the attention of these funds.

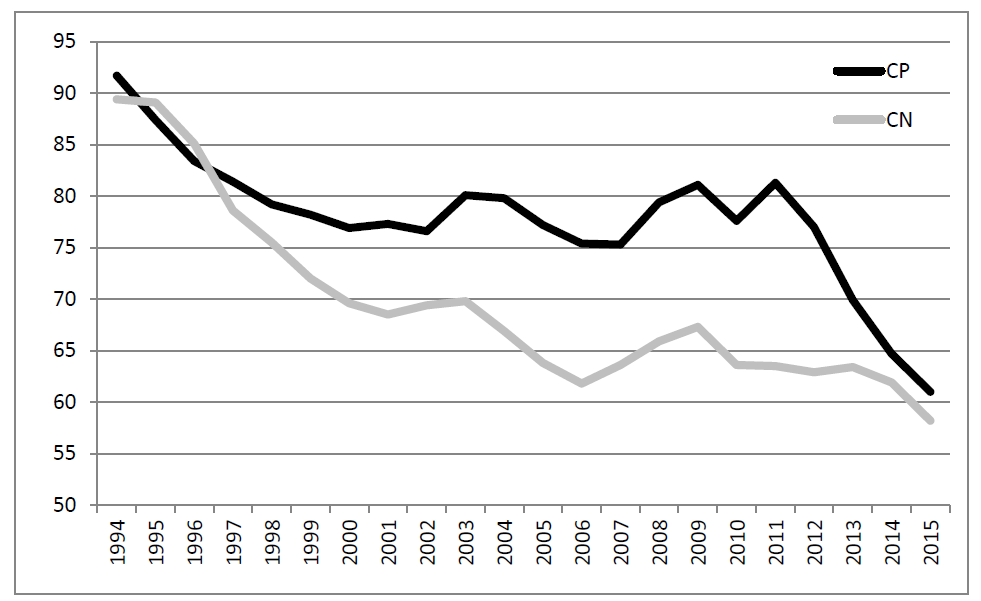

But the puzzling question and it is an unresolved dilemma of corporate governance remains: how come the board did not know earlier what became apparent very quickly after the Ackman/Harrison takeover? Why would the board not call on independent experts to assess management’s claim that structural differences made it impossible for CP to achieve a performance similar to that of other railroads? The gap in operating ratio between CP and CN had not always been as wide. In fact, as shown in Figure 1, CP had a lower operating ratio than CN during a period of time in the 1990s (Of course, CN was a Crown corporation at that time). The gap eventually widened, reaching unprecedented levels during Fred Green’s tenure (the last full year of operating ratios attributable to Green was in 2011).

Figure 1. Evolution of the operating ratio (%—left scale) for the CP and CN (1994-2015)

How could the board have known that performances far superior to those targeted by the CEO could be swiftly achieved?

Lurking behind these questions is the fundamental flaw of corporate governance: the asymmetry of information, of knowledge and time invested between the governors and the governed, between the board of directors and management. In CP’s case, the directors, as per the norms of “good” fiduciary governance, relied on the information provided by management, believed the plans submitted by management to be adequate and challenging, and based the executives’ lavish compensation on the achievement of these plans. The Chairman, on behalf of the Board, did “extend our appreciation to Fred Green and his management team for aggressively and successfully implementing our Multi-Year plan and creating superior value for our shareholders and customers.” [6] That form of governance is being challenged by activist investors of all stripes.

Their claim, a demonstrable one in the case of CP, is that with the massive amount of information now accessible about a publicly listed company and its competitors, it is possible for dedicated shareholders to spot poor strategies and call for drastic changes. If push comes to shove, these funds will make their case directly to other shareholders via a proxy contest for board membership.

Corporate boards of the future will have to act as “activists” in their quest for information and their ability to question strategies and performances.

5The case analysis identified four factors that are rarely present in other cases of activism, a fact which explains why few of these interventions achieve the level of success of the CP case.(go back)

6Cleghorn, John. Chairman’s letter to shareholders, CP’s Annual Information Form 2011.(go back)

__________________________________

*Yvan Allaire is Emeritus professor of strategy at Université du Québec à Montréal (UQAM) and Executive Chair of the Institute for Governance of Private and Public Organizations (IGOPP); François Dauphin is Director of Research of IGOPP and a lecturer at UQAM. This post is based on their recent paper.

Cet article récemment publié par Richard T. Thakor*, dans le Harvard Law School Forum on Corporate Governance, aborde une problématique très singulière des projets organisationnels de nature stratégique.

L’auteur tente de prouver que même si les CEO ont généralement une vision à long terme de l’organisation, ils doivent adopter des positions qui s’apparentent à des comportements courtermistes pour pouvoir évoluer avec succès dans le monde des affaires. Ainsi, l’auteur insiste sur l’efficacité de certaines actions à court terme lorsque la situation l’exige pour garantir l’avenir à long terme.

Aujourd’hui, le courtermisme a mauvaise presse, mais il faut bien se rendre à l’évidence que c’est très souvent l’approche poursuivie…

L’étude montre qu’il existe deux situations susceptibles d’exister dans toute entreprise :

il y a des circonstances qui amènent les propriétaires à choisir des projets à court terme, même si ceux-ci auraient plus de valeur s’ils étaient effectués avec une vision à long terme. L’auteur insiste pour avancer qu’il y a certaines situations qui retiennent l’attention des propriétaires pour des projets à long terme.

ce sont les gestionnaires détestent les projets à court terme, même si les propriétaires les favorisent. Pour les gestionnaires, ils ne voient pas d’avantages à faire carrière dans un contexte de court terme.

L’auteur donne des exemples de situations qui favorisent l’une ou l’autre approche. Ou les deux !

Bonne lecture. Vos commentaires sont les bienvenus.

In the area of corporate investment policy and governance, one of the most widely-studied topics is corporate “short-termism” or “investment myopia”, which is the practice of preferring lower-valued short-term projects over higher-valued long-term projects. It is widely asserted that short-termism is responsible for numerous ills, including excessive risk-taking and underinvestment in R&D, and that it may even represent a danger to capital quiism itself. Yet, short-termism continues to be widely practiced, exhibits little correlation with firm performance, and does not appear to be used only by incompetent or unsophisticated managers (e.g. Graham and Harvey (2001)). In A Theory of Efficient Short-termism, I challenge the notion that short-termism is inherently a misguided practice that is pursued only by self-serving managers or is the outcome of a desire to cater to short-horizon investors, and theoretically ask whether there are circumstances in which it is economically efficient.

I highlight two main findings related to this question. First, there are circumstances in which the owners of the firm prefer short-term projects, even though long-term projects may have higher values. There are other circumstances in which the firm’s owners prefer long-term projects. Moreover, this is independent of any stock market inefficiencies or pressures. Second, it is the managers with career concerns who dislike short-term projects, even when the firm’s owners prefer them.

These results are derived in the context of a model of internal governance and project choice, with a CEO who must approve projects that are proposed by a manager. The projects are of variable quality—they can be good (positive NPV) projects or bad (negative NPV) projects. The manager knows project quality, but the CEO does not. Regardless of quality, the project can be (observably) chosen to be short-term or long-term, and a long-term project has higher intrinsic value. The probability of success for any good project depends on managerial ability, which is ex ante unknown to everybody.

In this setting, the manager has an incentive to propose only long-term projects, because shorter projects carry with them a risk of revealing negative information about the manager’s ability in the interim. Put differently, by investing in a short-term project that reveals early information about managerial ability, the manager gives the firm (top management) the option of whether to give him a second-period project with managerial private benefits linked to it, whereas with the long-term project the manager keeps this option for himself. The option has value to the firm and to the manager. Thus, the manager prefers to retain the option rather than surrendering it to the firm.

The CEO recognizes the manager’s incentive, and may thus impose a requirement that any project that is funded in the first period must be a short-term project. This makes investing in a bad project in the first period more costly for the manager because adverse information is more likely to be revealed early about the project and hence about managerial ability. The manager’s response may be to not request first-period funding if he has only a bad project. Such short-termism generates another benefit to the firm in that it speeds up learning about the manager’s a priori unknown ability, permitting the firm to condition its second-period investment on this learning.

There are a number of implications of the analysis. First, not all firms will practice short-termism. For example, firms for which the value of long-term projects is much higher than that of short-term projects—such as some R&D-intensive firms—will prefer long-term projects, so not all firms will display short-termism. Second, since short-termism is intended to prevent lower-level managers from investing in bad projects, its use should be greater for managers who typically propose “routine” projects and less for top managers (like the CEO) who would typically be involved in more strategic projects. Related to this, since it is more difficult to ascertain an individual employee’s impact on a project’s payoffs at lower levels of the hierarchy, this suggests that the firm is more likely to impose a short-termism constraint on lower-level managers. Third, the analysis may be particularly germane for managers who care about how their ability is perceived prior to the realization of project payoffs. As an example of this, it is not uncommon for a manager to enter a job with the intention or expectation of finding a new job within a few years. The analysis then suggests that the manager would rather not jeopardize future employment opportunities by allowing (potentially risky) project outcomes to be revealed in the short-term, instead preferring that those outcomes be revealed at a time when the manager need not be concerned about the result (i.e. in a different job).

Overall, the most robust result from this analysis is that informational frictions may bias the investment horizons of firms, and that the bias towards short-termism may, in fact, be value-maximizing in the presence of such frictions. This means that castigating short-termism as well as the rush to regulate CEO compensation to reduce its emphasis on the short term may be worth re-examining. Indeed, not engaging in short-termism may signal an inability or unwillingness on the CEO’s part to resolve intrafirm agency problems and thus adversely affect the firm’s stock price. This is not to suggest that short-termism is necessarily always a value-maximizing practice, since some of it may be undertaken only to boost the firm’s stock price. The point of this paper is simply that some short-termism reduces agency costs and benefits the shareholders.

For example, the project horizon for a beer brewery is typically 15-20 years. Similarly, R&D investments by drug companies have payoff horizons typically exceeding 10 years.

Graham, John R., and Campbell R. Harvey, 2001, “The Theory and Practice of Corporate Finance: Evidence from the Field”. Journal of Financial Economics, 60 (2-3), 187-243.

This is in line with Roe (2015), who states: “Critics need to acknowledge that short-term thinking often makes sense for U.S. businesses, the economy and long-term employment … it makes no sense for brick-and-mortar retailers, say, to invest in long-term in new stores if their sector is likely to have no future because it will soon become a channel for Internet selling.”

One can think about the long-term and short-term projects concretely through examples. Within each firm, there are typically both short-term and long-term projects. For example, for an appliance manufacturer, investing in modifying some feature of an existing appliance, say the size of the freezer section in a refrigerator, would be a short-term project. By contrast, building a plant to make an entirely new product—say a high-technology blender that does not exist in the company’s existing product portfolio—would be a long-term project. The long-term project will have a longer gestation period, with not only a longer time to recover the initial investment through project cash flows, but also a longer time to resolve the uncertainty about whether the project has positive NPV in an ex post sense. There may also be industry differences that determine project duration. For example, long-distance telecom companies (e.g. AT&T) will typically have long-duration projects, whereas consumer electronics firms will have short-duration projects.

*Richard T. Thakor, Assistant Professor of Finance at the University of Minnesota Carlson School of Management.

Aujourd’hui, je partage avec vous les réflexions de Ben W. Heineman, Jr*, ex-conseiller en chef de GE et Fellow de la Harvard Law School et de la Kennedy School of Government.

L’article illustre certaines dysfonctions du processus politique américain et montre que les sociétés américaines sont, en partie responsable du climat de méfiance de la population envers Washington.

L’auteur identifie plusieurs moyens que le monde des affaires devrait explorer afin de remédier aux lacunes observées dans le fonctionnement de notre démocratie et des relations entre le gouvernement et les sociétés :

Limitation des sommes investies par les entreprises dans les campagnes politiques (7 milliards US en 2016)

Divulgation financière accrue

Meilleure identification des éléments factuels en matière politique

Reconnaître la nécessité de se mettre à la place de l’autre partie dans le but d’atteindre un équilibre des valeurs

Bâtir de larges coalitions

Garder la tête froide afin d’éviter la confrontation

Éviter la partisanerie

Le monde des entreprises ne doit pas s’ériger en modèle eu égard à la gestion des affaires de l’État ; cependant, je crois que les organisations doivent prendre en compte les moyens suggérés par l’auteur afin d’améliorer la communication et la bonne gouvernance.

Many business people are appalled at the current state of our politics. Few, however, would admit that the “business community” is responsible, in part, for our dysfunctional political culture. And fewer yet may be prepared to think about how business can take steps—in concert with other political actors—to help soothe the distemper.

But, this dreary campaign season is a good time for corporate leaders to consider specific changes in political processes—less money, more disclosure, fair facts, balanced proposals, broad coalitions, cooler rhetoric, bi-partisanship—which could help fix our broken politics and rehabilitate business’s own political standing. Such process changes proceed from an understanding that there will always be significant substantive policy differences about societal problems but that those differences require a national politics that promotes common sense, civility and compromise to move the country forward, as has happened before in our history.

First a brief background sketch on the sorry state of our current political discourse.

The problem in our political system is not just the cacophony of the campaigns which distorts and obscures the real issues facing the nation. Below the noise, we have a populist revolt among a significant segment of the electorate that is more sharply critical of business than the general anti-corporate undercurrent which has long been present in American politics. That revolt stems partly from genuine problems of recession and a changing economy which is leaving some people behind but partly from the demagogic appeals to latent anger about race, immigration, Islam and trade. Moreover, the two major parties have been dead-locked for a long time on how to deal with major issues of paramount concern to the economy and the country—e.g., taxes, trade, worker dislocation, inequality, stimulus/deficit, infrastructure, immigration, education, energy and the environment—yielding a Congressional approval rating of only 14 percent!

Moreover, the well-publicized problems in the corporate community have added to political dysfunction, leading to low levels of trust in business’ role in policy and politics. These include: a steady drumbeat of corporate scandals (Wells Fargo is only the latest); ever higher executive compensation combined with stagnant real income of average citizens; corporate mistakes relating to leverage and liquidity as a major cause of the Great Recession; the perception that business elites are have disproportionate influence due to money in politics; and an aggregate sense that too much of corporate involvement in policy is in the service of “crony capitalism”, the range of subsidies, loopholes, franchises, concessions et al. that have little or no basis in advancing the broad public interest.

Business is hardly alone in its credibility problems with parts of the electorate. Other prominent actors—for example, unions, consumers, environmentalists and political parties—also have perceived failings. And, while some of the general distrust is due to political hyperventilation, there are, as noted, genuine substantive differences about whether libertarian, conservative, populist or liberal ideas are the right approach to various national problems.

But the rude noise of our current politics and the genuine substantive differences suggest that business ought to consider working with other actors in our political system on at least the following issues of political process to engender more civility and compromise. Each of these subjects is worthy of extended, book-length discussions, but here are the headlines:

New substantive limits on campaigns awash in money (more than $7B estimated in 2016 federal elections).

Although “independent” spending for educational purposes or in support of candidates is protected speech under the First Amendment, it may be limited under the Constitution if improperly “coordinated” with candidates’ campaigns or if used for “corrupt” purposes. Similarly, “educational” efforts by social welfare organizations authorized by the IRS could be more carefully circumscribed only to include genuine charitable and less partisan activities. Congress could take such narrowing steps or authorize the IRS and a reconstituted Federal Election Commission (which could have a tie-breaking chair appointed by the party in power) to address these issues.

More financial disclosure.

In elections, the Federal Election Commission and the IRS could require more real time disclosure of contributors and expenditures for “independent” entities organized under their jurisdiction. This timely disclosure (the IRS is particularly slow) would also cover more campaign finance if the scope of campaign activity funded through IRS entities was limited, forcing independent funds into the more transparent FEC Super PACs. And, the IRS could consider whether there should be an exception to the general rule of non-disclosure regarding contributors for trade associations or other authorized 501(c)(3) entities engaged in “education” on campaign issues during a defined political season.

Develop fairer, clearer facts in policy disputes.

Corporations and other parties could work with public officials to devise better, honest methods for establishing a record of consensus facts in legislative and regulatory disputes and identifying the assumptions underlying contested facts so that the battle of experts is more clearly understood by decision-makers and the public.

Acknowledge the need to balance values in conflict.

Corporations and other parties should identify and acknowledge the values on both sides of most regulatory and legislative debates and make a good faith effort to give weight to all the values in conflict, e.g. finding a fair balance between the verities of equity and efficiency in social welfare legislation or between access, cost and quality in healthcare legislation or between expedition and safety in drug approvals or between short-term cost and long-term benefit in environmental regulation.

Build broad coalitions.

Too often business public policy efforts take place in the self-referential echo-chamber of trade associations or other business groups. Working with other interested parties to create coalitions that include, but are not limited to, business allies increases the chances of broad-minded approaches that can secure approval and provide durable benefits. Indeed, there no united “business community,” and disagreements among business actors (e.g. global v. domestic, tech v. industrial) means broader coalition building is necessary.

Cool the rhetoric.

One of the poisonous aspects of our current political culture is rhetoric that demonizes opponents with words like “hate” or that bemoans an approaching American Armageddon. Business, especially, should use calm and reasoned civil discourse, recognizing that there are usually legitimate opposing values in political debates and helping find a middle ground that does not demand total victory.

Avoid Partisanship.

Corporations should seek bipartisan or nonpartisan solutions to our most pressing problems to mitigate the anger and hostility exchanged across the aisle on so many pressing national issues which require sensible compromises. Too often relations in Congress or between Congress and the Executive look like an insoluble “blood feud.”

There should be no mistake. These political process issues—relating to money, facts, balance, coalitions, rhetoric and bipartisanship—may be as vexing and controversial for the business community as substantive policy positions. Some companies will resist, inter alia, because they believe their particular substantive position is more important than general process or because they believe gridlock in public policy is better than compromise.

Nonetheless, a timely question is whether corporations, by focusing on these and other process issues, can help heal, rather than exacerbate, the manifest ills in our political system—ills posing serious threats to the maintenance of a healthy constitutional democracy and a sound mixed economy in which vital public goods can be secured and private enterprise can flourish? These issues relating to the process of political participation should be central to a company’s future debates about what constitutes being a “good corporate citizen.” This subject is too vast for a single corporation, but a broad based “coalition of the willing,” extending far beyond corporations, may be the way past the dystopic present—what leading political scientist Francis Fukuyama has warned is American “political decay”—to a post-election future of a vibrant and workable democracy.

__________________________________

*Ben W. Heineman, Jr. is former GE General Counsel and is a senior fellow at Harvard Law School and Harvard Kennedy School of Government. He is author of the new book, The Inside Counsel Revolution: Resolving the Partner-Guardian Tension (Ankerwycke 2016), as well as High Performance with High Integrity (Harvard Business Press 2008).

Le 28 septembre 2016, le gouvernement fédéral a proposé un certain nombre de modifications à la Loi canadienne sur les sociétés par actions (projet de loi C-25) afin de clarifier les obligations de divulgation des émetteurs canadiens. Les amendements à la loi ont deux objectifs :

(1) s’assurer que certaines règles adoptées par le Toronto Stock Exchange (TSX) soient clarifiées et incorporées dans la loi canadienne sur les sociétés par actions ;

(2) faire en sorte que la loi amendée reflète davantage les bonnes pratiques de gouvernance généralement reconnue.

Dans leur compte rendu sur les implications de ce projet de loi, paru sur le site du Harvard Law School Forum on Corporate Governance, Louis-Martin O’NeilletJennifer Longhurst,associés de la firme Davies Ward Phillips & Vineberg LLP, discutent de trois changements susceptibles d’affecter la gouvernance et les modes de divulgation des sociétés.

Voici les changements proposés :

True majority voting: requiring shareholders to cast their votes “for” or “against” each individual director’s election (rather than slate voting), and prohibiting a director who has not been elected by a majority of the votes cast from serving as a direcror, except in “prescribed circumstances”;

Annual director elections: requiring corporations to hold annual elections for all directors of a company’s board, effectively prohibiting staggered boards; and

Diversity disclosures: requiring corporations to place before shareholders, at each AGM, information respecting diversity among the directors and among the members of senior management.

Je vous encourage à prendre connaissance de ce bref article.

Amendement à la loi canadienne sur les sociétés par actions | Proposed Changes to the Canada Business Corporations Act – How Could this Affect You?

True majority voting requirement

In 2014, the Toronto Stock Exchange (TSX) implemented rules requiring majority voting for most TSX-listed issuers. This entailed adopting a majority voting policy requiring any undersupported director (i.e., a nominee who does not receive a majority of “for” votes) in an uncontested director election to tender his or her resignation to the board; the board is then required to consider and, save for “exceptional circumstances,” accept that resignation and publicly announce its decision. Since then, there has been some lingering controversy surrounding the TSX’s majority voting standard as a result of many boards rejecting the resignations of undersupported directors in reliance on those so-called exceptional circumstances, despite the expressed will of the shareholders.

For example, our Davies Governance Insights 2015 report revealed that in 2015 only one of 10 directors who failed to achieve majority support from shareholders had their resignation accepted by the board. The report explained how some of the boards relied on the “exceptional circumstances” carve-out to allow undersupported directors to remain on the board. Our most recent Davies Governance Insights 2016 report, however, suggests that this trend may be changing: in 2016, in those cases where directors of issuers on the TSX/S&P Composite and SmallCap indices received less than majority approval, the boards accepted their resignations.

The Proposed Amendments would put an end to this debate. They provide that (1) the shareholders of a distributing corporation will be able to vote only “for” or “against” each individual director (as opposed to withholding their votes); and (2) each director is elected only if the number of “for” votes represents a majority of the total shareholder votes cast. Slate voting would no longer be permitted, except for certain “prescribed corporations” (to be outlined in revised regulations, not yet published, to the CBCA). Moreover, the Proposed Amendments also provide that a director who is not elected by a majority cannot be appointed by the remaining directors to fill a vacancy on the board, except in “prescribed circumstances.”

In doing so, the Proposed Amendments would reverse the current practice that has developed under the TSX rules: rather than having an undersupported nominee elected as a matter of law and leaving to the board the decision on whether to accept their resignation, the Proposed Amendments would mean that a nominee who fails to get a majority of “for” votes is not elected as a matter of law, and may be appointed by the directors only in “prescribed circumstances.” Whether the Proposed Amendments will result in meaningful change to the current practice for TSX-listed companies will, however, depend on what those “prescribed circumstances” are, to be set out in the not yet released regulations to the CBCA.

Annual elections now required

The TSX rules currently require its listed companies to hold annual director elections, effectively prohibiting staggered boards, a fairly uncommon practice in Canada. The Proposed Amendments will bring the CBCA up to speed with this current corporate governance best practice. We note that an exception included in the Proposed Amendments allows for elections to be held in accordance with existing CBCA requirements, which allow for three-year terms and staggered boards, in the case of “any prescribed class of distributing corporations” or “any prescribed circumstances respecting distributing corporations.” There is currently no such exception in the TSX rules, save for foreign issuers. The impact of this change will, therefore, depend upon the prescribed categories of corporations and circumstances that will be proposed in the CBCA regulations, if this change is implemented.

Disclosure relating to diversity

TSX-listed and other non-venture issuers are currently required, under National Instrument 58-101—Disclosure of Corporate Governance Practices (NI 58-101), to disclose certain information relating to the diversity of their board and executive officers, including whether they have adopted a written policy regarding female representation on the board, whether they consider the level of female representation when making board or executive officer nominations or appointments, and whether they have adopted a target regarding the representation of women on the board or in senior management; if not, the issuer must disclose why not. The Proposed Amendments to the CBCA would require “prescribed corporations” to provide the “prescribed information” respecting diversity among their directors and members of senior management.

Once again, the “prescribed corporations” and “prescribed information” that will need to be disclosed have not yet been determined. Accordingly, until proposed regulations clarifying these concepts have been released, it remains unclear whether the Proposed Amendments will alter the existing “comply or explain” model under NI 58-101 or impose stricter requirements on subject companies. We do not, however, expect the Proposed Amendments to impose targets or quotas on issuers; instead, they are likely to promote a similar approach to that currently in place under securities laws.

Conclusions

The majority voting requirement set forth in the Proposed Amendments is likely to bring an end to the debate over those circumstances in which an undersupported director may remain on the board. The questions, however, that are still unanswered will be whether boards will be inclined to use the Proposed Amendments to fill a vacancy by appointing an undersupported director whose failed election created the vacancy in the first place; and, in such a situation, how stringent the “prescribed circumstances” will be that would allow the directors to appoint an undersupported director. We also note there are some inconsistencies between the TSX rules and the Proposed Amendments that could subject some TSX-listed CBCA companies to potentially different (and potentially conflicting) sets of rules. We expect the regulators are attuned to and will be focused on minimizing that risk. In any case, if the Proposed Amendments are adopted, we expect TSX-listed issuers that are governed by the CBCA may need to revisit and revise their majority voting policies to ensure compliance with the Proposed Amendments.

While some view the Proposed Amendments as a welcome modernization of the federal corporate statute and a reflection of the need to enhance companies’ corporate governance practices, in many ways the Proposed Amendments are entrenching practices or policies that are already addressed under the TSX rules and securities laws. By delving into these areas, there remains a risk that the Proposed Amendments could lead to compliance and interpretational issues, as well as confusion over the appropriate mandates for each of the regulators, a concern expressed by some commentators in response to Industry Canada’s initial December 2013 consultation paper on the potential CBCA amendments. In addition, several undetermined exceptions and terms that will be laid out in revised CBCA regulations have yet to be published—only once they are will the full impact of the Proposed Amendments be known.

Cet article récemment publié par Richard T. Thakor*, dans le Harvard Law School Forum on Corporate Governance, aborde une problématique très singulière des projets organisationnels de nature stratégique.

L’auteur tente de prouver que même si les CEO ont généralement une vision à long terme de l’organisation, ils doivent adopter des positions qui s’apparentent à des comportements courtermistes pour pouvoir évoluer avec succès dans le monde des affaires. Ainsi, l’auteur insiste sur l’efficacité de certaines actions à court terme lorsque la situation l’exige pour garantir l’avenir à long terme.

Aujourd’hui, le courtermisme a mauvaise presse, mais il faut bien se rendre à l’évidence que c’est très souvent l’approche poursuivie…

L’étude montre qu’il existe deux situations susceptibles d’exister dans toute entreprise :

il y a des circonstances qui amènent les propriétaires à choisir des projets à court terme, même si ceux-ci auraient plus de valeur s’ils étaient effectués avec une vision à long terme. L’auteur insiste pour avancer qu’il y a certaines situations qui retiennent l’attention des propriétaires pour des projets à long terme.

ce sont les gestionnaires détestent les projets à court terme, même si les propriétaires les favorisent. Pour les gestionnaires, ils ne voient pas d’avantages à faire carrière dans un contexte de court terme.

L’auteur donne des exemples de situations qui favorisent l’une ou l’autre approche. Ou les deux !

Bonne lecture. Vos commentaires sont les bienvenus.

In the area of corporate investment policy and governance, one of the most widely-studied topics is corporate “short-termism” or “investment myopia”, which is the practice of preferring lower-valued short-term projects over higher-valued long-term projects. It is widely asserted that short-termism is responsible for numerous ills, including excessive risk-taking and underinvestment in R&D, and that it may even represent a danger to capital quiism itself. Yet, short-termism continues to be widely practiced, exhibits little correlation with firm performance, and does not appear to be used only by incompetent or unsophisticated managers (e.g. Graham and Harvey (2001)). In A Theory of Efficient Short-termism, I challenge the notion that short-termism is inherently a misguided practice that is pursued only by self-serving managers or is the outcome of a desire to cater to short-horizon investors, and theoretically ask whether there are circumstances in which it is economically efficient.

I highlight two main findings related to this question. First, there are circumstances in which the owners of the firm prefer short-term projects, even though long-term projects may have higher values. There are other circumstances in which the firm’s owners prefer long-term projects. Moreover, this is independent of any stock market inefficiencies or pressures. Second, it is the managers with career concerns who dislike short-term projects, even when the firm’s owners prefer them.

These results are derived in the context of a model of internal governance and project choice, with a CEO who must approve projects that are proposed by a manager. The projects are of variable quality—they can be good (positive NPV) projects or bad (negative NPV) projects. The manager knows project quality, but the CEO does not. Regardless of quality, the project can be (observably) chosen to be short-term or long-term, and a long-term project has higher intrinsic value. The probability of success for any good project depends on managerial ability, which is ex ante unknown to everybody.

In this setting, the manager has an incentive to propose only long-term projects, because shorter projects carry with them a risk of revealing negative information about the manager’s ability in the interim. Put differently, by investing in a short-term project that reveals early information about managerial ability, the manager gives the firm (top management) the option of whether to give him a second-period project with managerial private benefits linked to it, whereas with the long-term project the manager keeps this option for himself. The option has value to the firm and to the manager. Thus, the manager prefers to retain the option rather than surrendering it to the firm.

The CEO recognizes the manager’s incentive, and may thus impose a requirement that any project that is funded in the first period must be a short-term project. This makes investing in a bad project in the first period more costly for the manager because adverse information is more likely to be revealed early about the project and hence about managerial ability. The manager’s response may be to not request first-period funding if he has only a bad project. Such short-termism generates another benefit to the firm in that it speeds up learning about the manager’s a priori unknown ability, permitting the firm to condition its second-period investment on this learning.

There are a number of implications of the analysis. First, not all firms will practice short-termism. For example, firms for which the value of long-term projects is much higher than that of short-term projects—such as some R&D-intensive firms—will prefer long-term projects, so not all firms will display short-termism. Second, since short-termism is intended to prevent lower-level managers from investing in bad projects, its use should be greater for managers who typically propose “routine” projects and less for top managers (like the CEO) who would typically be involved in more strategic projects. Related to this, since it is more difficult to ascertain an individual employee’s impact on a project’s payoffs at lower levels of the hierarchy, this suggests that the firm is more likely to impose a short-termism constraint on lower-level managers. Third, the analysis may be particularly germane for managers who care about how their ability is perceived prior to the realization of project payoffs. As an example of this, it is not uncommon for a manager to enter a job with the intention or expectation of finding a new job within a few years. The analysis then suggests that the manager would rather not jeopardize future employment opportunities by allowing (potentially risky) project outcomes to be revealed in the short-term, instead preferring that those outcomes be revealed at a time when the manager need not be concerned about the result (i.e. in a different job).

Overall, the most robust result from this analysis is that informational frictions may bias the investment horizons of firms, and that the bias towards short-termism may, in fact, be value-maximizing in the presence of such frictions. This means that castigating short-termism as well as the rush to regulate CEO compensation to reduce its emphasis on the short term may be worth re-examining. Indeed, not engaging in short-termism may signal an inability or unwillingness on the CEO’s part to resolve intrafirm agency problems and thus adversely affect the firm’s stock price. This is not to suggest that short-termism is necessarily always a value-maximizing practice, since some of it may be undertaken only to boost the firm’s stock price. The point of this paper is simply that some short-termism reduces agency costs and benefits the shareholders.

For example, the project horizon for a beer brewery is typically 15-20 years. Similarly, R&D investments by drug companies have payoff horizons typically exceeding 10 years.

Graham, John R., and Campbell R. Harvey, 2001, “The Theory and Practice of Corporate Finance: Evidence from the Field”. Journal of Financial Economics, 60 (2-3), 187-243.

This is in line with Roe (2015), who states: “Critics need to acknowledge that short-term thinking often makes sense for U.S. businesses, the economy and long-term employment … it makes no sense for brick-and-mortar retailers, say, to invest in long-term in new stores if their sector is likely to have no future because it will soon become a channel for Internet selling.”

One can think about the long-term and short-term projects concretely through examples. Within each firm, there are typically both short-term and long-term projects. For example, for an appliance manufacturer, investing in modifying some feature of an existing appliance, say the size of the freezer section in a refrigerator, would be a short-term project. By contrast, building a plant to make an entirely new product—say a high-technology blender that does not exist in the company’s existing product portfolio—would be a long-term project. The long-term project will have a longer gestation period, with not only a longer time to recover the initial investment through project cash flows, but also a longer time to resolve the uncertainty about whether the project has positive NPV in an ex post sense. There may also be industry differences that determine project duration. For example, long-distance telecom companies (e.g. AT&T) will typically have long-duration projects, whereas consumer electronics firms will have short-duration projects.

*Richard T. Thakor, Assistant Professor of Finance at the University of Minnesota Carlson School of Management.

Au lendemain du référendum mené en Grande-Bretagne (GB), on peut se demander quelles sont les implications juridiques d’une telle décision. Celles-ci sont nombreuses ; plusieurs scénarios peuvent être envisagés pour prévoir l’avenir des relations entre la GB et l’Union européenne (UE).

Ben Perry de la firme Sullivan & Cromwell et Simon Witty de la firme Davis Polk & Wardwell ont exploré toutes les facettes légales de cette nouvelle situation dans deux articles parus récemment sur le site du Harvard Law School Forum on Corporate Governance.

Ce sont deux articles très approfondis sur les répercussions du Brexit. On doit admettre que le processus de retrait de l’UE est complexe, qu’il y a plusieurs modèles dont la GB peut s’inspirer (Suisse, Norvégien, Islandais, Liechtenstein), et que le vote n’a pas d’effets légaux immédiats. En fait, le processus de sortie et de renégociation peut durer trois ans !

Je vous invite à prendre connaissance de ces deux articles afin d’être mieux informés sur les principales avenues conséquentes au retrait de la GB de l’UE.

Le 25 juin, je vous ai déjà présenté l’article de Perry qui a suscité beaucoup d’intérêt (Brexit: Legal Implications).

Aujourd’hui, je vous présente le texte de l’article de Witty (The Legal Consequences of Brexit) qui met l’accent sur les répercussions prévisibles qu’aura ce retrait sur le marché des capitaux, les fusions et acquisitions, les différends liés aux contrats, les lois antitrusts, les services financiers et les mesures de taxation.

On June 23, 2016, the UK electorate voted to leave the European Union. The referendum was advisory rather than mandatory and does not have any immediate legal consequences. It will, however, have a profound effect. With any next steps being driven by UK and EU politics, it is difficult to predict the future of the UK’s relationship with the EU. This post discusses the process for Brexit, the alternative models of relationship that the UK may seek to adopt, and certain implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax.

The process for exiting the EU

The treaties that govern the EU expressly contemplate a member state leaving. Under Article 50 of the Treaty on European Union, the UK must notify the European Council of its intention to withdraw from the EU. Once notice is given, the UK has two years to negotiate the terms of its withdrawal. Any extension of the negotiation period will require the consent of all 27 remaining member states. When to invoke the Article 50 mechanism is, therefore, a strategically important decision. In a statement announcing his intention to resign as Prime Minister of the UK, David Cameron stated that the decision to provide notice under Article 50 to the European Council should be taken by the next Prime Minister, who is expected to be in place by October 2016.

Waving United Kingdom and European Union Flag

Any negotiated agreement will require the support of at least 20 out of the 27 remaining member states, representing at least 65% of the EU’s population, and the approval of the European Parliament. If no agreement is reached or no extension is agreed, the UK will automatically exit the EU two years after the Article 50 notice is given, even if no alternative trading model or arrangement has been negotiated. The UK continues to be a member of the EU in the interim period, subject to all EU legislation and rules.

Alternative models of relationship

It is not clear what model of relationship the UK will seek to negotiate with the EU. In the run-up to the referendum, a number of options were suggested. Politicians in favor of withdrawing from the EU did not coalesce around a specific alternative. It is, therefore, unclear what model will ultimately be followed or whether any of the models could be achieved through the Article 50 process. The principal options are outlined below.

The Norwegian model. The UK might seek to join the European Economic Area, as Norway has. The UK would have considerable access to the internal market, i.e., the association of European countries trading with each other without restrictions or tariffs, including in financial services. The UK would have limited access to the internal market for agriculture and fisheries; and it would not benefit from or be bound by the EU’s external trade agreements. In addition, the UK would have to make significant financial contributions to the EU and continue to allow free movement of persons. It would also have to apply EU law in a number of fields, but the UK would no longer participate in policymaking at the EU level, and would be excluded from participation in the European Supervisory Authorities, the key architects of secondary legislation in the financial services sphere. To adopt this model, the UK would require the agreement of all 27 remaining EU member states, plus Iceland, Liechtenstein and Norway.

Negotiated bilateral agreements. Like Switzerland, the UK might seek to enter into various bilateral agreements with the EU to obtain access to the internal market in specific sectors (rather than the market as a whole, which would be the case under the Norwegian model). This model would likely require the UK to accept some of the EU’s rules on free movement of persons and comply with particular EU laws. Again, the UK would not participate formally in the drafting of those laws. The UK would also have to make financial contributions to the EU. Negotiating these bilateral agreements would be a difficult and time-consuming process. Switzerland, for instance, has negotiated more than 100 individual agreements with the EU to cover market access in different sectors. As a result of its complexity, it is unclear whether the EU would work with the UK to negotiate this model within the Article 50 timeframe.

Customs union. A customs union is currently in place between the EU and Turkey in respect of trade in goods, but not services. Under this model, Turkey can export goods to the EU without having to comply with customs restrictions or tariffs. Its external tariffs are also aligned with EU tariffs. The UK might seek to negotiate a similar arrangement with the EU. Under such an arrangement, and unless separately negotiated, UK financial institutions (including UK subsidiaries of US holding companies) would not be able to provide financial and professional services into the EU on equal terms with EU member state firms. For example, the EU passporting regime would not be available, meaning UK firms would have to seek separate licensing in each EU member state to provide certain financial services. Furthermore, in areas where the UK would have access to the internal market, it would likely be required to enforce rules that are equivalent to those in the EU. The UK would not be required to make any financial contributions to the EU, nor would it be bound by the majority of EU law.

Free trade agreement. The UK might seek to negotiate a free trade agreement with the EU, which would cover goods and services. To do so, it may look to the agreement that was recently agreed between the EU and Canada after seven years of negotiations. This agreement removes tariffs in respect of trade in goods, as well as certain non-tariff barriers in respect of trade in goods and services. Although the UK would not be required to contribute to the EU budget, its exports to the EU would have to comply with the applicable EU standards.

WTO membership. Under this model, the UK would not have any preferential access to the internal market or the 53 markets with which the EU has negotiated free trade agreements. Tariffs and other barriers would be imposed on goods and services traded between the UK and the EU, although, under WTO rules, certain caps would apply on tariffs applicable to goods, and limits would be imposed on particular non-tariff barriers applicable to goods and services. The UK would no longer be required to make any financial contributions to the EU, nor would it be bound by EU laws (although it would have to comply with certain rules in order to trade with the EU).

Implications for UK legislation

Regardless of which model it adopts, the UK will no longer be required to apply some (if not all) EU legislation. The UK has implemented certain EU laws (generally, EU directives) via primary legislation that will continue to be part of English law, unless these are amended or repealed. Other EU laws (generally, EU regulations) have direct applicability in the UK without the need for implementation, which means that these laws would fall away once the UK withdraws from the EU, unless they are transposed into UK law. Finally, thousands of statutory instruments have been made pursuant to the European Communities Act 1972. If this act is repealed upon the UK’s withdrawal from the EU, then, unless transposed into UK law, these statutory instruments will cease to apply as well. Therefore, the UK will have to perform a complex exercise to determine which EU laws and EU-derived laws it wishes to retain, amend or repeal, driven in part by the nature of any agreement reached with the EU during exit negotiations.

How may Brexit affect you?

The UK’s withdrawal from the EU will impact countless areas of the economy. The following section discusses a number of Brexit’s potential implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax. The extent to which these areas will be affected by the UK’s withdrawal from the EU will depend on the model of relationship that the UK and the EU adopt following the Brexit negotiations.

Capital Markets

The financial markets will likely continue to be volatile, particularly during the Brexit negotiations. This may affect the timing of transactions or their ability to be consummated.

The EU Prospectus Directive, which has been transposed into UK law, governs the content, format, approval and publication of prospectuses throughout the EU. Following eventual Brexit, the UK may no longer be bound by the Prospectus Directive and, thus, may seek to amend its prospectus legislation. For example, the Prospectus Directive provides that a company incorporated in an EU member state must prepare a prospectus if it wishes to offer shares to the public and/or request that shares be admitted to trading in the EU, subject to certain exemptions. The UK may wish to expand these exemptions, so that more offers can be made in the UK without a prospectus. Significantly, the Prospectus Directive also provides for the passporting of prospectuses throughout the EU. This means that a company can use a prospectus that has been approved in one member state to offer shares in any other EU member state. Without this passporting regime, UK companies will have to have their prospectuses approved both in the UK and at least one other member state where they wish to offer their shares, which may be particularly costly and time-consuming if the UK amends, for instance, the content requirements for prospectuses following Brexit, so that these no longer align with those prescribed by the Prospectus Directive.

During the Brexit negotiations, transaction documents may need to include specific Brexit provisions, for example to address the uncertainty around the model of relationship to be adopted.

M&A

As a result of ongoing uncertainty around the future of the UK’s relationship with the EU, a number of transactions with a UK nexus may be affected pending the Brexit negotiations.

Share sale transactions generally are not subject to much EU law or regulation. Asset and business sales, however, may be more affected by Brexit. For example, the regulations that protect the rights of employees on a business transfer stem from a European directive. When the UK withdraws from the EU, it may no longer be bound by this directive, and, therefore, the UK may wish to amend or repeal the regulations.

Contractual Disputes and Enforcement

As a member of the EU, the UK is part of a framework for deciding jurisdiction in disputes, recognizing judgments of other member states (and having its own courts’ judgments recognized and enforced throughout the EU) and deciding the governing law of contracts. Following Brexit, the UK may no longer be part of this framework which may affect jurisdiction and governing law choices in transaction documents.

Anti-trust

Currently, mergers that fall within the scope of the EU Merger Regulation can receive EU-wide clearance, which means that they are not also required to be cleared by individual member states. Following Brexit, mergers with a UK nexus may need to be reviewed by the UK’s Competition and Markets Authority separately.

More generally, UK anti-trust legislation is currently based on, and interpreted in line with, EU law, including decisions of the European Commission and the European Court of Justice. Given that UK courts may no longer be required to interpret national law consistently with EU law once the UK withdraws from the EU, businesses face the prospect of having to comply with divergent systems.

Financial Services

Much of the UK’s financial services regulation is based on EU law. This includes legislation such as the Markets in Financial Instruments Directive (MiFID), which regulates investment services and trading venues, the European Market Infrastructure Regulation, which regulates the derivatives market, the Alternative Investment Fund Managers Directive, which regulates hedge funds and private equity, and the Capital Requirements Directive and the Capital Requirements Regulation, which together represent the EU’s implementation of the international Basel III accords for the prudential regulation of banks. The Bank Recovery and Resolution Directive (“BRRD”) has been implemented into UK law via the Banking Act 2009, so the fundamental bank resolution regime should initially survive Brexit. That said, substantial further EU legislative work is expected in this area to modify BRRD (e.g., in relation to the implementation of the TLAC standard), so it is possible that the regimes could diverge rapidly after Brexit. In general with financial services legislation, an assessment will need to be made whether to align with EU legislation or diverge; the greater the divergence, the more the dual burdens on cross-border firms.

As mentioned above, the UK will likely not be part of the European Supervisory Authorities framework and will have no influence in the development of primary or secondary EU legislation and guidance. The UK has been a significant force in the area of financial services legislation and has driven the introduction of, for instance, the BRRD. The UK’s withdrawal may impact the legislative agenda and ultimately the quality of the legislation produced.

Financial institutions established in EEA member states can obtain a “passport” that allows them to access the markets of other EEA member states without being required to set up a subsidiary and obtain a separate license to operate as a financial services institution in those member states. Following Brexit, UK financial services institutions, including subsidiaries of US and other non-EU parent companies, would no longer be able to benefit from passporting (unless the UK were to join the EEA pursuant to the Norway option described above).

Although the UK will likely remain a member of the EU for a substantial period while negotiations are ongoing, there are pressing questions as to how the UK will engage with the ongoing legislative processes that affect the UK financial services industry. There are a number of areas where framework legislation has been passed already, but key secondary legislation is being developed or revised. These areas include the complete overhaul of MiFID and the Payment Services Directive. Even before the UK leaves the EU, we can expect to see a diminished role for the UK Government, UK regulators and UK market participants in shaping the detailed policies and procedures in those areas.

We expect larger financial institutions in the UK, or those based outside the UK that have significant operations in the UK, will wish to contribute to the negotiation process between the EU and UK. In particular, to the extent a unique model for trading relationships is proposed, these institutions may wish to engage with policymakers to minimize disruption and damage to their EU business model.

Tax

The EU has influenced many areas of the UK’s tax system. In some cases, this has been through EU legislation which applies directly in the UK; in other cases, EU rules have been adopted through UK legislation (for example, the UK’s VAT legislation is based on principles which apply across the EU); and, in still other cases, decisions of the European Court of Justice have either influenced the development of UK tax rules, or have prevented the UK’s tax authority from enforcing aspects of the UK’s domestic tax code. This complicated backdrop means that the tax impact of Brexit will be varied and difficult to predict.

Areas to watch include the following:

Direct tax: although the UK has an extensive double tax treaty network, not all treaties provide for zero withholding tax on interest and royalty payments. Accordingly, corporate groups should consider the extent to which existing structures rely on EU rules such as the Parent-Subsidiary Directive or the Interest and Royalties Directive to secure tax efficient payment flows. Similarly, corporate groups proposing to undertake cross border reorganisations would need to consider the extent to which existing cross-EU border merger tax reliefs will survive intact. It should also be borne in mind that, even if Brexit occurs, the UK is likely to continue vigorously supporting the OECD’s BEPS initiative such that there may well be considerable constraints and complexities associated with locating businesses outside the UK.

VAT: although VAT is an EU-wide tax regime, it seems inconceivable that VAT will be abolished. However, it is likely that, over time, there will be a divergence between UK VAT rules and EU VAT rules, including as to input VAT recovery on supplies made to non-UK customers. Additionally, UK companies may lose the administrative benefit of the “one stop shop” for businesses operating in Europe.

Customs duty: if the UK left the customs union, exports to and imports from EU countries may become subject to tariffs or other import duties (as well as additional compliance requirements).

Transfer taxes: it seems that the UK would, at least in principle, be able to (re)impose the 1.5% stamp duty/stamp duty reserve tax charge in respect of UK shares issued or transferred into a clearance or depositary receipt system. Accordingly, the position for UK-headed corporate groups seeking to list on the NYSE or Nasdaq may become less certain.

______________________________

*Ben Perry is a partner in the London office of Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell publication.

*Simon Witty is a partner in the Corporate Department at Davis Polk & Wardwell LLP. This post is based on a Davis Polk memorandum.

Nous avons déjà abordé l’importance d’inscrire un item « huis clos » à l’ordre du jour des réunions du conseil d’administration. Celui-ci doit normalement être à la fin de la réunion et comporter une limite de temps afin d’éviter que la réunion ne s’éternise… et que les membres de la direction (qui souvent attendent la fin de la rencontre) soient mieux informés.

Ensuite, le président du conseil d’administration (PCA) devrait rencontrer le président et chef de la direction (PCD) en privé, et dans les meilleurs délais, afin de rendre compte des résultats et de la portée du huis clos. Cette responsabilité du PCA est déterminante, car les dirigeants ont de grandes attentes et un souci eu égard aux discussions du huis clos.