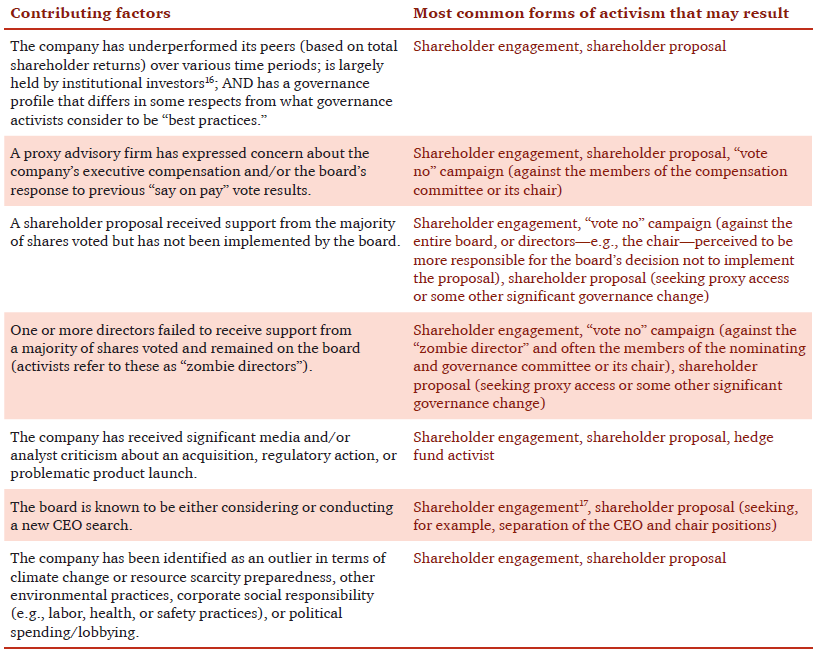

Dans ce billet, je vous propose une courte lecture suggérée par Chantal Rassart, associée | Chef de la gestion des connaissances en audit, de la firme Deloitte. Dans le numéro d’avril, un aperçu des nouveautés dans le domaine de la gouvernance d’entreprise, Chantal Rassart présente le point de vue de Heather Stockton, associée | Consultation, sur l’amélioration des pratiques des comités de ressources humaines du CA eu égard aux défis posés par la gestion des talents.

L’auteure insiste surtout sur l’importance cruciale de la mise en place d’un plan de formation à l’intention des hauts dirigeants. Les études montrent que les entreprises qui ont misées à fond sur le perfectionnement des dirigeants ont obtenu une performance financière significativement supérieure aux entreprises qui ont négligé cette acticité de développement des talents.

L’article présente également cinq questions que les comités de ressources humaines du CA devraient poser relativement à la gestion des talents.

Quel est votre point de vue à ce propos ? Voici un extrait de l’article en question.

Bonne lecture !

Nos prédictions se sont concrétisées

En 2011, nous avions prédit que nous assisterions à une baisse de l’importance accordée à la rémunération des cadres et à la relève du PDG et à une augmentation de l’importance accordée aux objectifs à long terme des entreprises en matière de gestion des talents et de diversité. Ces prédictions se sont bel et bien concrétisées. Il suffit de jeter un coup d’œil à ce qui est publié ou de discuter avec des administrateurs d’entreprises de toutes tailles et formes juridiques pour constater la place importante qu’occupent maintenant le leadership des futurs dirigeants et les talents dans les activités de gouvernance et de surveillance des conseils d’administration. Alors que nos regards se tournent vers l’avenir, nous constatons que les organisations devront faire face à de nouveaux défis et on s’attend à ce que les conseils d’administration adoptent une approche différente en matière de surveillance afin de les aider à répondre aux attentes de plus en plus élevées des clients, à la concurrence de plus en plus féroce, aux innovations rapides et à l’évolution accélérée des technologies.

Impératif d’affaires

L’attention accrue portée au perfectionnement des dirigeants a des incidences concrètes sur les indicateurs clés de performance de toutes les fonctions de l’organisation. Les organisations qui comptent au sein de leur équipe des dirigeants « de grande qualité » sont 13 fois plus susceptibles de dépasser leurs concurrents sur le plan notamment de la performance financière, de la qualité des produits et des services et de la fidélisation et de la mobilisation du personnel.

Une autre étude récente a examiné la performance d’entreprises durant une décennie en fonction du niveau d’effort consacré au perfectionnement des dirigeants. Les entreprises se situant dans la tranche des 15 % ayant consacré le plus d’efforts au perfectionnement des dirigeants ont accru leur capitalisation boursière de 122 pour cent, tandis que celles se situant dans la tranche des 15 % ayant consacré le moins d’efforts n’ont accru leur capitalisation boursière que de 37 pour cent.

Questions que les comités des ressources humaines devraient se poser

À la lumière de tous ces changements et compte tenu du rôle clair que joue le perfectionnement des talents dans la croissance de l’entreprise, les conseils d’administration devraient examiner continuellement comment leur entreprise se positionne par rapport à ses concurrents sur le plan des talents et comment elle parvient à répondre aux priorités d’affaires tandis que la concurrence s’intensifie. Le comité des ressources humaines peut contribuer au changement pour aider les chefs de la direction et des ressources humaines à diriger leur entreprise vers l’avenir. Outre les questions liées à la rémunération des dirigeants et à la relève du chef de la direction, les comités des ressources humaines devraient poser les cinq questions clés suivantes à la direction :

- Quelles qualités et connaissances les futurs hauts dirigeants et dirigeants actuels possèdent-ils? Dans quelle mesure sont-ils prêts à assumer la relève?

- Avez-vous en place un plan transition pour préparer les futurs candidats au poste de chef de la direction d’ici la fin du processus de relève?

- Le comité de gouvernance du conseil d’administration a-t-il passé en revue la composition du conseil à la lumière de la stratégie d’entreprise, de sa clientèle et des marchés dans lesquels l’entreprise évolue pour s’assurer que l’entreprise dispose des personnes adéquates pour diriger l’entreprise?

- Le comité des ressources humaines du conseil d’administration a-t-il discuté de la stratégie relative au travail de l’avenir lorsqu’il a approuvé la stratégie à moyen et à long terme et de la façon dont celle-ci pourrait changer les besoins immobiliers futurs, la nature du travail de votre entreprise et la façon dont vous appuierez vos dirigeants et employés dans le futur?

- Le comité des ressources humaines comprend-il les plans du chef des ressources humaines pour moderniser la fonction des ressources humaines et s’aligner sur le travail de l’avenir et votre stratégie d’affaires?

Si le chef de la direction et son équipe de direction ont une vision claire du « comment », vous avez alors les bons ingrédients pour continuer de vous démarquer de vos concurrents et d’obtenir des résultats durables. Une réponse négative à l’une des questions ci-dessus peut avoir une incidence sur la capacité de l’entreprise à atteindre les objectifs de sa stratégie d’affaires. Vos leaders et vos gens sont la seule chose que vos concurrents ne peuvent copier – tout le reste peut être automatisé, créé ou imité.