On me demande souvent de proposer un livre qui fait le tour de la question eu égard à ce qui est connu comme statistiquementvalide sur les relations entre la gouvernance et le succès des organisations (i.e. la performance financière !)

Voici un article de James McRitchie, publié dans Corporate governance, qui commente succinctement le dernier volume de Richard Leblanc.

Comme je l’ai déjà mentionné dans un autre billet, le livre de Richard Leblanc est certainement l’un des plus importants ouvrages (sinon le plus important) portant sur la gouvernance du conseil d’administration.

Mentionnons également que le volume publié par David F. Larckeret Brian Tayan, professeurs au Graduate School de l’Université Stanford, en est à sa deuxième édition et il donne l’heure juste sur l’efficacité des principes de gouvernance. Voici une brève présentation du volume de Larcker.

Je vous recommande donc vivement de vous procurer ces volumes.

Enfin, je profite de l’occasion pour vous indiquer que je viens de recevoir la dernière version des Principes de gouvernance d’entreprise du G20 et de l’OCDEen français et j’ai suggéré au Collège des administrateurs de sociétés (CAS) d’inclure cette publication dans la section Nouveauté du site du CAS.

Il s’agit d’une publication très attendue dans le monde de la gouvernance. La documentation des organismes internationaux est toujours d’abord publiée en anglais. Ce document en français de l’OCDE sur les principes de gouvernance est la bienvenue !

Voici un excellent article partagé par Paul Michaud, ASC, et publié dans The Economist.

Il y a plusieurs pratiques du management et de la gouvernance à revoir à l’âge des grandes entreprises internationales qui se démarquent par l’excellence de leur modèle d’acquisiteur, de consolidateur et de synergiste.

Incumbents have always had a tendency to grow fat and complacent. In an era of technological disruption, that can be lethal. New technology allows companies to come from nowhere (as Nokia once did) and turn entire markets upside down. Challengers can achieve scale faster than ever before. According to Bain, a consultancy, successful new companies reach Fortune 500 scale more than twice as fast as they did two decades ago. They can also take on incumbents in completely new ways: Airbnb is competing with the big hotel chains without buying a single hotel.

Vous trouverez, ci-dessous un bref extrait de cet article que je vous encourage à lire.

IN SEPTEMBER 2009 Fast Company magazine published a long article entitled “Nokia rocks the world”. The Finnish company was the world’s biggest mobile-phone maker, accounting for 40% of the global market and serving 1.1 billion users in 150 countries, the article pointed out. It had big plans to expand into other areas such as digital transactions, music and entertainment. “We will quickly become the world’s biggest entertainment media network,” a Nokia vice-president told the magazine.

It did not quite work out that way. Apple was already beginning to eat into Nokia’s market with its smartphones. Nokia’s digital dreams came to nothing. The company has become a shadow of its former self. Having sold its mobile-phone business to Microsoft, it now makes telecoms network Equipment.

There are plenty of examples of corporate heroes becoming zeros: think of BlackBerry, Blockbuster, Borders and Barings, to name just four that begin with a “b”. McKinsey notes that the average company’s tenure on the S&P 500 list has fallen from 61 years in 1958 to just 18 in 2011, and predicts that 75% of current S&P 500 companies will have disappeared by 2027. Ram Charan, a consultant, argues that the balance of power has shifted from defenders to attackers.

Incumbents have always had a tendency to grow fat and complacent. In an era of technological disruption, that can be lethal. New technology allows companies to come from nowhere (as Nokia once did) and turn entire markets upside down. Challengers can achieve scale faster than ever before. According to Bain, a consultancy, successful new companies reach Fortune 500 scale more than twice as fast as they did two decades ago. They can also take on incumbents in completely new ways: Airbnb is competing with the big hotel chains without buying a single hotel.

Next in line for disruption, some say, are financial services and the car industry. Anthony Jenkins, a former chief executive of Barclays, a bank, worries that banking is about to experience an “Uber moment”. Elon Musk, a founder of Tesla Motors, hopes to dismember the car industry (as well as colonise Mars).

It is perfectly possible that the consolidation described so far in this special report will prove temporary. But two things argue against it. First, a high degree of churn is compatible with winner-takes-most markets. Nokia and Motorola have been replaced by even bigger companies, not dozens of small ones. Venture capitalists are betting on continued consolidation, increasingly focusing on a handful of big companies such as Tesla. Sand Hill Road, the home of Silicon Valley’s venture capitalists, echoes with talk of “decacorns” and “hyperscaling”.

Second, today’s tech giants have a good chance of making it into old age. They have built a formidable array of defences against their rivals. Most obviously, they are making products that complement each other. Apple’s customers usually buy an entire suite of its gadgets because they are designed to work together. The tech giants are also continuously buying up smaller companies. In 2012 Facebook acquired Instagram for $1 billion, which works out at $30 for each of the service’s 33m users. In 2014 Facebook bought WhatsApp for $22 billion, or $49 for each of the 450m users. This year Microsoft spent $26.2 billion on LinkedIn, or $60.5 for each of the 433m users. Companies that a decade ago might have gone public, such as Nest, a company that makes remote-control gadgets for the home, and Waze, a mapping service, are now being gobbled up by established giants.

Voici un récent article publié par Julie Hembrock Daum, directrice à Spencer Stuart et Susan Stauberg, PDG à Fondation WomenCorporateDirectors.

Cet article a été publié dans le Harvard Law School Forum aujourd’hui et il présente l’état de la gouvernance à l’échelle internationale (60 pays) en mettant particulièrement l’accent sur la diversité et les différences de perception entre les hommes et les femmes qui occupent des postes d’administrateurs de grandes sociétés privées ou publiques.

On me demande souvent de proposer des références en relation avec la gouvernance globale. Les gens veulent connaître les tendances et les progrès des efforts entrepris dans le domaine de la diversité dans le monde.

L’enquête citée ci-dessous fournit des données actuelles sur les principaux enjeux concernant les Board.

Je crois que tous les gestionnaires seront intéressés par la présentation succincte, claire et bien illustrée des données de la mondialisation de la gouvernance.

The growing demands on corporate boards are transforming boardrooms globally, with directors taking on a more strategic, dynamic and responsive role to help steer their companies through a hypercompetitive and volatile business environment. Economic and political uncertainties make long-term planning more difficult. The proliferation of cyber attacks—and their consequences for business in financial olosses and reputational damage—increases the scope of risk oversight. A rise in institutional and activist shareholder activity requires boards to identify vulnerabilities in board renewal and performance and, in some cases, establish protocols for engagement. And all of these demands have pushed issues around board composition and diversity to the fore, as boards cannot afford to have directors around the table who aren’t delivering value.

Boardroom presentation

In this context, Spencer Stuart, the WomenCorporateDirectors (WCD) Foundation, Professor Boris Groysberg and doctoral candidate Yo-Jud Cheng of Harvard Business School and researcher Deborah Bell partnered together on the 2016 Global Board of Directors Survey, one of the most comprehensive surveys of corporate directors around the world.

We received responses from more than 4,000 male and female directors from 60 countries, providing a comprehensive snapshot of the business climate and strategic priorities as seen from the boardroom of many of the world’s top public and large, privately held companies.

The survey explores in depth how boards think and operate. It captures in detail the governance practices, strategic priorities and views on board effectiveness of corporate directors around the world. It also confirmed many of our observations from working with boards. The economy is top of mind, and many directors are uncertain about economic prospects and not seeing growth in the future. At the same time, directors are responding proactively to the many new demands they face, looking for opportunities to enhance composition and improve board performance.

Findings compare and contrast the views between male and female corporate board directors, and highlight similarities and differences between public and private companies and among directors from different regions in five key areas:

Political and economic landscape

Company strategy and risks

Board governance and effectiveness

Board diversity and quotas

Director identification and recruitment

This post highlights key findings around these topics, providing directors an overview of how their peers view their own boards and the challenges that their companies face. In subsequent reports, we will dive deeper into specific governance areas and explore additional perspectives on board composition, risk areas, and strengths and weaknesses in boardrooms today.

Key Findings

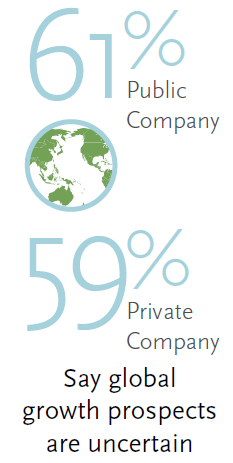

Political and Economic Landscape: Uncertainty dominates boardroom outlook.

Our survey finds that directors around the world are uncertain about global growth prospects, with directors in North America and Western Europe least confident about the prospects for growth. Sixty-three percent of directors in these regions see uncertain economic conditions, compared with 36% in Asia and 40% in Africa.

Only 2% of directors across all regions predict a period of strong global growth over the next three years, while 16% expect a global slowdown. “This pessimism about growth is one of the most surprising findings of our survey,” said Boris Groysberg of Harvard Business School. “It seems that the market volatility and low prospects for growth as well as the unpredictable economic outlook are what keep board members awake at night.”

More than one-third of directors of companies headquartered in Asia and roughly one-quarter of directors of companies in Australia/New Zealand expect relatively faster growth in emerging economies versus developed countries.

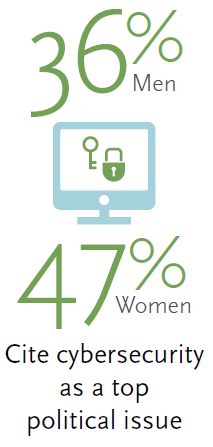

Political and Economic Landscape: Economy, regulations and cybersecurity top issues for directors.

Across all industries and regions, directors rank the economy and the regulatory environment as the political issues most relevant to them. Cybersecurity is an increasingly important issue in many regions. More than one-third of directors of companies in Australia/New Zealand, North America and Western Europe say cybersecurity is a top issue. “Cybersecurity continues to be a leading issue on the agenda from a regulatory, reputational and contingency standpoint,” says Julie Hembrock Daum, head of Spencer Stuart’s North American Board Practice.

“We see boards considering a number of different approaches to getting smart about the broader impact of technology on the business. In certain cases they have added a director with a strong digital or security background. However, the board should not isolate cybersecurity responsibility with just this one board member, but continue to view cybersecurity as a full board priority.”

Political instability is a concern in several regions. In Central and South America, one-half of directors cite political instability as an issue. Corporate tax rates are an issue particularly in North America.

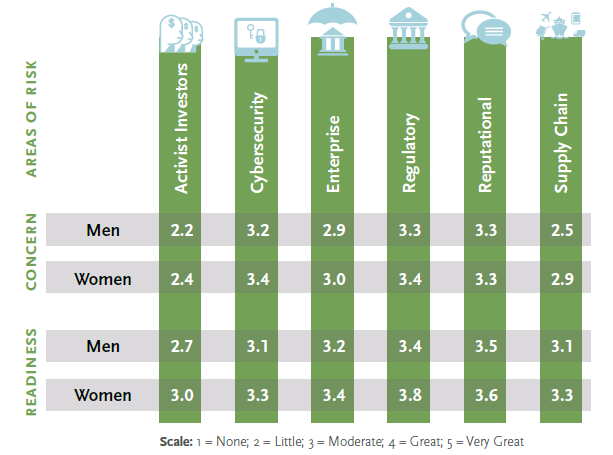

Company Risks: Women directors report higher concerns about risk than male directors.

Directors globally express the most concern about regulatory and reputational risks, followed by cybersecurity, and less about activist investors and supply chain risks. In general, directors report that their companies are prepared to handle the most important risks, with companies’ level of readiness matching the most concerning areas of risk. However, directors of private companies systematically rank their boards as being less prepared versus public company boards when it comes to such risks.

Nearly across the board, female directors report a higher level of concern about various risks to a company than their male peers—from concerns about activist investors and cybersecurity to regulatory risk and the supply chain. However, female directors also feel that their companies have a higher level of readiness to address these risks than do their male cohorts.

Susan Stautberg, chairman and CEO of the WCD Foundation, believes that women directors may be educating themselves more about the potential risks:

“We believe that women in particular bring a real thirst for knowledge and curiosity to their board service, and this includes getting up-to-speed on what the real risks are to an organization. All good directors do this, but we think being relatively new to the boardroom can create a greater sense of urgency to learn.”

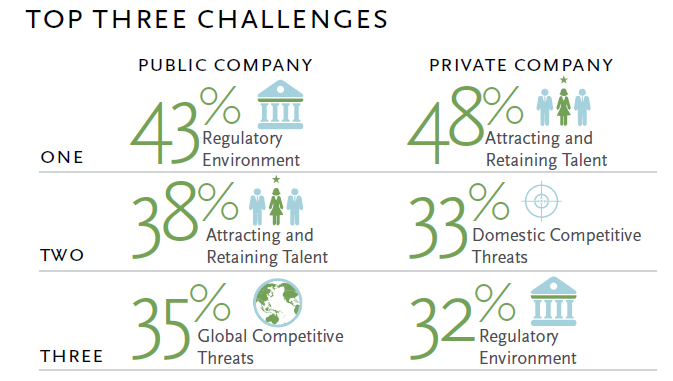

Strategy: Top challenges differ for public and private companies.

Talent, regulations, global and domestic competition, and innovation are seen by directors as the top impediments to achieving their companies’ strategic objectives. How those challenges rank specifically depends in part on whether directors are serving public or private companies.

Nearly half of private company directors (versus 38% of public company directors) rate attracting and retaining talent as a key challenge to achieving their company’s strategic objectives. This is followed by domestic competitive threats, the regulatory environment, innovation and global competitive threats. Among public companies, 43% of directors (versus 32% of private company directors) say the regulatory environment is a top challenge, followed by attracting and retaining talent, global competitive threats, innovation and domestic competitive threats.

“This was interesting because we do see in larger, more established public companies a greater maturity in their HR processes and deeper resources invested in talent management and development,” says Daum. “Identifying and recruiting individuals who fit the culture, bring impact to the organization and endure is a high priority for nearly all companies. However, many private companies, which tend to be smaller and have less brand awareness as a whole, often have less robust HR structures to attract the level of talent across the organization.”

Perceived challenges also differ somewhat by industry and region, with the regulatory environment being more concerning for companies in the energy/utilities, financials/professional services and healthcare industries, and in Asia, Australia/New Zealand, North America and Western Europe. Global competitive threats are the leading concern for companies in the industrials and materials sectors, and in Western Europe.

Interestingly, while cybersecurity is viewed as an important risk, few directors consider it a major challenge to achieving strategic objectives. Similarly, activist shareholders, compensation, cost of commodities and supply chain risk are not perceived as challenges to achieving strategic goals.

Boardroom Grades: Directors consider boards weaker in people-related processes.

On average, directors rate their board’s overall performance as being slightly above average (3.7 out of 5). Directors see their boards as having the strongest processes related to staying current on the company and the industry, compliance, financial planning and board composition, and weakest in cybersecurity, the evaluation of individual directors, CEO succession planning and HR/talent management.

“These ratings underscore directors’ views that attracting and retaining top talent is a common challenge, and underline the need for these HR competencies on boards,” says Stautberg. Harvard Business School doctoral candidate Yo-Jud Cheng adds, “Despite the fact that directors recognize their weaknesses in these areas, boards continue to prioritize more conventional areas of expertise, such as industry knowledge and auditing, in their appointments of new directors.”

Public company directors rate their overall board performance slightly higher than private company directors (3.8 versus 3.4) and give themselves higher marks for creating effective board structures, evaluation of individual directors, cybersecurity and compliance. We also see some variation across regions.

Board Turnover: Directors—especially women—favor tools to trigger change.

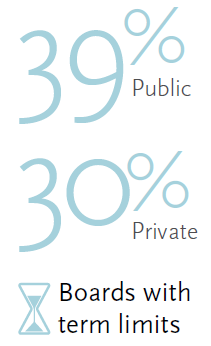

A little more than one-third of boards have term limits for directors, averaging six years, while approximately one-quarter of boards have a mandatory retirement age, averaging 72 years. Boards in Western Europe are most likely to have term limits, and boards in North America are least likely to set term limits. However, boards in North America are more likely to have a mandatory retirement age than boards in Western Europe (34% versus 18%). We also see a stark contrast between public and private companies in both term limits (39% versus 30%) and mandatory retirement ages (33% versus 12%).

While these tools for triggering director turnover generally have not been widely adopted, the survey indicates that directors favor adoption of such mechanisms. Sixty percent of directors think that boards should have mandatory term limits for directors, and 45% think that there should be a mandatory retirement age. Even in private companies, which are considerably less likely to adopt these practices today, directors shared similar opinions as compared to their counterparts in public companies. Female directors even more strongly support triggers for turnover; 68% (versus 56% of men) favor director term limits and 57% (versus 39% of men) support mandatory retirement ages.

“It was encouraging to see the majority of respondents in favor of retirement ages and term limits. Turnover among S&P 500 companies has trended at 5% to 7%—roughly 300 to 350 seats a year. Boards need tools they can use to ensure that new perspectives and thinking are regularly being brought to the boardroom,” says Daum. “This isn’t just an issue tied to activist shareholders, but something institutional shareholders are asking about as well: what are boards doing to ensure independent and fresh thinking?”

Not surprisingly, 43% of directors believe that a director loses his or her independence after about 10 years. Respondents from North America are less likely to tie director independence to years served, with only one-third agreeing that a director loses independence after a certain amount of time on the board.

Public companies represented in the survey have larger boards than private companies—on average 8.9 directors versus 7.6—and a larger representation of independent directors, 74% versus 54%. Yet, public and private company boards are similar in terms of the representation of women, minorities and new directors. On average, 18% of board members are women, 7% are ethnic minorities and 13% have been appointed in the past 12 months.

“This finding was very interesting. There has been much debate about the use and effectiveness of quotas. To see the relative parity of diversity among public and private companies reinforces that the tone needs to come from the top regarding bringing a fresh, diverse perspective representative of the company’s stakeholders and interests,” says Daum. Groysberg adds, “Although we are hearing more talk about the importance of diversity from boards, it’s not necessarily translating into numbers. Unfortunately, we haven’t seen as much progress as we were hoping for compared to our past survey on the diversity of boards.”

Boards are largest in the financials/professional services sector (9.1 directors) and smallest in the IT/telecom sector (7.5 directors). Female representation is highest (20% or more) in the consumer staples, financial services/professional services and consumer discretionary sectors, and lowest in IT/telecom (13%).

Looking across regions, board size is smallest in Australia/New Zealand, where boards average 6.7 members, as compared to the global average of 8.5 members. Boards in Australia/New Zealand and North America have the highest proportion of independent directors, and boards in Asia have the lowest proportion. Female representation is lowest in Central and South America and Asia.

Boardroom Diversity: Why isn’t the number of women on boards increasing?

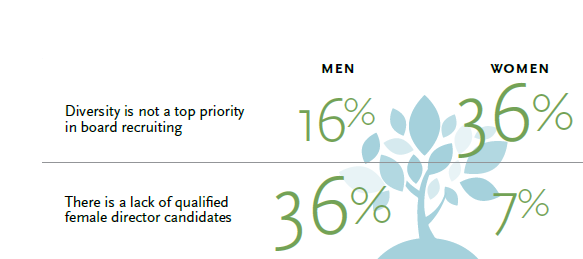

As the percentage of women on boards remains stagnant, there is both a gender divide and a generation divide on why this is. Male directors, especially older respondents, report the “lack of qualified female candidates,” while women directors most often cite the fact that diversity is not a priority in board recruiting and that traditional networks tend to be male-dominated. Younger male directors surveyed (those 55 and younger) are inclined to agree with women that traditional networks tend to be male-dominated. “Men in the younger generation, I think, just see their qualified female colleagues out there, but know that the traditional board networks still tend to be male,” says Stautberg. “It’s often hard to see an informal ‘network’ if you are in the middle of it, but you can see it very clearly when you’re on the outside.”

Boardroom Diversity: Quotas not supported overall.

Nearly 75% of surveyed directors do not personally support boardroom diversity quotas, but support for quotas varies significantly by gender and, to a lesser degree, by age. Forty-nine percent of female directors support diversity quotas, but only 9% of male directors do. Older women are less likely to favor quotas than younger women; 67% of female directors ages 55 and younger personally support boardroom quotas, compared with 36% of female directors over 55 (the majority of male directors, of any age, do not support quotas). Female directors also are more likely to be in favor of government regulatory agencies requiring boards to disclose specific practices/steps being taken to seat diverse candidates (43% versus 14% of male directors).

If quotas aren’t the answer, what do directors think would increase board diversity? Male and female directors agree that having board leadership that champions board diversity is the most effective way to build diverse corporate boards. Men feel more strongly than women that efforts to develop a pipeline of diverse board candidates through director advocacy, mentorship and training is an effective way to increase diversity.

Directors as a whole agree that shareholder pressure and board targets are less effective tools for increasing board diversity.

Boardroom Diversity: Search firms have been successful in expanding the talent pool of qualified female directors.

Directors take a variety of pathways to the boardroom: in roughly equal measures, directors were known to the board or another director, recruited by a search firm or known by the CEO. Public company directors are more likely to be recruited by an executive search firm than private company directors, while private company directors are more likely to have been appointed by a major shareholder.

The survey highlights gender differences, as well, in the paths to the boardroom. Female directors are more likely than their male counterparts to have been recruited by an executive search firm, while male directors are more likely to have been appointed by a major shareholder. “Search firms may be able to open doors that networking opportunities may not have been doing until relatively recently, at least for women,” says Stautberg. “Building up networks and getting known is something that women directors are engaging in much more actively now.”

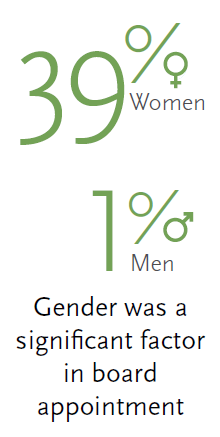

And, indeed, 39% of female directors report that their gender was a significant factor in their board appointment, versus 1% of men.

Conclusion

Corporate boards face no shortage of challenges—from economic uncertainty to strategic and competitive shifts to a dynamic set of risks. Investor attention to board performance and governance has also escalated, and many boards are holding themselves to higher standards. Directors want to ensure that their boards contribute at the highest level, incorporating diverse perspectives, aligning with shareholder interests and setting a positive tone at the top for the organization.

Yet our research has revealed a gap between best practice and reality, especially in areas such as board diversity, HR/talent management, CEO succession planning and director evaluations. But the study provides hope that boards will make progress, as directors support practices that can help promote change. Future research is needed to track progress on these fronts and to study the impact of measures such as quotas and diversity on board performance.

Amid the many challenges confronting corporations—and the growing expectations on corporate boards—directors must be thoughtful about defining the skill sets needed around the board table and diligent in recruiting the right directors, planning for CEO succession and evaluating their own performance. In this way, they will be best positioned to contribute at the high levels which they are demanding of themselves, and to which others are holding them accountable.

*Julie Hembrock Daum leads the North American Board Practice at Spencer Stuart, and Susan Stautberg is the Chairman and CEO of the WomenCorporateDirectors Foundation. This post relates to the 2016 Global Board of Directors Survey, a co-publication from Spencer Stuart and the WCD Foundation authored by Ms. Daum; Ms. Stautberg; Dr. Boris Groysberg, Richard P. Chapman Professor of Business Administration at Harvard Business School; Yo-Jud Cheng, doctoral candidate at Harvard Business School; and Deborah Bell, researcher.

Voici un cas de gouvernance publié sur le site de Julie Garland McLellan* qui concerne les relations entre la présidente du conseil et sa fille nouvellement nommée comme CEO de cette entreprise privée de taille moyenne.

Le cas illustre le processus de transition familiale et les efforts à exercer afin de ne pas interférer avec les affaires de l’entreprise.

Il s’agit d’un cas très fréquent dans les entreprises familiales. Comment Hannah peut-elle continuer à faire profiter sa fille de ses conseils tout en s’assurant de ne pas empiéter sur ses responsabilités ?

Le cas présente la situation de manière assez succincte, mais explicite ; puis, trois experts en gouvernance se prononcent sur le dilemme qui se présente aux personnes qui vivent des situations similaires.

Bonne lecture ! Vos commentaires sont toujours les bienvenus.

Hannah prepared for the transition. She did a course of director education and understands her duties as a non-executive. She loves her daughter, trusts her judgement as CEO and genuinely wants to see her succeed. Nothing is going wrong but Hannah can’t help interfering. She is bored and longs for the days when she could visit customers or sit and strategise with her management team.

Once a week she has a formal meeting with the CEO in her office. In between times she is in frequent contact. Although by mutual agreement these contacts should be purely social or family oriented Hannah finds herself talking business and is hurt when her daughter suggests they leave it for the weekly meeting or put it onto the board agenda.

Over the past few months Hannah has improved governance, record-keeping, training and succession planning systems but she is running out of projects she can do without undermining her daughter. She also recognises that, as a medium sized unlisted business, the company does not need any more governance structures.

How can Hannah find fulfilment in her new role?

Paul’s Answer …..

Julie’s Answer ….

Jakob’s Answer ….

*Julie Garland McLellan is a practising non-executive director and board consultant based in Sydney, Australia.

Vous trouverez, ci-dessous, les dix thèmes les plus importants pour les administrateurs de sociétés selon Kerry E. Berchem, associé du groupe de pratiques corporatives à la firme Akin Gump Strauss Hauer & Feld LLP. Cet article est paru aujourd’hui sur le blogue le Harvard Law School Forum on Corporate Governance.

Bien qu’il y ait peu de changements dans l’ensemble des priorités cette année, on peut quand même noter :

(1) l’accent crucial accordé au long terme ;

(2) Une bonne gestion des relations avec les actionnaires dans la foulée du nombre croissant d’activités menées par les activistes ;

(3) Une supervision accrue des activités liées à la cybersécurité…

Pour plus de détails sur chaque thème, je vous propose la lecture synthèse de l’article ci-dessous.

U.S. public companies face a host of challenges as they enter 2016. Here is our annual list of hot topics for the boardroom in the coming year:

Oversee the development of long-term corporate strategy in an increasingly interdependent and volatile world economy

Cultivate shareholder relations and assess company vulnerabilities as activist investors target more companies with increasing success

Oversee cybersecurity as the landscape becomes more developed and cyber risk tops director concerns

Oversee risk management, including the identification and assessment of new and emerging risks

Assess the impact of social media on the company’s business plans

Stay abreast of Delaware law developments and other trends in M&A

Review and refresh board composition and ensure appropriate succession

Monitor developments that could impact the audit committee’s already heavy workload

Set appropriate executive compensation as CEO pay ratios and income inequality continue to make headlines

Prepare for and monitor developments in proxy access

Strategic Planning Considerations

Strategic planning continues to be a high priority for directors and one to which they want to devote more time. Figuring out where the company wants to—and where it should want to—go and how to get there is not getting any easier, particularly as companies find themselves buffeted by macroeconomic and geopolitical events over which they have no control.

In addition to economic and geopolitical uncertainty, a few other challenges and considerations for boards to keep in mind as they strategize for 2016 and beyond include:

finding ways to drive top-line growth

focusing on long-term goals and enhancing long-term shareholder value in the face of mounting pressures to deliver short-term results

the effect of low oil and gas prices

figuring out whether and when to deploy growing cash stockpiles

assessing the opportunities and risks of climate change and resource scarcity

addressing corporate social responsibility.

Shareholder Activism

Shareholder activism and “suggestivism” continue to gain traction. With the success that activists have experienced throughout 2015, coupled with significant new money being allocated to activist funds, there is no question that activism will remain strong in 2016.

In the first half of 2015, more than 200 U.S. companies were publicly subjected to activist demands, and approximately two-thirds of these demands were successful, at least in part. [1] A much greater number of companies are actually targeted by activism, as activists report that less than a third of their campaigns actually become public knowledge. [2] Demands have continued, and will continue, to vary: from requests for board representation, the removal of officers and directors, launching a hostile bid, advocating specific business strategies and/or opining on the merit of M&A transactions. But one thing is clear: the demands are being heard. According to a recent survey of more than 350 mutual fund managers, half had been contacted by an activist in the past year, and 45 percent of those contacted decided to support the activist. [3]

With the threat of activism in the air, boards need to cultivate shareholder relations and assess company vulnerabilities. Directors—who are charged with overseeing the long-term goals of their companies—must also understand how activists may look at the company’s strategy and short-term results. They must understand what tactics and tools activists have available to them. They need to know and understand what defenses the company has in place and whether to adopt other protective measures for the benefit of the overall organization and stakeholders.

Cybersecurity

Nearly 90 percent of CEOs worry that cyber threats could adversely impact growth prospects. [4] Yet in a recent survey, nearly 80 percent of the more than 1,000 information technology leaders surveyed had not briefed their board of directors on cybersecurity in the last 12 months. [5] The cybersecurity landscape has become more developed and as such, companies and their directors will likely face stricter scrutiny of their protection against cyber risk. Cyber risk—and the ultimate fall out of a data breach—should be of paramount concern to directors.

One of the biggest concerns facing boards is how to provide effective oversight of cybersecurity. The following are questions that boards should be asking:

Governance. Has the board established a cybersecurity review > committee and determined clear lines of reporting and > responsibility for cyber issues? Does the board have directors with the necessary expertise to understand cybersecurity and related issues?

Critical asset review. Has the company identified what its highest cyber risks assets are (e.g., intellectual property, personal information and trade secrets)? Are sufficient resources allocated to protect these assets?

Threat assessment. What is the daily/weekly/monthly threat report for the company? What are the current gaps and how are they being resolved?

Incident response preparedness. Does the company have an incident response plan and has it been tested in the past six months? Has the company established contracts via outside counsel with forensic investigators in the event of a breach to facilitate quick response and privilege protection?

Employee training. What training is provided to employees to help them identify common risk areas for cyber threat?

Third-party management. What are the company’s practices with respect to third parties? What are the procedures for issuing credentials? Are access rights limited and backdoors to key data entry points restricted? Has the company conducted cyber due diligence for any acquired companies? Do the third-party contracts contain proper data breach notification, audit rights, indemnification and other provisions?

Insurance. Does the company have specific cyber insurance and does it have sufficient limits and coverage?

Risk disclosure. Has the company updated its cyber risk disclosures in SEC filings or other investor disclosures to reflect key incidents and specific risks?

The SEC and other government agencies have made clear that it is their expectation that boards actively manage cyber risk at an enterprise level. Given the complexity of the cybersecurity inquiry, boards should seriously consider conducting an annual third-party risk assessment to review current practices and risks.

Risk Management

Risk management goes hand in hand with strategic planning—it is impossible to make informed decisions about a company’s strategic direction without a comprehensive understanding of the risks involved. An increasingly interconnected world continues to spawn newer and more complex risks that challenge even the best-managed companies. How boards respond to these risks is critical, particularly with the increased scrutiny being placed on boards by regulators, shareholders and the media. In a recent survey, directors and general counsel identified IT/cybersecurity as their number one worry, and they also expressed increasing concern about corporate reputation and crisis preparedness. [6]

Given the wide spectrum of risks that most companies face, it is critical that boards evaluate the manner in which they oversee risk management. Most companies delegate primary oversight responsibility for risk management to the audit committee. Of course, audit committees are already burdened with a host of other responsibilities that have increased substantially over the years. According to Spencer Stuart’s 2015 Board Index, 12 percent of boards now have a stand-alone risk committee, up from 9 percent last year. Even if primary oversight for monitoring risk management is delegated to one or more committees, the entire board needs to remain engaged in the risk management process and be informed of material risks that can affect the company’s strategic plans. Also, if primary oversight responsibility for particular risks is assigned to different committees, collaboration among the committees is essential to ensure a complete and consistent approach to risk management oversight.

Social Media

Companies that ignore the significant influence that social media has on existing and potential customers, employees and investors, do so at their own peril. Ubiquitous connectivity has profound implications for businesses. In addition to understanding and encouraging changes in customer relationships via social media, directors need to understand and weigh the risks created by social media. According to a recent survey, 91 percent of directors and 79 percent of general counsel surveyed acknowledged that they do not have a thorough understanding of the social media risks that their companies face. [7]

As part of its oversight duties, the board of directors must ensure that management is thoughtfully addressing the strategic opportunities and challenges posed by the explosive growth of social media by probing management’s knowledge, plans and budget decisions regarding these developments. Given new technology and new social media forums that continue to arise, this is a topic that must be revisited regularly.

M&A Developments

M&A activity has been robust in 2015 and is on track for another record year. According to Thomson Reuters, global M&A activity exceeded $3.2 trillion with almost 32,000 deals during the first three quarters of 2015, representing a 32 percent increase in deal value and a 2 percent increase in deal volume compared to the same period last year. The record deal value mainly results from the increase in mega-deals over $10 billion, which represented 36 percent of the announced deal value. While there are some signs of a slowdown in certain regions based on deal volume in recent quarters, global M&A is expected to carry on its strong pace in the beginning of 2016.

Directors must prepare for possible M&A activity in the future by keeping abreast of developments in Delaware case law and other trends in M&A. The Delaware courts churned out several noteworthy decisions in 2015 regarding M&A transactions that should be of interest to directors, including decisions on the court’s standard of review of board actions, exculpation provisions, appraisal cases and disclosure-only settlements.

Board Composition and Succession Planning

Boards have to look at their composition and make an honest assessment of whether they collectively have the necessary experience and expertise to oversee the new opportunities and challenges facing their companies. Finding the right mix of people to serve on a company’s board of directors, however, is not necessarily an easy task, and not everyone will agree with what is “right.” According to Spencer Stuart’s 2015 Board Index, board composition and refreshment and director tenure were among the top issues that shareholders raised with boards. Because any perceived weakness in a director’s qualification could open the door for activist shareholders, boards should endeavor to have an optimal mix of experience, skills and diversity. In light of the importance placed on board composition, it is critical that boards have a long-term board succession plan in place. Boards that are proactive with their succession planning are able to find better candidates and respond faster and more effectively when an activist approaches or an unforeseen vacancy occurs.

Audit Committees

Averaging 8.8 meetings a year, audit continues to be the most time-consuming committee. [8] Audit committees are burdened not only with overseeing a company’s risks, but also a host of other responsibilities that have increased substantially over the years. Prioritizing an audit committee’s already heavy workload and keeping directors apprised of relevant developments, including enhanced audit committee disclosures, accounting changes and enhanced SEC scrutiny will be important as companies prepare for 2016.

Executive Compensation

Perennially in the spotlight, executive compensation will continue to be a hot topic for directors in 2016. But this year, due to the SEC’s active rulemaking in 2015, directors will have more to fret about than just say-on-pay. Roughly five years after the Dodd-Frank Wall Street Reform and Consumer Protection Act was enacted, the SEC finally adopted the much anticipated CEO pay ratio disclosure rules, which have already begun stirring the debate on income inequality and exorbitant CEO pay. The SEC also made headway on other Dodd-Frank regulations, including proposed rules on pay-for-performance, clawbacks and hedging disclosures. Directors need to start planning how they will comply with these rules as they craft executive compensation for 2016.

Proxy Access

2015 was a turning point for shareholder proposals seeking to implement proxy access, which gives certain shareholders the ability to nominate directors and include those nominees in a company’s proxy materials. During the 2015 proxy season, the number of shareholder proposals relating to proxy access, as well as the overall shareholder support for such proposals, increased significantly. Indeed, approximately 110 companies received proposals requesting the board to amend the company’s bylaws to allow for proxy access, and of those proposals that went to a vote, the average support was close to 54 percent of votes cast in favor, with 52 proposals receiving majority support. [9] New York City Comptroller Scott Springer and his 2015 Boardroom Accountability Project were a driving force, submitting 75 proxy access proposals at companies targeted for perceived excessive executive compensation, climate change issues and lack of board diversity. Shareholder campaigns for proxy access are expected to continue in 2016. Accordingly, it is paramount that boards prepare for and monitor developments in proxy access, including, understanding the provisions that are emerging as typical, as well as the role of institutional investors and proxy advisory firms.

[1] Activist Insight, “2015: The First Half in Numbers,” Activism Monthly (July 2015). (go back)

[2] Activist Insight, “Activist Investing—An Annual Review of Trends in Shareholder Activism,” p. 8. (2015). (go back)

[3] David Benoit and Kirsten Grind, “Activist Investors’ Secret Ally: Big Mutual Funds,” The Wall Street Journal (August 9, 2015). (go back)

[4] PwC’s 18th Annual Global CEO Survey 2015. (go back)

[5] Ponemon Institute’s 2015 Global Megatrends in Cybersecurity (February 2015). (go back)

[6] Kimberley S. Crowe, “Law in the Boardroom 2015,” Corporate Board Member Magazine (2nd Quarter 2015). See also, Protiviti, “Executive Perspectives on Top Risks for 2015.” (go back)

Au lendemain du référendum mené en Grande-Bretagne (GB), on peut se demander quelles sont les implications juridiques d’une telle décision. Celles-ci sont nombreuses ; plusieurs scénarios peuvent être envisagés pour prévoir l’avenir des relations entre la GB et l’Union européenne (UE).

Ben Perry de la firme Sullivan & Cromwell et Simon Witty de la firme Davis Polk & Wardwell ont exploré toutes les facettes légales de cette nouvelle situation dans deux articles parus récemment sur le site du Harvard Law School Forum on Corporate Governance.

Ce sont deux articles très approfondis sur les répercussions du Brexit. On doit admettre que le processus de retrait de l’UE est complexe, qu’il y a plusieurs modèles dont la GB peut s’inspirer (Suisse, Norvégien, Islandais, Liechtenstein), et que le vote n’a pas d’effets légaux immédiats. En fait, le processus de sortie et de renégociation peut durer trois ans !

Je vous invite à prendre connaissance de ces deux articles afin d’être mieux informés sur les principales avenues conséquentes au retrait de la GB de l’UE.

Le 25 juin, je vous ai déjà présenté l’article de Perry qui a suscité beaucoup d’intérêt (Brexit: Legal Implications).

Aujourd’hui, je vous présente le texte de l’article de Witty (The Legal Consequences of Brexit) qui met l’accent sur les répercussions prévisibles qu’aura ce retrait sur le marché des capitaux, les fusions et acquisitions, les différends liés aux contrats, les lois antitrusts, les services financiers et les mesures de taxation.

On June 23, 2016, the UK electorate voted to leave the European Union. The referendum was advisory rather than mandatory and does not have any immediate legal consequences. It will, however, have a profound effect. With any next steps being driven by UK and EU politics, it is difficult to predict the future of the UK’s relationship with the EU. This post discusses the process for Brexit, the alternative models of relationship that the UK may seek to adopt, and certain implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax.

The process for exiting the EU

The treaties that govern the EU expressly contemplate a member state leaving. Under Article 50 of the Treaty on European Union, the UK must notify the European Council of its intention to withdraw from the EU. Once notice is given, the UK has two years to negotiate the terms of its withdrawal. Any extension of the negotiation period will require the consent of all 27 remaining member states. When to invoke the Article 50 mechanism is, therefore, a strategically important decision. In a statement announcing his intention to resign as Prime Minister of the UK, David Cameron stated that the decision to provide notice under Article 50 to the European Council should be taken by the next Prime Minister, who is expected to be in place by October 2016.

Waving United Kingdom and European Union Flag

Any negotiated agreement will require the support of at least 20 out of the 27 remaining member states, representing at least 65% of the EU’s population, and the approval of the European Parliament. If no agreement is reached or no extension is agreed, the UK will automatically exit the EU two years after the Article 50 notice is given, even if no alternative trading model or arrangement has been negotiated. The UK continues to be a member of the EU in the interim period, subject to all EU legislation and rules.

Alternative models of relationship

It is not clear what model of relationship the UK will seek to negotiate with the EU. In the run-up to the referendum, a number of options were suggested. Politicians in favor of withdrawing from the EU did not coalesce around a specific alternative. It is, therefore, unclear what model will ultimately be followed or whether any of the models could be achieved through the Article 50 process. The principal options are outlined below.

The Norwegian model. The UK might seek to join the European Economic Area, as Norway has. The UK would have considerable access to the internal market, i.e., the association of European countries trading with each other without restrictions or tariffs, including in financial services. The UK would have limited access to the internal market for agriculture and fisheries; and it would not benefit from or be bound by the EU’s external trade agreements. In addition, the UK would have to make significant financial contributions to the EU and continue to allow free movement of persons. It would also have to apply EU law in a number of fields, but the UK would no longer participate in policymaking at the EU level, and would be excluded from participation in the European Supervisory Authorities, the key architects of secondary legislation in the financial services sphere. To adopt this model, the UK would require the agreement of all 27 remaining EU member states, plus Iceland, Liechtenstein and Norway.

Negotiated bilateral agreements. Like Switzerland, the UK might seek to enter into various bilateral agreements with the EU to obtain access to the internal market in specific sectors (rather than the market as a whole, which would be the case under the Norwegian model). This model would likely require the UK to accept some of the EU’s rules on free movement of persons and comply with particular EU laws. Again, the UK would not participate formally in the drafting of those laws. The UK would also have to make financial contributions to the EU. Negotiating these bilateral agreements would be a difficult and time-consuming process. Switzerland, for instance, has negotiated more than 100 individual agreements with the EU to cover market access in different sectors. As a result of its complexity, it is unclear whether the EU would work with the UK to negotiate this model within the Article 50 timeframe.

Customs union. A customs union is currently in place between the EU and Turkey in respect of trade in goods, but not services. Under this model, Turkey can export goods to the EU without having to comply with customs restrictions or tariffs. Its external tariffs are also aligned with EU tariffs. The UK might seek to negotiate a similar arrangement with the EU. Under such an arrangement, and unless separately negotiated, UK financial institutions (including UK subsidiaries of US holding companies) would not be able to provide financial and professional services into the EU on equal terms with EU member state firms. For example, the EU passporting regime would not be available, meaning UK firms would have to seek separate licensing in each EU member state to provide certain financial services. Furthermore, in areas where the UK would have access to the internal market, it would likely be required to enforce rules that are equivalent to those in the EU. The UK would not be required to make any financial contributions to the EU, nor would it be bound by the majority of EU law.

Free trade agreement. The UK might seek to negotiate a free trade agreement with the EU, which would cover goods and services. To do so, it may look to the agreement that was recently agreed between the EU and Canada after seven years of negotiations. This agreement removes tariffs in respect of trade in goods, as well as certain non-tariff barriers in respect of trade in goods and services. Although the UK would not be required to contribute to the EU budget, its exports to the EU would have to comply with the applicable EU standards.

WTO membership. Under this model, the UK would not have any preferential access to the internal market or the 53 markets with which the EU has negotiated free trade agreements. Tariffs and other barriers would be imposed on goods and services traded between the UK and the EU, although, under WTO rules, certain caps would apply on tariffs applicable to goods, and limits would be imposed on particular non-tariff barriers applicable to goods and services. The UK would no longer be required to make any financial contributions to the EU, nor would it be bound by EU laws (although it would have to comply with certain rules in order to trade with the EU).

Implications for UK legislation

Regardless of which model it adopts, the UK will no longer be required to apply some (if not all) EU legislation. The UK has implemented certain EU laws (generally, EU directives) via primary legislation that will continue to be part of English law, unless these are amended or repealed. Other EU laws (generally, EU regulations) have direct applicability in the UK without the need for implementation, which means that these laws would fall away once the UK withdraws from the EU, unless they are transposed into UK law. Finally, thousands of statutory instruments have been made pursuant to the European Communities Act 1972. If this act is repealed upon the UK’s withdrawal from the EU, then, unless transposed into UK law, these statutory instruments will cease to apply as well. Therefore, the UK will have to perform a complex exercise to determine which EU laws and EU-derived laws it wishes to retain, amend or repeal, driven in part by the nature of any agreement reached with the EU during exit negotiations.

How may Brexit affect you?

The UK’s withdrawal from the EU will impact countless areas of the economy. The following section discusses a number of Brexit’s potential implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax. The extent to which these areas will be affected by the UK’s withdrawal from the EU will depend on the model of relationship that the UK and the EU adopt following the Brexit negotiations.

Capital Markets

The financial markets will likely continue to be volatile, particularly during the Brexit negotiations. This may affect the timing of transactions or their ability to be consummated.

The EU Prospectus Directive, which has been transposed into UK law, governs the content, format, approval and publication of prospectuses throughout the EU. Following eventual Brexit, the UK may no longer be bound by the Prospectus Directive and, thus, may seek to amend its prospectus legislation. For example, the Prospectus Directive provides that a company incorporated in an EU member state must prepare a prospectus if it wishes to offer shares to the public and/or request that shares be admitted to trading in the EU, subject to certain exemptions. The UK may wish to expand these exemptions, so that more offers can be made in the UK without a prospectus. Significantly, the Prospectus Directive also provides for the passporting of prospectuses throughout the EU. This means that a company can use a prospectus that has been approved in one member state to offer shares in any other EU member state. Without this passporting regime, UK companies will have to have their prospectuses approved both in the UK and at least one other member state where they wish to offer their shares, which may be particularly costly and time-consuming if the UK amends, for instance, the content requirements for prospectuses following Brexit, so that these no longer align with those prescribed by the Prospectus Directive.

During the Brexit negotiations, transaction documents may need to include specific Brexit provisions, for example to address the uncertainty around the model of relationship to be adopted.

M&A

As a result of ongoing uncertainty around the future of the UK’s relationship with the EU, a number of transactions with a UK nexus may be affected pending the Brexit negotiations.

Share sale transactions generally are not subject to much EU law or regulation. Asset and business sales, however, may be more affected by Brexit. For example, the regulations that protect the rights of employees on a business transfer stem from a European directive. When the UK withdraws from the EU, it may no longer be bound by this directive, and, therefore, the UK may wish to amend or repeal the regulations.

Contractual Disputes and Enforcement

As a member of the EU, the UK is part of a framework for deciding jurisdiction in disputes, recognizing judgments of other member states (and having its own courts’ judgments recognized and enforced throughout the EU) and deciding the governing law of contracts. Following Brexit, the UK may no longer be part of this framework which may affect jurisdiction and governing law choices in transaction documents.

Anti-trust

Currently, mergers that fall within the scope of the EU Merger Regulation can receive EU-wide clearance, which means that they are not also required to be cleared by individual member states. Following Brexit, mergers with a UK nexus may need to be reviewed by the UK’s Competition and Markets Authority separately.

More generally, UK anti-trust legislation is currently based on, and interpreted in line with, EU law, including decisions of the European Commission and the European Court of Justice. Given that UK courts may no longer be required to interpret national law consistently with EU law once the UK withdraws from the EU, businesses face the prospect of having to comply with divergent systems.

Financial Services

Much of the UK’s financial services regulation is based on EU law. This includes legislation such as the Markets in Financial Instruments Directive (MiFID), which regulates investment services and trading venues, the European Market Infrastructure Regulation, which regulates the derivatives market, the Alternative Investment Fund Managers Directive, which regulates hedge funds and private equity, and the Capital Requirements Directive and the Capital Requirements Regulation, which together represent the EU’s implementation of the international Basel III accords for the prudential regulation of banks. The Bank Recovery and Resolution Directive (“BRRD”) has been implemented into UK law via the Banking Act 2009, so the fundamental bank resolution regime should initially survive Brexit. That said, substantial further EU legislative work is expected in this area to modify BRRD (e.g., in relation to the implementation of the TLAC standard), so it is possible that the regimes could diverge rapidly after Brexit. In general with financial services legislation, an assessment will need to be made whether to align with EU legislation or diverge; the greater the divergence, the more the dual burdens on cross-border firms.

As mentioned above, the UK will likely not be part of the European Supervisory Authorities framework and will have no influence in the development of primary or secondary EU legislation and guidance. The UK has been a significant force in the area of financial services legislation and has driven the introduction of, for instance, the BRRD. The UK’s withdrawal may impact the legislative agenda and ultimately the quality of the legislation produced.

Financial institutions established in EEA member states can obtain a “passport” that allows them to access the markets of other EEA member states without being required to set up a subsidiary and obtain a separate license to operate as a financial services institution in those member states. Following Brexit, UK financial services institutions, including subsidiaries of US and other non-EU parent companies, would no longer be able to benefit from passporting (unless the UK were to join the EEA pursuant to the Norway option described above).

Although the UK will likely remain a member of the EU for a substantial period while negotiations are ongoing, there are pressing questions as to how the UK will engage with the ongoing legislative processes that affect the UK financial services industry. There are a number of areas where framework legislation has been passed already, but key secondary legislation is being developed or revised. These areas include the complete overhaul of MiFID and the Payment Services Directive. Even before the UK leaves the EU, we can expect to see a diminished role for the UK Government, UK regulators and UK market participants in shaping the detailed policies and procedures in those areas.

We expect larger financial institutions in the UK, or those based outside the UK that have significant operations in the UK, will wish to contribute to the negotiation process between the EU and UK. In particular, to the extent a unique model for trading relationships is proposed, these institutions may wish to engage with policymakers to minimize disruption and damage to their EU business model.

Tax

The EU has influenced many areas of the UK’s tax system. In some cases, this has been through EU legislation which applies directly in the UK; in other cases, EU rules have been adopted through UK legislation (for example, the UK’s VAT legislation is based on principles which apply across the EU); and, in still other cases, decisions of the European Court of Justice have either influenced the development of UK tax rules, or have prevented the UK’s tax authority from enforcing aspects of the UK’s domestic tax code. This complicated backdrop means that the tax impact of Brexit will be varied and difficult to predict.

Areas to watch include the following:

Direct tax: although the UK has an extensive double tax treaty network, not all treaties provide for zero withholding tax on interest and royalty payments. Accordingly, corporate groups should consider the extent to which existing structures rely on EU rules such as the Parent-Subsidiary Directive or the Interest and Royalties Directive to secure tax efficient payment flows. Similarly, corporate groups proposing to undertake cross border reorganisations would need to consider the extent to which existing cross-EU border merger tax reliefs will survive intact. It should also be borne in mind that, even if Brexit occurs, the UK is likely to continue vigorously supporting the OECD’s BEPS initiative such that there may well be considerable constraints and complexities associated with locating businesses outside the UK.

VAT: although VAT is an EU-wide tax regime, it seems inconceivable that VAT will be abolished. However, it is likely that, over time, there will be a divergence between UK VAT rules and EU VAT rules, including as to input VAT recovery on supplies made to non-UK customers. Additionally, UK companies may lose the administrative benefit of the “one stop shop” for businesses operating in Europe.

Customs duty: if the UK left the customs union, exports to and imports from EU countries may become subject to tariffs or other import duties (as well as additional compliance requirements).

Transfer taxes: it seems that the UK would, at least in principle, be able to (re)impose the 1.5% stamp duty/stamp duty reserve tax charge in respect of UK shares issued or transferred into a clearance or depositary receipt system. Accordingly, the position for UK-headed corporate groups seeking to list on the NYSE or Nasdaq may become less certain.

______________________________

*Ben Perry is a partner in the London office of Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell publication.

*Simon Witty is a partner in the Corporate Department at Davis Polk & Wardwell LLP. This post is based on a Davis Polk memorandum.

Voici la troisième édition d’un document australien de KPMG, très bien conçu, qui répond clairement aux questions que tous les administrateurs de sociétés se posent dans le cours de leurs mandats.

Même si la publication est dédiée à l’auditoire australien de KPMG, je crois que la réalité réglementaire nord-américaine est trop semblable pour se priver d’un bon « kit » d’outils qui peut aider à constituer un Board efficace.

C’est un formidable document électronique interactif de 182 pages. Voyez la table des matières ci-dessous.

J’ai demandé à KPMG de me procurer une version française du même document mais il ne semble pas en exister.

Our business environment provides an ever-changing spectrum of risks and opportunities. The role of the director continues to be shaped by a multitude of forces including economic uncertainty, larger and more complex organisations, the increasing pace of technological innovation and digitisation along with a more rigorous regulatory environment.

At the same time there is more onus on directors to operate transparently and be more accountable for their actions and decisions.

To support directors in their challenging role, KPMG has created an interactive Directors’ Toolkit. Now in its third edition, this comprehensive guide is in a user friendly electronic format. It is designed to assist directors to more effectively discharge their duties and improve board performance and decision-making.

Key topics

Duties and responsibilities of a director

Oversight of strategy and governance

Managing shareholder and stakeholder expectations

Structuring an effective board and sub-committees

Enabling key executive appointments

Managing productive meetings

Better practice terms of reference, charters and agendas

Establishing new boards.

What’s New

In this latest version, we have included newly updated sections on:

Roles, responsibilities and expectations of directors of not-for-profit organisations

Risks and opportunities social media presents for directors and organisations

Key responsibilities of directors for overseeing investment governance, operations and processes.

Plusieurs administrateurs et formateurs me demandent de leur proposer un document de vulgarisation sur le sujet de la gouvernance. J’ai déjà diffusé sur mon blogue un guide à l’intention des journalistes spécialisés dans le domaine de la gouvernance des sociétés à travers le monde. Il a été publié par le Global Corporate Governance Forum et International Finance Corporation (un organisme de la World Bank) en étroite coopération avec International Center for Journalists.

Je n’ai encore rien vu de plus complet et de plus pertinent sur la meilleure manière d’appréhender les multiples problématiques reliées à la gouvernance des entreprises mondiales. La direction de Global Corporate Governance Forum m’a fait parvenir le document en français le 14 février.

Ce guide est un outil pédagogique indispensable pour acquérir une solide compréhension des diverses facettes de la gouvernance des sociétés. Les auteurs ont multiplié les exemples de problèmes d’éthiques et de conflits d’intérêts liés à la conduite des entreprises mondiales.

On apprend aux journalistes économiques — et à toutes les personnes préoccupées par la saine gouvernance — à raffiner les investigations et à diffuser les résultats des analyses effectuées. Je vous recommande fortement de lire le document, mais aussi de le conserver en lieu sûr car il est fort probable que vous aurez l’occasion de vous en servir.

Vous trouverez ci-dessous quelques extraits de l’introduction à l’ouvrage. Bonne lecture !

« This Guide is designed for reporters and editors who already have some experience covering business and finance. The goal is to help journalists develop stories that examine how a company is governed, and spot events that may have serious consequences for the company’s survival, shareholders and stakeholders. Topics include the media’s role as a watchdog, how the board of directors functions, what constitutes good practice, what financial reports reveal, what role shareholders play and how to track down and use information shedding light on a company’s inner workings. Journalists will learn how to recognize “red flags,” or warning signs, that indicate whether a company may be violating laws and rules. Tips on reporting and writing guide reporters in developing clear, balanced, fair and convincing stories.

Three recurring features in the Guide help reporters apply “lessons learned” to their own “beats,” or coverage areas:

– Reporter’s Notebook: Advise from successful business journalists

– Story Toolbox: How and where to find the story ideas

– What Do You Know? Applying the Guide’s lessons

Each chapter helps journalists acquire the knowledge and skills needed to recognize potential stories in the companies they cover, dig out the essential facts, interpret their findings and write clear, compelling stories:

What corporate governance is, and how it can lead to stories. (Chapter 1, What’s good governance, and why should journalists care?)

How understanding the role that the board and its committees play can lead to stories that competitors miss. (Chapter 2, The all-important board of directors)

Shareholders are not only the ultimate stakeholders in public companies, but they often are an excellent source for story ideas. (Chapter 3, All about shareholders)

Understanding how companies are structured helps journalists figure out how the board and management interact and why family-owned and state-owned enterprises (SOEs), may not always operate in the best interests of shareholders and the public. (Chapter 4, Inside family-owned and state-owned enterprises)

Regulatory disclosures can be a rich source of exclusive stories for journalists who know where to look and how to interpret what they see. (Chapter 5, Toeing the line: regulations and disclosure)

Reading financial statements and annual reports — especially the fine print — often leads to journalistic scoops. (Chapter 6, Finding the story behind the numbers)

Developing sources is a key element for reporters covering companies. So is dealing with resistance and pressure from company executives and public relations directors. (Chapter 7, Writing and reporting tips)

Each chapter ends with a section on Sources, which lists background resources pertinent to that chapter’s topics. At the end of the Guide, a Selected Resources section provides useful websites and recommended reading on corporate governance. The Glossary defines terminology used in covering companies and corporate governance ».

Voici les éléments de la proposition de Theresa May eu égard à la nouvelle gouvernance corporative de la Grande-Bretagne.

Ce texte est de Martin Lipton de la firme Wachtell, Lipton, Rosen & Katz. C’est un résumé des principaux points évoqués aujourd’hui par la ministre.

Bonne lecture !

Corporate Governance—A New Paradigm from the U.K.

1. Stakeholder, not shareholder, governance.

2. Board diversity: consumers and workers to be added.

3. Protection from takeover for national champions like Cadbury and AstraZeneca.

4. Binding, not advisory, say-on-pay.

5. Long-term, not short-term, business strategy.

6. Greater corporate transparency.

7. Stricter antitrust.

8. Higher taxes and crack down on tax avoidance and evasion.

9. It is not anti-business to suggest that big business needs to change. Better governance will help these companies to take better decisions, for their own long-term benefit and that of the economy overall.

Au lendemain du référendum mené en Grande-Bretagne (GB), on peut se demander quelles sont les implications juridiques d’une telle décision. Celles-ci sont nombreuses ; plusieurs scénarios peuvent être envisagés pour prévoir l’avenir des relations entre la GB et l’Union européenne (UE).

Ben Perry de la firme Sullivan & Cromwell et Simon Witty de la firme Davis Polk & Wardwell ont exploré toutes les facettes légales de cette nouvelle situation dans deux articles parus récemment sur le site du Harvard Law School Forum on Corporate Governance.

Ce sont deux articles très approfondis sur les répercussions du Brexit. On doit admettre que le processus de retrait de l’UE est complexe, qu’il y a plusieurs modèles dont la GB peut s’inspirer (Suisse, Norvégien, Islandais, Liechtenstein), et que le vote n’a pas d’effets légaux immédiats. En fait, le processus de sortie et de renégociation peut durer trois ans !

Je vous invite à prendre connaissance de ces deux articles afin d’être mieux informés sur les principales avenues conséquentes au retrait de la GB de l’UE.

Le 25 juin, je vous ai déjà présenté l’article de Perry qui a suscité beaucoup d’intérêt (Brexit: Legal Implications).

Aujourd’hui, je vous présente le texte de l’article de Witty (The Legal Consequences of Brexit) qui met l’accent sur les répercussions prévisibles qu’aura ce retrait sur le marché des capitaux, les fusions et acquisitions, les différends liés aux contrats, les lois antitrusts, les services financiers et les mesures de taxation.

On June 23, 2016, the UK electorate voted to leave the European Union. The referendum was advisory rather than mandatory and does not have any immediate legal consequences. It will, however, have a profound effect. With any next steps being driven by UK and EU politics, it is difficult to predict the future of the UK’s relationship with the EU. This post discusses the process for Brexit, the alternative models of relationship that the UK may seek to adopt, and certain implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax.

The process for exiting the EU

The treaties that govern the EU expressly contemplate a member state leaving. Under Article 50 of the Treaty on European Union, the UK must notify the European Council of its intention to withdraw from the EU. Once notice is given, the UK has two years to negotiate the terms of its withdrawal. Any extension of the negotiation period will require the consent of all 27 remaining member states. When to invoke the Article 50 mechanism is, therefore, a strategically important decision. In a statement announcing his intention to resign as Prime Minister of the UK, David Cameron stated that the decision to provide notice under Article 50 to the European Council should be taken by the next Prime Minister, who is expected to be in place by October 2016.

Waving United Kingdom and European Union Flag

Any negotiated agreement will require the support of at least 20 out of the 27 remaining member states, representing at least 65% of the EU’s population, and the approval of the European Parliament. If no agreement is reached or no extension is agreed, the UK will automatically exit the EU two years after the Article 50 notice is given, even if no alternative trading model or arrangement has been negotiated. The UK continues to be a member of the EU in the interim period, subject to all EU legislation and rules.

Alternative models of relationship

It is not clear what model of relationship the UK will seek to negotiate with the EU. In the run-up to the referendum, a number of options were suggested. Politicians in favor of withdrawing from the EU did not coalesce around a specific alternative. It is, therefore, unclear what model will ultimately be followed or whether any of the models could be achieved through the Article 50 process. The principal options are outlined below.

The Norwegian model. The UK might seek to join the European Economic Area, as Norway has. The UK would have considerable access to the internal market, i.e., the association of European countries trading with each other without restrictions or tariffs, including in financial services. The UK would have limited access to the internal market for agriculture and fisheries; and it would not benefit from or be bound by the EU’s external trade agreements. In addition, the UK would have to make significant financial contributions to the EU and continue to allow free movement of persons. It would also have to apply EU law in a number of fields, but the UK would no longer participate in policymaking at the EU level, and would be excluded from participation in the European Supervisory Authorities, the key architects of secondary legislation in the financial services sphere. To adopt this model, the UK would require the agreement of all 27 remaining EU member states, plus Iceland, Liechtenstein and Norway.

Negotiated bilateral agreements. Like Switzerland, the UK might seek to enter into various bilateral agreements with the EU to obtain access to the internal market in specific sectors (rather than the market as a whole, which would be the case under the Norwegian model). This model would likely require the UK to accept some of the EU’s rules on free movement of persons and comply with particular EU laws. Again, the UK would not participate formally in the drafting of those laws. The UK would also have to make financial contributions to the EU. Negotiating these bilateral agreements would be a difficult and time-consuming process. Switzerland, for instance, has negotiated more than 100 individual agreements with the EU to cover market access in different sectors. As a result of its complexity, it is unclear whether the EU would work with the UK to negotiate this model within the Article 50 timeframe.

Customs union. A customs union is currently in place between the EU and Turkey in respect of trade in goods, but not services. Under this model, Turkey can export goods to the EU without having to comply with customs restrictions or tariffs. Its external tariffs are also aligned with EU tariffs. The UK might seek to negotiate a similar arrangement with the EU. Under such an arrangement, and unless separately negotiated, UK financial institutions (including UK subsidiaries of US holding companies) would not be able to provide financial and professional services into the EU on equal terms with EU member state firms. For example, the EU passporting regime would not be available, meaning UK firms would have to seek separate licensing in each EU member state to provide certain financial services. Furthermore, in areas where the UK would have access to the internal market, it would likely be required to enforce rules that are equivalent to those in the EU. The UK would not be required to make any financial contributions to the EU, nor would it be bound by the majority of EU law.

Free trade agreement. The UK might seek to negotiate a free trade agreement with the EU, which would cover goods and services. To do so, it may look to the agreement that was recently agreed between the EU and Canada after seven years of negotiations. This agreement removes tariffs in respect of trade in goods, as well as certain non-tariff barriers in respect of trade in goods and services. Although the UK would not be required to contribute to the EU budget, its exports to the EU would have to comply with the applicable EU standards.