Plusieurs administrateurs et formateurs me demandent de leur proposer un document de vulgarisation sur le sujet de la gouvernance. J’ai déjà diffusé sur mon blogue un guide à l’intention des journalistes spécialisés dans le domaine de la gouvernance des sociétés à travers le monde. Il a été publié par le Global Corporate Governance Forum et International Finance Corporation (un organisme de la World Bank) en étroite coopération avec International Center for Journalists.

Je n’ai encore rien vu de plus complet et de plus pertinent sur la meilleure manière d’appréhender les multiples problématiques reliées à la gouvernance des entreprises mondiales. La direction de Global Corporate Governance Forum m’a fait parvenir le document en français le 14 février.

Ce guide est un outil pédagogique indispensable pour acquérir une solide compréhension des diverses facettes de la gouvernance des sociétés. Les auteurs ont multiplié les exemples de problèmes d’éthiques et de conflits d’intérêts liés à la conduite des entreprises mondiales.

On apprend aux journalistes économiques — et à toutes les personnes préoccupées par la saine gouvernance — à raffiner les investigations et à diffuser les résultats des analyses effectuées. Je vous recommande fortement de lire le document, mais aussi de le conserver en lieu sûr car il est fort probable que vous aurez l’occasion de vous en servir.

Vous trouverez ci-dessous quelques extraits de l’introduction à l’ouvrage. Bonne lecture !

« This Guide is designed for reporters and editors who already have some experience covering business and finance. The goal is to help journalists develop stories that examine how a company is governed, and spot events that may have serious consequences for the company’s survival, shareholders and stakeholders. Topics include the media’s role as a watchdog, how the board of directors functions, what constitutes good practice, what financial reports reveal, what role shareholders play and how to track down and use information shedding light on a company’s inner workings. Journalists will learn how to recognize “red flags,” or warning signs, that indicate whether a company may be violating laws and rules. Tips on reporting and writing guide reporters in developing clear, balanced, fair and convincing stories.

Three recurring features in the Guide help reporters apply “lessons learned” to their own “beats,” or coverage areas:

– Reporter’s Notebook: Advise from successful business journalists

– Story Toolbox: How and where to find the story ideas

– What Do You Know? Applying the Guide’s lessons

Each chapter helps journalists acquire the knowledge and skills needed to recognize potential stories in the companies they cover, dig out the essential facts, interpret their findings and write clear, compelling stories:

What corporate governance is, and how it can lead to stories. (Chapter 1, What’s good governance, and why should journalists care?)

How understanding the role that the board and its committees play can lead to stories that competitors miss. (Chapter 2, The all-important board of directors)

Shareholders are not only the ultimate stakeholders in public companies, but they often are an excellent source for story ideas. (Chapter 3, All about shareholders)

Understanding how companies are structured helps journalists figure out how the board and management interact and why family-owned and state-owned enterprises (SOEs), may not always operate in the best interests of shareholders and the public. (Chapter 4, Inside family-owned and state-owned enterprises)

Regulatory disclosures can be a rich source of exclusive stories for journalists who know where to look and how to interpret what they see. (Chapter 5, Toeing the line: regulations and disclosure)

Reading financial statements and annual reports — especially the fine print — often leads to journalistic scoops. (Chapter 6, Finding the story behind the numbers)

Developing sources is a key element for reporters covering companies. So is dealing with resistance and pressure from company executives and public relations directors. (Chapter 7, Writing and reporting tips)

Each chapter ends with a section on Sources, which lists background resources pertinent to that chapter’s topics. At the end of the Guide, a Selected Resources section provides useful websites and recommended reading on corporate governance. The Glossary defines terminology used in covering companies and corporate governance ».

Nous avons déjà abordé l’importance d’inscrire un item « huis clos » à l’ordre du jour des réunions du conseil d’administration. Celui-ci doit normalement être à la fin de la réunion et comporter une limite de temps afin d’éviter que la réunion ne s’éternise… et que les membres de la direction (qui souvent attendent la fin de la rencontre) soient mieux informés.

Ensuite, le président du conseil d’administration (PCA) devrait rencontrer le président et chef de la direction (PCD) en privé, et dans les meilleurs délais, afin de rendre compte des résultats et de la portée du huis clos. Cette responsabilité du PCA est déterminante, car les dirigeants ont de grandes attentes et un souci eu égard aux discussions du huis clos.

Plusieurs dirigeants et membres de conseil m’ont fait part de leurs préoccupations concernant la tenue des huis clos. Il y a des malaises dissimulés en ce qui a trait à cette activité ; il faut donc s’assurer de bien gérer la situation, car les huis clos peuvent souvent avoir des conséquences inattendues, voire contre-productives !

Ainsi, le huis clos :

(1) ne doit pas être une activité imprévue et occasionnelle inscrite à l’ordre du jour

(2) doit comporter une limite de temps

(3) doit être piloté par le PCA

(4) doit comporter un suivi systématique et

(5) doit se dérouler dans un lieu qui permet de préserver la confidentialité absolue des discussions.

J’insiste sur cette dernière condition parce que l’on a trop souvent tendance à la négliger ou à l’oublier, carrément. Dans de nombreux cas, la rencontre du conseil a lieu dans un local inapproprié, et les dirigeants peuvent entendre les conversations, surtout lorsqu’elles sont très animées…

Au début de la séance, les membres sont souvent insoucieux ; avec le temps, certains peuvent s’exprimer très (trop) directement, impulsivement et de manière inconvenante. Si, par mégarde, les membres de la direction entendent les propos énoncés, l’exercice peut prendre l’allure d’une véritable calamité et avoir des conséquences non anticipées sur le plan des relations interpersonnelles entre les membres de la direction et avec les membres du conseil.

L’ajout d’un huis clos à l’ordre du jour témoigne d’une volonté de saine gouvernance, mais, on le comprend, il y a un certain nombre de règles à respecter si on ne veut pas provoquer la discorde. Les OBNL, qui ont généralement peu de moyens, sont particulièrement vulnérables aux manquements à la confidentialité ! Je crois que dans les OBNL, les dommages collatéraux peuvent avoir des incidences graves sur les relations entre employés, et même sur la pérennité de l’organisation.

J’ai à l’esprit plusieurs cas de mauvaise gestion des facteurs susmentionnés et je crois qu’il vaut mieux ne pas tenir le bien-fondé du huis clos pour acquis.

Ayant déjà traité des bienfaits des huis clos lors d’un billet antérieur, je profite de l’occasion pour vous souligner, à nouveau, un article intéressant de Matthew Scott sur le site de Corporate Secretary qui aborde un sujet qui préoccupe beaucoup de hauts dirigeants : lehuis clos lors des sessions du conseil d’administration ou de certains comités.

L’auteur explique très bien la nature et la nécessité de cette activité à inscrire à l’ordre du jour du conseil. Voici les commentaires que j’exprimais à cette occasion.

«Compte tenu de la “réticence” de plusieurs hauts dirigeants à la tenue de cette activité, il est généralement reconnu que cet item devrait toujours être présent à l’ordre du jour afin d’éliminer certaines susceptibilités.

Le huis clos est un temps privilégié que les administrateurs indépendants se donnent pour se questionner sur l’efficacité du conseil et la possibilité d’améliorer la dynamique interne; mais c’est surtout une occasion pour les membres de discuter librement, sans la présence des gestionnaires, de sujets délicats tels que la planification de la relève, la performance des dirigeants, la rémunération globale de la direction, les poursuites judiciaires, les situations de conflits d’intérêts, les arrangements confidentiels, etc. On ne rédige généralement pas de procès-verbal à la suite de cette activité, sauf lorsque les membres croient qu’une résolution doit absolument apparaître au P.V.

La mise en place d’une période de huis clos est une pratique relativement récente, depuis que les conseils d’administration ont réaffirmé leur souveraineté sur la gouvernance des entreprises. Cette activité est maintenant considérée comme une pratique exemplaire de gouvernance et presque toutes les sociétés l’ont adoptée.

Notons que le rôle du président du conseil, en tant que premier responsable de l’établissement de l’agenda, est primordial à cet égard. C’est lui qui doit informer le PCD de la position des membres indépendants à la suite du huis clos, un exercice qui demande du tact!

Je vous invite à lire l’article ci-dessous. Vos commentaires sont les bienvenus».

Plusieurs OBNL sont à la recherche d’un document présentant les principes les plus importants s’appliquant aux organismes à buts charitables.

Le site ci-dessous vous mènera à une description sommaire des principes de gouvernance qui vous servirons de guide dans la gestion et la surveillance des OBNL de ce type. J’espère que ces informations vous seront utiles.

Vous pouvez également vous procurer le livre The Complete Principles for Good Governance and Ethical Practice.

What are the principles ?

The Principles for Good Governance and Ethical Practice outlines 33 principles of sound practice for charitable organizations and foundations related to legal compliance and public disclosure, effective governance, financial oversight, and responsible fundraising. The Principles should be considered by every charitable organization as a guide for strengthening its effectiveness and accountability. The Principles were developed by the Panel on the Nonprofit Sector in 2007 and updated in 2015 to reflect new circumstances in which the charitable sector functions, and new relationships within and between the sectors.

The Principles Organizational Assessment Tool allows organizations to determine their strengths and weaknesses in the application of the Principles, based on its four key content areas (Legal Compliance and Public Disclosure, Effective Governance, Strong Financial Oversight, and Responsible Fundraising). This probing tool asks not just whether an organization has the requisite policies and practices in place, but also enables an organization to determine the efficacy of those practices. After completing the survey (by content area or in full), organizations will receive a score report for each content area and a link to suggested resources for areas of improvement.

Voici une liste des 33 principes énoncés. Bonne lecture !

Ayant collaboré à la réalisation du volume « Améliorer la gouvernance de votre OSBL » des auteurs Jean-Paul Gagné et Daniel Lapointe, j’ai obtenu la primeur de la publication d’un chapitre sur mon blogue en gouvernance.

Le volume a paru en mars. Pour vous donner un aperçu de cette importante publication sur la gouvernance des organisations sans but lucratif (OSBN), j’ai eu la permission des éditeurs, Éditions Caractère et Éditions Transcontinental, de publier l’intégralité du chapitre 4 qui porte sur la composition du conseil d’administration et le recrutement d’administrateurs d’OSBL.

Je suis donc très fier de vous offrir cette primeur et j’espère que le sujet vous intéressera suffisamment pour vous inciter à vous procurer cette nouvelle publication.

Vous trouverez, ci-dessous, un court extrait de la page d’introduction du chapitre 4. Je vous invite à cliquer sur le lien suivant pour avoir accès à l’intégralité du chapitre.

Vous pouvez également feuilleter cet ouvrage en cliquant ici

Bonne lecture ! Vos commentaires sont les bienvenus.

__________________________________

Les administrateurs d’un OSBL sont généralement élus dans le cadre d’un processus électoral tenu lors d’une assemblée générale des membres. Ils peuvent aussi faire l’objet d’une cooptation ou être désignés en vertu d’un mécanisme particulier prévu dans une loi (tel le Code des professions).

L’élection des administrateurs par l’assemblée générale emprunte l’un ou l’autre des deux scénarios suivants:

1. Les OSBL ont habituellement des membres qui sont invités à une assemblée générale annuelle et qui élisent des administrateurs aux postes à pourvoir. Le plus souvent, les personnes présentes sont aussi appelées à choisir l’auditeur qui fera la vérification des états financiers de l’organisation pour l’exercice en cours.

2. Certains OSBL n’ont pas d’autres membres que leurs administrateurs. Dans ce cas, ces derniers se transforment une fois par année en membres de l’assemblée générale, élisent des administrateurs aux postes vacants et choisissent l’auditeur qui fera la vérification des états financiers de l’organisation pour l’exercice en cours.

La cooptation autorise le recrutement d’administrateurs en cours d’exercice. Les personnes ainsi choisies entrent au CA lors de la première réunion suivant celle où leur nomination a été approuvée. Ils y siègent de plein droit, en dépit du fait que celle-ci ne sera entérinée qu’à l’assemblée générale annuelle suivante. La cooptation n’est pas seulement utile pour pourvoir rapidement aux postes vacants; elle a aussi comme avantage de permettre au conseil de faciliter la nomination de candidats dont le profil correspond aux compétences recherchées.

Dans les organisations qui élisent leurs administrateurs en assemblée générale, la sélection en fonction des profils déterminés peut présenter une difficulté : en effet, il peut arriver que les membres choisissent des administrateurs selon des critères qui ont peu à voir avec les compétences recherchées, telles leur amabilité, leur popularité, etc. Le comité du conseil responsable du recrutement d’administrateurs peut présenter une liste de candidats (en mentionnant leurs qualifications pour les postes à pourvoir) dans l’espoir que l’assemblée lui fasse confiance et les élise. Certains organismes préfèrent coopter en cours d’exercice, ce qui les assure de recruter un administrateur qui a le profil désiré et qui entrera en fonction dès sa sélection.

Quant à l’élection du président du conseil et, le cas échéant, du vice-président, du secrétaire et du trésorier, elle est généralement faite par les administrateurs. Dans les ordres professionnels, le Code des professions leur permet de déterminer par règlement si le président est élu par le conseil d’administration ou au suffrage universel des membres. Comme on l’a vu, malgré son caractère démocratique, l’élection du président au suffrage universel des membres présente un certain risque, puisqu’un candidat peut réussir à se faire élire à ce poste sans expérience du fonctionnement d’un CA ou en poursuivant un objectif qui tranche avec la mission, la vision ou encore le plan stratégique de l’organisation. Cet enjeu ne doit pas être pris à la légère par le CA. Une façon de minimiser ce risque est de faire connaître aux membres votants le profil recherché pour le président, profil qui aura été préalablement établi par le conseil. On peut notamment y inclure une expérience de conseil d’administration, ce qui aide à réduire la période d’apprentissage du nouveau président et facilite une transition en douceur.

Voici le billet qui a attiré l’attention du plus grand nombre de lecteurs sur mon blogue depuis le début. Celui-ci a été publié le 30 octobre 2011. Je l’ai mis à jour afin que les nombreuses personnes intéressés par la gouvernance des OBNL puissent être mieux informées. L’Institut canadien des comptables agréés (ICCA) a produit des documents pratiques, pertinents, synthétiques et accessibles sur presque toutes les questions de gouvernance. Il est également important de noter que l’ICCA accorde une attention toute particulière aux pratiques de gouvernance des organismes sans but lucratif (OSBL = OBNL).

Ainsi, l’ICCA met à la disposition de ces organisations la collection 20 Questions pour les OSBL qui comprend des questions que les administrateurs d’organismes sans but lucratif (OSBL=OBNL) devraient se poser concernant des enjeux importants pour la gouvernance de ce type d’organismes. Ces documents sont révisés régulièrement afin qu’ils demeurent actuels et pertinents. Si vous avez des questions dans le domaine de la gouvernance des OBNL, vous y trouverez certainement des réponses satisfaisantes.Si vous souhaitez avoir une idée du type de document à votre disposition, vous pouvez télécharger le PDF suivant:

Le présent cahier d’information aidera les administrateurs d’OSBL à assumer leurs principales responsabilités à cet égard, soit : le recrutement, l’évaluation et la planification de la relève du directeur général ou du principal responsable au sein du personnel, l’établissement de la rémunération du directeur général et l’approbation de la philosophie de rémunération de l’organisme, ainsi que la surveillance des politiques et pratiques en matière de ressources humaines de l’organisme pris dans son ensemble.

20 Questions que les administrateurs d’organismes sans but lucratif devraient poser sur les risques a été rédigé pour aider les membres des conseils d’administration des OSBL à comprendre leur responsabilité à l’égard de la surveillance des risques.

20 Questions que les administrateurs des organismes sans but lucratif devraient poser sur l’obligation fiduciaire vise à aider les membres des conseils d’administration d’OSBL à comprendre leurs obligations fiduciaires et à s’en acquitter en leur fournissant un résumé des principes juridiques et des pratiques de pointe en matière de gouvernance pour ces organismes.

Ce cahier d’information décrit brièvement les principaux éléments de gouvernance des organismes sans but lucratif et des responsabilités des administrateurs. Il sera utile non seulement aux administrateurs éventuels, nouveaux et expérimentés, mais aussi aux comités des candidatures et aux organisateurs des séances d’orientation et de formation des administrateurs. Il est le premier d’une série de cahiers d’information destinés aux administrateurs d’organismes sans but lucratif et portant sur des aspects particuliers de la gouvernance de ces organisations.

La viabilité d’un organisme sans but lucratif, soit sa capacité de poursuivre et de financer ses activités année après année, est l’une des principales responsabilités du conseil. Les administrateurs doivent comprendre la raison d’être de l’organisme, les intérêts de ses parties prenantes et la façon dont il gère les risques auxquels il est exposé. Ils doivent également participer activement à l’élaboration de la stratégie de l’organisme et à son approbation.

Le document 20 Questions que les administrateurs des organismes sans but lucratif devraient poser sur le recrutement, la formation et l’évaluation des membres du conseil explore les défis que doivent relever les OSBL pour recruter les personnes aptes à siéger à leur conseil d’administration. Il souligne aussi l’importance qu’il convient d’accorder à la formation et au perfectionnement des administrateurs ainsi qu’à l’évaluation régulière du conseil et de ses membres.

Les administrateurs sont exposés à divers risques juridiques du fait de leur association avec une société et de leur obligation fiduciaire à son égard. De plus en plus, ils s’intéressent aux conditions de leur indemnisation et de leur assurance et se tournent vers leurs conseillers professionnels pour vérifier qu’ils disposent d’un niveau de protection adéquat. Il est recommandé aux conseils de s’intéresser activement aux dispositions prises par la société en ce qui concerne l’indemnisation et l’assurance relatives à la responsabilité civile des administrateurs et des dirigeants.

Voici une discussion très intéressante paru sur le groupe de discussion LinkedIn Board of Directors Society, et initiée par Jean-François Denault, concernant la nécessité de faire appel à un comité exécutif.

Je vous invite à lire les commentaires présentés sur le fil de discussion du groupe afin de vous former une opinion.

Personnellement, je crois que le comité exécutif est beaucoup trop souvent impliqué dans des activités de nature managériale.

Dans plusieurs cas, le CA pourrait s’en passer et reprendre l’initiative !

I’m looking for feedback for a situation I encountered.I am a board member for a non-profit. Some of us learned of an issue, and we brought it up at the last meeting for an update.We were told that it was being handled by the Executive Committee, and would not be brought up in board meetings.It is my understanding that the executive committee’s role is not to take issues upon themselves, but to act in interim of board meetings. It should not be discussing issues independently from the board.Am I correct in thinking this? Should all issues be brought up to the board, or can the executive committee handle situations that it qualifies as « sensitive »?

Depends whether it’s an operational matter I guess – e.g. a staffing issue below CEO/Director level. If it’s a matter of policy or strategy, or impacts on them, then the Board is entitled to be kept informed, surely, and to consider the matter itself.

Helping boards improve their performance and contributionI’ll respond a bit more broadly, Jean-François. While I am not opposed to the use of executive committees, a red flag often goes up when I conduct a governance review for clients and review their EC mandate and practices. There is a slippery slope where such committees find themselves assuming more accountability for the board’s work over time. Two classes of directors often form unintentionally as a result. Your situation is an example where the executive committee has usurped the board’s final authority. While I don’t recommend one approach, my inclination is to suggest that boards try to function without an executive committee because of the frequency that situations similar to the one you describe arise at boards where such committees play an active role. There are pros and cons, of course, for having these committees, but I believe the associated risk often warrants reconsideration of their real value and need.

I currently sit on the EC and have been in that role with other boards. Although I can see the EC working on projects as a subset of the board we Always go back to the full board and disclose those projects and will take items to the full board for approval. The board as a whole is accountable for decisions! There has to be transparency on the board! I found this article for you. http://www.help4nonprofits.com/BrainTeaser/BrainTeaser-Role_of_Executive_Committee.htm , which concurs to John’s comment. If used correctly the EC or a subset of the board can work on board issues more efficiently then venting through the full board, but they should always go back to the Full board for consideration or approval.

I have experienced couple of EB’s and unless the company is in deep financial or legal trouble for the most part the took away from the main board and in the whole worked ok but not great. If the board has over 10 to 15 board members it is almost a requirement but the board them is there for optics more than or effective and efficient decision making

Experienced CEO & Board member of Domestic and European companies.

I think Mr. Dinner, Mr. Molina, and Mr. Chapman summed it up beautifully:

– You cannot have two classes of Directors

– You have to have transparency and every Board member is entitled to the same information

– A Board of 10-15 members is inefficient and may need committees, but that does not change the fact that all Board members are entitled to have input into anything that the Board decides as a body.

– An Executive Committee is a sub-committee of the entire Board, not an independent body with extraordinary powers.

I agree with John, executive committees tend to be a slippery slope to bad governance. The board of directors has the responsibility of direction and oversight of the business or organization. If anything goes substantially wrong, the board of directors will also be accountable, legally. The rules of thumb for any and all committees is

– Committees must always be accountable to the board of directors, not the other way around.

– Committees must always have limits defined by the board of directors on authority and responsibility, and should have limits on duration.

– Committees should always have a specific reason to exist and that reason should be to support the board of directors in addressing it’s responsibilities.

Judging from the responses, we need to clearly define the context of what an Executive Committee is. Every organization can have it’s own function/view of what an Executive Committee is.

From my experience, an Executive Committee is under the CEO and reflects a group of trusted C-level executives that influence his decisions. I have had NO experience with Executive Boards other than the usual specific Board Committees dealing with specific realms of the organization.

So coming from this perspective, the Executive Committee is two steps down from the organizational pecking order and should be treated or viewed in that context..

President & CEO at Prevention Pharmaceuticals Inc.

I concur with Mr. James Clouser (above).

They should be avoided except in matters involving a performance question regarding C-Level Executive Board member, where a replacement may be sought.

James hit the nail on the head. Executive committees are a throwback to times when we didn’t have the communication tools we do now. They no longer have a reason for their existence. All directors, weather on a not for profit or a corporate board have equal responsibilities and legal exposures. There is no room or reason for a board within a board in today’s world.

My experience is; Board members have the last say in all policy issues- especially when it concerns operational matter. But in this case, where there is Executive Committee, what it sounds like is that, the organization in question has not clearly identified, nor delineated the roles of each body- which seem to have brought up the issue of ‘conflict’ in final decision- making. Often Executive Committees are created to act as a buffer or interim to the Board, this may sometime cause some over-lapping in executive decision-making.

My suggestion is for the organization to assess and evaluate its current hierarchy- clearly identify & define roles-benefits for creating and having both bodies, and how specific policies/ protocol would benefit the organization. In other words, the CEO needs to define the goals or benefits of having just a Board or having both bodies, and to avoid role conflict or over-lap, which may lead to confusion, as it seems to have been the case here.

CEO / PRESIDENT/BOARD OF DIRECTORS /PRIVATE EQUITY OPERATING PARTNER known for returning growth to stagnant businesses

The critical consideration for all board members is ‘ fiduciary accountability’ of all bod members. With that exposure , all bod members should be aware of key issues .

I think for large organizations, that executive committees still have an important role as many board members have a great deal going on and operational matters may come up from time to time that need to be handled in a judicial manner. While I think that the Executive committee has an important, at times critical role for a BOD, it is also critical that trust is built between the executive Committee and the BOD. This is only done when the executive committee is transparent, and pushes as many decisions that it can to the full board. If the committee does not have time to bring a matter to the full BOD, then they must convey to the BOD the circumstances why and reasoning for their decision. It is the executive committees responsibility to build that trust with the BOD and work hard to maintain it. All strategic decisions must be made by the full BOD. It sounds like you either have a communication failure, governance issue, or need work with your policies and procedures or a combination of issues.

Voici un document appréciable et remarquable qui illustre les principales données sur la gouvernance des sociétés américaines en les présentant sous forme chiffrée. Cet article est paru dans Harvard Law School forum par Ann Yerger, directrice générale du « Center for Board Matters » d’Ernst & Young.

L’auteur a compilé les données de plus de 3 000 sociétés publiques aux États-Unis, en les présentant selon les 5 indices les plus importants : S&P 500, S&P MidCap 400, S&P SmallCap 600, S&P 1500 et Russell 3000.

On se pose souvent des questions sur le profil de la gouvernance, notamment sur la composition des CA ; l’étude répond bien à ces interrogations et est facile à comprendre.

La présentation sous forme de tableaux et d’infographies est très explicite.

* Numbers based on all directorships in each index; gender diversity data represents average number of women directors on a board (and the percentage this represents)

Board Meetings and Size

Board meetings and size

S&P 500

S&P MidCap 400

S&P SmallCap 600

S&P 1500

Russell 3000

Board meetings

8

7

8

8

8

Board size

10.8

9.3

8.3

9.4

8.8

Board Leadership Structure

Board leadership structure*

S&P 500

S&P MidCap 400

S&P SmallCap 600

S&P 1500

Russell 3000

Separate chair/CEO

47%

57%

61%

55%

56%

Independent chair

28%

37%

42%

36%

36%

Independent lead director

54%

51%

41%

48%

40%

* Percentage based on portion of index; data through 31 Dec 2015

Board Elections

Board elections*

S&P 500

S&P MidCap 400

S&P SmallCap 600

S&P 1500

Russell 3000

Annual elections

91%

62%

55%

69%

60%

Majority voting in director elections

88%

60%

38%

62%

44%

* Percentage based on portion of index; data through 31 Dec 2015

Board and Executive Compensation

Board and executive compensation

S&P 500

S&P MidCap 400

S&P SmallCap 600

S&P 1500

Russell 3000

Independent directors

$291,987

$310,238

$171,120

$248,625

$226,053

CEO 3-yr average pay

$12.4 million

$6.2 million

$3.3 million

$7.1 million

$5.6 million

NEO 3-yr average pay

$4.7 million

$2.2 million

$1.2 million

$2.6 million

$2.1 million

Average pay ratio: CEO / NEO

2.6 times

2.8 times

2.8 times

2.7 times

2.7 times

* Numbers based on all directorships and executive positions in each index

Russell 3000 Opposition in Votes in Director Elections

Russell 3000: Opposition votes in director elections

Full year 2015

Year to date 2016

Total elections

17,808

15,529

Average opposition votes received (support)

4.0% (96.0%)

4.1% (95.9%)

Russell 3000: Opposition votes received by board nominees

Full year 2015

Year to date 2016

Directors with less than 80% support (% of nominees)

4.0%

4.0%

Number of directors

709

615

Directors with less than 50% support (% of nominees)

0.3%

0.3%

Number of directors

56

46

Say-on-Pay Proposals

Russell 3000: Say-on-Pay proposals voted

Full year 2015

Year to date 2016

Total proposals voted

2,194

1,850

Proposals with less than 70% support (% of proposals)

8.0%

6.7%

Number of proposals

175

124

Proposals with less than 50% support (% of proposals)

2.6%

1.5%

Number of proposals

56

27

Say-on-Pay proposals vote support

Full year 2015

Year to date 2016

S&P 500

92.0%

91.5%

S&P 1500

91.6%

91.8%

Russell 3000

91.3%

91.5%

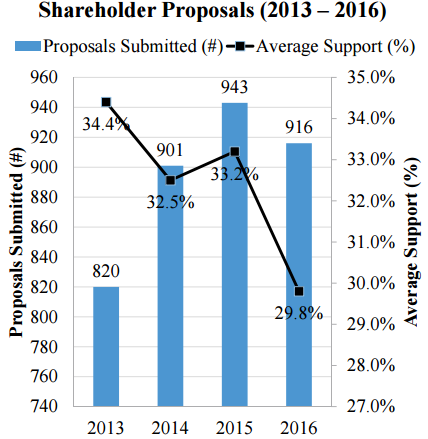

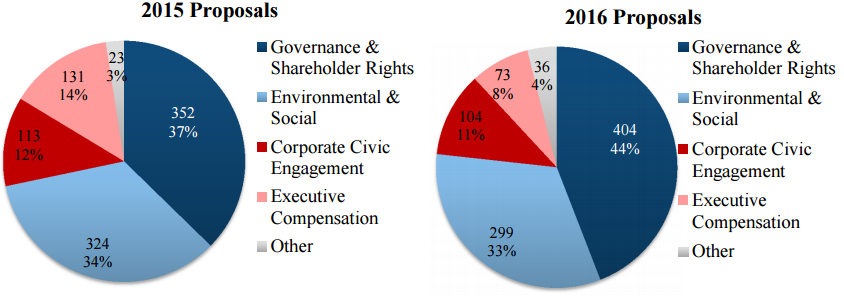

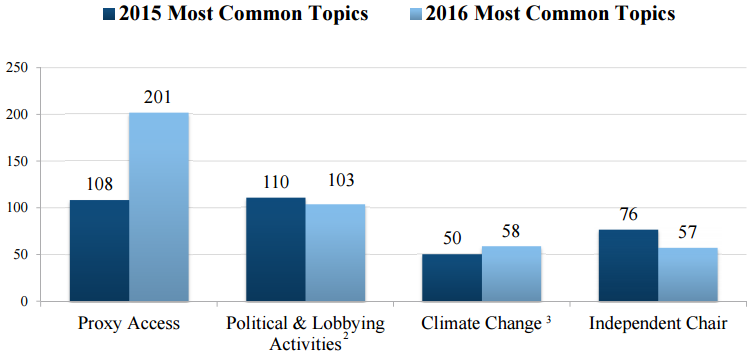

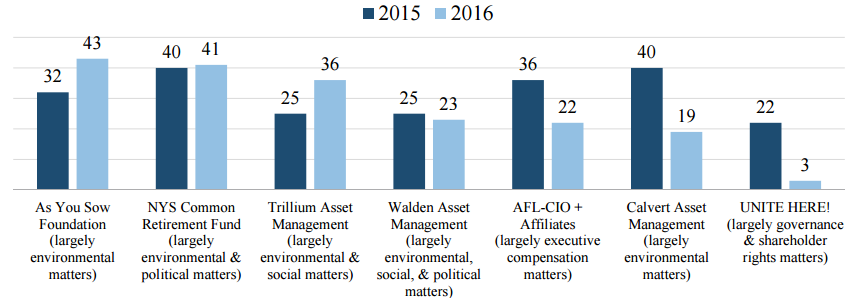

Shareholder Proposals

Shareholder proposal categories

Number voted

Portion of voted proposals

Environmental/social

199

39%

Board-focused

163

32%

Compensation

56

11%

Anti-takeover/strategic

86

17%

Routine/other

7

1%

All

511

100%

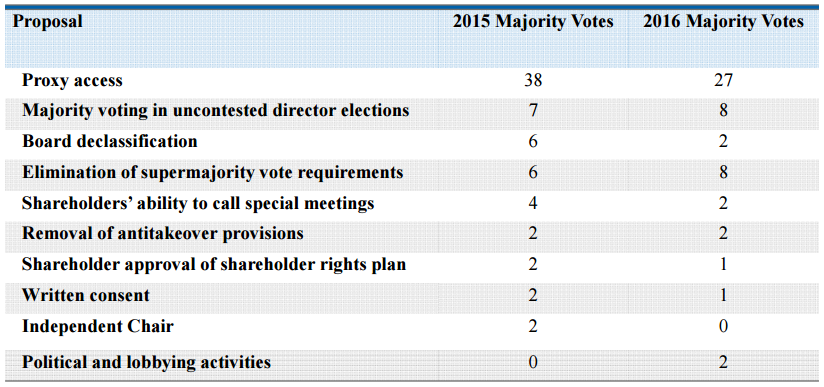

Top shareholder proposals by vote support*

Average support

Eliminate Classified Board

74.7%

Adopt Majority Vote to Elect Directors

68.5%

Eliminate Supermajority Vote

61.0%

Adopt/Amend Proxy Access

51.8%

Allow Shareholders to Call Special Meeting

41.9%

Allow Shareholders to Act by Written Consent

39.7%

Increase/Report on Board Diversity

35.4%

Address Corporate EEO/Diversity

32.5%

Appoint Independent Board Chair

29.2%

Review/Report on Climate Related Risks

28.6%

* Based on topics where at least 5 shareholder proposals went to a vote

Top shareholder proposals by number voted*

Number voted

Adopt/Amend Proxy Access

76

Appoint Independent Board Chair

47

Review/Report on Lobbying Activities

40

Review/Report on Political Spending

29

Address Human Rights

23

Adopt Majority Vote to Elect Directors

22

Limit Post-Employment Executive Pay

21

Report on Sustainability

20

Allow Shareholders to Call Special Meeting

18

Review/Report on Climate Related Risks

18

* Based on topics where at least 5 shareholder proposals went to a vote

Voici un article de James McRitchie, publié dans Corporate governance, qui commente succinctement le dernier volume de Richard Leblanc.

Comme je l’ai déjà mentionné dans un autre billet, le livre de Richard Leblanc est certainement l’un des plus importants ouvrages (sinon le plus important) portant sur la gouvernance du conseil d’administration.

Je vous encourage à prendre connaissance de la revue de M. McRitchie, et à vous procurer cette bible.

I continue my review of The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board Member. With the current post, I provide comments on Part 2 of the book, What Makes for a Good Board? See prior introductory comments and those on Part 1. I suspect the book will soon be the most popular collection of articles of current interest in the field of corporate governance.

The Handbook of Board Governance: Director Independence, Competency, and Behavior

Dr. Richard Leblanc‘s chapter focuses on the above three elements that make an effective director. Regulations require independence but not industry expertise; both are important elements. Leblanc cites ways director independence is commonly compromised and how independence ‘of mind’ can be enhanced. He then applies most of the same principles to choosing external advisors. Throughout the chapter he employees useful exhibits that reinforce the text with bullet points, tables, etc. for quick reference.

Director competency matrices have become relatively commonplace, although not ubiquitous. Leblanc not only provides a sample and scale, he reminds readers that being a CEO is an experience, not a competency and experience is not synonymous with competency. A sample board diversity matrix is also presented with measurable objectives for age, gender, ethnicity and geography.

Director behavior is the last topic in Leblanc’s chapter. Of course, each board needs to define how its directors are to act, subject to self- and peer-assessment but Leblanc’s ten behaviors is a good starting place:

Independent Judgment

Integrity

Organizational Loyalty

Commitment

Capacity to Challenge

Willingness to Act

Conceptual Thinking Skills

Communication Skills

Teamwork Skills

Influence Skills

That’s just one list of many. Leblanc’s examples and commentary on each adds color and depth. Under the UK’s Corporate Governance Code, director reviews are required to be facilitated by an independent provider every two or three years. Great advice for boards elsewhere as well. As Leblanc reminds readers:

« Proxy access and other renewal reforms are the direct result of boards steadfastly resisting director recruitment on the basis of competencies, the removal of underperforming directors; and the lack of boardroom refreshment, diversification, and renewal ».

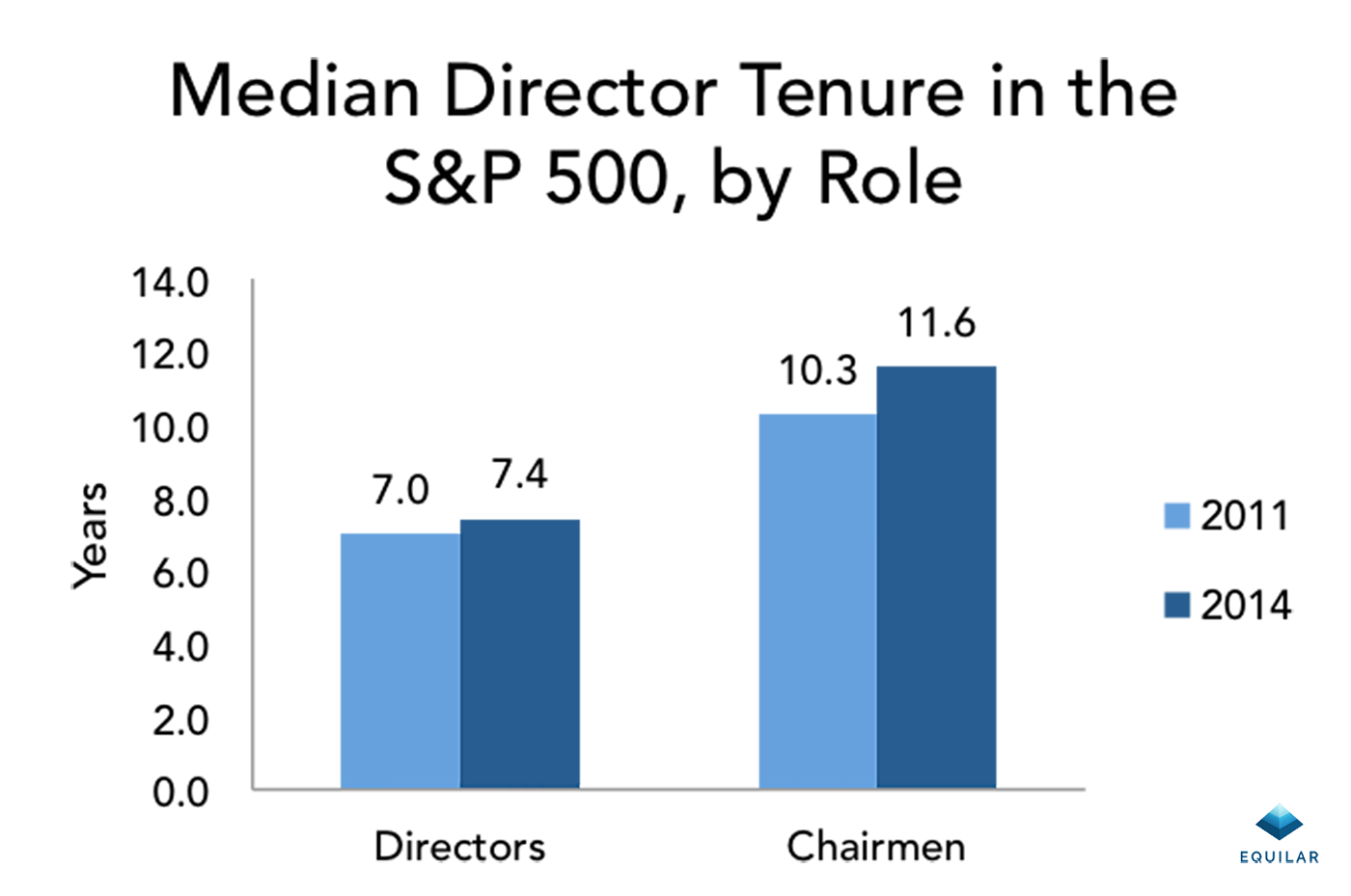

La littérature en gouvernance aborde de plus en plus fréquemment les sujets du renouvellement des membres du conseil d’administration, de l’âge et de la durée des mandats en les associant à l’indépendance des administrateurs.

Plusieurs investisseurs institutionnels et firmes de conseil en votation ont inclus le facteur de longévité des administrateurs parmi les éléments à considérer dans l’évaluation du rôle des administrateurs indépendants.

David A. Katz*, associé de la firme Wachtell, Lipton, Rosen & Katz, a publié un article dans le Harvard Law School Forum, qui présente clairement la problématique liée à cet enjeu ; il conclut qu’il n’y a pas de lien de causalité entre le nombre d’années de présence à un conseil et l’indépendance des administrateurs.

Le travail du comité de gouvernance, notamment les plans de relève des administrateurs et l’évaluation des performances des administrateurs sont les meilleurs gages d’une saine indépendance.

In conclusion, we believe that the focus on director tenure is generally misplaced, and that investors would be better served by directly addressing any underlying issues and concerns rather than using board tenure as a proxy. Appropriate board refreshment and director succession plans, accompanied by robust annual director evaluations, are the best means for public companies to ensure that board members are independent, engaged and productive and that they have the relevant experience and expertise to assist the company as it executes on its strategy.

Director tenure, or “board refreshment,” is a corporate governance flashpoint at the moment for institutional investors, boards of directors and proxy advisory firms. One of the top takeaways from the 2016 proxy season, according to EY, is that “board composition remains a key focus—with director tenure and board leadership coming under increased investor scrutiny.” [1] Many investors and shareholder activists view director tenure as integral to issues of board composition, succession planning, diversity, and, most of all, independence.

Fortunately, term limits for directors is an idea that, in the United States, appears to have more appeal in theory than in practice. Term limits are in place at only three percent of S&P 500 companies—a decrease from five percent in 2010. Although the sample size is small, term limits in this group range from 10 to 20 years. [2] And, despite the seeming popularity of term limits among investors, during the 2016 proxy season, there were no shareholder proposals regarding director term limits, and during the 2015 proxy season, there were only two. [3] The small number of boards that have mandatory term limits indicates that the vast majority of directors—though they may appreciate the arguments in favor of term limits—determine, as a practical matter, that director tenure is best evaluated on a case-by-case basis, both at the company level and at the level of individual directors. The best way to achieve healthy board turnover is not term limits or retirement ages but a robust director evaluation process combined with an ongoing director succession process.

Board Tenure and Director Independence

For some investors, director term limits represent another avenue to address concerns over director independence. Firmly entrenched as an ideal, yet subject to many interpretations, “director independence” remains the linchpin of good corporate governance. Rules on independence generally aim to ensure that directors deemed “independent” have no conflicts of interest with respect to their service on the board, through financial investments, professional or personal connections, recent employment with the company, and the like. It is considered particularly important that members of the key board committees—audit, nominating/governance, and compensation—have no apparent conflicts that would cast doubt on their ability to exercise, or their likelihood of exercising, their business judgment in an objective and professional manner. Notably, having a significant investment in the company as a stockholder (other than a controlling stockholder), generally does not affect a director’s independence under the SEC or stock exchange rules, even though such directors may have different interests than other shareholders.

Shareholder groups and institutional investors have begun to incorporate director tenure considerations into their company evaluations and voting recommendations. Globally, mandatory term limits and comply-or-explain regimes are being implemented as the issue becomes increasingly high-profile worldwide. [4] Notably, a 2016 Spencer Stuart global survey of 4,000 directors in 60 different countries indicated that directors in private companies are significantly less likely to be subject to term limits. [5] It is telling that, absent the pressures faced by public companies, private boards clearly choose to maintain their latitude regarding board composition decisions.

One source of these pressures may be that in recent years, the average age of directors has increased, and mandatory director retirement ages have either been increased or eliminated at many public companies. Public companies naturally wish to retain productive, experienced directors—many of whom are staying active later in life than their predecessors in previous generations—as well as a recognition that age is not itself generally a limiting fact for a good director. Companies with robust annual director evaluation programs should not need a mandatory retirement age to weed out poorly performing directors. Similarly, younger directors need to undergo the same evaluation on an annual basis to ensure that their performance is up to par.

Long service as an independent director on a board is viewed by some as creating a conflict on the basis that extended tenure creates too close a relationship among longstanding board members and chief executives. Accordingly, a number of influential investors and proxy advisors include director tenure as a consideration in determining their proxy voting policies. CalPERS, for example, updated its proxy voting policy for 2016 to assert that “director independence can be compromised at twelve years of service,” and that after such time, companies should conduct “rigorous evaluations to either classify the director as non-independent or provide a detailed annual explanation of why the director can continue to be classified as independent.” [6]

Equating long tenure with a lack of independence is problematic in several ways. As a statistical matter, the average tenure of CEOs in the S&P 500 is 7.4 years, an increase of less than one year in the last decade. [7] Average director tenure in the S&P 500, meanwhile, has remained stable in recent years at roughly 8.5 years. [8] Long coterminous service of directors and chief executives would appear to be the exception rather than the norm. Moreover, long-serving directors are often the ones that have accrued the expertise and standing to influence and effectively oversee a long-serving or otherwise powerful CEO. Institutional investors surveyed by EY last year expressed reservations about director term limits, indicating their concern that mandatory limits do not adequately account for the valuable contributions of experienced directors. Some of these investors felt that a guideline, rather than a strict requirement, as to director tenure could provide a useful starting point for a discussion of board refreshment. [9]

Some investors and academics have gone so far as to propose that, after a certain length of tenure, directors should be considered not independent for the purposes of serving on the audit and compensation committees. [10] In our view, this would be counterproductive in important ways. First, it would limit the usefulness of a board’s most experienced directors by precluding them from serving on the key committees where their expertise may be most valuable. Second, such a ban would impinge upon the board’s business judgment and discretion by micromanaging the very organizational structure of the board itself. Ultimately, if a company’s shareholders have so little confidence in their directors that they feel the need to intervene in board committee assignments, they could not possibly trust the directors to supervise the company generally. Director tenure is an issue at once too picayune—as it is well within the discretion of the board—and too significant—as it affects the board’s latitude to do its job effectively—to be determined by shareholders or outside groups rather than by directors themselves.

We believe that many investors as well as proxy advisory firms are looking at this issue the wrong way. Rather than focusing on simply the longest tenured directors, we believe that it is the average tenure of the entire board that is most relevant. This is a more meaningful metric for evaluating board refreshment and director succession.

Boards Must Maintain Flexibility

Boards should, as a general matter, annually perform a substantive self-evaluation, in which director tenure is one element to consider. The directors should review not only the contributions of current directors, but also the ongoing needs of the board. New directors will be essential as the company undergoes natural changes in strategy and management, and as the board ensures that it creates opportunities to benefit from the contributions of directors with diverse professional and personal backgrounds. A significant amount of director turnover happens as a matter of course: For instance, EY estimates that nearly 20 percent of directors in the S&P 100 are set to retire in the next five years. [11] As an indication that the board is aware of tenure concerns among some investor groups, companies may choose to set forth the average tenure of non-management directors as a separate item in their proxy statement disclosures. [12] As noted above, in our view, average tenure is a more appropriate measure.

When considering the adoption of mandatory term or age limits, boards should recognize that waiving the limits often requires disclosure and may result in negative publicity and even negative vote recommendations. Glass Lewis, for example, does not encourage the adoption of what it calls “inflexible rules” regarding director terms; indeed, its 2016 proxy guidelines endorse the position that length of tenure and age are not correlated with director performance. That said, its policy is to consider recommending a vote against directors on the nominating and/or governance committees if the board waives the company’s mandatory term limit absent explanations and special circumstances. [13]

Directors would be well advised to consider the approach of BlackRock, whose policy is aimed at the substantive issues to which director tenure is only superficially related. BlackRock focuses not on the number of years of service but instead on “board responsiveness to shareholders on board composition concerns, evidence of board entrenchment, insufficient attention to board diversity, and/or failure to promote adequate board succession planning.” [14]

BlackRock sensibly observes in its stated policy that long board tenure does not necessarily impair director independence.

As both Glass Lewis and BlackRock note in their policy statements, term limits can be a tool for boards that are having difficulty in moving long-serving members off the board. Though negotiations of this nature indeed can be fraught, boards are far better served in the long term by working their way through the issue and preserving their own discretion rather than implementing a rule that, while helpful in one instance, may prove undesirable in the future.

In conclusion, we believe that the focus on director tenure is generally misplaced, and that investors would be better served by directly addressing any underlying issues and concerns rather than using board tenure as a proxy. Appropriate board refreshment and director succession plans, accompanied by robust annual director evaluations, are the best means for public companies to ensure that board members are independent, engaged and productive and that they have the relevant experience and expertise to assist the company as it executes on its strategy.

Endnotes:

[1] EY Center for Board Matters, “Four Takeaways from Proxy Season 2016,” discussed on the Forum here. (go back)

[3] The first was at Barnwell Industries, Inc., and it did not come to a vote. The second was at Costco Wholesale Corporation, and it received supporting votes from less than 5 percent of the outstanding shares. (go back)

[4] See David A. Katz & Laura A. McIntosh, “Renewed Focus on Director Tenure,” May 22, 2014, discussed on the Forum here, for a discussion of viewpoints on director tenure in the United States and abroad. (go back)

[5] Spencer Stuart 2016 Global Board of Directors Survey, at 9, available at https://www.spencerstuart.com/research-and-insight/2016-global-board-of-directors-survey. The survey found that 39 percent of public companies have mandatory term limits, as opposed to 30 percent of private companies. In addition, 33 percent of public companies had mandatory retirement ages, as opposed to 12 percent of private companies. (go back)

*David A. Katz is a partner and Laura A. McIntosh is a consulting attorney at Wachtell, Lipton, Rosen & Katz. The following post is based on an article by Mr. Katz and Ms. McIntosh that first appeared in the New York Law Journal. The views expressed are the authors’ and do not necessarily represent the views of the partners of Wachtell, Lipton, Rosen & Katz or the firm as a whole. Related research from the Program on Corporate Governance includes The “New Insiders”: Rethinking Independent Directors’ Tenure by Yaron Nili (discussed on the Forum here).

L’étude de David Larcker*, professeur de comptabilité à la Stanford Graduate School of Business, publié dans le forum du Harvard Law School, examine la controverse eu égard à la combinaison des fonctions de PDG et de président du conseil. Environ 50 % des grandes sociétés américaines sont présidées par un administrateur indépendant, comparativement à 23 % il y a 15 ans.

Toute la question du bien-fondé de la dualité des rôles PDG/Chairman est encore ambiguë, même si les experts de la gouvernance et les actionnaires activistes sont généralement d’accord avec la séparation des fonctions.

L’auteur a procédé à une enquête auprès des 100 plus grandes sociétés ainsi qu’auprès des 100 plus petites entreprises du Fortune 1000, afin d’étudier l’évolution de ce phénomène au cours des 20 dernières années.

Il ressort de ces études que les grandes sociétés sont beaucoup plus incitées (par les actionnaires) à séparer les deux fonctions que les entreprises plus petites (57 % vs 3 %).

En fait, les 100 plus petites entreprises du Fortune 1000 ne sont pas ciblées par les actionnaires pour opérer ce changement.

In recent years, companies have consistently moved toward separating the chairman and CEO roles. According to Spencer Stuart, just over half of companies in the S&P 500 Index are led by a dual chairman/CEO, down from 77 percent 15 years ago. In theory, an independent chairman improves the ability of the board of directors to oversee management. However, separation of the chairman and CEO roles is not unambiguously positive, and there is little research support for requiring a separation of these roles. Still, shareholder activists and many governance experts remain active in pressuring companies to divide their leadership structure.

Given the controversy over chairman/CEO duality, we examined in detail the leadership structures of publicly traded corporations and the circumstances under which they are changed. Our sample includes the 100 largest and 100 smallest companies in the Fortune 1000 in 2016. The measurement period includes the 20-year period 1996-2015.

We find that board leadership structures are not stable. Only a third (34 percent) of companies made no changes during the entire 20-year measurement period. Slightly under half of these consistently maintained separate chairman and CEO positions (such as Costco, Intel, and Walgreens); slightly more than half of these consistently combined them (such as Amazon, Berkshire Hathaway, and ExxonMobil). Still, these companies are the exception rather than the rule. It is significantly more likely that a company makes at least one change to board leadership structure (combination or separation) over time. On average, companies made 1.7 changes, or approximately 1 change every 12 years. Changes are more frequent among large companies (2.2 changes, on average) than smaller companies (1.3 changes). In both cases, companies are slightly more likely to separate the roles than to combine them.

Most separations occur during the succession process, with the former CEO, founder, or other officer continuing to serve as chair on either a temporary or permanent basis. Of the 171 separations in our sample, 134 (78 percent) are associated with an orderly succession. This is true of both small and large companies. However, large companies are significantly more likely to separate the roles temporarily, whereas smaller companies are more likely to do so permanently.

Approximately a quarter (22 percent) of separations are not part of an orderly succession. Nine percent follow an abrupt resignation of the CEO, 6 percent a governance issue (such as accounting restatement or CEO scandal), 3 percent a merger, 2 percent a shareholder vote, and 2 percent are required of the company as part of a government bailout.

The decision to combine the chairman and CEO roles tends to be more uniform. The vast majority of combinations (91 percent) involve an orderly succession at the top. Only 9 percent are associated with a merger, sudden resignation, or governance-related issue. In 90 percent of combinations, the current CEO is given the additional title of chair; in 10 percent of cases, a new CEO is recruited to become dual chair/CEO.

Most interesting, perhaps, is the frequency with which companies “permanently” separate the leadership roles only to recombine them at a later date. Slightly over one-third (34 percent) of companies in our sample permanently separated the chairman and CEO roles and later recombined them during the 20-year measurement period. Best Buy split the roles for nearly 13 years when founder and chairman Richard Schultze stepped down as CEO in 2002; Schultze eventually resigned from the board and when his successor as chairman retired in 2015, then-CEO Hubert Joly was given the additional title of board chair. The company gave no public explanation of its decision to recombine the roles. Bank of America and Walt Disney both separated the chairman and CEO roles following shareholder votes and subsequently recombined them 5 and 9 years later, respectively, under different management. In both cases, the board justified the decision to recombine as rewarding the successful leadership of the current CEO.

In the cases of Bank of America and Walt Disney, the decisions to recombine the roles were highly controversial. Across the entire sample, however, shareholder response was unexpectedly varied. Only 34 percent of the companies that separated and recombined the chairman and CEO roles were targeted by shareholder-sponsored proxy proposals to require separation. Average support for these proposals was 33 percent, not significantly different from companies that consistently maintain a dual chairman/CEO structure (34 percent support) or that separate the roles temporarily during succession (36 percent support). It was also not significantly different from the average support across the total universe of companies that face shareholder-sponsored proposals requiring separation (32 percent).

Finally, it is interesting to note that pressure to separate the chairman and CEO roles seems to center almost exclusively on large companies. Only 3 of the 95 small companies in our sample were the target of a shareholder proposal to require an independent chairman over the entire 20-year measurement period, even though their board leadership structures are not significantly different from those of larger corporations. By contrast, a majority (56 out of 92) of large companies were targeted at least once. This suggests that the companies that shareholders target to advocate for independent board leadership might not necessarily be those with the most egregious governance problems but instead those that are the most visible public targets.

*David Larcker is Professor of Accounting at Stanford Graduate School of Business. This post is based on a paper authored by Professor Larcker and Bryan Tayan, Researcher with the Corporate Governance Research Initiative at Stanford Graduate School of Business.

La très grande majorité des gens croient que la rémunération des dirigeants est associée à une performance supérieure de leurs sociétés. Ce n’est pas ce que l’étude récemment publiée dans le Wall Street Journal par Theo Francis* tend à démontrer.

L’étude de la firme de recherche MSCI auprès de 800 CEO indique que, depuis 2006, les CEO les moins bien payés produisent des rendements supérieurs pour leurs firmes ! La différence est assez significative.

Je vous laisse le soin de lire ce compte rendu et de me donner vos impressions.

The best-paid CEOs tend to run some of the worst-performing companies and vice versa—even when pay and performance are measured over the course of many years, according to a new study.

The analysis, from corporate-governance research firm MSCI, examined the pay of some 800 CEOs at 429 large and midsize U.S. companies during the decade ending in 2014, and also looked at the total shareholder return of the companies during the same period.

MSCI found that $100 invested in the 20% of companies with the highest-paid CEOs would have grown to $265 over 10 years. The same amount invested in the companies with the lowest-paid CEOs would have grown to $367. The report is expected to be released as early as Monday.

The results call into question a fundamental tenet of modern CEO pay: the idea that significant slugs of stock options or restricted stock, especially when the size of the award is also tied to company performance in other ways, helps drive better company performance, which in turn will improve results for shareholders. Equity incentive awards now make up 70% of CEO pay in the U.S.

“The highest paid had the worst performance by a significant margin,” said Ric Marshall, a senior corporate governance researcher at MSCI. “It just argues for the equity portion of CEO pay to be more conservative.”

Executive-pay critics have long said pay and performance could be better aligned, and in June, The Wall Street Journal reported little relationship between one-year pay and performance figures for the S&P 500. Most longer-term analyses have used considered three or five years at a time.

The MSCI study compared 10-year total shareholder return—stock appreciation plus dividends—and cumulative total CEO pay as reported in proxy-filing summary-compensation tables.

The study also examined pay and performance among companies within the same broad economic sectors and found similar results: The top-paid half of CEOs in a sector tended to run companies that performed worse than their peers, while the lower-paid half tended to outperform.

“Whether you look at the entire group or adjust by market-cap and sector, you really get very similar results,” Mr. Marshall.

One possible factor driving the results, the researchers concluded: Annual pay reviews and proxy disclosures, which discourage boards and executives from focusing on longer-term results. The report recommended that the Securities and Exchange Commission require disclosure of cumulative incentive pay over long periods, to help illustrate a CEO’s pay relative to longer-term performance.

__________________________

*Theo Francis covers corporate news for The Wall Street Journal from Washington, D.C., and specializes in using regulatory documents to write about complex financial, business, economic, legal and regulatory issues.

Voici une « lettre ouverte » publiée sur le forum de la Harvard Law School on Corporate Governance par un groupe d’éminents dirigeants de sociétés publiques (cotées) qui présente les principes de la saine gouvernance : « The Commonsense Principles of Corporate Governance »*.

Les principes sont regroupés en plusieurs thèmes :

La composition du CA et la gouvernance interne

Composition

Élection des administrateurs

Nomination des administrateurs

Rémunération des administrateurs et la propriété d’actions

Structure et fonctionnement des comités du conseil

Nombre de mandats et âge de la retraite

Efficacité des administrateurs

Responsabilités des administrateurs

Communication des administrateurs avec de tierces parties

Activités cruciales du conseil : préparer les ordres du jour

Le droit des actionnaires

La reddition de comptes et la divulgation des activités

Le leadership du conseil

La planification de la relève managériale

La rémunération de la direction

Le rôle du gestionnaire des actifs des clients dans la gouvernance des sociétés

Bonne lecture ! Vos commentaires sont les bienvenus.

The following is a series of corporate governance principles for public companies, their boards of directors and their shareholders. These principles are intended to provide a basic framework for sound, long-term-oriented governance. But given the differences among our many public companies—including their size, their products and services, their history and their leadership—not every principle (or every part of every principle) will work for every company, and not every principle will be applied in the same fashion by all companies.

I. Board of Directors—Composition and Internal Governance

a. Composition

Directors’ loyalty should be to the shareholders and the company. A board must not be beholden to the CEO or management. A significant majority of the board should be independent under the New York Stock Exchange rules or similar standards.

All directors must have high integrity and the appropriate competence to represent the interests of all shareholders in achieving the long-term success of their company. Ideally, in order to facilitate engaged and informed oversight of the company and the performance of its management, a subset of directors will have professional experiences directly related to the company’s business. At the same time, however, it is important to recognize that some of the best ideas, insights and contributions can come from directors whose professional experiences are not directly related to the company’s business.

Directors should be strong and steadfast, independent of mind and willing to challenge constructively but not be divisive or self-serving. Collaboration and collegiality also are critical for a healthy, functioning board.

Directors should be business savvy, be shareholder oriented and have a genuine passion for their company.

Directors should have complementary and diverse skill sets, backgrounds and experiences. Diversity along multiple dimensions is critical to a high-functioning board. Director candidates should be drawn from a rigorously diverse pool.

While no one size fits all—boards need to be large enough to allow for a variety of perspectives, as well as to manage required board processes—they generally should be as small as practicable so as to promote an open dialogue among directors.

Directors need to commit substantial time and energy to the role. Therefore, a board should assess the ability of its members to maintain appropriate focus and not be distracted by competing responsibilities. In so doing, the board should carefully consider a director’s service on multiple boards and other commitments.

b. Election of directors

Directors should be elected by a majority of the votes cast “for” and “against/withhold” (i.e., abstentions and non-votes should not be counted for this purpose).

c. Nominating directors

Long-term shareholders should recommend potential directors if they know the individuals well and believe they would be additive to the board.

A company is more likely to attract and retain strong directors if the board focuses on big-picture issues and can delegate other matters to management (see below at II.b., “Board of Directors’ Responsibilities/Critical activities of the board; setting the agenda”).

d. Director compensation and stock ownership

A company’s independent directors should be fairly and equally compensated for board service, although (i) lead independent directors and committee chairs may receive additional compensation and (ii) committee service fees may vary. If directors receive any additional compensation from the company that is not related to their service as a board member, such activity should be disclosed and explained.

Companies should consider paying a substantial portion (e.g., for some companies, as much as 50% or more) of director compensation in stock, performance stock units or similar equity-like instruments. Companies also should consider requiring directors to retain a significant portion of their equity compensation for the duration of their tenure to further directors’ economic alignment with the long-term performance of the company.

e. Board committee structure and service

Companies should conduct a thorough and robust orientation program for their new directors, including background on the industry and the competitive landscape in which the company operates, the company’s business, its operations, and important legal and regulatory issues, etc.

A board should have a well-developed committee structure with clearly understood responsibilities. Disclosures to shareholders should describe the structure and function of each board committee.

Boards should consider periodic rotation of board leadership roles (i.e., committee chairs and the lead independent director), balancing the benefits of rotation against the benefits of continuity, experience and expertise.

f. Director tenure and retirement age

It is essential that a company attract and retain strong, experienced and knowledgeable board members.

Some boards have rules around maximum length of service and mandatory retirement age for directors; others have such rules but permit exceptions; and still others have no such rules at all. Whatever the case, companies should clearly articulate their approach on term limits and retirement age. And insofar as a board permits exceptions, the board should explain (ordinarily in the company’s proxy statement) why a particular exception was warranted in the context of the board’s assessment of its performance and composition.

Board refreshment should always be considered in order to ensure that the board’s skill set and perspectives remain sufficiently current and broad in dealing with fast-changing business dynamics. But the importance of fresh thinking and new perspectives should be tempered with the understanding that age and experience often bring wisdom, judgment and knowledge.

g. Director effectiveness

Boards should have a robust process to evaluate themselves on a regular basis, led by the non-executive chair, lead independent director or appropriate committee chair. The board should have the fortitude to replace ineffective directors.

II. Board of Directors’ Responsibilities

a. Director communication with third parties

Robust communication of a board’s thinking to the company’s shareholders is important. There are multiple ways of going about it. For example, companies may wish to designate certain directors—as and when appropriate and in coordination with management—to communicate directly with shareholders on governance and key shareholder issues, such as CEO compensation. Directors who communicate directly with shareholders ideally will be experienced in such matters.

Directors should speak with the media about the company only if authorized by the board and in accordance with company policy.

In addition, the CEO should actively engage on corporate governance and key shareholder issues (other than the CEO’s own compensation) when meeting with shareholders.

b. Critical activities of the board; setting the agenda

The full board (including, where appropriate, through the non-executive chair or lead independent director) should have input into the setting of the board agenda.

Over the course of the year, the agenda should include and focus on the following items, among others:

A robust, forward-looking discussion of the business.

The performance of the current CEO and other key members of management and succession planning for each of them. One of the board’s most important jobs is making sure the company has the right CEO. If the company does not have the appropriate CEO, the board should act promptly to address the issue.

Creation of shareholder value, with a focus on the long term. This means encouraging the sort of long-term thinking owners of a private company might bring to their strategic discussions, including investments that may not pay off in the short run.

Major strategic issues (including material mergers and acquisitions and major capital commitments) and long-term strategy, including thorough consideration of operational and financial plans, quantitative and qualitative key performance indicators, and assessment of organic and inorganic growth, among others.

The board should receive a balanced assessment on strategic fit, risks and valuation in connection with material mergers and acquisitions. The board should consider establishing an ad hoc Transaction Committee if significant board time is otherwise required to consider a material merger or acquisition. If the company’s stock is to be used in such a transaction, the board should carefully assess the company’s valuation relative to the valuation implied in the acquisition. The objective is to properly evaluate the value of what you are giving vs. the value of what you are getting.

Significant risks, including reputational risks. The board should not be reflexively risk averse; it should seek the proper calibration of risk and reward as it focuses on the long-term interests of the company’s shareholders.

Standards of performance, including the maintaining and strengthening of the company’s culture and values.

Material corporate responsibility matters.

Shareholder proposals and key shareholder concerns.

The board (or appropriate board committee) should determine the best approach to compensate management, taking into account all the factors it deems appropriate, including corporate and individual performance and other qualitative and quantitative factors (see below at VII., “Compensation of Management”).

A board should be continually educated on the company and its industry. If a Board feels it would be productive, outside experts and advisors should be brought in to inform directors on issues and events affecting the company.

The board should minimize the amount of time it spends on frivolous or non-essential matters—the goal is to provide perspective and make decisions to build real value for the company and its shareholders.

As authorized and coordinated by the board, directors should have unfettered access to management, including those below the CEO’s direct reports.

At each meeting, to ensure open and free discussion, the board should meet in executive session without the CEO or other members of management. The independent directors should ensure that they have enough time to do this properly.

The board (or appropriate board committee) should discuss and approve the CEO’s compensation.

In addition to its other responsibilities, the Audit Committee should focus on whether the company’s financial statements would be prepared or disclosed in a materially different manner if the external auditor itself were solely responsible for their preparation.

III. Shareholder Rights

Many public companies and asset managers have recently reviewed their approach to proxy access. Others have not yet undertaken such a review or may have one under way. Among the larger market capitalization companies that have adopted proxy access provisions, generally a shareholder (or group of up to 20 shareholders) who has continuously held a minimum of 3% of the company’s outstanding shares for three years is eligible to include on the company’s proxy statement nominees for a minimum of 20% (and, in some cases, 25%) of the company’s board seats. Generally, only shares in which the shareholder has full, unhedged economic interest count toward satisfaction of the ownership/holding period requirements. A higher threshold of ownership (e.g., 5%) often has been adopted for smaller market capitalization companies (e.g., less than $2 billion).

Dual-class voting is not a best practice. If a company has dual-class voting, which sometimes is intended to protect the company from short-term behavior, the company should consider having specific sunset provisions based upon time or a triggering event, which eliminate dual-class voting. In addition, all shareholders should be treated equally in any corporate transaction.

Written consent and special meeting provisions can be important mechanisms for shareholder action. Where they are adopted, there should be a reasonable minimum amount of outstanding shares required in order to prevent a small minority of shareholders from being able to abuse the rights or waste corporate time and resources.

IV. Public Reporting

Transparency around quarterly financial results is important.

Companies should frame their required quarterly reporting in the broader context of their articulated strategy and provide an outlook, as appropriate, for trends and metrics that reflect progress (or not) on long-term goals. A company should not feel obligated to provide earnings guidance—and should determine whether providing earnings guidance for the company’s shareholders does more harm than good. If a company does provide earnings guidance, the company should be realistic and avoid inflated projections. Making short-term decisions to beat guidance (or any performance benchmark) is likely to be value destructive in the long run.

As appropriate, long-term goals should be disclosed and explained in a specific and measurable way.

A company should take a long-term strategic view, as though the company were private, and explain clearly to shareholders how material decisions and actions are consistent with that view.

Companies should explain when and why they are undertaking material mergers or acquisitions or major capital commitments.

Companies are required to report their results in accordance with Generally Accepted Accounting Principles (“GAAP”). While it is acceptable in certain instances to use non-GAAP measures to explain and clarify results for shareholders, such measures should be sensible and should not be used to obscure GAAP results. In this regard, it is important to note that all compensation, including equity compensation, is plainly a cost of doing business and should be reflected in any non-GAAP measurement of earnings in precisely the same manner it is reflected in GAAP earnings.

V. Board Leadership (Including the Lead Independent Director’s Role)

The board’s independent directors should decide, based upon the circumstances at the time, whether it is appropriate for the company to have separate or combined chair and CEO roles. The board should explain clearly (ordinarily in the company’s proxy statement) to shareholders why it has separated or combined the roles.

If a board decides to combine the chair and CEO roles, it is critical that the board has in place a strong designated lead independent director and governance structure.

Depending on the circumstances, a lead independent director’s responsibilities may include:

Serving as liaison between the chair and the independent directors

Presiding over meetings of the board at which the chair is not present, including executive sessions of the independent directors

Ensuring that the board has proper input into meeting agendas for, and information sent to, the board

Having the authority to call meetings of the independent directors

Insofar as the company’s board wishes to communicate directly with shareholders, engaging (or overseeing the board’s process for engaging) with those shareholders

Guiding the annual board self-assessment

Guiding the board’s consideration of CEO compensation

Guiding the CEO succession planning process

VI. Management Succession Planning

Senior management bench strength can be evaluated by the board and shareholders through an assessment of key company employees; direct exposure to those employees is helpful in making that assessment.

Companies should inform shareholders of the process the board has for succession planning and also should have an appropriate plan if an unexpected, emergency succession is necessary.

VII. Compensation of Management