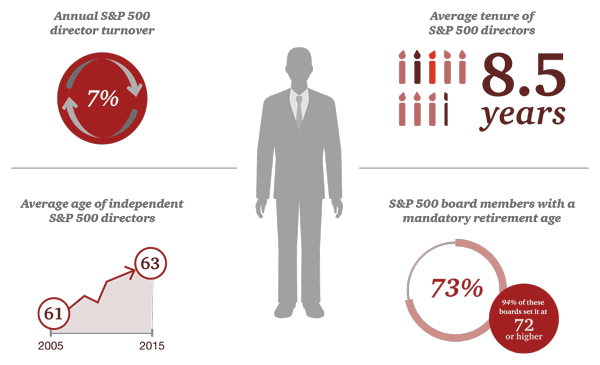

Voici les principaux résultats eu égard aux propositions des actionnaires lors des assemblées annuelles de 2016. Ce sont des données relatives aux grandes sociétés publiques américaines.

Je crois qu’il est intéressant d’avoir le pouls de l’évolution des propositions des actionnaires, car cela révèle l’état de la gouvernance dans les grandes corporations ainsi que le niveau d’activités des activistes.

Cet article, publié par Elizabeth Ising, associée et co-présidente de la « Securities Regulation and Corporate Governance practice group » de la firme Gibson, Dunn & Crutcher, est paru sur le forum de HLS hier.

L’auteure présente les résultats de manière très illustrée, sans porter de jugement.

Personnellement, je constate un certain essoufflement des propositions des actionnaires en 2016. Dans plusieurs cas cependant les entreprises ont remédié aux lacunes de gouvernance.

This post provides an overview of shareholder proposals submitted to public companies for 2016 shareholder meetings, including statistics, notable decisions from the staff of the Securities and Exchange Commission on no-action requests, and information about litigation regarding shareholder proposals. All shareholder proposal data in this post is as of June 1, 2016 unless otherwise indicated.

Submitted Shareholder Proposals

Overview

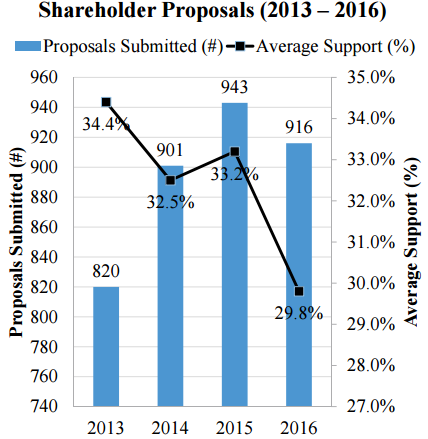

Fewer Proposals Submitted: According to ISS data, shareholders have submitted fewer shareholder proposals for 2016 meetings than they did for 2015 meetings.

However, the number of proposals submitted for 2016 meetings is still higher than the approximate number of proposals submitted for 2014 and 2013 meetings.

Support Declined: Average support for shareholder proposals is at its lowest in four years. [1]

Only 14.5% of proposals (61 proposals) voted on at 2016 meetings received support from a majority of votes cast, compared to 16.7% of proposals (75 proposals) at 2015 meetings.

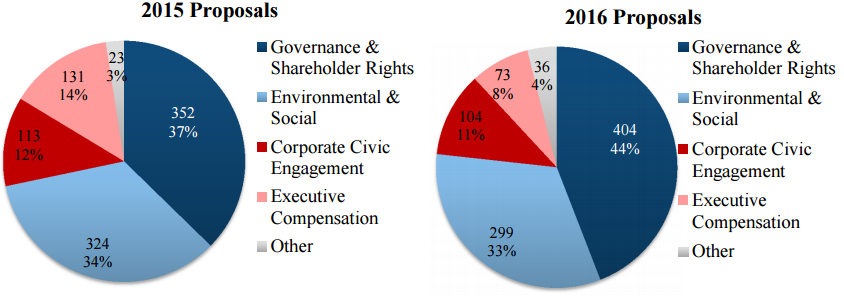

Focus Remains on Governance

Across five broad categories of shareholder proposals, the approximate number of proposals submitted for 2016 meetings (as compared to 2015 meetings) was as follows:

For the second year in a row, governance & shareholder rights proposals were the most frequently submitted proposals, largely due to the yet again unprecedented number of proxy access shareholder proposals submitted (201 proposals (or 21.9% of all proposals) submitted for 2016 meetings versus 108 proposals submitted for 2015 meetings).

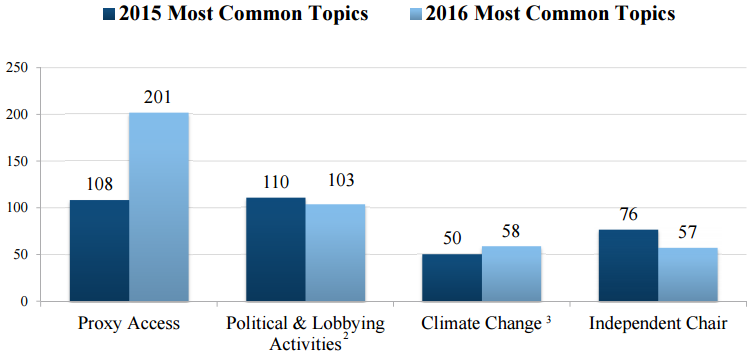

Proxy Access Proposals Continue to Dominate

The most common 2016 shareholder proposal topics, along with the approximate numbers of proposals submitted and as compared to the most common 2015 shareholder proposal topics, were [2][3]:

Most Active Proponents

Chevedden & Co.: As is typically the case, John Chevedden and shareholders associated with him (including James McRitchie) submitted by far the greatest number of shareholder proposals—approximately 227 for 2016 meetings.

Most of these proposals (66.6%) have either been voted on or are pending. Twenty-three percent have been omitted after obtaining relief through the SEC no-action process; another 7% have ultimately not been included in proxy statements or have not been properly presented at the meeting; and only 3.1% of these proposals have been withdrawn.

By way of comparison, shareholder proponents withdrew approximately 19.2% of the proposals submitted for 2016 meetings, up from approximately 17% of the proposals withdrawn for 2015 meetings.

NYC Pension Funds: This season once again saw a large number of proposals submitted by the New York City Comptroller on behalf of five New York City pension funds, which submitted or cofiled at least 79 proposals (as compared to 86 proposals submitted for 2015 meetings), including approximately 72 proxy access proposals, [4] as part of the Comptroller’s continuation of its “Boardroom Accountability Project” for 2016.

Only 34.6% of these proposals have either been voted on or are pending; most (55.6%) of these proposals have been withdrawn. The remainder (9.8%) have been omitted or not otherwise included in proxy statements.

Other Proponents

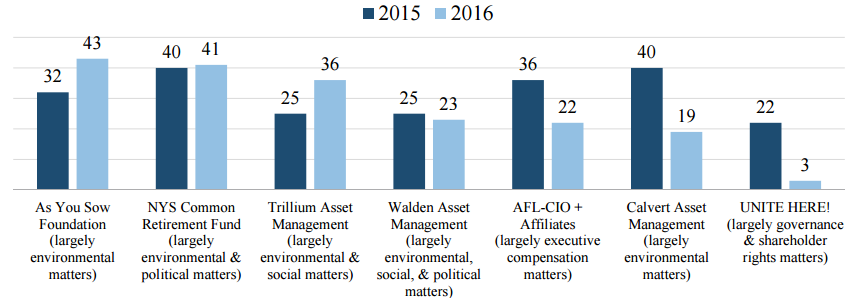

Some of the Same Players (But Not Everyone Returned in 2016): As was true for 2015 meetings, with the exception of Calvert Asset Management and UNITE HERE!, several of the same proponents that were reported to have submitted or co-filed at least 20 proposals each for 2015 meetings, did so again for 2016 meetings:

Same Subject Areas: As reflected in the chart above, the focus of these proponents remained largely consistent with their focus for 2015 meetings.

Public Pension Funds: In addition to the New York City and New York State pension funds, several other state pension funds submitted shareholder proposals as well:

California State Teachers’ Retirement System (18 proposals, largely focused on governance matters and climate change);

Connecticut Retirement Plans and Trust Funds (14 proposals, largely focused on governance, social, and political matters);

City of Philadelphia Public Employees Retirement System (10 proposals, largely focused on political and lobbying matters);

North Carolina Retirement Systems (two board diversity proposals);

California Public Employees’ Retirement System (one proxy access proposal); and

Firefighters’ Pension System of Kansas City, Missouri (one majority voting in director elections proposal).

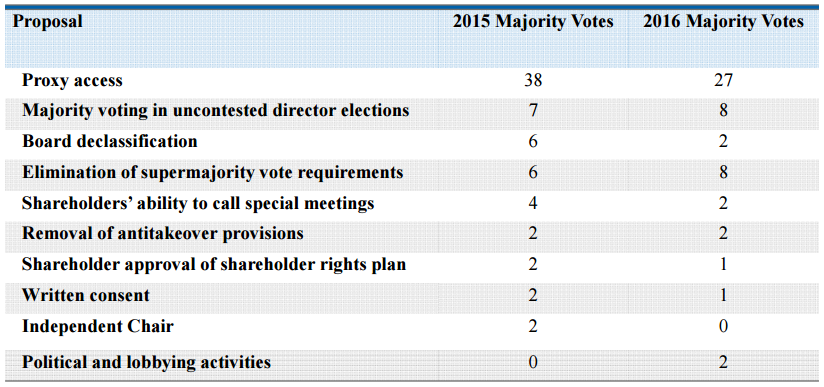

Shareholder Proposal Voting Results

Majority Voting in Director Elections Receives the Highest Support

The following are the principal topics addressed in proposals that received high shareholder support at a number of companies’ 2016 meetings:

Majority Voting in Uncontested Director Elections: Ten proposals voted on averaged 74.2% of votes cast, compared to 76.6% in 2015;

Amendment of Bylaws or Articles to Remove Antitakeover Provisions: Two proposals voted on averaged 70.6% of votes cast, compared to 79% in 2015;

Board Declassification: Three proposals voted on averaged 64.5% of votes cast, compared to 72.6% in 2015;

Elimination of Supermajority Vote Requirements: Thirteen proposals voted on averaged 59.6% of votes cast, compared to 53.0% in 2015;

Proxy Access: Fifty-eight proposals voted on averaged 48.7% of votes cast, compared to 54.6% in 2015;

Shareholder Ability to Call Special Meetings: Sixteen proposals voted on averaged 39.6% of votes cast, compared to 44.4% in 2015; and

Written Consent: Thirteen proposals voted on averaged 43.4% of votes cast, compared to 39.4% in 2015.

Majority Votes on Shareholder Proposals

The table below shows the principal topics addressed in proposals that received a majority of votes cast at a number of companies:

[1] As of June 1, 2016, voting results were available through the ISS databases for a total of 422 proposals. As a matter of practice, the vast majority of shareholder proposals submitted to companies for shareholder meetings are submitted under Rule 14a-8 rather than pursuant to companies’ advance notice bylaws. However, because the ISS data does not indicate whether a shareholder proposal has been submitted under Rule 14a-8 or under a company’s advance notice bylaws, it is possible that the ISS data includes voting results for shareholder proposals not submitted pursuant to Rule 14a-8. This discrepancy is likely to account for only a very small number of proposals. (go back)

[2] Includes all corporate civic engagement proposals, except proposals relating to charitable contributions (one submitted as of June 1, 2016 for 2016 meetings). (go back)

[3] Includes proposals relating to (i) reports on climate change; (ii) greenhouse gas emissions; and (iii) climate change action (i.e., proposals requesting increasing return of capital to shareholders in light of climate change risks). Note that climate change is a subtopic of the environmental and social category of proposals. (go back)

Voici une liste des billets en gouvernance les plus populaires publiés sur mon blogue au deuxième trimestre de 2016.

Cette liste de 15 billets constitue, en quelque sorte, un sondage de l’intérêt manifesté par des milliers de personnes sur différents thèmes de la gouvernance des sociétés. On y retrouve des points de vue bien étayés sur des sujets d’actualité relatifs aux conseils d’administration.

Que retrouve-t-on dans ce blogue et quels en sont les objectifs?

Ce blogue fait l’inventaire des documents les plus pertinents et les plus récents en gouvernance des entreprises. La sélection des billets est le résultat d’une veille assidue des articles de revue, des blogues et des sites web dans le domaine de la gouvernance, des publications scientifiques et professionnelles, des études et autres rapports portant sur la gouvernance des sociétés, au Canada et dans d’autres pays, notamment aux États-Unis, au Royaume-Uni, en France, en Europe, et en Australie.

Je fais un choix parmi l’ensemble des publications récentes et pertinentes et je commente brièvement la publication. L’objectif de ce blogue est d’être la référence en matière de documentation en gouvernance dans le monde francophone, en fournissant au lecteur une mine de renseignements récents (les billets) ainsi qu’un outil de recherche simple et facile à utiliser pour répertorier les publications en fonction des catégories les plus pertinentes.

Quelques statistiques à propos du blogue Gouvernance | Jacques Grisé

Ce blogue a été initié le 15 juillet 2011 et, à date, il a accueilli plus de 192000 visiteurs. Le blogue a progressé de manière tout à fait remarquable et, au30 juin 2016, il était fréquenté pardes milliers devisiteurs par mois. Depuis le début,j’aiœuvré à la publication de 1373billets.

En 2016, j’estime qu’environ 5000 personnes par mois visiteront le blogue afin de s’informer sur diverses questions de gouvernance. À ce rythme, on peut penser qu’environ 60000 personnesvisiteront le site du blogue en 2016.

On note que 80 % des billets sont partagés par l’intermédiaire de différents moteurs de recherche et 20 % par LinkedIn, Twitter, Facebook et Tumblr.

Voici un aperçu du nombre de visiteurs par pays :

Canada (64 %)

France, Suisse, Belgique (20 %)

Maghreb [Maroc, Tunisie, Algérie] (5 %)

Autres pays de l’Union européenne (3 %)

États-Unis [3 %]

Autres pays de provenance (5 %)

En 2014, le blogue Gouvernance | Jacques Grisé a été inscrit dans deux catégories distinctes du concours canadien Made in Blog [MiB Awards] : Business et Marketing et médias sociaux. Le blogue a été retenu parmi les dix [10] finalistes à l’échelle canadienne dans chacune de ces catégories, le seul en gouvernance. Il n’y avait pas de concours en 2015.

Vos commentaires sont toujours grandement appréciés. Je réponds toujours à ceux-ci.

N.B. Vous pouvez vous inscrire ou faire des recherches en allant au bas de cette page.

Bonne lecture !

Voici les Tops 15 du second trimestre de 2016 du blogue en gouvernance

Les autorités réglementaires, les firmes spécialisées en votation et les experts en gouvernance suggèrent que les rôles et les fonctions de président du conseil d’administration soient distincts des attributions des PDG (CEO).

En fait, on suppose que la séparation des fonctions, entre la présidence du conseil et la présidence de l’entreprise (CEO), est généralement bénéfique, c’est-à-dire que des pouvoirs distincts permettent d’éviter les conflits d’intérêts, tout en rassurant les actionnaires.

C’est ce que les professeurs de finance Harley Ryan*, Narayanan Jayaraman et Vikram Nanda ont tenté de valider empiriquement dans leur récente étude sur le sujet. L’article a paru aujourd’hui dans le forum du Harvard Law School on Corporate Governance. Comme on le sait, la plupart des études antérieures ne sont pas concluantes à cet égard.

Les auteurs ont proposé un modèle d’apprentissage de la dualité des deux fonctions en identifiant une stratégie basée sur la préparation de la relève : “passing the baton” (PTB). Dans ce modèle, les administrateurs s’allouent une période de probation afin de bien connaître les habiletés de leurs nouveaux CEO.

Si les membres du CA sont rassurés sur les talents du CEO et s’ils sont satisfaits de ses performances, ils lui attribuent également le poste de « chairman ». Le pouvoir accru du CEO améliore la rétention des meilleurs éléments.

Les résultats de la recherche montrent que les CEO qui ont obtenu le titre de « chairman » dans ces conditions (PTB) tendent à mieux réussir qu’avant la nomination à ce poste. De plus, les actionnaires sont plutôt réceptifs à ce mode de nomination, surtout si la promotion est faite dans un court délai, car cela leur indique que le CEO constitue une valeur sûre pour l’organisation.

Les auteurs insistent sur l’importance de considérer les mécanismes d’apprentissage en place (PTB) ainsi que les objectifs de rétention des meilleurs CEO dans l’évaluation des structures de gouvernance.

Ainsi, les actionnaires ne sont pas toujours nécessairement mieux servis par la séparation des deux rôles. Notons cependant qu’en général, les sociétés cotées ont de plus en plus tendance à séparer les deux fonctions.

Le billet paru sur mon blogue le 17 novembre 2015 fait état de la situation à ce jour :

Les études contemporaines démontrent une nette tendance en faveur de la séparation des deux rôles. Le Canadian Spencer Stuart Board Index estime qu’une majorité de 85 % des 100 plus grandes entreprises canadiennes cotées en bourse ont opté pour la dissociation entre les deux fonctions. Dans le même sens, le rapport Clarkson affiche que 84 % des entreprises inscrites à la bourse de Toronto ont procédé à ladite séparation. Subsistent cependant encore de nos jours des entreprises canadiennes qui permettent le cumul. L’entreprise Air Transat A.T. Inc en est la parfaite illustration : M. Jean-Marc Eustache est à la fois président du conseil et chef de la direction. A contrario, le fond de solidarité de la Fédération des travailleurs du Québec vient récemment de procéder à la séparation des deux fonctions.

Aux États-Unis en 2013, 45 % des entreprises de l’indice S&P500 (au total 221 entreprises) dissocient les rôles de PDG et de président du conseil. Toutefois, les choses ne sont pas aussi simples qu’elles y paraissent : 27 % des entreprises de cet indice ont recombiné ces deux rôles. Évoquons à ce titre le cas de Target Corp dont les actionnaires ont refusé la dissociation des deux fonctions .

Est-ce dans l’air du temps ? Est-ce le résultat d’études sérieuses sur les principes de bonne gouvernance ?

Comme on dit souvent en management : Ça dépend des cas !

Considerable disagreement exists on the merits of CEO-Chair duality. In recent years, there has been growing regulatory and investor pressure to split the titles of CEO and Chairman of the Board. In fact, there is a significant trend towards separation of the two titles. However, the empirical evidence in the literature is inconclusive on the impact of separating these roles. We argue that the inconclusive evidence arises from endogenous self-selection that complicates empirical identification strategies and the ability to recognize the correct counterfactual firms.

In our paper, Does Combining the CEO and Chair Roles Cause Poor Firm Performance?, which was recently made publicly available on SSRN, we propose a learning model of CEO-chair duality and implement an identification strategy to address sample selection issues. Our model and identification is based on “passing the baton” (PTB) firms that award the chair position after a probationary period during which the board of directors learns about the ability of the CEO. In the model, the board optimally awards the additional position of board chair if the CEO demonstrates sufficient talent. The increase in CEO power improves the retention of high-quality CEOs by mitigating concerns about the board reneging on compensation contracts. The model delivers several implications that we test in our empirical analysis.

Using a very large sample of over 22,000 firm-year observations for the period 1995-2010, we explore the determinants and consequences of the combining the two roles. Firms that always combine the two roles, always separate the roles, or award the additional title following a period of evaluation exhibit significantly different firm characteristics, which suggest self-selection. We find that PTB firms are more likely to be from industries that are less homogenous. This is consistent with a learning rationale underlying PTB strategies: CEO performance is harder to benchmark in such industries and reneging on contracts may be of greater concern to CEOs. We also find that firms with more business segments are more likely to combine the two roles. These findings suggest that more complex organizations are better served by combining the roles of the CEO and the Chairman.

Overall, CEOs that receive the additional title of board chair outperform their industry benchmark before receiving both titles. In firms that combine the roles after observing the CEO’s performance under a separate board chair, the combination is positively related to both firm and industry performance in the two years prior to the combination. As predicted by our model, a naïve analysis of the post-chair appointment performance, one that fails to control for selection issues and mean reversion in performance data, indicates a significant drop in firm performance relative to the pre-chair period. However, in a matched sample of firms where the matching criteria includes the pre-appointment performance and firm attributes that predict a high propensity for using a PTB succession strategy, there is no evidence of post-appointment underperformance. These results suggest that the pass-the-baton succession process appears to be an equilibrium mechanism in which some firms optimally use the PTB structure to learn about the CEO and then award the additional title of board chair to increase the odds of retaining talented CEOS. Thus, the evidence is broadly consistent with the learning hypothesis that the additional title is awarded by the board after evaluating the ability of the CEO.

Our model suggests that, ceteris paribus, talented CEOs in a weaker bargaining position relative to the board will tend to be promoted to chair more quickly. The reason is that more vulnerable CEOs are more likely to pursue outside opportunities. Supportive of the prediction, we find that when the board is more independent, is not coopted and the CEO is externally sourced—the promotion to chair occurs more quickly. These findings are also counter to the notion that agency considerations and influence are central to the CEO being appointed chairman. We also show that stockholders react positively to combinations that occur early in the CEO’s tenure, which suggests that early promotions reveal directors’ private information about the quality of the CEO to the market. This is inconsistent with alternative explanations such as an incentive rationale for PTB or agency problem, since both of these alternatives would suggest a negative market reaction to such promotions.

A major implication of our analysis for researchers is that one should consider learning mechanisms and retention objectives when evaluating various board structures. Structures that are seemingly incompatible with effective monitoring may in fact be optimal when one considers the impact of learning on retention. For governance activists and policy makers, the implications of our analysis are straightforward: the results call into question the prevailing wisdom that suggests that shareholders will always be better served by separating the two roles. Thus, those who seek to reform governance should be cautious in proposing to unambiguously separate the roles of CEO and board chair. Forcing separation by fiat is likely not an ideal policy. Overall our evidence suggests that having one type of executive and board leadership structure is not optimal for all firms.

Harley Ryan* is Associate Professor of Finance at Georgia State University, Narayanan Jayaraman is Professor of Finance at Georgia Institute of Technology et Vikram Nanda is Professor of Finance at the University of Texas at Dallas.

Les théories contemporaines de la gouvernance sont basées sur le modèle de la « maximisation de la valeur aux actionnaires ».

Dans un article paru sur le forum du Harvard Law School on Corporate Governance, l’auteur Marc Moore* explique que, malgré l’émergence d’autres paradigmes des rouages de la gouvernance moderne (Post — Shareholders-Values | PSV), c’est encore le modèle de la maximisation de la valeur aux actionnaires qui domine.

C’est ainsi que le nouveau modèle de réallocation des profits des PSV, qui favoriserait le développement interne de l’entreprise et les investissements à long terme, cède le pas, la plupart du temps, à la redistribution des surplus aux actionnaires, notamment par la voie des dividendes ou par le rachat des actions.

Voici comment l’auteur conclut son article. Quel est votre point de vue ?

The somewhat uncomfortable truth for many observers is that, for better or worse, the American system of shareholder capitalism, and its pivotal corporate governance principle of shareholder primacy, are ultimately products of our own collective (albeit unintentional) civic design. Accordingly, while in many respects the orthodox shareholder-oriented corporate governance framework may be a social evil; it is nonetheless a necessary evil, which US worker-savers implicitly tolerate as the effective social price for sustaining a system of non-occupational income provision outside of direct state control. Until corporate governance scholars and policymakers are capable of coordinating their respective energies towards somehow alleviating US worker-savers’ significant dependence on corporate equity as a source of non-occupational wealth gains, the shareholder-oriented corporation is likely to remain a socially indispensable phenomenon. To those who rue this prospect, it might be retorted “better the devil you know than the devil you don’t.”

Despite their differences of opinion on other issues, most corporate law and governance scholars have tended to agree upon one thing at least: that the overarching normative objective of corporate governance—and, by implication, corporate law—should be the maximization (or, at least, long-term enhancement) of shareholder wealth. Indeed this proposition—variously referred to as the “shareholder wealth maximization”, “shareholder value”, or “shareholder primacy” norm—is so ingrained within mainstream corporate governance thinking that it has traditionally been subjected to little serious policy or even academic question. However, the zeitgeist would appear to be slowly but surely changing. The financial crisis may not quite have proved the watershed moment it was initially heralded as in terms of resetting dominant currents of economic or political opinion. Nonetheless, in the narrower but still important domain of corporate governance thinking and policymaking, the past decade’s events have triggered the onset of what promises to be a potentially major paradigm shift in the direction of an evolving “Post-Shareholder-Value” (or “PSV”) consensus.

On an academic level, this movement is represented by a growing body of influential legal and economic scholarship which contests most of the staple ideological tenets of orthodox corporate governance theory. Amongst the most noteworthy contributions to this literature are Professor Lynn Stout’s influential 2012 book The Shareholder Value Myth (Berret-Koehler), and also Professor Colin Mayer’s excellent 2013 work Firm Commitment: Why the corporation is failing us and how to restore trust in it (Oxford University Press). In particular, proponents of the PSV paradigm typically dismiss the common neo-classical equation of shareholder wealth maximization with economic efficiency in the broader social sense. They also typically eschew individualistic understandings of the firm in terms of its purported internal bargaining dynamics, in favour of alternative conceptual models which celebrate the distinctive value of the corporation’s inherently autonomous corporeal features.

Evidence of a potential drift from the formerly dominant shareholder primacy paradigm in corporate governance is additionally apparent on a practical policy-making level today, not least in the rapid proliferation of Benefit Corporations as a viable and popular alternative legal form to the orthodox for-profit corporation. At the same time, the increasing use by US-listed firms of dual-class voting structures designed to insulate management from outside capital market pressures, coupled with the seemingly greater flexibility afforded to boards over recent years in defending against unwanted takeover bids from so-called corporate “raiders,” both provide additional cause to question the longevity of the shareholder-oriented corporate governance status quo.

But while evolving PSV institutional mechanisms such as Benefit Corporations and dual-class share structures are prima facie encouraging from a social perspective, there is cause for scepticism about their capacity to become anything more than a relatively niche or peripheral feature of the US public corporations landscape. This is principally because such measures, in spite of their apparent reformist potential, are still ultimately quasi-contractual and thus essentially voluntary in nature, meaning that they are unlikely to be adopted in a public corporations context except in extraordinary instances. From a normative point of view, moreover, it is arguable that such measures—irrespective of the extent of their take-up over the coming years—ultimately should remain quasi-contractual and voluntary in nature, as opposed to being placed on any sort of mandatory basis.

In this regard, it should be respected that public corporations are not only the predominant organizational vehicle for conducting large-scale industrial production projects over indefinite time horizons, as academic proponents of the PSV position have vigorously emphasized. Of comparable importance and ingenuity is that fact that—in the United States at least—public corporations are also a necessary structural means of enabling the residual income streams accruing from successful industrial projects to fund the provision of socially essential financial services, via the medium of public capital (and especially equity) markets. Unfortunately, though, these two dimensions of the public corporation are not always mutually compatible. Rather, it would seem that more often than not they are prone to antagonize, rather than complement, one another. This is especially so when it comes to the periodically-vexing managerial question of whether a firm’s residual earnings should be committed internally to the sustenance and development of the productive corporate enterprise itself, or else distributed externally to shareholders in the form of either enhanced dividends or stock buybacks. The problem is that the evolving PSV corporate governance paradigm—as manifested on both an intellectual and policy level today—focuses exclusively on the former of those dimensions at the expense of the latter.

The somewhat uncomfortable truth for many observers is that, for better or worse, the American system of shareholder capitalism, and its pivotal corporate governance principle of shareholder primacy, are ultimately products of our own collective (albeit unintentional) civic design. Accordingly, while in many respects the orthodox shareholder-oriented corporate governance framework may be a social evil; it is nonetheless a necessary evil, which US worker-savers implicitly tolerate as the effective social price for sustaining a system of non-occupational income provision outside of direct state control. Until corporate governance scholars and policymakers are capable of coordinating their respective energies towards somehow alleviating US worker-savers’ significant dependence on corporate equity as a source of non-occupational wealth gains, the shareholder-oriented corporation is likely to remain a socially indispensable phenomenon. To those who rue this prospect, it might be retorted “better the devil you know than the devil you don’t.”

The complete paper is available for download here.

Marc Moore* is Reader in Corporate Law and Director of the Centre for Corporate and Commercial Law (3CL) at the University of Cambridge. This post is based on a recent paper by Dr. Moore. Related research from the Program on Corporate Governance includes The Case for Increasing Shareholder Power by Lucian Bebchuk.

Je crois que cet article intéressera tous les administrateurs siégeant à des conseils d’administration. Personnellement, je suis très heureux de constater que la démarche ait consisté en des rencontres avec des groupes d’administrateurs chevronnés.

Plusieurs messages très pertinents ressortent des rencontres. Ils sont regroupés selon les catégories suivantes :

La taille du conseil

La composition du conseil

La présidence du conseil

L’évaluation du conseil

Information et prise de décision

Les comités du conseil

Je vous invite à lire l’ensemble du document sur le site de l’IGOPP. Voici un extrait de cet article.

« Une longue expérience comme administrateur de sociétés mène souvent au constat que la qualité de la gouvernance et l’efficacité d’un conseil tiennent à des facteurs subtils, difficilement quantifiables, mais tout aussi importants, voire plus importants, que les aspects fiduciaires et formels.

Cette dimension informelle de la gouvernance prend forme et substance dans les échanges, les interactions sociales, l’encadrement des discussions, le style de leadership du président du conseil, dans tout ce qui se passe avant et après les réunions formelles ainsi qu’autour de la table au moment des réunions du conseil et de ses comités.

Cela est vrai pour tout type de sociétés, que ce soient une entreprise cotée en bourse, un organisme public, une société d’État, une coopérative ou un organisme sans but lucratif.

L’IGOPP estime que pour relever encore l’efficacité des conseils d’administration il est important de bien comprendre ce qui peut contribuer à une dynamique productive entre les membres d’un conseil.

Pourtant, alors que les études sur tous les aspects de la gouvernance foisonnent, cet aspect fait l’objet de peu de recherches empiriques, et ce pour une raison bien simple. Les conseils d’administration ne peuvent donner à des chercheurs un accès direct à leurs réunions ni à leur documentation en raison des contraintes de confidentialité.

Le professeur Richard Leblanc, grâce au réseau de son directeur de thèse de doctorat et co-auteur James Gillies, a pu, rare exception, observer un certain nombre de conseils d’administration en action. Ils ont publié en 2005 un ouvrage Inside the Boardroom, lequel propose une intéressante typologie des comportements dominants des membres de conseil au cours de réunions.

Depuis aucune autre étude empirique n’a été menée sur le sujet. D’ailleurs, l’ouvrage de Leblanc et Gillies, se limitant aux comportements observables lors de réunions formelles, ne nous éclairait que sur une partie du phénomène »

…

« L’IGOPP a voulu mieux comprendre cette dynamique et, si possible, proposer aux administrateurs et présidents de conseil des suggestions pouvant améliorer la qualité de la gouvernance.

L’IGOPP a donc invité des membres de conseil expérimentés et férus de gouvernance pour un échange sur cet enjeu. Les 14 personnes suivantes ont accepté promptement notre invitation et nous les en remercions chaleureusement:

Jacynthe Côté

Gérard Coulombe

Isabelle Courville

Paule Doré

Jean La Couture

Sylvie Lalande

John LeBoutillier

Brian Levitt

David L. McAusland

Marie-José Nadeau

Réal Raymond

Louise Roy

Guylaine Saucier

Jean-Marie Toulouse, qui a agi comme modérateur des discussions.

Collectivement, nos interlocuteurs siègent au sein de 75 conseils, dont 34 sont des sociétés ouvertes parmi lesquelles 14 ont leur siège hors Québec.

Nous avons tenu quatre sessions, chacune comptant un petit nombre d’administrateurs, de façon à ce que les discussions permettent à tous de s’exprimer pleinement.

Ces sessions furent riches en commentaires, observations pertinentes et suggestions utiles ».

Plusieurs messages très pertinents ressortent des rencontres. Ils sont regroupés selon les catégories suivantes :

La taille du conseil

La composition du conseil

La présidence du conseil

L’évaluation du conseil

Information et prise de décision

Les comités du conseil

En conclusion, l’auteur mentionne que « ce texte tente de rendre justice aux échanges entre les 14 administrateurs chevronnés qui ont participé à cette recherche de pistes d’amélioration de la dynamique des conseils d’administration et donc de la gouvernance de nos sociétés ».

Aujourd’hui, je vous propose la lecture d’un article paru dans la revue European Journal of Risk Regulation (EJRR) qui scrute le scandale de Volkswagensous l’angle juridique, mais, surtout, sous l’angle des manquements à la saine gouvernance.

Le texte se présente comme un cas en gouvernance et en management. Celui-ci devrait alimenter les réflexions sur l’éthique, les valeurs culturelles et les effets des pressions excessives à la performance.

Vous trouverez, ci-dessous, l’intégralité de l’article avec le consentement de l’auteure. Je n’ai pas inclus les références, qui sont très abondantes et qui peuvent être consultées sur le site de la maison d’édition lexxion.

Like some other crises and scandals that periodically occur in the business community, the Volkswagen (“VW”) scandal once again highlights the devastating consequences of corporate misconduct, once publicly disclosed, and the media storm that generally follows the discovery of such significant misbehaviour by a major corporation. Since the crisis broke in September 2015, the media have relayed endless détails about the substantial negative impacts on VW on various stakeholder groups such as employees, directors, investors, suppliers and consumers, and on the automobile industry as a whole (1)

The multiple and negative repercussions at the economic, organizational and legal levels have quickly become apparent, in particular in the form of resignations, changes in VW’s senior management, layoffs, a hiring freeze, the end to the marketing of diesel-engined vehicles, vehicle recalls, a decline in car sales, a drop in market capitalization, and the launching of internal investigations by VW and external investigations by the public authorities. This comes in addition to the threat of numerous civil, administrative, penal and criminal lawsuits and the substantial penalties they entail, as well as the erosion of trust in VW and the automobile industry generally (2).

FILE PHOTO: Martin Winterkorn, chief executive officer of Volkswagen AG, reacts during an earnings news conference at the company’s headquarters in Wolfsburg, Germany, on Monday, March 12, 2012. Volkswagen said 11 million vehicles were equipped with diesel engines at the center of a widening scandal over faked pollution controls that will cost the company at least 6.5 billion euros ($7.3 billion). Photographer: Michele Tantussi/Bloomberg *** Local Caption *** Martin Winterkorn

A scandal of this extent cannot fail to raise a number of questions, in particular concerning the cause of the alleged cheating, liable actors, the potential organizational and regulatory problems related to compliance, and ways to prevent further misconduct at VW and within the automobile industry. Based on the information surrounding the VW scandal, it is premature to capture all facets of the case. In order to analyze inmore depth the various problems raised, we will have to wait for the findings of the investigations conducted both internally by the VW Group and externally by the regulatory authorities.

While recognizing the incompleteness of the information made available to date by VW and certain commentators, we can still use this documentation to highlight a few features of the case that deserve to be studied from the standpoint of corporate governance.

This Article remains relatively modest in scope, and is designed to highlight certain organizational factors that may explain the deviant behaviour observed at VW. More specifically, it submits that the main cause of VW’s alleged wrongdoing lies in the company’s ambitious production targets for the U.S. market and the time and budget constraints imposed on employees to reach those targets. Arguably, the corporate strategy and pressures exerted on VW’s employees may have led them to give preference to the performance priorities set by the company rather than compliance with the applicable legal and ethical standards. And this corporate misconduct could not be detected because of deficiencies in the monitoring and control mechanisms, and especially in the compliance system established by the company to ensure that legal requirements were respected.

Although limited in scope, this inquiry may prove useful in identifying means to minimize, in the future, the risk of similar misconduct, not only at VW but wihin other companies as well (3). Given the limited objectives of the Article, which focuses on certain specific organizational deficiencies at VW, the legal questions raised by the case will not be addressed. However, the Article will refer to one aspect of the law of business corporations in the United States, Canada and in the EU Member States in order to emphasize the crucial role that boards in publicly-held companies must exercise to minimize the risk of misconduct (4).

II. A Preliminary Admission by VW: Individual Misconduct by a few Software Engineers

When a scandal erupts in the business community following a case of fraud, embezzlement, corruption, the marketing of dangerous products or other deviant behaviour, the company concerned and the regulatory authorities are required to quickly identify the individuals responsible for the alleged misbehaviour. For example, in the Enron, WorldCom, Tyco and Adelphia scandals of the early 2000s, the investigations revealed that certain company senior managers had acted fraudulently by orchestrating accounting manipulations to camouflage their business’s dire financial situation (5).

These revelations led to the prosecution and conviction of the officers responsible for the corporations’ misconduct (6). In the United States, the importanace of identifying individual wrongdoers is clearly stated in the Principles of Federal Prosecutions of Business Organizations issued by the U.S. Department of Justice which provide guidelines for prosecutions of corporate misbehaviour (7). On the basis of a memo issued in 2015 by the Department of Justice (the “Yatesmemo”) (8), these principles were recently revised to express a renewed commitment to investigate and prosecute individuals responsible for corporate wrongdoing.While recognizing the importance of individual prosecutions in that context, the strategy is only one of the ways to respond to white-collar crime. From a prevention standpoint, it is essential to conduct a broader examination of the organizational environment in which senior managers and employees work to determine if the enterprise’s culture, values, policies, monitoring mechanisms and practices contribute or have contributed to the adoption of deviant behaviour (9).

In the Volkswagen case, the company’s management concentrated first on identifying the handful of individuals it considered to be responsible for the deception, before admitting few weeks later that organizational problems had also encouraged or facilitated the unlawful corporate behaviour. Once news broke of the Volkswagen scandal, one of VW’s officers quickly linked the wrongdoing to the actions of a few employees, but without uncovering any governance problems or misbehaviour at the VW management level (10).

In October 2015, the President and Chief Executive Officer of the VW Group in the United States, Michael Horn, stated in testimony before a Congressional Subcommittee: “[t]his was a couple of software engineers who put this for whatever reason » […]. To my understanding, this was not a corporate decision. This was something individuals did » (11). In other words, the US CEO considered that sole responsibility for the scandal lay with a handful of engineers working at the company, while rejecting any allegation tending to incriminate the company’s management.

This portion of his testimony failed to convince the members of the Subcommittee, who expressed serious doubts about placing sole blame on the misbehaviour of a few engineers, given that the problem had existed since 2009. As expressed in a sceptical response from one of the committee’s members: « I cannot accept VW’s portrayal of this as something by a couple of rogue software engineers […] Suspending three folks – it goes way, way higher than that » (12).

Although misconduct similar to the behaviour uncovered at Volkswagen can often be explained by the reprehensible actions of a few individuals described as « bad apples », the violation of rules can also be explained by the existence of organizational problems within a company (13).

III. Recognition of Organizational Failures by VW

In terms of corporate governance, an analysis of misbehaviour can highlight problems connected with the culture, values, policies and strategies promoted by a company’s management that have a negative influence on the behaviour of senior managers and employees. Considering the importance of the organizational environment in which these players act, regulators provide for several internal and external governance mechanisms to reduce the risk of corporate misbehaviour or to minimize agency problems (14). As one example of an internal governance mechanism, the law of business corporations in the U.S., Canada and the EU Member States gives the board of directors (in a one-tier board structure, as prescribed Under American and Canadian corporation law) and the management board and supervisory board (in a two tier board structure, as provided for in some EU Member States, such as Germany) a key role to play in monitoring the company’s activities and internal dealings (15). As part of their monitoring mission, the board must ensure that the company and its agents act in a diligent and honest way and in compliance with the regulations, in particular by establishing mechanisms or policies in connection with risk management, internal controls, information disclosure, due diligence investigation and compliance (16).

When analysing the Volkswagen scandal from the viewpoint of its corporate governance, the question to be asked is whether the culture, values, priorities, strategies and monitoring and control mechanisms established by the company’s management board and supervisory board – in other words « the tone at the top »-, created an environment that contributed to the emergence of misbehaviour (17).

In this saga, although the initial testimony given to the Congressional Subcommittee by the company’s U.S. CEO, Michael Horn, assigned sole responsibility to a small circle of individuals, « VW’s senior management later recognized that the misconduct could not be explained simply by the deviant behaviour of a few people, since the evidence also pointed to organizational problems supporting the violation of regulations (18). In December 2015, VW’s management released the following observations, drawn from the preliminary results of its internal investigation:

« Group Audit’s examination of the relevant processes indicates that the software-influenced NOx emissions behavior was due to the interaction of three factors:

– The misconduct and shortcomings of individual employees

– Weaknesses in some processes

– A mindset in some areas of the Company that tolerated breaches of rules » (19).

Concerning the question of process,VW released the following audit key findings:

« Procedural problems in the relevant subdivisions have encouraged misconduct;

Faults in reporting and monitoring systems as well as failure to comply with existing regulations;

IT infrastructure partially insufficient and antiquated. » (20)

More fundamentally, VW’s management pointed out at the same time that the information obtained up to that point on “the origin and development of the nitrogen issue […] proves not to have been a one-time error, but rather a chain of errors that were allowed to happen (21). The starting point was a strategic decision to launch a large-scale promotion of diesel vehicles in the United States in 2005. Initially, it proved impossible to have the EA 189 engine meet by legal means the stricter nitrogen oxide requirements in the United States within the required timeframe and budget » (22).

In other words, this revelation by VW’s management suggests that « the end justified the means » in the sense that the ambitious production targets for the U.S. market and the time and budget constraints imposed on employees encouraged those employees to use illegal methods in operational terms to achieve the company’s objective. And this misconduct could not be detected because of deficiencies in the monitoring and control mechanisms, and especially in the compliance system established by the company to ensure that legal requirements were respected. Among the reasons given to explain the crisis, some observers also pointed to the excessive centralization of decision-making powers within VW’s senior management, and an organizational culture that acted as a brake on internal communications and discouraged mid-level managers from passing on bad news (23).

IV. Organizational Changes Considered as a Preliminary Step

In response to the crisis, VW’s management, in a press release in December 2015, set out the main organizational changes planned to minimize the risk of similar misconduct in the future. The changes mainly involved « instituting a comprehensive new alignment that affects the structure of the Group, as well as is way of thinking and its strategic goals (24).

In structural terms, VW changed the composition of the Group’s Board of Management to include the person responsible for the Integrity and Legal Affairs Department as a board member (25). In the future, the company wanted to give « more importance to digitalization, which will report directly to the Chairman of the Board of Management, » and intended to give « more independence to brand and divisions through a more decentralized management (26). With a view to initiating a new mindset, VW’s management stated that it wanted to avoid « yes-men » and to encourage managers and engineers « who are curious, independent, and pioneering » (27). However, the December 2015 press release reveals little about VW’s strategic objectives: « Strategy 2025, with which Volkswagen will address the main issues for the future, is scheduled to be presented in mid 2016 » (28).

Although VW’s management has not yet provided any details on the specific objectives targeted in its « Strategy 2025 », it is revealing to read the VW annual reports from before 2015 in which the company sets out clear and ambitious objectives for productivity and profitability. For example, the annual reports for 2007, 2009 and 2014 contained the following financial objectives, which the company hoped to reach by 2018.

In its 2007 annual report,VW specified, under the heading « Driving ideas »:

“Financial targets are equally ambitious: for example, the Volkswagen Passenger Cars brand aims to increase its unit sales by over 80 percent to 6.6 million vehicles by 2018, thereby reaching a global market share of approximately 9 percent. To make it one of the most profitable automobile companies as well, it is aiming for an ROI of 21 percent and a return on sales before tax of 9 percent.” (29).

Under the same heading, VW stated in its 2009 annual report:

“In 2018, the Volkswagen Group aims to be the most successful and fascinating automaker in the world. […] Over the long term, Volkswagen aims to increase unit sales to more than 10 million vehicles a year: it intends to capture an above-average share as the major growth markets develop (30).

And in its 2014 annual report, under the heading « Goals and Strategies », VW said:

“The goal is to generate unit sales of more than 10 million vehicles a year; in particular, Volkswagen intends to capture an above-average share of growth in the major growth markets.”

Volkswagen’s aim is a long-term return on sales before tax of at least 8% so as to ensure that the Group’s solid financial position and ability to act are guaranteed even in difficult market periods (31).

Besides these specific objectives for financial performance, the annual reports show that the company’s management recognized, at least on paper, the importance of ensuring regulatory compliance and promoting corporate social responsibility (CSR) and sustainability (31). However, after the scandal broke in September 2015, questions can be asked about the effectiveness of the governance mechanisms, especially of the reporting and monitoring systems put in place by VW to achieve company goals in this area (33). In light of the preliminary results of VW’s internal investigation (34), as mentionned above, it seems that, in the organizational culture, the commitment to promote compliance, CSR and sustainability was not as strong as the effort made to achieve the company’s financial performance objectives.

Concerning the specific and challenging priorities of productivity and profitability established by VW’s management in previous years, the question is whether the promotion of financial objectives such as these created a risk because of the pressure it placed on employees within the organizational environment. The priorities can, of course, exert a positive influence and motivate employees to make an even greater effort to achieve the objectives (35). On the other hand, the same priority can exert a negative influence by potentially encouraging employees to use all means necessary to achieve the performance objectives set, in order to protect their job or obtain a promotion, even if the means they use for that purpose contravene the regulations. In other words, the employees face a « double bind » or dilemma which, depending on the circumstances, can lead them to give preference to the performance priorities set by the company rather than compliance with the applicable legal and ethical standards.

In the management literature, a large number of theoretical and empirical studies emphasize the beneficial effects of the setting of specific and challenging goals on employee motivation and performance within a company (36). However, while recognizing these beneficial effects, some authors point out the unwanted or negative side effects they may have.

As highlighted by Ordóñez, Schweitzer, Galinsky and Bazerman, specific goal setting can result in employees focusing solely on those goals while neglecting other important, but unstated, objectives (37). They also mention that employees motivated by « specific, challenging goals adopt riskier strategies and choose riskier gambles than do those with less challenging or vague goals (38). As an additional unwanted side effet, goal setting can encourage unlawful or unethical behaviour, either by inciting employees to use dishonest methods to meet the performance objectives targeted, or to “misrepresent their performance level – in other words, to report that they met a goal when in fact they fell short (39). Based on these observations, the authors suggest that companies should set their objectives with the greatest care and propose various ways to guard against the unwanted side effects highlighted in their study. This approach could prove useful for VW’s management which will once again, at some point, have to define its objectives and stratégies.

V. Conclusion

In the information released to the public after the emissions cheating scandal broke, as mentioned above, VW’s management quickly stated that the misconduct was directly caused by the individual misbehaviour of a couple of software engineers. Later, however, it admitted that the individual misconduct of a few employees was not the only cause, and that there were also organizational deficiencies within the company itself.

Although the VW Group’s public communications have so far provided few details about the cause of the crisis, the admission by management that both individual and organizational failings were involved constitutes, in our opinion, a lever for understanding the various factors that may have led to reprehensible conduct within the company. Based on the investigations that will be completed over the coming months, VW’s management will be in a position to identify more precisely the nature of these organizational failings and to propose ways to minimize the risk of future violations. During 2016, VW’s management will also announce the objectives and stratégies it intends to pursue over the next few years.

Les conseils d’administration sont de plus en plus confrontés à l’exigence d’évaluer l’efficacité de leur fonctionnement par le biais d’une évaluation annuelle du CA, des comités et des administrateurs.

En fait, le NYSE exige depuis dix ans que les conseils procèdent à leur évaluation et que les résultats du processus soient divulgués aux actionnaires. Également, les investisseurs institutionnels et les activistes demandent de plus en plus d’informations au sujet du processus d’évaluation.

Les résultats de l’évaluation peuvent être divulgués de plusieurs façons, notamment dans les circulaires de procuration et sur le site de l’entreprise.

L’article publié par John Olson, associé fondateur de la firme Gibson, Dunn & Crutcher, professeur invité à Georgetown Law Center, et paru sur le forum du Harvard Law School, présente certaines approches fréquemment utilisées pour l’évaluation du CA, des comités et des administrateurs.

On recommande de modifier les méthodes et les paramètres de l’évaluation à chaque trois ans afin d’éviter la routine susceptible de s’installer si les administrateurs remplissent les mêmes questionnaires, gérés par le président du conseil. De plus, l’objectif de l’évaluation est sujet à changement (par exemple, depuis une décennie, on accorde une grande place à la cybersécurité).

C’est au comité de gouvernance que revient la supervision du processus d’évaluation du conseil d’administration. L’article décrit quatre méthodes fréquemment utilisées.

(1) Les questionnaires gérés par le comité de gouvernance ou une personne externe

(2) les discussions entre administrateurs sur des sujets déterminés à l’avance

(3) les entretiens individuels avec les administrateurs sur des thèmes précis par le président du conseil, le président du comité de gouvernance ou un expert externe.

(4) L’évaluation des contributions de chaque administrateur par la méthode d’auto-évaluation et par l’évaluation des pairs.

Chaque approche a ses particularités et la clé est de varier les façons de faire périodiquement. On constate également que beaucoup de sociétés cotées utilisent les services de spécialistes pour les aider dans leurs démarches.

La quasi-totalité des entreprises du S&P 500 divulgue le processus d’évaluation utilisé pour améliorer leur efficacité. L’article présente deux manières de diffuser les résultats du processus d’évaluation.

(1) Structuré, c’est-à-dire un format qui précise — qui évalue quoi ; la fréquence de l’évaluation ; qui supervise les résultats ; comment le CA a-t-il agi eu égard aux résultats de l’opération d’évaluation.

(2) Information axée sur les résultats — les grandes conclusions ; les facteurs positifs et les points à améliorer ; un plan d’action visant à corriger les lacunes observées.

Notons que la firme de services aux actionnaires ISS (Institutional Shareholder Services) utilise la qualité du processus d’évaluation pour évaluer la robustesse de la gouvernance des sociétés. L’article présente des recommandations très utiles pour toute personne intéressée par la mise en place d’un système d’évaluation du CA et par sa gestion.

Voici trois articles parus sur mon blogue qui abordent le sujet de l’évaluation :

More than ten years have passed since the New York Stock Exchange (NYSE) began requiring annual evaluations for boards of directors and “key” committees (audit, compensation, nominating/governance), and many NASDAQ companies also conduct these evaluations annually as a matter of good governance. [1] With boards now firmly in the routine of doing annual evaluations, one challenge (as with any recurring activity) is to keep the process fresh and productive so that it continues to provide the board with valuable insights. In addition, companies are increasingly providing, and institutional shareholders are increasingly seeking, more information about the board’s evaluation process. Boards that have implemented a substantive, effective evaluation process will want information about their work in this area to be communicated to shareholders and potential investors. This can be done in a variety of ways, including in the annual proxy statement, in the governance or investor information section on the corporate website, and/or as part of shareholder engagement outreach.

To assist companies and their boards in maximizing the effectiveness of the evaluation process and related disclosures, this post provides an overview of several frequently used methods for conducting evaluations of the full board, board committees and individual directors. It is our experience that using a variety of methods, with some variation from year to year, results in more substantive and useful evaluations. This post also discusses trends and considerations relating to disclosures about board evaluations. We close with some practical tips for boards to consider as they look ahead to their next annual evaluation cycle.

Common Methods of Board Evaluation

As a threshold matter, it is important to note that there is no one “right” way to conduct board evaluations. There is room for flexibility, and the boards and committees we work with use a variety of methods. We believe it is good practice to “change up” the board evaluation process every few years by using a different format in order to keep the process fresh. Boards have increasingly found that year-after-year use of a written questionnaire, with the results compiled and summarized by a board leader or the corporate secretary for consideration by the board, becomes a routine exercise that produces few new insights as the years go by. This has been the most common practice, and it does respond to the NYSE requirement, but it may not bring as much useful information to the board as some other methods.

Doing something different from time to time can bring new perspectives and insights, enhancing the effectiveness of the process and the value it provides to the board. The evaluation process should be dynamic, changing from time to time as the board identifies practices that work well and those that it finds less effective, and as the board deals with changing expectations for how to meet its oversight duties. As an example, over the last decade there have been increasing expectations that boards will be proactive in oversight of compliance issues and risk (including cyber risk) identification and management issues.

Three of the most common methods for conducting a board or committee evaluation are: (1) written questionnaires; (2) discussions; and (3) interviews. Some of the approaches outlined below reflect a combination of these methods. A company’s nominating/governance committee typically oversees the evaluation process since it has primary responsibility for overseeing governance matters on behalf of the board.

1. Questionnaires

The most common method for conducting board evaluations has been through written responses to questionnaires that elicit information about the board’s effectiveness. The questionnaires may be prepared with the assistance of outside counsel or an outside advisor with expertise in governance matters. A well-designed questionnaire often will address a combination of substantive topics and topics relating to the board’s operations. For example, the questionnaire could touch on major subject matter areas that fall under the board’s oversight responsibility, such as views on whether the board’s oversight of critical areas like risk, compliance and crisis preparedness are effective, including whether there is appropriate and timely information flow to the board on these issues. Questionnaires typically also inquire about whether board refreshment mechanisms and board succession planning are effective, and whether the board is comfortable with the senior management succession plan. With respect to board operations, a questionnaire could inquire about matters such as the number and frequency of meetings, quality and timeliness of meeting materials, and allocation of meeting time between presentation and discussion. Some boards also consider their efforts to increase board diversity as part of the annual evaluation process.

Many boards review their questionnaires annually and update them as appropriate to address new, relevant topics or to emphasize particular areas. For example, if the board recently changed its leadership structure or reallocated responsibility for a major subject matter area among its committees, or the company acquired or started a new line of business or experienced recent issues related to operations, legal compliance or a breach of security, the questionnaire should be updated to request feedback on how the board has handled these developments. Generally, each director completes the questionnaire, the results of the questionnaires are consolidated, and a written or verbal summary of the results is then shared with the board.

Written questionnaires offer the advantage of anonymity because responses generally are summarized or reported back to the full board without attribution. As a result, directors may be more candid in their responses than they would be using another evaluation format, such as a face-to-face discussion. A potential disadvantage of written questionnaires is that they may become rote, particularly after several years of using the same or substantially similar questionnaires. Further, the final product the board receives may be a summary that does not pick up the nuances or tone of the views of individual directors.

In our experience, increasingly, at least once every few years, boards that use questionnaires are retaining a third party, such as outside counsel or another experienced facilitator, to compile the questionnaire responses, prepare a summary and moderate a discussion based on the questionnaire responses. The desirability of using an outside party for this purpose depends on a number of factors. These include the culture of the board and, specifically, whether the boardroom environment is one in which directors are comfortable expressing their views candidly. In addition, using counsel (inside or outside) may help preserve any argument that the evaluation process and related materials are privileged communications if, during the process, counsel is providing legal advice to the board.

In lieu of asking directors to complete written questionnaires, a questionnaire could be distributed to stimulate and guide discussion at an interactive full board evaluation discussion.

2. Group Discussions

Setting aside board time for a structured, in-person conversation is another common method for conducting board evaluations. The discussion can be led by one of several individuals, including: (a) the chairman of the board; (b) an independent director, such as the lead director or the chair of the nominating/governance committee; or (c) an outside facilitator, such as a lawyer or consultant with expertise in governance matters. Using a discussion format can help to “change up” the evaluation process in situations where written questionnaires are no longer providing useful, new information. It may also work well if there are particular concerns about creating a written record.

Boards that use a discussion format often circulate a list of discussion items or topics for directors to consider in advance of the meeting at which the discussion will occur. This helps to focus the conversation and make the best use of the time available. It also provides an opportunity to develop a set of topics that is tailored to the company, its business and issues it has faced and is facing. Another approach to determining discussion topics is to elicit directors’ views on what should be covered as part of the annual evaluation. For example, the nominating/governance could ask that each director select a handful of possible topics for discussion at the board evaluation session and then place the most commonly cited topics on the agenda for the evaluation.

A discussion format can be a useful tool for facilitating a candid exchange of views among directors and promoting meaningful dialogue, which can be valuable in assessing effectiveness and identifying areas for improvement. Discussions allow directors to elaborate on their views in ways that may not be feasible with a written questionnaire and to respond in real time to views expressed by their colleagues on the board. On the other hand, they do not provide an opportunity for anonymity. In our experience, this approach works best in boards with a high degree of collegiality and a tradition of candor.

3. Interviews

Another method of conducting board evaluations that is becoming more common is interviews with individual directors, done in-person or over the phone. A set of questions is often distributed in advance to help guide the discussion. Interviews can be done by: (a) an outside party such as a lawyer or consultant; (b) an independent director, such as the lead director or the chair of the nominating/governance committee; or (c) the corporate secretary or inside counsel, if directors are comfortable with that. The party conducting the interviews generally summarizes the information obtained in the interview process and may facilitate a discussion of the information obtained with the board.

In our experience, boards that have used interviews to conduct their annual evaluation process generally have found them very productive. Directors have observed that the interviews yielded rich feedback about the board’s performance and effectiveness. Relative to other types of evaluations, interviews are more labor-intensive because they can be time-consuming, particularly for larger boards. They also can be expensive, particularly if the board retains an outside party to conduct the interviews. For these reasons, the interview format generally is not one that is used every year. However, we do see a growing number of boards taking this path as a “refresher”—every three to five years—after periods of using a written questionnaire, or after a major event, such as a corporate crisis of some kind, when the board wants to do an in-depth “lessons learned” analysis as part of its self-evaluation. Interviews also offer an opportunity to develop a targeted list of questions that focuses on issues and themes that are specific to the board and company in question, which can contribute further to the value derived from the interview process.

For nominating/governance committees considering the use of an interview format, one key question is who will conduct the interviews. In our experience, the most common approach is to retain an outside party (such as a lawyer or consultant) to conduct and summarize interviews. An outside party can enhance the effectiveness of the process because directors may be more forthcoming in their responses than they would if another director or a member of management were involved.

Individual Director Evaluations

Another practice that some boards have incorporated into their evaluation process is formal evaluations of individual directors. In our experience, these are not yet widespread but are becoming more common. At companies where the nominating/governance committee has a robust process for assessing the contributions of individual directors each year in deciding whether to recommend them for renomination to the board, the committee and the board may conclude that a formal evaluation every year is unnecessary. Historically, some boards have been hesitant to conduct individual director evaluations because of concerns about the impact on board collegiality and dynamics. However, if done thoughtfully, a structured process for evaluating the performance of each director can result in valuable insights that can strengthen the performance of individual directors and the board as a whole.

As with board and committee evaluations, no single “best practice” has emerged for conducting individual director evaluations, and the methods described above can be adapted for this purpose. In addition, these evaluations may involve directors either evaluating their own performance (self-evaluations), or evaluating their fellow directors individually and as a group (peer evaluations). Directors may be more willing to evaluate their own performance than that of their colleagues, and the utility of self-evaluations can be enhanced by having an independent director, such as the chairman of the board or lead director, or the chair of the nominating/governance committee, provide feedback to each director after the director evaluates his or her own performance. On the other hand, peer evaluations can provide directors with valuable, constructive comments. Here, too, each director’s evaluation results typically would be presented only to that director by the chairman of the board or lead director, or the chair of the nominating/governance committee. Ultimately, whether and how to conduct individual director evaluations will depend on a variety of factors, including board culture.

Disclosures about Board Evaluations

Many companies discuss the board evaluation process in their corporate governance guidelines. [2] In addition, many companies now provide disclosure about the evaluation process in the proxy statement, as one element of increasingly robust proxy disclosures about their corporate governance practices. According to the 2015 Spencer Stuart Board Index, all but 2% of S&P 500 companies disclose in their proxy statements, at a minimum, that they conduct some form of annual board evaluation.

In addition, institutional shareholders increasingly are expressing an interest in knowing more about the evaluation process at companies where they invest. In particular, they want to understand whether the board’s process is a meaningful one, with actionable items emerging from the evaluation process, and not a “check the box” exercise. In the United Kingdom, companies must report annually on their processes for evaluating the performance of the board, its committees and individual directors under the UK Corporate Governance Code. As part of the code’s “comply or explain approach,” the largest companies are expected to use an external facilitator at least every three years (or explain why they have not done so) and to disclose the identity of the facilitator and whether he or she has any other connection to the company.

In September 2014, the Council of Institutional Investors issued a report entitled Best Disclosure: Board Evaluation (available here), as part of a series of reports aimed at providing investors and companies with approaches to and examples of disclosures that CII considers exemplary. The report recommended two possible approaches to enhanced disclosure about board evaluations, identified through an informal survey of CII members, and included examples of disclosures illustrating each approach. As a threshold matter, CII acknowledged in the report that shareholders generally do not expect details about evaluations of individual directors. Rather, shareholders “want to understand the process by which the board goes about regularly improving itself.” According to CII, detailed disclosure about the board evaluation process can give shareholders a “window” into the boardroom and the board’s capacity for change.

The first approach in the CII report focuses on the “nuts and bolts” of how the board conducts the evaluation process and analyzes the results. Under this approach, a company’s disclosures would address: (1) who evaluates whom; (2) how often the evaluations are done; (3) who reviews the results; and (4) how the board decides to address the results. Disclosures under this approach do not address feedback from specific evaluations, either individually or more generally, or conclusions that the board has drawn from recent self-evaluations. As a result, according to CII, this approach can take the form of “evergreen” proxy disclosure that remains similar from year to year, unless the evaluation process itself changes.

The second approach focuses more on the board’s most recent evaluation. Under this approach, in addition to addressing the evaluation process, a company’s disclosures would provide information about “big-picture, board-wide findings and any steps for tackling areas identified for improvement” during the board’s last evaluation. The disclosures would identify: (1) key takeaways from the board’s review of its own performance, including both areas where the board believes it functions effectively and where it could improve; and (2) a “plan of action” to address areas for improvement over the coming year. According to CII, this type of disclosure is more common in the United Kingdom and other non-U.S. jurisdictions.

Also reflecting a greater emphasis on disclosure about board evaluations, proxy advisory firm Institutional Shareholder Services Inc. (“ISS”) added this subject to the factors it uses in evaluating companies’ governance practices when it released an updated version of “QuickScore,” its corporate governance benchmarking tool, in Fall 2014. QuickScore views a company as having a “robust” board evaluation policy where the board discloses that it conducts an annual performance evaluation, including evaluations of individual directors, and that it uses an external evaluator at least every three years (consistent with the approach taken in the UK Corporate Governance Code). For individual director evaluations, it appears that companies can receive QuickScore “credit” in this regard where the nominating/governance committee assesses director performance in connection with the renomination process.

What Companies Should Do Now

As noted above, there is no “one size fits all” approach to board evaluations, but the process should be viewed as an opportunity to enhance board, committee and director performance. In this regard, a company’s nominating/governance committee and board should periodically assess the evaluation process itself to determine whether it is resulting in meaningful takeaways, and whether changes are appropriate. This includes considering whether the board would benefit from trying new approaches to the evaluation process every few years.

Factors to consider in deciding what evaluation format to use include any specific objectives the board seeks to achieve through the evaluation process, aspects of the current evaluation process that have worked well, the board’s culture, and any concerns directors may have about confidentiality. And, we believe that every board should carefully consider “changing up” the evaluation process used from time to time so that the exercise does not become rote. What will be the most beneficial in any given year will depend on a variety of factors specific to the board and the company. For the board, this includes considerations of board refreshment and tenure, and developments the board may be facing, such as changes in board or committee leadership. Factors relevant to the company include where the company is in its lifecycle, whether the company is in a period of relative stability, challenge or transformation, whether there has been a significant change in the company’s business or a senior management change, whether there is activist interest in the company and whether the company has recently gone through or is going through a crisis of some kind. Specific items that nominating/governance committees could consider as part of maintaining an effective evaluation process include:

Revisit the content and focus of written questionnaires. Evaluation questionnaires should be updated each time they are used in order to reflect significant new developments, both in the external environment and internal to the board.

“Change it up.” If the board has been using the same written questionnaire, or the same evaluation format, for several years, consider trying something new for an upcoming annual evaluation. This can bring renewed vigor to the process, reengage the participants, and result in more meaningful feedback.

Consider whether to bring in an external facilitator. Boards that have not previously used an outside party to assist in their evaluations should consider whether this would enhance the candor and overall effectiveness of the process.

Engage in a meaningful discussion of the evaluation results. Unless the board does its evaluation using a discussion format, there should be time on the board’s agenda to discuss the evaluation results so that all directors have an opportunity to hear and discuss the feedback from the evaluation.

Incorporate follow-up into the process. Regardless of the evaluation method used, it is critical to follow up on issues and concerns that emerge from the evaluation process. The process should include identifying concrete takeaways and formulating action items to address any concerns or areas for improvement that emerge from the evaluation. Senior management can be a valuable partner in this endeavor, and should be briefed as appropriate on conclusions reached as a result of the evaluation and related action items. The board also should consider its progress in addressing these items.

Revisit disclosures. Working with management, the nominating/governance committee and the board should discuss whether the company’s proxy disclosures, investor and governance website information and other communications to shareholders and potential investors contain meaningful, current information about the board evaluation process.

Endnotes: