Voici les principaux résultats eu égard aux propositions des actionnaires lors des assemblées annuelles de 2016. Ce sont des données relatives aux grandes sociétés publiques américaines.

Je crois qu’il est intéressant d’avoir le pouls de l’évolution des propositions des actionnaires, car cela révèle l’état de la gouvernance dans les grandes corporations ainsi que le niveau d’activités des activistes.

Cet article, publié par Elizabeth Ising, associée et co-présidente de la « Securities Regulation and Corporate Governance practice group » de la firme Gibson, Dunn & Crutcher, est paru sur le forum de HLS hier.

L’auteure présente les résultats de manière très illustrée, sans porter de jugement.

Personnellement, je constate un certain essoufflement des propositions des actionnaires en 2016. Dans plusieurs cas cependant les entreprises ont remédié aux lacunes de gouvernance.

This post provides an overview of shareholder proposals submitted to public companies for 2016 shareholder meetings, including statistics, notable decisions from the staff of the Securities and Exchange Commission on no-action requests, and information about litigation regarding shareholder proposals. All shareholder proposal data in this post is as of June 1, 2016 unless otherwise indicated.

Submitted Shareholder Proposals

Overview

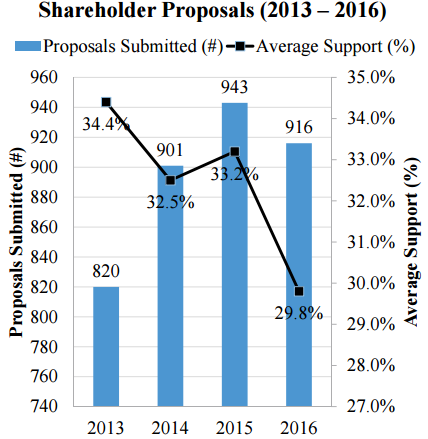

Fewer Proposals Submitted: According to ISS data, shareholders have submitted fewer shareholder proposals for 2016 meetings than they did for 2015 meetings.

However, the number of proposals submitted for 2016 meetings is still higher than the approximate number of proposals submitted for 2014 and 2013 meetings.

Support Declined: Average support for shareholder proposals is at its lowest in four years. [1]

Only 14.5% of proposals (61 proposals) voted on at 2016 meetings received support from a majority of votes cast, compared to 16.7% of proposals (75 proposals) at 2015 meetings.

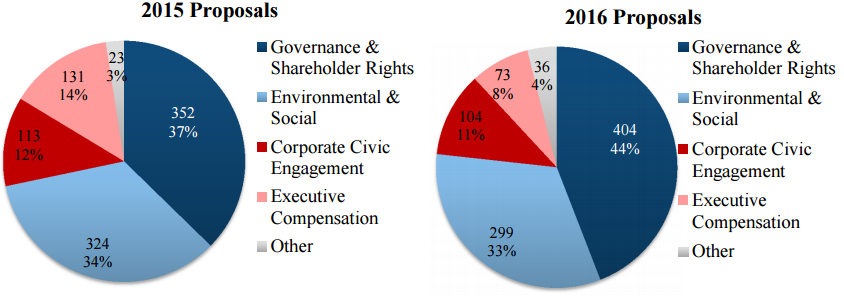

Focus Remains on Governance

Across five broad categories of shareholder proposals, the approximate number of proposals submitted for 2016 meetings (as compared to 2015 meetings) was as follows:

For the second year in a row, governance & shareholder rights proposals were the most frequently submitted proposals, largely due to the yet again unprecedented number of proxy access shareholder proposals submitted (201 proposals (or 21.9% of all proposals) submitted for 2016 meetings versus 108 proposals submitted for 2015 meetings).

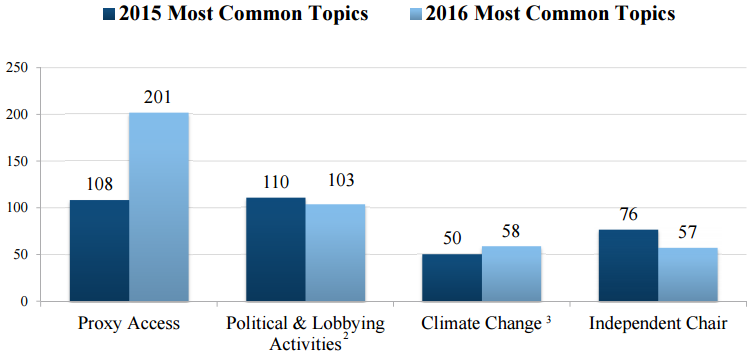

Proxy Access Proposals Continue to Dominate

The most common 2016 shareholder proposal topics, along with the approximate numbers of proposals submitted and as compared to the most common 2015 shareholder proposal topics, were [2][3]:

Most Active Proponents

Chevedden & Co.: As is typically the case, John Chevedden and shareholders associated with him (including James McRitchie) submitted by far the greatest number of shareholder proposals—approximately 227 for 2016 meetings.

Most of these proposals (66.6%) have either been voted on or are pending. Twenty-three percent have been omitted after obtaining relief through the SEC no-action process; another 7% have ultimately not been included in proxy statements or have not been properly presented at the meeting; and only 3.1% of these proposals have been withdrawn.

By way of comparison, shareholder proponents withdrew approximately 19.2% of the proposals submitted for 2016 meetings, up from approximately 17% of the proposals withdrawn for 2015 meetings.

NYC Pension Funds: This season once again saw a large number of proposals submitted by the New York City Comptroller on behalf of five New York City pension funds, which submitted or cofiled at least 79 proposals (as compared to 86 proposals submitted for 2015 meetings), including approximately 72 proxy access proposals, [4] as part of the Comptroller’s continuation of its “Boardroom Accountability Project” for 2016.

Only 34.6% of these proposals have either been voted on or are pending; most (55.6%) of these proposals have been withdrawn. The remainder (9.8%) have been omitted or not otherwise included in proxy statements.

Other Proponents

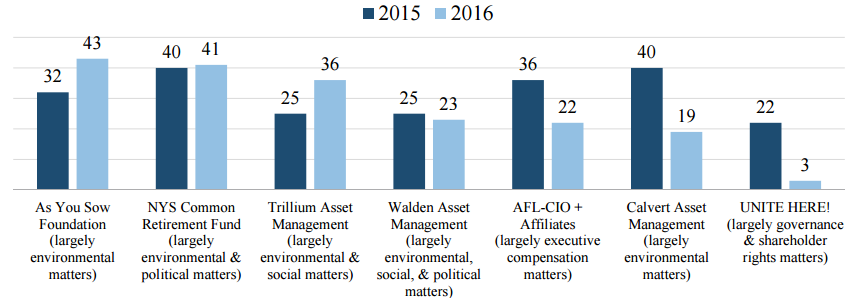

Some of the Same Players (But Not Everyone Returned in 2016): As was true for 2015 meetings, with the exception of Calvert Asset Management and UNITE HERE!, several of the same proponents that were reported to have submitted or co-filed at least 20 proposals each for 2015 meetings, did so again for 2016 meetings:

Same Subject Areas: As reflected in the chart above, the focus of these proponents remained largely consistent with their focus for 2015 meetings.

Public Pension Funds: In addition to the New York City and New York State pension funds, several other state pension funds submitted shareholder proposals as well:

California State Teachers’ Retirement System (18 proposals, largely focused on governance matters and climate change);

Connecticut Retirement Plans and Trust Funds (14 proposals, largely focused on governance, social, and political matters);

City of Philadelphia Public Employees Retirement System (10 proposals, largely focused on political and lobbying matters);

North Carolina Retirement Systems (two board diversity proposals);

California Public Employees’ Retirement System (one proxy access proposal); and

Firefighters’ Pension System of Kansas City, Missouri (one majority voting in director elections proposal).

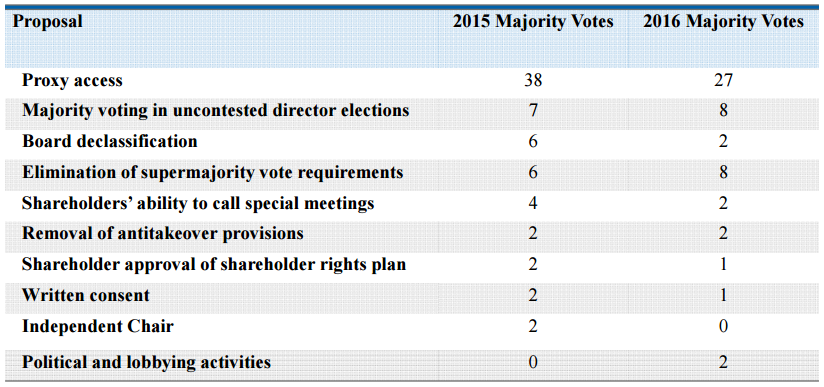

Shareholder Proposal Voting Results

Majority Voting in Director Elections Receives the Highest Support

The following are the principal topics addressed in proposals that received high shareholder support at a number of companies’ 2016 meetings:

Majority Voting in Uncontested Director Elections: Ten proposals voted on averaged 74.2% of votes cast, compared to 76.6% in 2015;

Amendment of Bylaws or Articles to Remove Antitakeover Provisions: Two proposals voted on averaged 70.6% of votes cast, compared to 79% in 2015;

Board Declassification: Three proposals voted on averaged 64.5% of votes cast, compared to 72.6% in 2015;

Elimination of Supermajority Vote Requirements: Thirteen proposals voted on averaged 59.6% of votes cast, compared to 53.0% in 2015;

Proxy Access: Fifty-eight proposals voted on averaged 48.7% of votes cast, compared to 54.6% in 2015;

Shareholder Ability to Call Special Meetings: Sixteen proposals voted on averaged 39.6% of votes cast, compared to 44.4% in 2015; and

Written Consent: Thirteen proposals voted on averaged 43.4% of votes cast, compared to 39.4% in 2015.

Majority Votes on Shareholder Proposals

The table below shows the principal topics addressed in proposals that received a majority of votes cast at a number of companies:

[1] As of June 1, 2016, voting results were available through the ISS databases for a total of 422 proposals. As a matter of practice, the vast majority of shareholder proposals submitted to companies for shareholder meetings are submitted under Rule 14a-8 rather than pursuant to companies’ advance notice bylaws. However, because the ISS data does not indicate whether a shareholder proposal has been submitted under Rule 14a-8 or under a company’s advance notice bylaws, it is possible that the ISS data includes voting results for shareholder proposals not submitted pursuant to Rule 14a-8. This discrepancy is likely to account for only a very small number of proposals. (go back)

[2] Includes all corporate civic engagement proposals, except proposals relating to charitable contributions (one submitted as of June 1, 2016 for 2016 meetings). (go back)

[3] Includes proposals relating to (i) reports on climate change; (ii) greenhouse gas emissions; and (iii) climate change action (i.e., proposals requesting increasing return of capital to shareholders in light of climate change risks). Note that climate change is a subtopic of the environmental and social category of proposals. (go back)

Voici une liste des billets en gouvernance les plus populaires publiés sur mon blogue au deuxième trimestre de 2016.

Cette liste de 15 billets constitue, en quelque sorte, un sondage de l’intérêt manifesté par des milliers de personnes sur différents thèmes de la gouvernance des sociétés. On y retrouve des points de vue bien étayés sur des sujets d’actualité relatifs aux conseils d’administration.

Que retrouve-t-on dans ce blogue et quels en sont les objectifs?

Ce blogue fait l’inventaire des documents les plus pertinents et les plus récents en gouvernance des entreprises. La sélection des billets est le résultat d’une veille assidue des articles de revue, des blogues et des sites web dans le domaine de la gouvernance, des publications scientifiques et professionnelles, des études et autres rapports portant sur la gouvernance des sociétés, au Canada et dans d’autres pays, notamment aux États-Unis, au Royaume-Uni, en France, en Europe, et en Australie.

Je fais un choix parmi l’ensemble des publications récentes et pertinentes et je commente brièvement la publication. L’objectif de ce blogue est d’être la référence en matière de documentation en gouvernance dans le monde francophone, en fournissant au lecteur une mine de renseignements récents (les billets) ainsi qu’un outil de recherche simple et facile à utiliser pour répertorier les publications en fonction des catégories les plus pertinentes.

Quelques statistiques à propos du blogue Gouvernance | Jacques Grisé

Ce blogue a été initié le 15 juillet 2011 et, à date, il a accueilli plus de 192000 visiteurs. Le blogue a progressé de manière tout à fait remarquable et, au30 juin 2016, il était fréquenté pardes milliers devisiteurs par mois. Depuis le début,j’aiœuvré à la publication de 1373billets.

En 2016, j’estime qu’environ 5000 personnes par mois visiteront le blogue afin de s’informer sur diverses questions de gouvernance. À ce rythme, on peut penser qu’environ 60000 personnesvisiteront le site du blogue en 2016.

On note que 80 % des billets sont partagés par l’intermédiaire de différents moteurs de recherche et 20 % par LinkedIn, Twitter, Facebook et Tumblr.

Voici un aperçu du nombre de visiteurs par pays :

Canada (64 %)

France, Suisse, Belgique (20 %)

Maghreb [Maroc, Tunisie, Algérie] (5 %)

Autres pays de l’Union européenne (3 %)

États-Unis [3 %]

Autres pays de provenance (5 %)

En 2014, le blogue Gouvernance | Jacques Grisé a été inscrit dans deux catégories distinctes du concours canadien Made in Blog [MiB Awards] : Business et Marketing et médias sociaux. Le blogue a été retenu parmi les dix [10] finalistes à l’échelle canadienne dans chacune de ces catégories, le seul en gouvernance. Il n’y avait pas de concours en 2015.

Vos commentaires sont toujours grandement appréciés. Je réponds toujours à ceux-ci.

N.B. Vous pouvez vous inscrire ou faire des recherches en allant au bas de cette page.

Bonne lecture !

Voici les Tops 15 du second trimestre de 2016 du blogue en gouvernance

Je crois que cet article intéressera tous les administrateurs siégeant à des conseils d’administration. Personnellement, je suis très heureux de constater que la démarche ait consisté en des rencontres avec des groupes d’administrateurs chevronnés.

Plusieurs messages très pertinents ressortent des rencontres. Ils sont regroupés selon les catégories suivantes :

La taille du conseil

La composition du conseil

La présidence du conseil

L’évaluation du conseil

Information et prise de décision

Les comités du conseil

Je vous invite à lire l’ensemble du document sur le site de l’IGOPP. Voici un extrait de cet article.

« Une longue expérience comme administrateur de sociétés mène souvent au constat que la qualité de la gouvernance et l’efficacité d’un conseil tiennent à des facteurs subtils, difficilement quantifiables, mais tout aussi importants, voire plus importants, que les aspects fiduciaires et formels.

Cette dimension informelle de la gouvernance prend forme et substance dans les échanges, les interactions sociales, l’encadrement des discussions, le style de leadership du président du conseil, dans tout ce qui se passe avant et après les réunions formelles ainsi qu’autour de la table au moment des réunions du conseil et de ses comités.

Cela est vrai pour tout type de sociétés, que ce soient une entreprise cotée en bourse, un organisme public, une société d’État, une coopérative ou un organisme sans but lucratif.

L’IGOPP estime que pour relever encore l’efficacité des conseils d’administration il est important de bien comprendre ce qui peut contribuer à une dynamique productive entre les membres d’un conseil.

Pourtant, alors que les études sur tous les aspects de la gouvernance foisonnent, cet aspect fait l’objet de peu de recherches empiriques, et ce pour une raison bien simple. Les conseils d’administration ne peuvent donner à des chercheurs un accès direct à leurs réunions ni à leur documentation en raison des contraintes de confidentialité.

Le professeur Richard Leblanc, grâce au réseau de son directeur de thèse de doctorat et co-auteur James Gillies, a pu, rare exception, observer un certain nombre de conseils d’administration en action. Ils ont publié en 2005 un ouvrage Inside the Boardroom, lequel propose une intéressante typologie des comportements dominants des membres de conseil au cours de réunions.

Depuis aucune autre étude empirique n’a été menée sur le sujet. D’ailleurs, l’ouvrage de Leblanc et Gillies, se limitant aux comportements observables lors de réunions formelles, ne nous éclairait que sur une partie du phénomène »

…

« L’IGOPP a voulu mieux comprendre cette dynamique et, si possible, proposer aux administrateurs et présidents de conseil des suggestions pouvant améliorer la qualité de la gouvernance.

L’IGOPP a donc invité des membres de conseil expérimentés et férus de gouvernance pour un échange sur cet enjeu. Les 14 personnes suivantes ont accepté promptement notre invitation et nous les en remercions chaleureusement:

Jacynthe Côté

Gérard Coulombe

Isabelle Courville

Paule Doré

Jean La Couture

Sylvie Lalande

John LeBoutillier

Brian Levitt

David L. McAusland

Marie-José Nadeau

Réal Raymond

Louise Roy

Guylaine Saucier

Jean-Marie Toulouse, qui a agi comme modérateur des discussions.

Collectivement, nos interlocuteurs siègent au sein de 75 conseils, dont 34 sont des sociétés ouvertes parmi lesquelles 14 ont leur siège hors Québec.

Nous avons tenu quatre sessions, chacune comptant un petit nombre d’administrateurs, de façon à ce que les discussions permettent à tous de s’exprimer pleinement.

Ces sessions furent riches en commentaires, observations pertinentes et suggestions utiles ».

Plusieurs messages très pertinents ressortent des rencontres. Ils sont regroupés selon les catégories suivantes :

La taille du conseil

La composition du conseil

La présidence du conseil

L’évaluation du conseil

Information et prise de décision

Les comités du conseil

En conclusion, l’auteur mentionne que « ce texte tente de rendre justice aux échanges entre les 14 administrateurs chevronnés qui ont participé à cette recherche de pistes d’amélioration de la dynamique des conseils d’administration et donc de la gouvernance de nos sociétés ».

Au lendemain du référendum mené en Grande-Bretagne (GB), on peut se demander quelles sont les implications juridiques d’une telle décision. Celles-ci sont nombreuses ; plusieurs scénarios peuvent être envisagés pour prévoir l’avenir des relations entre la GB et l’Union européenne (UE).

Ben Perry de la firme Sullivan & Cromwell et Simon Witty de la firme Davis Polk & Wardwell ont exploré toutes les facettes légales de cette nouvelle situation dans deux articles parus récemment sur le site du Harvard Law School Forum on Corporate Governance.

Ce sont deux articles très approfondis sur les répercussions du Brexit. On doit admettre que le processus de retrait de l’UE est complexe, qu’il y a plusieurs modèles dont la GB peut s’inspirer (Suisse, Norvégien, Islandais, Liechtenstein), et que le vote n’a pas d’effets légaux immédiats. En fait, le processus de sortie et de renégociation peut durer trois ans !

Je vous invite à prendre connaissance de ces deux articles afin d’être mieux informés sur les principales avenues conséquentes au retrait de la GB de l’UE.

Le 25 juin, je vous ai déjà présenté l’article de Perry qui a suscité beaucoup d’intérêt (Brexit: Legal Implications).

Aujourd’hui, je vous présente le texte de l’article de Witty (The Legal Consequences of Brexit) qui met l’accent sur les répercussions prévisibles qu’aura ce retrait sur le marché des capitaux, les fusions et acquisitions, les différends liés aux contrats, les lois antitrusts, les services financiers et les mesures de taxation.

On June 23, 2016, the UK electorate voted to leave the European Union. The referendum was advisory rather than mandatory and does not have any immediate legal consequences. It will, however, have a profound effect. With any next steps being driven by UK and EU politics, it is difficult to predict the future of the UK’s relationship with the EU. This post discusses the process for Brexit, the alternative models of relationship that the UK may seek to adopt, and certain implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax.

The process for exiting the EU

The treaties that govern the EU expressly contemplate a member state leaving. Under Article 50 of the Treaty on European Union, the UK must notify the European Council of its intention to withdraw from the EU. Once notice is given, the UK has two years to negotiate the terms of its withdrawal. Any extension of the negotiation period will require the consent of all 27 remaining member states. When to invoke the Article 50 mechanism is, therefore, a strategically important decision. In a statement announcing his intention to resign as Prime Minister of the UK, David Cameron stated that the decision to provide notice under Article 50 to the European Council should be taken by the next Prime Minister, who is expected to be in place by October 2016.

Waving United Kingdom and European Union Flag

Any negotiated agreement will require the support of at least 20 out of the 27 remaining member states, representing at least 65% of the EU’s population, and the approval of the European Parliament. If no agreement is reached or no extension is agreed, the UK will automatically exit the EU two years after the Article 50 notice is given, even if no alternative trading model or arrangement has been negotiated. The UK continues to be a member of the EU in the interim period, subject to all EU legislation and rules.

Alternative models of relationship

It is not clear what model of relationship the UK will seek to negotiate with the EU. In the run-up to the referendum, a number of options were suggested. Politicians in favor of withdrawing from the EU did not coalesce around a specific alternative. It is, therefore, unclear what model will ultimately be followed or whether any of the models could be achieved through the Article 50 process. The principal options are outlined below.

The Norwegian model. The UK might seek to join the European Economic Area, as Norway has. The UK would have considerable access to the internal market, i.e., the association of European countries trading with each other without restrictions or tariffs, including in financial services. The UK would have limited access to the internal market for agriculture and fisheries; and it would not benefit from or be bound by the EU’s external trade agreements. In addition, the UK would have to make significant financial contributions to the EU and continue to allow free movement of persons. It would also have to apply EU law in a number of fields, but the UK would no longer participate in policymaking at the EU level, and would be excluded from participation in the European Supervisory Authorities, the key architects of secondary legislation in the financial services sphere. To adopt this model, the UK would require the agreement of all 27 remaining EU member states, plus Iceland, Liechtenstein and Norway.

Negotiated bilateral agreements. Like Switzerland, the UK might seek to enter into various bilateral agreements with the EU to obtain access to the internal market in specific sectors (rather than the market as a whole, which would be the case under the Norwegian model). This model would likely require the UK to accept some of the EU’s rules on free movement of persons and comply with particular EU laws. Again, the UK would not participate formally in the drafting of those laws. The UK would also have to make financial contributions to the EU. Negotiating these bilateral agreements would be a difficult and time-consuming process. Switzerland, for instance, has negotiated more than 100 individual agreements with the EU to cover market access in different sectors. As a result of its complexity, it is unclear whether the EU would work with the UK to negotiate this model within the Article 50 timeframe.

Customs union. A customs union is currently in place between the EU and Turkey in respect of trade in goods, but not services. Under this model, Turkey can export goods to the EU without having to comply with customs restrictions or tariffs. Its external tariffs are also aligned with EU tariffs. The UK might seek to negotiate a similar arrangement with the EU. Under such an arrangement, and unless separately negotiated, UK financial institutions (including UK subsidiaries of US holding companies) would not be able to provide financial and professional services into the EU on equal terms with EU member state firms. For example, the EU passporting regime would not be available, meaning UK firms would have to seek separate licensing in each EU member state to provide certain financial services. Furthermore, in areas where the UK would have access to the internal market, it would likely be required to enforce rules that are equivalent to those in the EU. The UK would not be required to make any financial contributions to the EU, nor would it be bound by the majority of EU law.

Free trade agreement. The UK might seek to negotiate a free trade agreement with the EU, which would cover goods and services. To do so, it may look to the agreement that was recently agreed between the EU and Canada after seven years of negotiations. This agreement removes tariffs in respect of trade in goods, as well as certain non-tariff barriers in respect of trade in goods and services. Although the UK would not be required to contribute to the EU budget, its exports to the EU would have to comply with the applicable EU standards.

WTO membership. Under this model, the UK would not have any preferential access to the internal market or the 53 markets with which the EU has negotiated free trade agreements. Tariffs and other barriers would be imposed on goods and services traded between the UK and the EU, although, under WTO rules, certain caps would apply on tariffs applicable to goods, and limits would be imposed on particular non-tariff barriers applicable to goods and services. The UK would no longer be required to make any financial contributions to the EU, nor would it be bound by EU laws (although it would have to comply with certain rules in order to trade with the EU).

Implications for UK legislation

Regardless of which model it adopts, the UK will no longer be required to apply some (if not all) EU legislation. The UK has implemented certain EU laws (generally, EU directives) via primary legislation that will continue to be part of English law, unless these are amended or repealed. Other EU laws (generally, EU regulations) have direct applicability in the UK without the need for implementation, which means that these laws would fall away once the UK withdraws from the EU, unless they are transposed into UK law. Finally, thousands of statutory instruments have been made pursuant to the European Communities Act 1972. If this act is repealed upon the UK’s withdrawal from the EU, then, unless transposed into UK law, these statutory instruments will cease to apply as well. Therefore, the UK will have to perform a complex exercise to determine which EU laws and EU-derived laws it wishes to retain, amend or repeal, driven in part by the nature of any agreement reached with the EU during exit negotiations.

How may Brexit affect you?

The UK’s withdrawal from the EU will impact countless areas of the economy. The following section discusses a number of Brexit’s potential implications for the capital markets, mergers and acquisitions, contractual disputes and enforcement, anti-trust, financial services and tax. The extent to which these areas will be affected by the UK’s withdrawal from the EU will depend on the model of relationship that the UK and the EU adopt following the Brexit negotiations.

Capital Markets

The financial markets will likely continue to be volatile, particularly during the Brexit negotiations. This may affect the timing of transactions or their ability to be consummated.

The EU Prospectus Directive, which has been transposed into UK law, governs the content, format, approval and publication of prospectuses throughout the EU. Following eventual Brexit, the UK may no longer be bound by the Prospectus Directive and, thus, may seek to amend its prospectus legislation. For example, the Prospectus Directive provides that a company incorporated in an EU member state must prepare a prospectus if it wishes to offer shares to the public and/or request that shares be admitted to trading in the EU, subject to certain exemptions. The UK may wish to expand these exemptions, so that more offers can be made in the UK without a prospectus. Significantly, the Prospectus Directive also provides for the passporting of prospectuses throughout the EU. This means that a company can use a prospectus that has been approved in one member state to offer shares in any other EU member state. Without this passporting regime, UK companies will have to have their prospectuses approved both in the UK and at least one other member state where they wish to offer their shares, which may be particularly costly and time-consuming if the UK amends, for instance, the content requirements for prospectuses following Brexit, so that these no longer align with those prescribed by the Prospectus Directive.

During the Brexit negotiations, transaction documents may need to include specific Brexit provisions, for example to address the uncertainty around the model of relationship to be adopted.

M&A

As a result of ongoing uncertainty around the future of the UK’s relationship with the EU, a number of transactions with a UK nexus may be affected pending the Brexit negotiations.

Share sale transactions generally are not subject to much EU law or regulation. Asset and business sales, however, may be more affected by Brexit. For example, the regulations that protect the rights of employees on a business transfer stem from a European directive. When the UK withdraws from the EU, it may no longer be bound by this directive, and, therefore, the UK may wish to amend or repeal the regulations.

Contractual Disputes and Enforcement

As a member of the EU, the UK is part of a framework for deciding jurisdiction in disputes, recognizing judgments of other member states (and having its own courts’ judgments recognized and enforced throughout the EU) and deciding the governing law of contracts. Following Brexit, the UK may no longer be part of this framework which may affect jurisdiction and governing law choices in transaction documents.

Anti-trust

Currently, mergers that fall within the scope of the EU Merger Regulation can receive EU-wide clearance, which means that they are not also required to be cleared by individual member states. Following Brexit, mergers with a UK nexus may need to be reviewed by the UK’s Competition and Markets Authority separately.

More generally, UK anti-trust legislation is currently based on, and interpreted in line with, EU law, including decisions of the European Commission and the European Court of Justice. Given that UK courts may no longer be required to interpret national law consistently with EU law once the UK withdraws from the EU, businesses face the prospect of having to comply with divergent systems.

Financial Services

Much of the UK’s financial services regulation is based on EU law. This includes legislation such as the Markets in Financial Instruments Directive (MiFID), which regulates investment services and trading venues, the European Market Infrastructure Regulation, which regulates the derivatives market, the Alternative Investment Fund Managers Directive, which regulates hedge funds and private equity, and the Capital Requirements Directive and the Capital Requirements Regulation, which together represent the EU’s implementation of the international Basel III accords for the prudential regulation of banks. The Bank Recovery and Resolution Directive (“BRRD”) has been implemented into UK law via the Banking Act 2009, so the fundamental bank resolution regime should initially survive Brexit. That said, substantial further EU legislative work is expected in this area to modify BRRD (e.g., in relation to the implementation of the TLAC standard), so it is possible that the regimes could diverge rapidly after Brexit. In general with financial services legislation, an assessment will need to be made whether to align with EU legislation or diverge; the greater the divergence, the more the dual burdens on cross-border firms.

As mentioned above, the UK will likely not be part of the European Supervisory Authorities framework and will have no influence in the development of primary or secondary EU legislation and guidance. The UK has been a significant force in the area of financial services legislation and has driven the introduction of, for instance, the BRRD. The UK’s withdrawal may impact the legislative agenda and ultimately the quality of the legislation produced.

Financial institutions established in EEA member states can obtain a “passport” that allows them to access the markets of other EEA member states without being required to set up a subsidiary and obtain a separate license to operate as a financial services institution in those member states. Following Brexit, UK financial services institutions, including subsidiaries of US and other non-EU parent companies, would no longer be able to benefit from passporting (unless the UK were to join the EEA pursuant to the Norway option described above).

Although the UK will likely remain a member of the EU for a substantial period while negotiations are ongoing, there are pressing questions as to how the UK will engage with the ongoing legislative processes that affect the UK financial services industry. There are a number of areas where framework legislation has been passed already, but key secondary legislation is being developed or revised. These areas include the complete overhaul of MiFID and the Payment Services Directive. Even before the UK leaves the EU, we can expect to see a diminished role for the UK Government, UK regulators and UK market participants in shaping the detailed policies and procedures in those areas.

We expect larger financial institutions in the UK, or those based outside the UK that have significant operations in the UK, will wish to contribute to the negotiation process between the EU and UK. In particular, to the extent a unique model for trading relationships is proposed, these institutions may wish to engage with policymakers to minimize disruption and damage to their EU business model.

Tax

The EU has influenced many areas of the UK’s tax system. In some cases, this has been through EU legislation which applies directly in the UK; in other cases, EU rules have been adopted through UK legislation (for example, the UK’s VAT legislation is based on principles which apply across the EU); and, in still other cases, decisions of the European Court of Justice have either influenced the development of UK tax rules, or have prevented the UK’s tax authority from enforcing aspects of the UK’s domestic tax code. This complicated backdrop means that the tax impact of Brexit will be varied and difficult to predict.

Areas to watch include the following:

Direct tax: although the UK has an extensive double tax treaty network, not all treaties provide for zero withholding tax on interest and royalty payments. Accordingly, corporate groups should consider the extent to which existing structures rely on EU rules such as the Parent-Subsidiary Directive or the Interest and Royalties Directive to secure tax efficient payment flows. Similarly, corporate groups proposing to undertake cross border reorganisations would need to consider the extent to which existing cross-EU border merger tax reliefs will survive intact. It should also be borne in mind that, even if Brexit occurs, the UK is likely to continue vigorously supporting the OECD’s BEPS initiative such that there may well be considerable constraints and complexities associated with locating businesses outside the UK.

VAT: although VAT is an EU-wide tax regime, it seems inconceivable that VAT will be abolished. However, it is likely that, over time, there will be a divergence between UK VAT rules and EU VAT rules, including as to input VAT recovery on supplies made to non-UK customers. Additionally, UK companies may lose the administrative benefit of the “one stop shop” for businesses operating in Europe.

Customs duty: if the UK left the customs union, exports to and imports from EU countries may become subject to tariffs or other import duties (as well as additional compliance requirements).

Transfer taxes: it seems that the UK would, at least in principle, be able to (re)impose the 1.5% stamp duty/stamp duty reserve tax charge in respect of UK shares issued or transferred into a clearance or depositary receipt system. Accordingly, the position for UK-headed corporate groups seeking to list on the NYSE or Nasdaq may become less certain.

______________________________

*Ben Perry is a partner in the London office of Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell publication.

*Simon Witty is a partner in the Corporate Department at Davis Polk & Wardwell LLP. This post is based on a Davis Polk memorandum.

Aujourd’hui, je vous propose la lecture d’un article paru dans la revue European Journal of Risk Regulation (EJRR) qui scrute le scandale de Volkswagensous l’angle juridique, mais, surtout, sous l’angle des manquements à la saine gouvernance.

Le texte se présente comme un cas en gouvernance et en management. Celui-ci devrait alimenter les réflexions sur l’éthique, les valeurs culturelles et les effets des pressions excessives à la performance.

Vous trouverez, ci-dessous, l’intégralité de l’article avec le consentement de l’auteure. Je n’ai pas inclus les références, qui sont très abondantes et qui peuvent être consultées sur le site de la maison d’édition lexxion.

Like some other crises and scandals that periodically occur in the business community, the Volkswagen (“VW”) scandal once again highlights the devastating consequences of corporate misconduct, once publicly disclosed, and the media storm that generally follows the discovery of such significant misbehaviour by a major corporation. Since the crisis broke in September 2015, the media have relayed endless détails about the substantial negative impacts on VW on various stakeholder groups such as employees, directors, investors, suppliers and consumers, and on the automobile industry as a whole (1)

The multiple and negative repercussions at the economic, organizational and legal levels have quickly become apparent, in particular in the form of resignations, changes in VW’s senior management, layoffs, a hiring freeze, the end to the marketing of diesel-engined vehicles, vehicle recalls, a decline in car sales, a drop in market capitalization, and the launching of internal investigations by VW and external investigations by the public authorities. This comes in addition to the threat of numerous civil, administrative, penal and criminal lawsuits and the substantial penalties they entail, as well as the erosion of trust in VW and the automobile industry generally (2).

FILE PHOTO: Martin Winterkorn, chief executive officer of Volkswagen AG, reacts during an earnings news conference at the company’s headquarters in Wolfsburg, Germany, on Monday, March 12, 2012. Volkswagen said 11 million vehicles were equipped with diesel engines at the center of a widening scandal over faked pollution controls that will cost the company at least 6.5 billion euros ($7.3 billion). Photographer: Michele Tantussi/Bloomberg *** Local Caption *** Martin Winterkorn

A scandal of this extent cannot fail to raise a number of questions, in particular concerning the cause of the alleged cheating, liable actors, the potential organizational and regulatory problems related to compliance, and ways to prevent further misconduct at VW and within the automobile industry. Based on the information surrounding the VW scandal, it is premature to capture all facets of the case. In order to analyze inmore depth the various problems raised, we will have to wait for the findings of the investigations conducted both internally by the VW Group and externally by the regulatory authorities.

While recognizing the incompleteness of the information made available to date by VW and certain commentators, we can still use this documentation to highlight a few features of the case that deserve to be studied from the standpoint of corporate governance.

This Article remains relatively modest in scope, and is designed to highlight certain organizational factors that may explain the deviant behaviour observed at VW. More specifically, it submits that the main cause of VW’s alleged wrongdoing lies in the company’s ambitious production targets for the U.S. market and the time and budget constraints imposed on employees to reach those targets. Arguably, the corporate strategy and pressures exerted on VW’s employees may have led them to give preference to the performance priorities set by the company rather than compliance with the applicable legal and ethical standards. And this corporate misconduct could not be detected because of deficiencies in the monitoring and control mechanisms, and especially in the compliance system established by the company to ensure that legal requirements were respected.

Although limited in scope, this inquiry may prove useful in identifying means to minimize, in the future, the risk of similar misconduct, not only at VW but wihin other companies as well (3). Given the limited objectives of the Article, which focuses on certain specific organizational deficiencies at VW, the legal questions raised by the case will not be addressed. However, the Article will refer to one aspect of the law of business corporations in the United States, Canada and in the EU Member States in order to emphasize the crucial role that boards in publicly-held companies must exercise to minimize the risk of misconduct (4).

II. A Preliminary Admission by VW: Individual Misconduct by a few Software Engineers

When a scandal erupts in the business community following a case of fraud, embezzlement, corruption, the marketing of dangerous products or other deviant behaviour, the company concerned and the regulatory authorities are required to quickly identify the individuals responsible for the alleged misbehaviour. For example, in the Enron, WorldCom, Tyco and Adelphia scandals of the early 2000s, the investigations revealed that certain company senior managers had acted fraudulently by orchestrating accounting manipulations to camouflage their business’s dire financial situation (5).

These revelations led to the prosecution and conviction of the officers responsible for the corporations’ misconduct (6). In the United States, the importanace of identifying individual wrongdoers is clearly stated in the Principles of Federal Prosecutions of Business Organizations issued by the U.S. Department of Justice which provide guidelines for prosecutions of corporate misbehaviour (7). On the basis of a memo issued in 2015 by the Department of Justice (the “Yatesmemo”) (8), these principles were recently revised to express a renewed commitment to investigate and prosecute individuals responsible for corporate wrongdoing.While recognizing the importance of individual prosecutions in that context, the strategy is only one of the ways to respond to white-collar crime. From a prevention standpoint, it is essential to conduct a broader examination of the organizational environment in which senior managers and employees work to determine if the enterprise’s culture, values, policies, monitoring mechanisms and practices contribute or have contributed to the adoption of deviant behaviour (9).

In the Volkswagen case, the company’s management concentrated first on identifying the handful of individuals it considered to be responsible for the deception, before admitting few weeks later that organizational problems had also encouraged or facilitated the unlawful corporate behaviour. Once news broke of the Volkswagen scandal, one of VW’s officers quickly linked the wrongdoing to the actions of a few employees, but without uncovering any governance problems or misbehaviour at the VW management level (10).

In October 2015, the President and Chief Executive Officer of the VW Group in the United States, Michael Horn, stated in testimony before a Congressional Subcommittee: “[t]his was a couple of software engineers who put this for whatever reason » […]. To my understanding, this was not a corporate decision. This was something individuals did » (11). In other words, the US CEO considered that sole responsibility for the scandal lay with a handful of engineers working at the company, while rejecting any allegation tending to incriminate the company’s management.

This portion of his testimony failed to convince the members of the Subcommittee, who expressed serious doubts about placing sole blame on the misbehaviour of a few engineers, given that the problem had existed since 2009. As expressed in a sceptical response from one of the committee’s members: « I cannot accept VW’s portrayal of this as something by a couple of rogue software engineers […] Suspending three folks – it goes way, way higher than that » (12).

Although misconduct similar to the behaviour uncovered at Volkswagen can often be explained by the reprehensible actions of a few individuals described as « bad apples », the violation of rules can also be explained by the existence of organizational problems within a company (13).

III. Recognition of Organizational Failures by VW

In terms of corporate governance, an analysis of misbehaviour can highlight problems connected with the culture, values, policies and strategies promoted by a company’s management that have a negative influence on the behaviour of senior managers and employees. Considering the importance of the organizational environment in which these players act, regulators provide for several internal and external governance mechanisms to reduce the risk of corporate misbehaviour or to minimize agency problems (14). As one example of an internal governance mechanism, the law of business corporations in the U.S., Canada and the EU Member States gives the board of directors (in a one-tier board structure, as prescribed Under American and Canadian corporation law) and the management board and supervisory board (in a two tier board structure, as provided for in some EU Member States, such as Germany) a key role to play in monitoring the company’s activities and internal dealings (15). As part of their monitoring mission, the board must ensure that the company and its agents act in a diligent and honest way and in compliance with the regulations, in particular by establishing mechanisms or policies in connection with risk management, internal controls, information disclosure, due diligence investigation and compliance (16).

When analysing the Volkswagen scandal from the viewpoint of its corporate governance, the question to be asked is whether the culture, values, priorities, strategies and monitoring and control mechanisms established by the company’s management board and supervisory board – in other words « the tone at the top »-, created an environment that contributed to the emergence of misbehaviour (17).

In this saga, although the initial testimony given to the Congressional Subcommittee by the company’s U.S. CEO, Michael Horn, assigned sole responsibility to a small circle of individuals, « VW’s senior management later recognized that the misconduct could not be explained simply by the deviant behaviour of a few people, since the evidence also pointed to organizational problems supporting the violation of regulations (18). In December 2015, VW’s management released the following observations, drawn from the preliminary results of its internal investigation:

« Group Audit’s examination of the relevant processes indicates that the software-influenced NOx emissions behavior was due to the interaction of three factors:

– The misconduct and shortcomings of individual employees

– Weaknesses in some processes

– A mindset in some areas of the Company that tolerated breaches of rules » (19).

Concerning the question of process,VW released the following audit key findings:

« Procedural problems in the relevant subdivisions have encouraged misconduct;

Faults in reporting and monitoring systems as well as failure to comply with existing regulations;

IT infrastructure partially insufficient and antiquated. » (20)

More fundamentally, VW’s management pointed out at the same time that the information obtained up to that point on “the origin and development of the nitrogen issue […] proves not to have been a one-time error, but rather a chain of errors that were allowed to happen (21). The starting point was a strategic decision to launch a large-scale promotion of diesel vehicles in the United States in 2005. Initially, it proved impossible to have the EA 189 engine meet by legal means the stricter nitrogen oxide requirements in the United States within the required timeframe and budget » (22).

In other words, this revelation by VW’s management suggests that « the end justified the means » in the sense that the ambitious production targets for the U.S. market and the time and budget constraints imposed on employees encouraged those employees to use illegal methods in operational terms to achieve the company’s objective. And this misconduct could not be detected because of deficiencies in the monitoring and control mechanisms, and especially in the compliance system established by the company to ensure that legal requirements were respected. Among the reasons given to explain the crisis, some observers also pointed to the excessive centralization of decision-making powers within VW’s senior management, and an organizational culture that acted as a brake on internal communications and discouraged mid-level managers from passing on bad news (23).

IV. Organizational Changes Considered as a Preliminary Step

In response to the crisis, VW’s management, in a press release in December 2015, set out the main organizational changes planned to minimize the risk of similar misconduct in the future. The changes mainly involved « instituting a comprehensive new alignment that affects the structure of the Group, as well as is way of thinking and its strategic goals (24).

In structural terms, VW changed the composition of the Group’s Board of Management to include the person responsible for the Integrity and Legal Affairs Department as a board member (25). In the future, the company wanted to give « more importance to digitalization, which will report directly to the Chairman of the Board of Management, » and intended to give « more independence to brand and divisions through a more decentralized management (26). With a view to initiating a new mindset, VW’s management stated that it wanted to avoid « yes-men » and to encourage managers and engineers « who are curious, independent, and pioneering » (27). However, the December 2015 press release reveals little about VW’s strategic objectives: « Strategy 2025, with which Volkswagen will address the main issues for the future, is scheduled to be presented in mid 2016 » (28).

Although VW’s management has not yet provided any details on the specific objectives targeted in its « Strategy 2025 », it is revealing to read the VW annual reports from before 2015 in which the company sets out clear and ambitious objectives for productivity and profitability. For example, the annual reports for 2007, 2009 and 2014 contained the following financial objectives, which the company hoped to reach by 2018.

In its 2007 annual report,VW specified, under the heading « Driving ideas »:

“Financial targets are equally ambitious: for example, the Volkswagen Passenger Cars brand aims to increase its unit sales by over 80 percent to 6.6 million vehicles by 2018, thereby reaching a global market share of approximately 9 percent. To make it one of the most profitable automobile companies as well, it is aiming for an ROI of 21 percent and a return on sales before tax of 9 percent.” (29).

Under the same heading, VW stated in its 2009 annual report:

“In 2018, the Volkswagen Group aims to be the most successful and fascinating automaker in the world. […] Over the long term, Volkswagen aims to increase unit sales to more than 10 million vehicles a year: it intends to capture an above-average share as the major growth markets develop (30).

And in its 2014 annual report, under the heading « Goals and Strategies », VW said:

“The goal is to generate unit sales of more than 10 million vehicles a year; in particular, Volkswagen intends to capture an above-average share of growth in the major growth markets.”

Volkswagen’s aim is a long-term return on sales before tax of at least 8% so as to ensure that the Group’s solid financial position and ability to act are guaranteed even in difficult market periods (31).

Besides these specific objectives for financial performance, the annual reports show that the company’s management recognized, at least on paper, the importance of ensuring regulatory compliance and promoting corporate social responsibility (CSR) and sustainability (31). However, after the scandal broke in September 2015, questions can be asked about the effectiveness of the governance mechanisms, especially of the reporting and monitoring systems put in place by VW to achieve company goals in this area (33). In light of the preliminary results of VW’s internal investigation (34), as mentionned above, it seems that, in the organizational culture, the commitment to promote compliance, CSR and sustainability was not as strong as the effort made to achieve the company’s financial performance objectives.

Concerning the specific and challenging priorities of productivity and profitability established by VW’s management in previous years, the question is whether the promotion of financial objectives such as these created a risk because of the pressure it placed on employees within the organizational environment. The priorities can, of course, exert a positive influence and motivate employees to make an even greater effort to achieve the objectives (35). On the other hand, the same priority can exert a negative influence by potentially encouraging employees to use all means necessary to achieve the performance objectives set, in order to protect their job or obtain a promotion, even if the means they use for that purpose contravene the regulations. In other words, the employees face a « double bind » or dilemma which, depending on the circumstances, can lead them to give preference to the performance priorities set by the company rather than compliance with the applicable legal and ethical standards.

In the management literature, a large number of theoretical and empirical studies emphasize the beneficial effects of the setting of specific and challenging goals on employee motivation and performance within a company (36). However, while recognizing these beneficial effects, some authors point out the unwanted or negative side effects they may have.

As highlighted by Ordóñez, Schweitzer, Galinsky and Bazerman, specific goal setting can result in employees focusing solely on those goals while neglecting other important, but unstated, objectives (37). They also mention that employees motivated by « specific, challenging goals adopt riskier strategies and choose riskier gambles than do those with less challenging or vague goals (38). As an additional unwanted side effet, goal setting can encourage unlawful or unethical behaviour, either by inciting employees to use dishonest methods to meet the performance objectives targeted, or to “misrepresent their performance level – in other words, to report that they met a goal when in fact they fell short (39). Based on these observations, the authors suggest that companies should set their objectives with the greatest care and propose various ways to guard against the unwanted side effects highlighted in their study. This approach could prove useful for VW’s management which will once again, at some point, have to define its objectives and stratégies.

V. Conclusion

In the information released to the public after the emissions cheating scandal broke, as mentioned above, VW’s management quickly stated that the misconduct was directly caused by the individual misbehaviour of a couple of software engineers. Later, however, it admitted that the individual misconduct of a few employees was not the only cause, and that there were also organizational deficiencies within the company itself.

Although the VW Group’s public communications have so far provided few details about the cause of the crisis, the admission by management that both individual and organizational failings were involved constitutes, in our opinion, a lever for understanding the various factors that may have led to reprehensible conduct within the company. Based on the investigations that will be completed over the coming months, VW’s management will be in a position to identify more precisely the nature of these organizational failings and to propose ways to minimize the risk of future violations. During 2016, VW’s management will also announce the objectives and stratégies it intends to pursue over the next few years.

Quelles actions les conseils d’administration sont-ils susceptibles d’adopter dans les cas où leur PDG (CEO) a un comportement « limite » tout en n’étant pas illégal ?

L’article récemment publié par David Larcker* et Brian Tayan** dans la Harvard Business Review présente plusieurs exemples de situations où les CEO captent l’attention du public pour de mauvaises raisons !

Les CA sont les garants de la réputation de l’entreprise et, lorsque confrontés à des comportements fautifs de la part de leur CEO, ils doivent s’assurer de prendre toutes les mesures appropriées.

Les auteurs ont identifié 38 cas de comportements de CEO déviants qui ont un des échos révélateurs et qui ont généré des actions de gestion de crises. L’échantillon des cas retenus a été présenté en cinq grandes catégories :

(1) 34 % des cas impliquent des CEO qui ont menti à propos de leurs affaires personnelles ;

(2) 21 % des cas sont de nature sexuelle, impliquant un subordonné, un entrepreneur ou un consultant ;

(3) 16 % des cas concernent l’utilisation « questionnable » des fonds de l’entreprise ;

(4) 16 % des cas consistent en comportements grossiers ou abusifs ;

(5) 13 % des cas consistent en déclarations publiques qui ont des conséquences négatives sur les clients ou sur un groupe social en particulier.

Les résultats suivants ressortent clairement de l’étude :

– The impact of misbehavior on corporate reputation is significant and long-lasting.

– Shareholders generally (but do not always) react negatively to news of misconduct.

– Most companies take an active approach in responding to allegations of misconduct.

– Corporate punishment for CEO misbehavior is inconsistent.

– CEO misbehavior can reverberate across the organization.

For boards of directors, the lessons are clear: For better or worse, the CEO is often the face of the corporation. When the CEO engages in misconduct, the board has an obligation to investigate the matter, take proactive steps to ensure that it is properly dealt with, and — most important — ensure that corporate reputation, culture, and long-term performance are not damaged.

Je vous invite à lire plus à fond les répercussions de ces mauvais comportements sur la réputation de l’organisation ainsi que les décisions prises par les CA dans chaque situation.

Bonne lecture ! Vos commentaires sont les bienvenus.

Most boards of directors know what to do when their CEO is accused of illegal activity. They conduct an independent investigation, and if the allegations are verified, they take corrective action. In most cases, the CEO is terminated.

It is much less obvious what actions the board should take when the CEO is accused of behavior that is questionable but not illegal. For example, if the CEO makes controversial public statements, has personal relations with an employee or contractor, or develops a reputation for being rude, overbearing, or verbally combative, the board must decide what merits investigation. It must also decide whether to address matters publicly or privately. These decisions become even more important when CEO misbehavior is picked up by the media, bringing unwanted public attention that can have an impact on the organization and its reputation.

To examine how corporations handle allegations of CEO misbehavior, we conducted an extensive review of news media between 2000 and 2015. We identified 38 incidents where a CEO’s behavior garnered a meaningful level of media coverage (defined as more than 10 unique news references). We categorized these incidents as follows:

34% involved reports of a CEO lying to the board or shareholders over personal matters, such as a drunk driving offense, undisclosed criminal record, falsification of credentials, or other behavior.

21% involved a sexual affair or relations with a subordinate, contractor, or consultant.

16% involved CEOs making use of corporate funds in a manner that is questionable but not strictly illegal.

16% involved CEOs engaging in objectionable personal behavior or using abusive language.

13% involved CEOs making public statements that are offensive to customers or social groups.

Examining these incidents in detail, five main findings stood out:

The impact of misbehavior on corporate reputation is significant and long-lasting. The incidents that we identified were cited in over 250 news stories each, on average. Furthermore, media coverage was persistent, with references made to the CEO’s actions up to an average of 4.9 years after initial occurrence. For example, news stories today continue to reference former American Apparel CEO Dov Charney’s odd behavior of walking around the company’s offices in his underwear, even though it was first reported over 10 years ago. Boards should not expect allegations of misbehavior to disappear quickly.

Shareholders generally (but do not always) react negatively to news of misconduct. Among the companies in our sample, share prices declined by a market-adjusted 3.1% (1.1% median) over the three-day trading period around the initial news story. For example, Hewlett-Packard stock fell almost 9% following reports that former CEO Mark Hurd had a personal relationship with a female contractor. However, shareholder reactions are not uniformly negative. Of the 38 companies in our sample. 11 exhibited positive stock price returns when CEO misbehavior made the news. Perhaps unexpectedly, there is no discernible relationship between the type of behavior and stock price reaction.

Most companies take an active approach in responding to allegations of misconduct. In 84% of cases, the company issued a press release or formal statement on the matter. In 71% of cases, a spokesperson provided direct commentary to the press. Board members were much less likely to speak to the media, making direct comments only 37% of the time. In over half of cases (55%), the board of directors was known to initiate an independent review or investigation. The board is most likely to announce an independent review in cases of potential financial misconduct. However, the willingness of an individual director to discuss the matter directly with the press does not appear to be associated with the type of behavior involved or the “severity” of the CEO’s actions.

Corporate punishment for CEO misbehavior is inconsistent. In 58% of incidents, the CEO was eventually terminated for his or her actions. Questionable financial practices was the only category of behavior that almost uniformly resulted in termination; all other behaviors resulted in both outcomes (termination and retention) across our sample. Even behavior as straightforward as falsifying information on a resume was treated inconsistently by different boards. In a third of cases (32%), the board took actions other than termination in response to CEO misconduct, such as stripping the CEO of the chair title, removing the CEO from the board, amending the corporate code of conduct, reducing or eliminating the CEO’s bonus, other director resignation, and other changes to board structure or composition.

CEO misbehavior can reverberate across the organization. Approximately one-third of companies faced additional fallout from the CEO’s actions, including loss of a major client, federal investigation, shareholder or federal lawsuit, or shareholder action such as a proxy battle. Forty-five percent of companies in the sample experienced a significant unrelated governance issue following the event, such as an accounting restatement, unrelated lawsuit, shareholder action, or bankruptcy. As for the CEOs themselves, three were reported to resign from other boards because of their actions. Two CEOs who were terminated were subsequently rehired by the same company. We found that many continued in their position or were hired by other corporations or investment groups; otherwise there was no notable news of what happened to them professionally.

For boards of directors, the lessons are clear: For better or worse, the CEO is often the face of the corporation. When the CEO engages in misconduct, the board has an obligation to investigate the matter, take proactive steps to ensure that it is properly dealt with, and — most important — ensure that corporate reputation, culture, and long-term performance are not damaged.

David Larcker* is the James Irvin Miller Professor of Accounting and Senior Faculty at the Rock Center for Corporate Governance at Stanford University. He is a co-author of the books Corporate Governance Matters and A Real Look at Real World Corporate Governance.

Brian Tayan** is a researcher at the Rock Center for Corporate Governance at Stanford University. He is a co-author of the books Corporate Governance Matters and A Real Look at Real World Corporate Governance.

Il existe peu de recherche sur les stratégies utilisées par les entreprises publiques (dans ce cas-ci l’indice S&P 1500) eu égard à l’adoption des réseaux sociaux pour divulguer de l’information aux investisseurs.

L’étude dont il est ici question a été réalisée par une équipe de chercheurs et elle a été publiée dans le Harvard Law School Forum par Matteo Tonello*, directeur du Conference Board. Elle montre que plus de la moitié des entreprises utilisent Twitter pour relayer différents types d’informations (principalement de nature financière) auprès d’investisseurs actuels ou potentiels.

Tout le monde reconnaît l’impact phénoménal des médias sociaux pour communiquer nos messages, instantanément, à l’échelle planétaire ; l’étude démontre que les entreprises ont également pris le virage et qu’elles utilisent abondamment les médias sociaux dans toutes les sphères des activités relatives aux affaires.

Mais, comment les entreprises utilisent-elles les réseaux sociaux pour communiquer plus efficacement leurs résultats financiers auprès de leurs investisseurs ? Comment ces entreprises profitent-elles des médias sociaux pour améliorer leur image de marque ? Quelles sont les conséquences non anticipées de la diffusion d’information financière par l’intermédiaire de Twitter ?

Avec les médias traditionnels, les organisations sont très dépendantes des services de presse, si bien que les informations financières ne sont généralement pas bien ciblées et que les entreprises ne savent pas si les investisseurs actuels ou futurs ont bien reçu l’information.

Les auteurs recommandent l’utilisation de courts messages dans un média tel que Twitter, avec un lien vers un communiqué de presse ou vers le site de l’entreprise. La recherche montre également que la divulgation de l’information financière aux investisseurs en utilisant ce moyen peut engendrer une perte de contrôle du message !

Aussi, l’étude montre que les organisations sont moins susceptibles de divulguer leurs résultats financiers via Twitter lorsque les profits ne satisfont pas les attentes des analystes. Les entreprises utilisent essentiellement Twitter pour divulguer les bonnes nouvelles. Cela ne surprendra personne, mais ce comportement illustre le manque de transparence de plusieurs entreprises.

Également, l’étude montre que les grands investisseurs réagissent plus rapidement aux tweets liés aux résultats financiers.

Enfin, les résultats indiquent que les retweets d’informations négatives ont une portée virale et qu’ils génèrent une couverture négative dans les médias traditionnels.

Si vous souhaitez approfondir vos connaissances sur la diffusion d’informations par les entreprises publiques via les médias sociaux, je vous invite à lire ce court extrait de l’étude.

While companies devote considerable effort to creating and managing social media presences, little is known about how they use social media to communicate financial information to investors. This report examines the use of social media by S&P 1500 companies to disseminate financial information and the response from investors and traditional media. The findings show that companies use social media to overcome a perceived lack of traditional media attention and that social media usage improves the company’s information environment. There is also evidence that, in contrast with other types of company communications, the beneficial effects of social media on the company’s information environment are offset when the investor-focused social media communications are disseminated by other social media users. The findings are relevant for managers and boards establishing corporate social media disclosure policies, since they suggest that companies may benefit from developing different approaches to disseminating positive versus negative earnings news.

Social media has transformed communications in many sectors of the US economy. It is now used for disaster preparation and emergency response, security at major events, and public agencies are researching new uses in geolocation, law enforcement, court decisions, and military intelligence. Internationally, social media is credited for organizing political protests across the Middle East and a revolution in Egypt. In the business world, social media has revolutionized sales and marketing practices and developed into a powerful recruiting and networking channel.

Conventionally, if a company wanted to publicize investor-related information such as an earnings announcement, it would do so by sending a press release to intermediaries such as newswire services, equity research databases, and brokerage firms. A company would not know if or when any of its existing or prospective investors received the information. In contrast, with social media platforms such as Twitter, a company can send one or more short messages directly to a known number of followers with a link to a press release on its corporate website. As such, a company can use Twitter to target its news dissemination, increase the speed and flexibility of the news dissemination, and reduce information acquisition costs for its investors and the traditional media outlets that follow it.

Little research exists, however, on how firms use social media to communicate financial information to investors and how investors respond to information disseminated through social media, despite firms devoting considerable effort to creating and managing social media presences directed at investors. While social media is generally viewed as an opportunity to improve investor communications and increase visibility, the authors hypothesize that disseminating investor communications via social media could also result in the company not retaining full control over its financial communications. This concern stems from the viral nature of social media—even though social media allows a company to connect more easily with its investors, it also allows investors to connect more easily with the company, with each other, and with individuals who do not directly follow the company and are likely less informed about the company’s prior financial communications. As a result, a company’s investor communications via social media can potentially spread to uniformed individuals in a way that creates adverse consequences for the company.

The Adoption Rate of Social Media to Disseminate Information to Investors

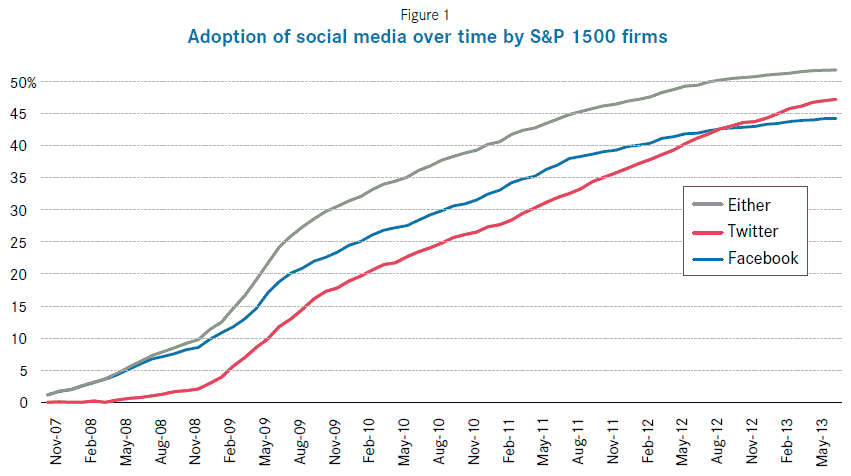

To collect data on social media usage, the authors identify whether each company in the S&P 1500 Index had a social media presence on Twitter, Facebook, LinkedIn, Pinterest, YouTube, and Google+ as of January 2013 by visiting each corporate website and looking for icons or links to the company’s social media sites. Twitter and Facebook are the two most frequently adopted social media platforms for corporations. The data show that adoption of Twitter and Facebook exceeds 47 percent and 44 percent, respectively, and is highest for customer-facing industries such as meals, retail, books and services (each over 65 percent) and lowest for industrial sectors such as oil (roughly 20 percent) and steel (roughly 14 percent). Corporate adoption is much lower for the other social media platforms, suggesting that they are less conducive for delivering typical corporate communications.

The authors also collect data on when companies joined Twitter or Facebook by searching for the earliest tweets or posts. The time trend in corporate social media adoption for Facebook and Twitter is illustrated in Figure 1. The earliest adopters of Facebook joined in November 2007 and the first set of firms to create Twitter accounts did so in May 2008. By early 2013, the corporate adoption rate of Twitter surpassed the rate for Facebook. By the end of the data collection period, 51 percent of the S&P 1500 companies had adopted one or the other, with Twitter appearing to edge out Facebook slightly as the preferred social media platform for companies.

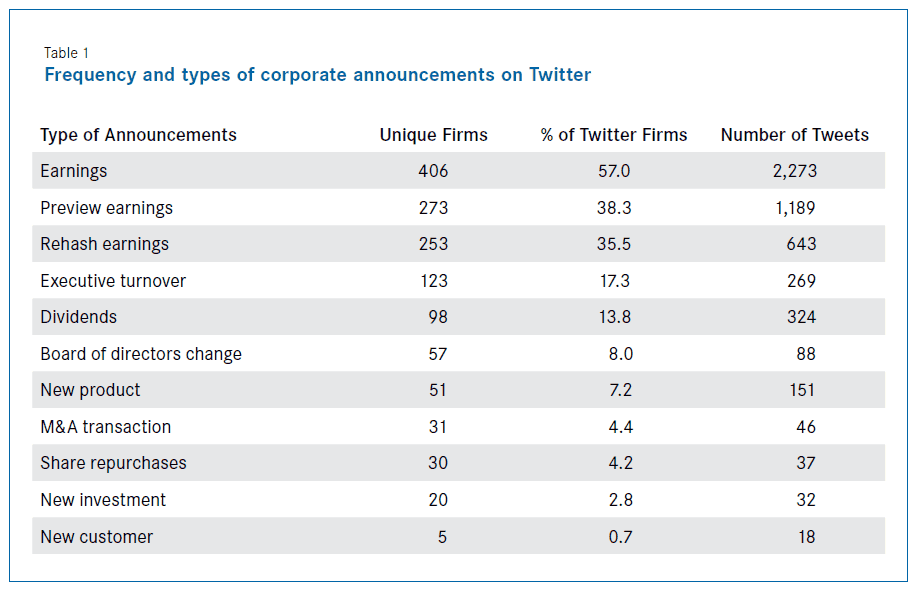

Since social media adoption does not necessarily imply that social media is used to disseminate information to investors, which is the focus of the study, the next step is to analyze what types of investor-focused information are disseminated over social media. Since the data suggest that Twitter is the preferred social media platform, it is the focus of this analysis. Quarterly earnings-related tweets are the most prevalent type of investor-focused tweets, far outnumbering tweets related to executive turnover, dividends, board of directors, and even new products and customers. The frequency of each type of investor-related tweet is summarized in Table 1.

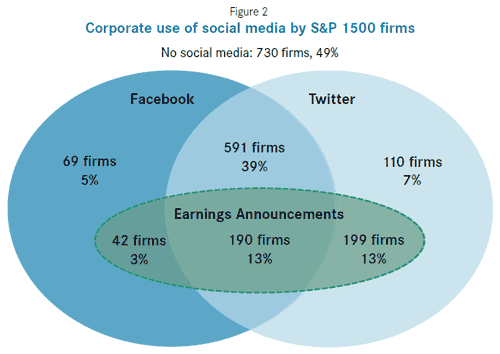

The number of firm-quarters with earnings announcements on Facebook (5.7 percent) is approximately half the number on Twitter (11.8 percent), suggesting that the preference for Twitter is even stronger when it comes to earnings news. An overview of the corporate use of Twitter and Facebook is illustrated in Figure 2.

Which Companies Use Social Media and What Is The Capital Market Response?

The consequences of social media usage are identified by combining the detailed information on Twitter usage with other data on stock market outcomes and financial statement data. Using Twitter, rather than other social media data, is advantageous because 1) earnings announcements have been shown in prior work to be of first-order importance to investors, 2) the information content of earnings announcements can be controlled for more effectively than the information content of other financial disclosures, and 3) the precise time that earnings announcements were disseminated through Twitter can be identified. The analyses address four related research questions, which are described in the following subsections:

What Types of Companies Disseminate Earnings through Social Media?

An investigation of the factors associated with the choice to disseminate earnings news through Twitter finds that companies that tweet earnings have less traditional media coverage and tend to issue more press releases than those that do not use Twitter. These findings suggest that companies use social media along with other firm-initiated communications in response to a perceived lack of traditional media coverage. The analysis also shows that larger companies are more likely to use Twitter to disseminate earnings news, which is contrary to the notion that smaller companies benefit more from using social media.

Are Companies Strategic in their use of Social Media?

The authors investigate whether companies strategically disseminate earnings news using Twitter by examining whether there is differential usage of Twitter based on the direction of the earnings news (i.e., positive versus negative earnings news). They find that companies are less likely to disseminate earnings news through Twitter when the earnings miss the consensus forecast and the magnitude of the miss is larger. When the sample is split between companies that consistently use Twitter versus those that do not, these results are driven by this latter group. In other words, it appears that there is a subset of companies that are sporadic in their Twitter usage, and that these companies use Twitter strategically to disseminate positive earnings news.

How does the Capital Market Respond to the Corporate Use of Social Media?

The capital market response to social media dissemination is investigated by looking at intra-day and three-day changes in capital market measures related to price, volume, and spreads. There is a reduction in bid-ask spreads when the company tweets earnings news and when more followers receive the earnings announcement tweet. [1]

Modest price- and volume-based responses are found to earnings announcements disseminated over Twitter during three-day earnings announcement windows. However, when short-window intraday tests focused on companies that tweet earnings news during market hours are used, both trading volume and trade size respond to earnings tweets. There is a significant increase in the mean and median abnormal volume, primarily due to an increase in large trades. Therefore, while social media is commonly viewed as a dissemination channel that provides timely access to information for all investors, the results suggest that larger investors react more quickly to earnings-related tweets.

Does Social Media Influence Traditional Media Coverage?

The authors investigate whether there are adverse consequences to the company from non-firm initiated social media disseminations by examining whether retweets negatively affect the company’s information environment and its coverage by traditional media. In contrast with the evidence for tweets, there is an increase in information asymmetry when the company’s earnings announcement tweets are retweeted to individuals who do not follow the company (i.e., the follower’s followers). Media coverage is also adversely affected by retweet activity. While more retweets are associated with more coverage in traditional media, this association is entirely attributable to negative media coverage. This finding suggests that retweets of earnings information increase negative media coverage, but have no effect on positive media coverage.

Conclusion

The findings shows that the usage of social media by corporations has grown dramatically over a relatively short period of time, from less than 5 percent of S&P 1500 companies in 2008 to more than 50 percent in 2013. This trend suggests that social media usage for communicating with investors has the potential to become an integral part of many companies’ disclosure policies. The findings show that even in the absence of the Securities and Commission’s approval of social media as a channel for investor communication, companies used it to disseminate a variety of information, including earnings news, board and executive changes, new contracts, and dividends.

Overall, the findings demonstrate that social media usage improves the company’s information environment, consistent with the notion that it improves investor communications. However, the benefits are offset when the company’s disclosures are disseminated by other social media users, consistent with the notion that there are potential adverse consequences to the company’s information environment that derive from the viral nature of social media. This finding suggests that an appropriate social media policy for investor communications likely differs from social media usage for other business purposes, such as marketing campaigns, in which companies often want to generate viral reactions to social media dissemination. The results also suggest that companies that adopt social media disclosure policies benefit from developing different approaches to disseminating positive versus negative earnings news. These conclusions are relevant for companies, managers, and boards of directors that are establishing social media disclosure policies.

Endnotes:

[1] The bid-ask spread is the difference between the price that someone is willing to pay for a security at a specific point in time (the bid) and the price at which someone is willing to sell (the ask).